AL3: New $2.6M US Navy submarine parts order... A week after $9.9M military shipbuilding order.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 6,378,029 AL3 Shares at the time of publishing this article. The Company has been engaged by AL3 to share our commentary on the progress of our Investment in AL3 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

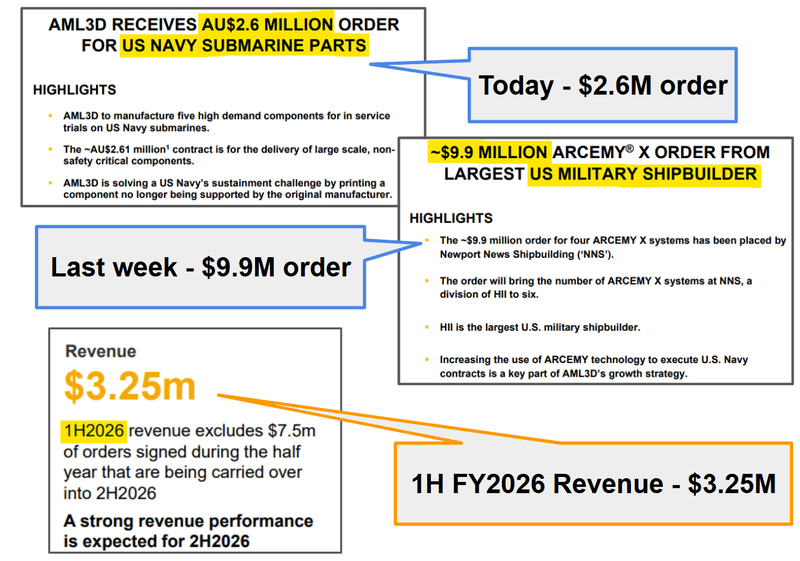

That’s now a total of $12.5M in new orders from the US defence industrial complex for our Investment AML3D (ASX:AL3) in the last 9 days.

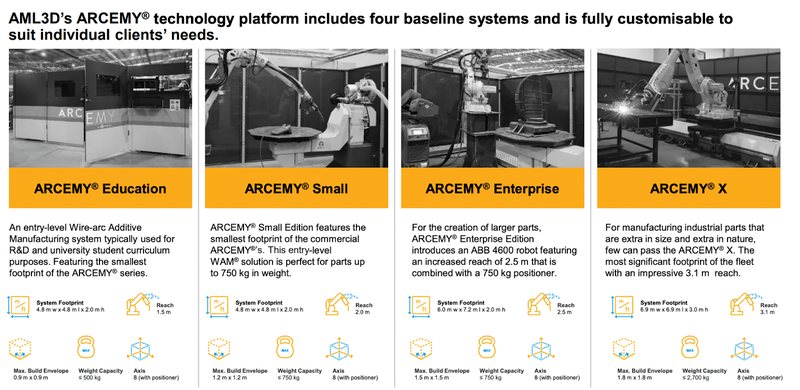

AL3 sells 3D printing systems that produce complex parts using metals - faster, stronger and cheaper than traditional casting and forging.

AL3’s strategy has been to sell into the US defence and US military ship building sector.

(from their recently opened facility in Ohio, USA)

And the US has made it an urgent priority to rebuild their domestic ship and submarine manufacturing capability (more on this in a second).

Last week, AL3 announced a $9.9M order from America’s largest military shipbuilder.

Today it's a $2.6M parts order for the US Navy submarine program.

(The US Navy says it aims to reach a production rate of three submarines per year by 2028, up from a current average of 1.2 subs every year - and building a new submarine is no joke)

Combined, these two new orders from the last 9 days are more than FOUR times AL3’s ~$3.2M last reported half-yearly revenues.

AL3’s US strategy has already delivered US Defense related contracts in excess of AU$30M, and revenue continues to accelerate.

