US Navy Letter of Intent: AL3 “pivotal” to US Navy’s forecast demand of 100 x 3D printing systems.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 6,685,029 AL3 shares at the time of publishing this article. The Company has been engaged by AL3 to share our commentary on the progress of our Investment in AL3 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

The US Navy just issued AML3D (ASX:AL3) a “Letter of Intent”.

(yes, THE US Navy)

The letter outlines the US Navy’s forecasts of what it needs in the 3D printing space and basically tells AL3 to “get ready to deliver it” - because AL3 will play “a pivotal role in achieving these targeted needs”. (See full letter from the US Navy linked below)

The US Navy letter says they need from AL3:

- 100 new additive manufacturing (3D printing) systems to be installed across the US marine industrial base

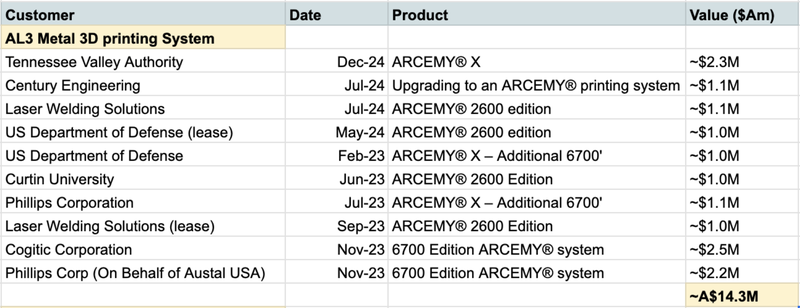

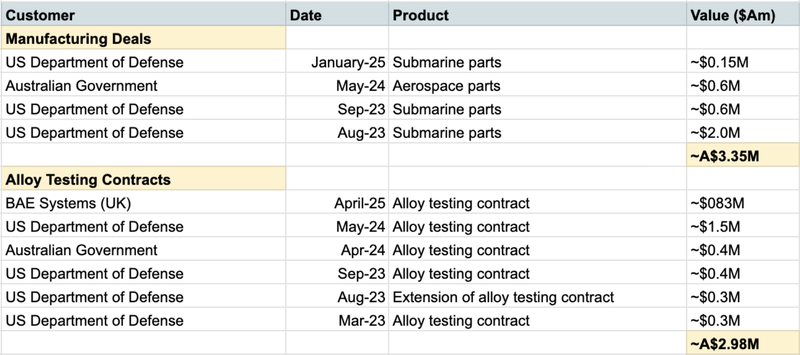

(for context, over the last 18 months AL3 has announced a total 10 system sales for total revenue of $14.3M) - A minimum of ~400 manufactured parts printed in FY26, growing each year until an estimated ~1,600 parts will need to be produced in FY30

(for context, over the last 27 months AL3 has announced 4 custom parts contracts for a total of $3.35M revenue, noting that smaller parts contracts may not have been announced)

We do some rough calculations on what this all could mean for AL3’s revenue in a second.

The letter also says that AL3 will regularly be briefed on US Navy demand forecasts, which AL3 says will support a doubling in its US manufacturing capability.

Here is the US Navy Letter to AL3 (the full letter is in the AL3 Announcement here):

(Source: US Navy Letter of Intent to AL3)

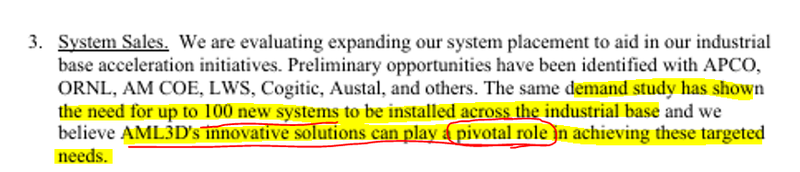

For us, the most interesting section in the US Navy letter is about forecast demand for 100 3D printing systems:

(Source: US Navy Letter of Intent to AL3)

Where AL3 can play a “pivotal role”:

The letter basically tells AL3 to "get ready" because the US Navy predicts they will need ONE HUNDRED 3D printing systems and 400 custom 3D printed parts per year.