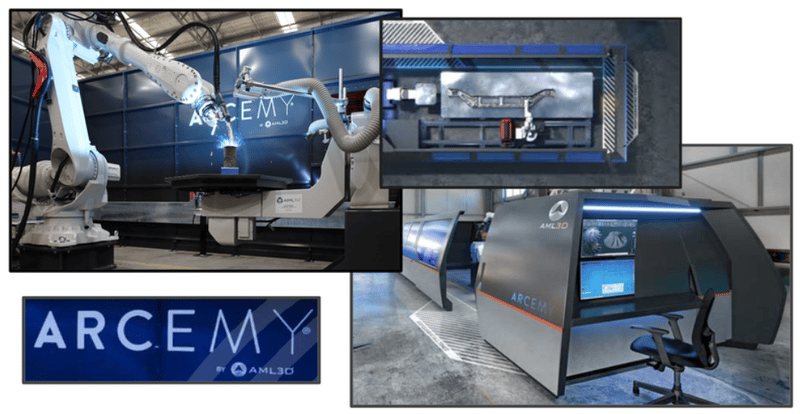

AL3’s complex software drives a giant robot arm that welds layers and layers of metal wire into the shape of the required part - on site, at the point-of-need.

This is called “additive manufacturing”

(source)

Maybe last week’s $9.9M order was the first domino to set off a chain reaction of more and/or bigger orders?

Last year, US President Trump was apparently texting the newly sworn in Navy Secretary in the middle of the night, bemoaning the current condition of US Navy ships.

(Source)

And then President Trump went on the record saying:

“We used to make so many ships. We don’t make them anymore very much, but we’re going to make them very fast, very soon. It will have a huge impact.” (source)

The supply chains that built America’s Cold War fleet have been hollowed out by decades of offshoring manufacturing.

The US government's response so far has been to rapidly throw money and attention at the problem:

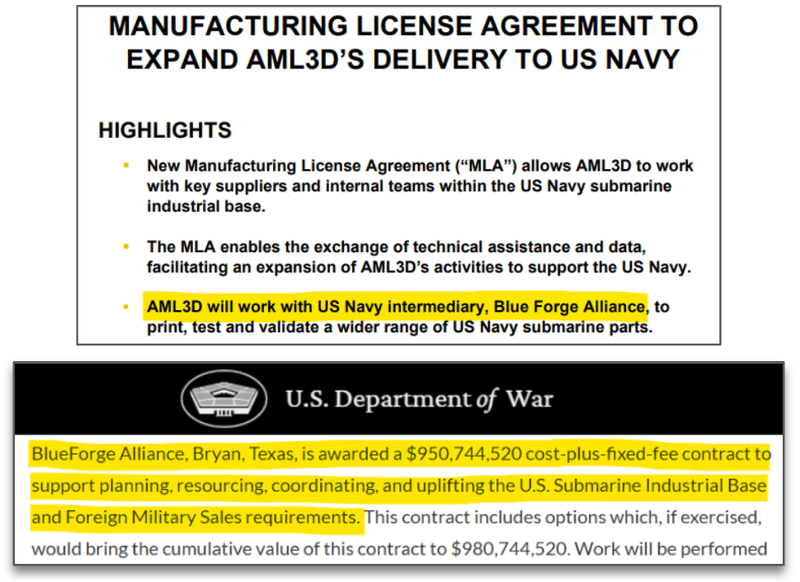

- The BlueForge Alliance (and AL3 customer) has been allocated US$951M specifically to rebuild and strengthen the US submarine industrial base.

- US$450M for additive manufacturing in shipbuilding (which is exactly what AL3 does). The Big Beautiful Bill that passed into law set aside

- At the same time, the US Department of War's FY2026 budget allocated US$3.3BN for additive manufacturing (which is exactly what AL3 does). (source)

And now with everything happening between the US and Iran - especially with the Strait Of Hormuz - the urgency is such that the US Navy is calling metallic additive manufacturing its "Manhattan Project".

(its words, not ours)

Telling parts suppliers to either adopt 3D printing to get left behind.

Here’s a direct quote from Matt Sermon, Executive Director of PEO-Strategic Submarine (linked to NAVSEA):

(source)

NAVSEA is responsible for the acquisition, development and maintenance of US Navy strategic submarine systems/programs (source), Matt is listed as an Executive Director on NAVSEA’s website (source)

This is the same Matt Sermon who featured in AL3’s latest Investor presentation on slide 20:

(source)

Additive manufacturing is exactly what AL3 does.