Please also note the US Navy also lists a number of other companies they have identified who could also help it.

(growing to 1,600 custom 3D printed parts per year in 2030):

(Source: US Navy Letter of Intent to AL3)

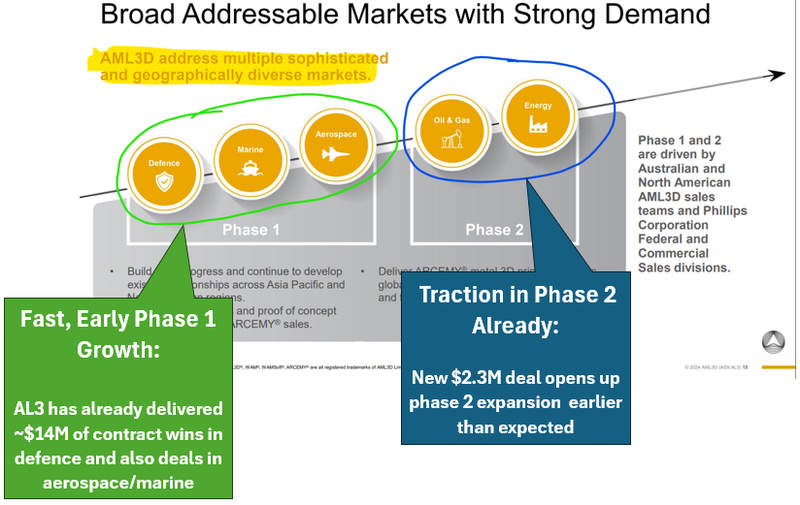

AL3’s ARCEMY metal 3D printing tech quickly and cheaply “3D prints” complex industrial parts for the shipbuilding and defence industry.

A robot arm driven by AL3’s complex software welds layers and layers of metal wires into the shape of the required metal part - much faster and cheaper than the traditional method of casting large metal parts in a foundry.

AL3 makes revenue from three key product areas:

- ARCEMY 3D Printing system sales: ARCEMY is the name of AL3’s 3D printing system that customers can use to 3D print desired parts on site. These sell for between $1M-$2.5M and are big contracts.

- ARCEMY software & services recurring yearly fees: For customers that have purchased an ARCEMY 3D printing system, AL3 provides annual support through maintenance, product support and software licensing that enables customers to use the facility. This is the Annual Recurring Revenue (ARR) side of the business.

- Manufacturing Deals: AL3 sells specific 3D printed parts to various organisations. These sales contracts are generally smaller and proof of concept that will hopefully lead to repeat business. Product testing and certifications expand the library of products that AL3 can sell in this way.

So how much could AL3 make from the sale of up to 100 3D printing systems to the US Navy?

For context, in the last ~18 months AL3 announced 10 ARCEMY 3D printing system sales for between US$1M all the way up to ~US$2.5M.

(Source, Updated from AL3 Presentation November 2024)

(These are sales AL3 has announced to the market - there could be more that have happened but haven’t been announced to the market)

Using those sales as a benchmark, the forecast demand of 100 systems could be worth somewhere between ~A$100M to A$250M (gross revenue, before costs, taxes, etc).

(keep in mind, AL3 still has work to do to land and execute on this forecast demand from the US Navy)

Even if AL3 is contracted to meet just 40% of the forecast demand, it means $40M - $100M in gross sales revenue for the company.

That $40-100M doesn’t include the yearly recurring revenues that would be made from the servicing and maintenance for all those systems.

Whatever the final revenue numbers are for AL3, anything in the above range will be big for AL3, considering AL3’s current market cap is ~$130M and half-yearly revenues up to 31 December 2024 were ~$4.6M.

It's important to note that any “back of the napkin” rough calculation we make depends on assumptions made about AL3’s “pivotal role” to fill this US Navy demand.

Will it be 20 systems? 50 systems? 80 systems - we can't predict what final number AL3 will achieve.

3D printing system sales = big upfront cash in the door for AL3...