AL3's software drives a giant robotic arm that welds layers of metal wire on top of each other, building complex industrial parts from scratch.

The metal wire part of it is why the tech is actually called “additive manufacturing” - the robot arm “adds” layers and layers of metal to build up a part.

Three days ago we wrote about AL3 signing its biggest US defence order last week - a $9.9M order with $23BN Huntington Ingalls Industries.

That was AL3’s biggest order to date - from the largest military shipbuilder in the USA.

Today, AL3 confirmed another order for ~$2.6M - this time with the US Navy (to 3D print five different components for US Navy submarines).

The $2.6M order comes from the BlueForge Alliance with which AL3 already has a Master Licensing Agreement in place.

BlueForge Alliance is a nonprofit defense industrial base integrator that works directly with the U.S. Navy to revitalize and strengthen the country’s maritime manufacturing sector.

(A Master Licensing Agreement is basically AL3 being plugged into the parts database that the BlueForge Alliance covers - sort of like the Uber Eats for parts the US military industrial complex needs).

So AL3 is one of the many food delivery (parts) apps that the intermediary has on speed dial.

Why we think the first few orders could unlock more orders, faster

AL3 has now delivered US defence related contracts in excess of AU$30M total.

We think that’s a big milestone considering AL3 first opened its US facility in Ohio in June 2025.

AL3 is planning to invest another ~$12M to double its capacity in the US and we think things could snowball for the company from here.

(AL3 held $29.2M cash at December 31st)

For this order, AL3 will be “manufacturing submarine parts that the original manufacturer no longer makes”.

Which means the US Navy literally can’t source these parts from anyone else.

The original manufacturers either stopped making them or they just don't exist anymore.

AL3 being hand picked to deliver those parts means that AL3’s 3D printing system can do something no one else can.

More importantly, AL3’s 3D printed parts have passed all the rigorous testing the US Navy would have done to see if AL3’s parts match or exceed the quality of the original parts.

AND AL3 has given an efficient enough solution for them to be given that responsibility.

Our view is that getting through all of the quality control/audits and being chosen to produce parts is a signal AL3 has passed that invisible “trust” milestone, where the US Navy feels comfortable requesting orders for parts manufacturing to AL3.

We also think that the more AL3's tech gets used across different US Navy programs, the stickier the relationship becomes and the harder it is for anyone to displace them.

So there is a scenario (we hope) where the orders in the last two weeks unlock more parts manufacturing orders - and unlock them much easier/quicker going forward.

No guarantees of course - AL3 is a speculative early stage company, things can and do go wrong.

More orders could come from all three of AL3’s different revenue streams:

- System sales (like the $9.9M order announced last week) - selling the 3D printing machines themselves for ~$1-2.5M each

- System software and service fees - ~$250K/year recurring revenues per system sold.

- Manufacturing contracts (like the $2.6M order announced today) - using AL3's own systems to print specific parts on demand

(source)