But more importantly, it means a giant fleet of systems will be operating from which AL3 can generate services/maintenance recurring revenues from.

(What's the collective noun for a group of installed 3D printing systems? Is it called a “farm”? A 3D printing farm?)

AL3 also charges software and services fees for each 3D printing system sold on a recurring annual revenue basis.

AL3 has previously said that those yearly recurring fees are ~$250K per system sold - which means every system sale adds recurring revenues to AL3’s financials.

Again, the US Navy says AL3 will play a “pivotal role” in achieving the target 100 3D printing systems installed across the entire US Maritime Industrial Base.

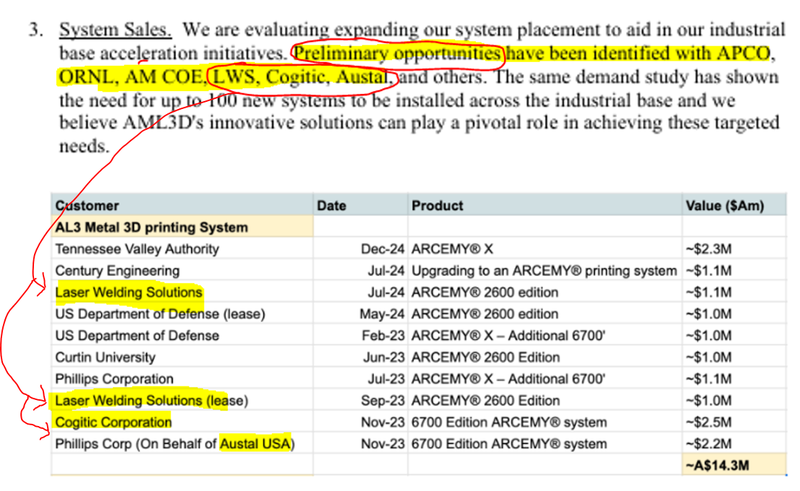

It is also worth noting from the Navy letter, that three of the six US Navy industrial base companies identified to be “preliminary opportunities” are ALREADY AL3 customers

(Source AL3 Announcement)

We take “Preliminary opportunities” to mean that these named companies will be the first to buy more 3D printing system as the first step to fill the 100 system demand: (but note, “preliminary” also means that it is still doubtful and has to be confirmed).

So it's positive that 3 of the 6 have already bought/used AL3’s systems in the past.

How much could AL3 make from the sale of hundreds of parts annually?

Based on the ongoing demand study, initial calculations show a minimum of ~400 parts will need to be produced in FY26 ramping up to ~1,600 by FY30.

(Source: US Navy Letter of Intent to AL3)

Rough calculations of the potential financial impacts of this for AL3 is quite a bit harder.

Based on previously announced custom 3D print jobs:

- On the lower end have sold for $156,000 - like the recent prototype tailpiece that AL3 sold in January,

- On the higher end for $2M for the more complex, high quality competents.

We won’t attempt any rough calculations on what potential annual revenue could be for AL3 assuming that 400 parts are sold in the next financial year.

Growing at a further ~300 parts annually until at least FY30.

(Source, Updated from AL3 Presentation November 2024)

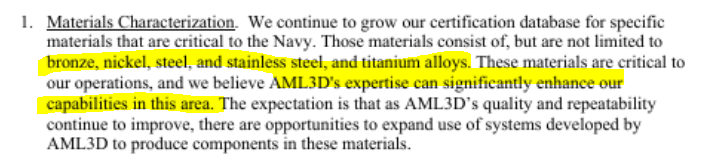

We also note in the letter that the Navy has requested for AL3 to expand its “certification database” to 3D print using more different materials that are critical to the Navy:

(Source: US Navy Letter of Intent to AL3)

Big Beautiful Bill approved - funding unlocked for these big deals

Over the weekend the multi-trillion dollar Big Beautiful Bill was voted on, approved and is now law:

The Big Bill could be what is prompting things like today’s Letter of Intent.

We highlighted it last week, but the Big Beautiful Bill specifically called out US$450M for “additive manufacturing for wire production and machining capacity for the shipbuilding industrial base”:

(Source: Big Beautiful Bill page 110)

(Source: Big Beautiful Bill page 134)

As per above, it also called for US$50M on manufacturing capacity for things like “Naval propellers” and US$35M for military additive manufacturing capabilities.

While we think that AL3 may well be a winner from this extra government spending in the sector, the exact amounts and specific benefits are not yet clear.

There is also an element of timing risk here - government initiatives can take a lot longer to be actioned than anyone would expect so its hard to predict IF/When these funding initiatives start to come into play.

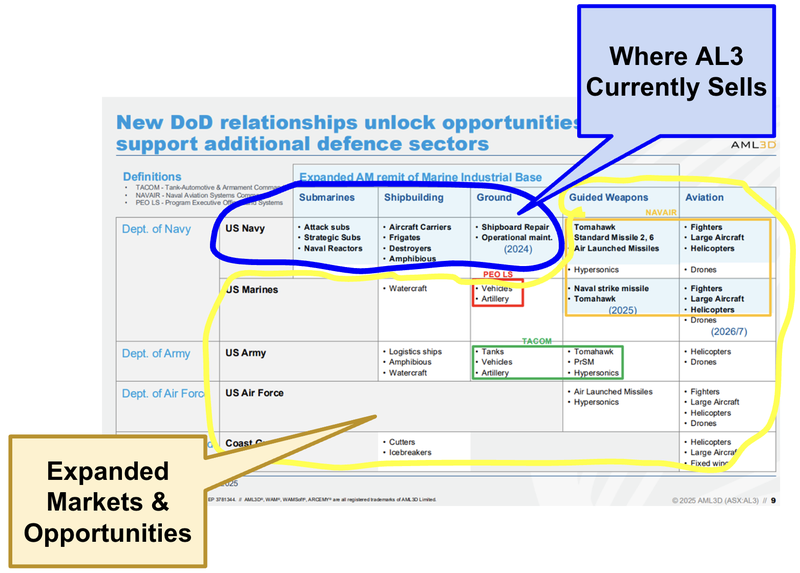

Where else could even more AL3 contracts come from?

Today’s Letter of Intent is from the US Navy - and should keep AL3 very busy going by the language that AL3 can “play a pivotal role” in the marine industrial base reaching their target of 100 additive manufacturing systems.

Assuming that AL3 delivers on this relationship, AL3 could expand, selling its additive manufacturing products into the US Army and Airforce.

(Source)

Outside of the US government, associated industries AL3 can also sign big deals in other industries like oil and gas, utilities and other industries where on-site manufacturing is important:

AL3 is already selling systems and parts to those other industries, like Boeing, Austal (the Australian military shipbuilder) and oil & gas giants Chevron and Exxon - so it's not inconceivable to see AL3 sign bigger deals here.

(Source)

The US Navy adopting AL3’s tech could also act as a starting gun for wider market adoption...

Everything mentioned up to this point is just in the USA.

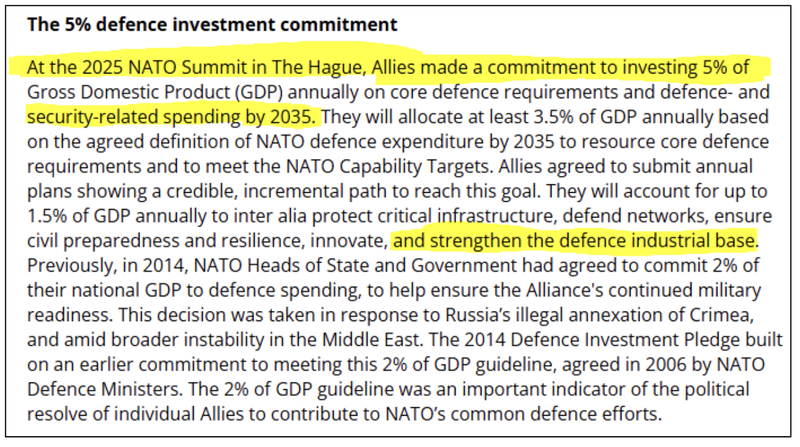

Only a few weeks back at the 2025 NATO summit, allies agreed to increase defence related spending between now and 2035.