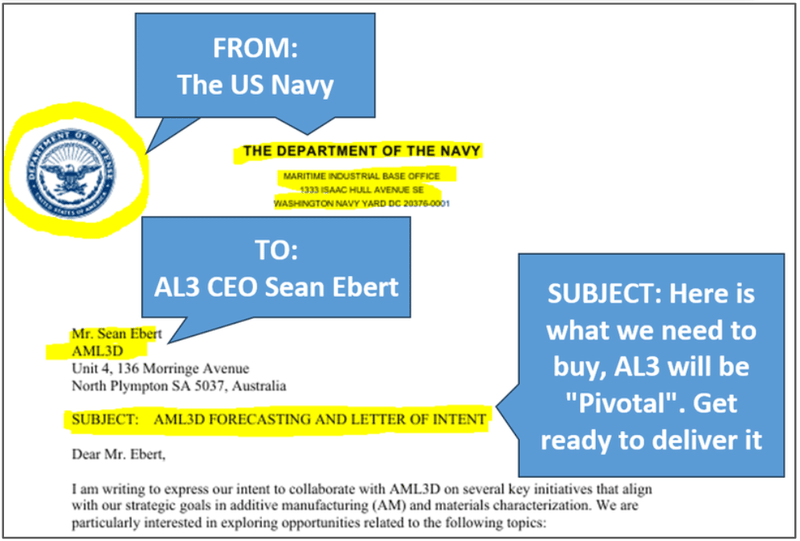

We note AL3 received a Letter of Intent from the US Navy forecasting demand for 100 additive manufacturing systems across the Marine Industrial Base back in July 2025:

(source: US Navy Letter of Intent to AL3)

Even if AL3 is contracted to meet just 40% of the forecast demand, it means US$40M - US$100M in gross sales revenue for the company.

(assuming ~US$1M to US$2.5M sale price per system) (source)

That $40-100M doesn’t include the yearly recurring revenues that would be made from the servicing and maintenance for all those systems.

This is all very rough, back of the napkin calcs here, there’s no guarantee that AL3 will secure sales of this magnitude, we are just speculating.

We note, AL3 has previously said that those yearly recurring fees are ~$250K per system sold - which means every system sale adds recurring revenues to AL3’s financials.

It also doesn’t include any revenues AL3 could make from its contract manufacturing business.

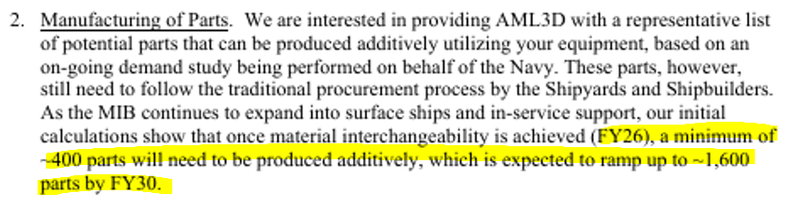

That letter of interest from the US Navy also had calculations for parts totaling ~400 in FY26 and ramping up to 1,600 by FY30.

(Source: US Navy Letter of Intent to AL3)

We won’t attempt any rough calculations on what potential annual revenue could be for AL3, assuming it manufactures some small % of those parts.

BUT IF today’s deal is $2.6M for five parts, then the numbers become material fairly quickly.

Even if AL3 is only servicing 10% of demand...

Whatever the revenue numbers AL3 actually ends up generating in the future, anything in the above range will be big for AL3, considering AL3’s current market cap is ~$94M.

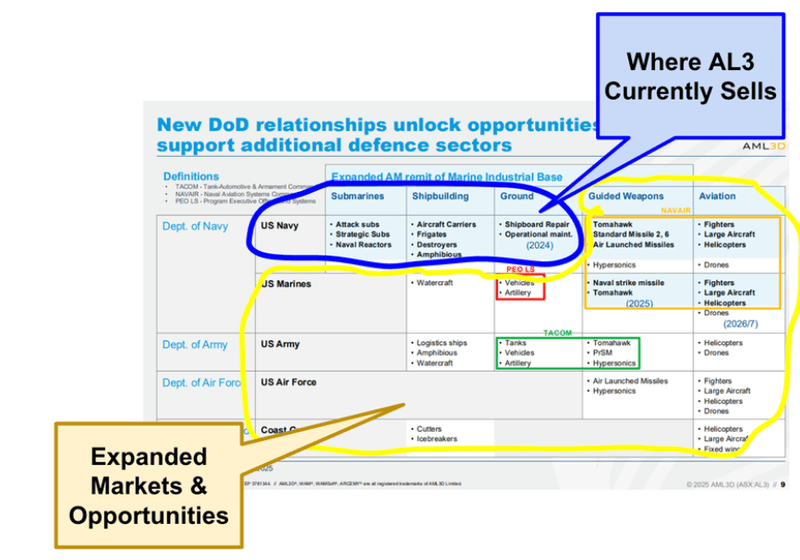

Oh and there is always a chance AL3 starts selling into other parts of the US Defence industrial complex (not just the US Navy).