The target set was to increase spending to 5% of Gross Domestic Product (GDP) annually...

(Source)

A specific commitment was to “innovate, and strengthen the defence industrial base” - which is exactly where we think AL3’s tech sits.

(Source)

We think that a wave of ramped-up defence spending across Europe, the UK and the Middle East could eventually flow in AL3’s direction too.

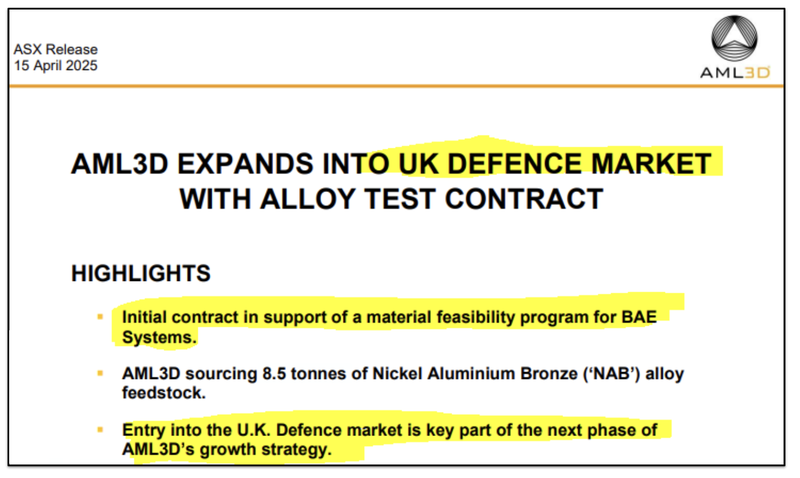

From the $30M that AL3 raised in November last year, A$5M was set aside to grow into the UK and European markets.

Back in April AL3 signed an alloy testing contract with $118BN BAE Systems “in support of a material feasibility study” for expansion into the UK defence market:

(Source)

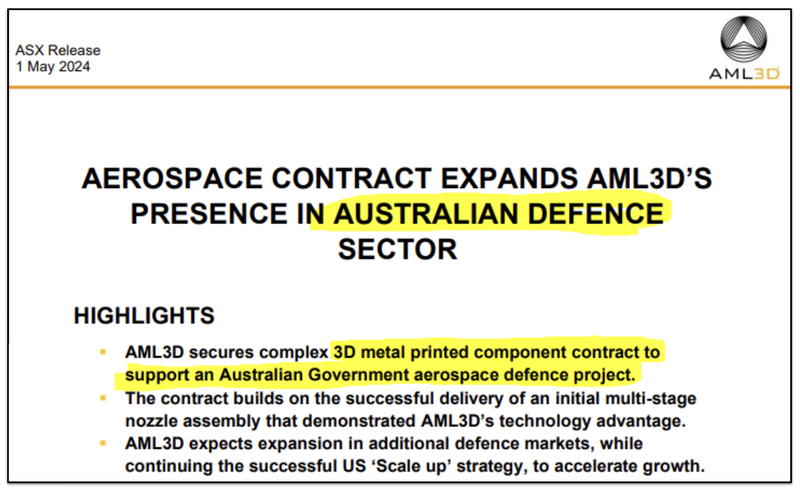

AL3 has also sold into the Australian Defence Department too:

(Source)

Our view is that big sales contracts and growth opportunities from outside of the US is a real possibility for AL3.

Once AL3 establishes itself in the US, and expands globally, it could be the next stepchange for material re-rate in the company.

There are still a lot of hurdles for AL3 to overcome, and execution risk is a real challenge for AL3 at this important juncture, and just because there is an increase in defence spending does not guarantee success for AL3.

To get a view of the upside case, take a look at what happened with another ASX-listed company leveraged to the defence thematic recently - Droneshield.

A few weeks ago Droneshield signed a $61.6M european military contract and hit a NEW all time high market cap north of ~A$2BN.