Here is the table we look at when thinking about where those different AL3 customers might come from:

(source)

Ultimately, we are Invested in AL3 to see it expand into the US, grow revenues and achieve a market cap of $500M.

Our AL3 Big Bet:

“AL3 re-rates to a $500M market cap on achieving significant sales growth across an expanding range of industries and jurisdictions”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and regulatory risk - just some of which we list in our AL3 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

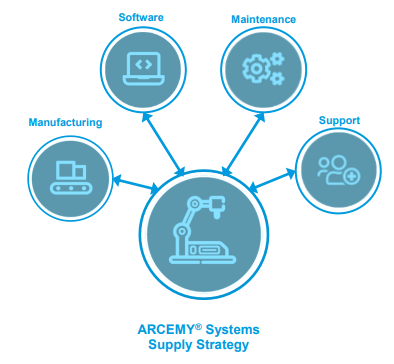

Recap: What does AL3 do?

AL3’s technology combines robotics, welding, automation and software.

A robot arm paired with AL3’s software welds layers and layers of metal wire into the shape of the required metal part.

And it gets the job done faster and cheaper than the traditional method of casting parts. (source)

(source)

AL3 makes revenue from three areas:

- ARCEMY system sales - this is where the customer pays upfront for one of AL3’s printing systems and gets it installed on site (typically $1M-$2.5M each).

- Software & services recurring fees - ~$250K per year, per system for software licensing, hardware maintenance and tech support.

- Manufacturing/prototype deals - this is where AL3 uses its own fully owned systems to print specific parts for customers.

Some of the key customers right now include:

- The US Navy (via Blue Forge Alliance MLA and Austal-run AM Centre of Excellence)

- HII / Newport News Shipbuilding ($23BN) - now 6 ARCEMY X systems

- Boeing ($172BN) - Defence Manufacturing License Agreement

- Austal ($2.6BN) - Australian military shipbuilder

- Chevron, Exxon (oil & gas)

- Tennessee Valley Authority (largest US public utility)

- FasTech LLC (US defence contractor)

- BAE Systems ($118BN) - This one is an “alloy testing” contract, IF successful it could turn into system sales/manufacturing deals (fingers crossed)

- Philips Corporation ($35BN) - value added reseller in the US

Over the last 18 months, AL3’s focus has been on expanding its US business.

AL3 raised $30M in November 2024 (at 19c), opened its US technology centre in Ohio (in June 2025) and is now looking to double the size of that facility.

(AL3 still has $29M cash in the bank as at December 31st, so has a healthy cash runway to deliver that expansion too)

And then there's Europe and the UK.

At the 2025 NATO summit, allies agreed to increase defence spending to 5% of GDP by 2035.

AL3 has set aside ~$5M from the $30M raise to push into the UK market.

It's already signed an alloy testing contract with $118BN BAE Systems - which we think could be a precursor to deals being done in the UK/Europe (IF BAE like what they see).

We think the international expansion is a potential second act for AL3 once the US business is established. But we acknowledge it's early days and execution risk is real.

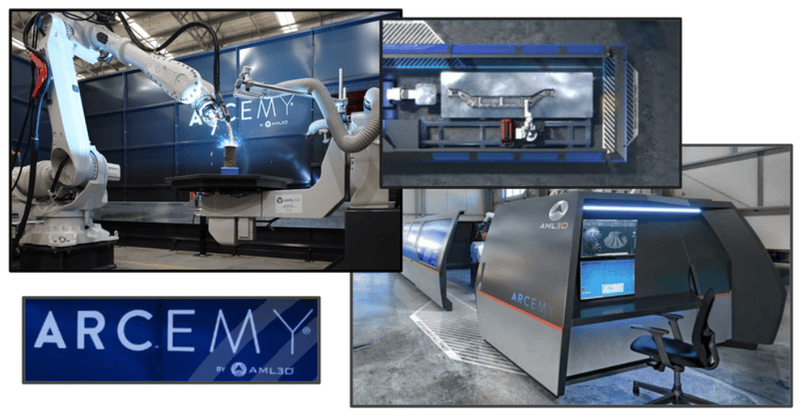

We have been to AL3's Australian facility in Adelaide a few times to check the systems out and it's genuinely amazing to see these things in motion.