The past performance is not and should not be taken as an indication of future performance for this or any stock. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think a few big orders in a row have the potential to trigger a similar re-rate in AL3’s market cap (but note, that Droneshield’s past performance is not an indicator of AL3’s future performance).

We have seen before that these bigger deals are often delayed and may never eventuate, even if US government funding is unlocked.

Many factors may determine the success of AL3 in its ability to secure major contracts and eventual re-rate in its share price.

Our AL3 ‘Big Bet’:

“AL3 re-rates to a $500M market cap on achieving significant sales growth across an expanding range of industries and jurisdictions”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and regulatory risk - just some of which we list in our AL3 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

AML3D

ASX:AL3

How does AL3’s tech work? What we learned from our site visit...

AL3’s technology combines robotics, welding, automation and software.

AL3 tech “3D prints” complex industrial parts for the defence, oil & gas and aerospace industries, and sells these 3D printers to industries looking for on-site custom solutions.

We have been to AL3’s Australian facility in Adelaide to check the systems out and it's genuinely amazing to see these things in motion.

We saw the largest ever custom AL3 ARCEMY 3D printing system ever built, before it was to be shipped off to the USA:

As well as some of what the product software looks like:

To see our full site visit write up read: Our AL3 site visit and what we learnt.

8 Key reasons why we Invested in AL3:

Here are the 8 reasons we Invested in AL3 from our first Investment Memo published on 27th June 2024

Check out our AL3 Investment Memo here.

Since then, a significant amount has changed in the markets, and AL3 has made considerable progress, which is why we have included updates on some of the reasons below:

1. 3D printing product at the forefront of manufacturing innovation

AL3 sells large scale modular 3D printing systems to industrial manufacturers. Its product, ARCEMY, provides a better solution to manufacturing parts for complex industrial machinery.

2. Blue-chip client base including US Department of Defence

AL3 has a range of high-profile customers including the US Navy, US Department of Defence, Austal (the Australian military shipbuilder) as well as oil & gas giants Chevron and Exxon.

These customers provide validation for AL3’s product in future sales as well as a network of potential smaller suppliers for AL3 to target.

🚨 UPDATE:

Since we published these reasons AL3 added NEW high profile customers to its books.

AL3 signed a $2.27M deal with the Tennessee Valley Authority, the largest public utility in the US.

AL3 also signed another $830k deal with $118BN British multinational aerospace, arms and information security company - BAE Systems.

We think this reason has only become stronger now (especially after today’s news).

3. Tiny EV for AL3 with proven tech with sales

At 7.3c AL3 has a market cap of ~$22M, with ~$8M in the bank has an Enterprise Value of ~$14M. AL3 is already at ~A$6.6M in revenue for the first 9 months of FY24. AL3 has invested over ~$30M building out its tech.

🚨 UPDATE:

AL3’s market cap has changed from when we first Invested in the company.

AL3 tucked away a $30M capital raise at 19c per share in November 2024.

And now, AL3’s market cap sits at ~$130M

AL3 had ~$31M cash in the bank at 31 March 2025 which means the company’s enterprise value is ~$100M at today’s prices.

We think the valuation change is a positive for AL3 with interest in its systems/services increasing from high profile customers (like the US Navy).

These customers would want to see AL3 be in a position where it can meet ambitious sales orders - and we think AL3’s balance sheet is now in a position where the company can do that.

4. New sales strategy already driving revenue growth

AL3 has moved from a “sell the 3D printed parts” to a “sell the 3D printing system” strategy. This new strategy means bigger contracts for AL3 and gives customers what they want because the parts are made closer to where they are needed.

🚨 UPDATE:

Since our Investment Memo was published we have actually seen one customer move from a lease on a system to an outright purchase.

As mentioned above we have also seen orders for systems come from different industries (like that Tennessee Valley Authority $2.27M system sale (from a public utility).

We think the change in business model has opened the company up to a much wider range of potential adopters of AL3’s 3D Printing System tech.