(We don’t get out of the office much)

We saw the largest ever custom AL3 ARCEMY 3D printing system ever built, before it was to be shipped off to the USA:

As well as some of what the product software looks like:

To see our full site visit write up read: Our AL3 site visit and what we learnt.

What's next for AL3?

More system sales into the US market

We want to see more orders from the six US naval base companies named in the Navy's LOI.

US facility expansion

AL3 has flagged that it will be doubling the capacity of its Ohio facility.

In last week’s announcement it referred to plans to invest $12M to expand production capabilities.

The US Navy LOI said AL3 would receive "regular demand forecast briefings" to support this expansion.

We don't expect things to suddenly take off but a few system sales every few weeks/months would be a great outcome here.

UK and European market entry

AL3 has appointed distributors in the UK and Germany, and is running alloy testing with $118BN BAE Systems.

We think the alloy testing contracts are precursors for system sales/manufacturing deals - these testing contracts are where the bigger guys test AL3’s tech before buying.

Sales into Europe or the UK could change the way the market sees AL3’s future growth potential.

Revenue growth

Ultimately, we want to see AL3’s revenues grow and the company become profitable.

The $9.9M order from last week is AL3’s biggest (fingers crossed we see more of these get locked away over the coming months).

In the 2026 interim results, AL3 referred to ~ $16.5M orders in hand, made up of $7.5M signed last half, in addition to $9M in orders carried over from FY25. (source)

Not including new sales...

What could go wrong?

The key short term risk for AL3 is that no further sales are made OR there are delays to sales contracts.

If AL3 fails to deliver more sales and its financial performance suffers, the market may start to price in lower growth potential for the future and re-rate AL3's share price lower.

At the same time, any delays to big sales contracts could lead to protracted periods of no newsflow which would decrease market interest in AL3.

Sales risk

There is always the possibility that AL3 does not close more sales, and its financial performance suffers as a result.

Source: "What could go wrong" section - AL3 Investment Memo 27 June 2024

Other Risks

Like any emerging technology company operating in the defence sector, AL3 carries significant risk, here we aim to identify a few more risks.

A major risk for AL3 is customer concentration and reliance on US defence spending. The company's massive growth pipeline is heavily dependent on the US Navy and prime contractors like Huntington Ingalls. If US defence budgets are cut, political priorities shift, or the anticipated demand fails to materialise, AL3’s revenue projections would be severely impacted.

AL3 also faces significant execution and scale-up risk. Moving from selling a handful of systems to delivering multiple high-value robotic ARCEMY units requires flawless manufacturing, supply chain management, and installation capabilities. Any delays, cost blowouts, or technical failures during the rollout of its expanded Ohio facility could damage its reputation with tier-1 military clients.

Selling into the US military-industrial complex introduces intense regulatory and compliance risks. AL3 must navigate strict defence procurement rules, cybersecurity standards, and potentially ITAR (International Traffic in Arms Regulations). Any compliance failure or data breach could result in the immediate loss of contracts and exclusion from future US defence work.

The industrial 3D printing and additive manufacturing sector is highly competitive and rapidly evolving. AL3 competes against massive, well-funded global manufacturing and technology firms. There is a constant risk that competitors develop faster, cheaper, or more precise metal 3D printing technologies, which could render AL3’s ARCEMY systems obsolete or force them to slash margins to compete.

Finally, while the US Navy is pushing for the adoption of 3D printing, widespread industry adoption risk remains. Traditional shipbuilders and defence contractors may be slow to transition away from deeply entrenched casting and forging supply chains, potentially delaying AL3's sales cycle and slowing its path to profitability.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our AL3 Investment Memo

You can read our AL3 Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

In our AL3 Investment Memo, you can find the following:

- What does AL3 do?

- The macro theme for AL3

- Our AL3 Big Bet

- What we want to see AL3 achieve

- Why we are Invested in AL3

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.