5. “Sell the 3D printing system” strategy opens up yearly recurring revenue

For new orders of the ARCEMY system, AL3 will now build in ARCEMY services to include software and services fees on a recurring revenue basis.

This includes software licensing fees, hardware maintenance, and tech support. This is an untapped stream of revenue for AL3 and a potential source of upside for the company as the company grows.

🚨 UPDATE:

AL3 has been including software/services contracts in its latest system sales.

It’s hard to pin down an exact dollar figure for these contracts BUT if AL3 sold 100 systems and was able to generate $250K in Annual Recurring Revenues (ARR) from the software/maintenance contracts it could mean ~$25M in ARR to AL3.

(The $250,000 is an estimate posted by AL3’s official Facebook page)

These are just, rough back of the napkin calculations and 100 systems - we don't know how many systems AL3 will end up selling and how much ARR will be attached to any future sales.

6. Strong US focus as AM Forward Program rolls out

In 2023 AL3 commenced its US focused strategy. The US spends more on its defence than the next 9 countries combined and as such is easily the most lucrative defence market jurisdiction to operate in.

In 2022, the US has also launched the AM Forward Program to support 3D Printing across the industrial manufacturing sector. We think that the US is the right place for AL3 to grow its business.

🚨 UPDATE:

We have been very happy with AL3’s US expansion to date - raising $30M and opening its new US facilities in Ohio.

We think today’s Letter of Intent from the US Navy is a big validation signal for the US expansion actually working for AL3...

7. US distribution partner Philips has proven its ability to sell AL3’s product

AL3 has a value added reseller agreement with ~$35BN capped Philips Corporation.

Philips’ sales team has already helped AL3 make two US sales, including an ARCEMY sale to the US Navy Centre of Excellence which we see as the first signs that Philips is an engaged partner and we expect their sales team to help drive the marketing of AL3’s products.

8. US Navy to help to push AL3 to its parts suppliers

The early signs are there. We want to see AL3 expand into smaller US Navy parts suppliers who are following the US Navy’s lead. In September 2023, a Navy parts supplier called Laser Welding Solutions leased the ARCEMY product from AL3 - we hope the first of many contracts for AL3 from this type of smaller organisation.

🚨 UPDATE:

Today, the US Navy penned a Letter of Intent, forecasting the demand for additive manufacturing systems that they see AL3 will play a “pivotal role” in delivering.

The letter mentions “Preliminary opportunities have been identified with APCO, ORNL, AM COE, LWS, Cogitic, Austal” - these are the companies or organisation that sit inside the military industrial complex.

(some of which AL3 already has relationships with)

(Source: US Navy Letter of Intent to AL3)

What are the risks?

The key short term risk for AL3 is a risk that there are no sales made OR delays to sales contracts.

If AL3 fails to deliver more sales and its financial performance suffers, the market may start to price in lower growth potential for the future and re-rate AL3’s share price lower.

At the same time, any delays to big sales contracts could lead to protracted periods of no newsflow which would decrease market interest in AL3.

Sales risk

There is always the possibility that AL3 does not close more sales, and its financial performance suffers as a result.

Source: “What could go wrong” section - AL3 Investment Memo 27 June 2024

Other Risks:

There are also a number of other risks worth keeping in mind. These include regulatory risk – with AL3 operating in highly sensitive defense and industrial sectors, changes in US or Australian policy, licensing, or procurement processes could impact operations.

There’s also tech and execution risk – AL3’s advanced manufacturing process is impressive but scaling it successfully to meet future US demand involves complex logistics.

And finally, customer and funding concentration risk – any delays in securing or fulfilling major US orders, or needing additional capital, could affect financial performance.

As always, these risks are part of early-stage industrial tech investments.

For the full set of risks we have identified and accepted in making our Investment in AL3, see our AL3 Investment Memo below.

Our AL3 Investment Memo

You can read our AL3 Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

In our AL3 Investment Memo, you can find the following:

- What does AL3 do?

- The macro theme for AL3

- Our AL3 Big Bet

- What we want to see AL3 achieve

- Why we are Invested in AL3

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.