$5.7M capped PFE cuts $40M deal for its US assets: start of a bidding war?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 11,853,770 PFE shares and 3,460,950 PFE Options at the time of publishing this article. The Company has been engaged by PFE to share our commentary on the progress of our Investment in PFE over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

The starter’s gun has been fired...

Will today's binding sale agreement flush out interest from bigger neighbours?

$5.7M capped Pantera Lithium (ASX:PFE) has just signed a binding deal to sell its US lithium brine assets in the Smackover Basin for A$40M.

PFE’s ground is surrounded by $753BN Exxon, $103BN Equinor and $393BN Chevron’s new lithium projects.

...the binding offer announced today is from US-based private lithium company EnergyX, to increase its existing land holding in the Smackover Basin.

The deal is split $6M cash, and $34M in equity in EnergyX.

EnergyX has two lithium brine assets (also in the Smackover, USA and in Chile) and owns 5 Direct Lithium Extraction (DLE) technologies protected by 130 patents.

EnergyX has raised over US$130M to date including from General Motors who came in at the series B round.

(More on EnergyX later)

We note the deal completion date is set for 1 October 2025 - which gives any potential bidders three months to make a move...

We think today’s offer might also flush out any other companies that may have had an eye on acreage in the Smackover, but hadn’t yet made a move...

OR it could force the hand of any of the existing majors already in the region who don't want PFE’s acreage to end up in someone else's hands...

Right now PFE’s ground is surrounded by $753BN ExxonMobil, $103BN Equinor and $393BN Chevron - Energy super majors have moved into the Smackover for its lithium brine potential.

Outside of the major petrochemical players, Tetra Technologies and the world’s biggest lithium producer Albemarle also hold ground in the region...

Check out the map below:

PFE’s binding agreement on an asset sale might now tease out another bidder who wants to consolidate ground OR a new bidder who wants to enter the Smackover...

(We note that PFE would have to pay a “break fee” of 2.5% to EnergyX if a superior offer is made and accepted for PFE’s assets in the next 180 days).

There is industry and corporate consensus on the Smackover becoming a US lithium hotspot...

Exxon’s plan is to be producing lithium from the Smackover by 2027 and a well known lithium industry expert thinks the Smackover will be “where the US has DLE & brine success”.

The deal completion date is expected to be 1 October 2025.

So there will be a ~3 month period for anyone interested in making a competing approach to acquire PFE.

Almost all of the ground in the Smackover has now been acquired by major oil and gas or lithium DLE companies.

Chevron entered the Smackover just a few weeks ago picking up ground to the west of PFE.

PFE’s ground was acquired before Exxon entered the frame, and now PFE’s acreage is surrounded by:

- May 2023: $753BN ExxonMobil, which came into the region with an acquisition reported to be over US$100M (source).

- May 2024: $103BN Equinor came in for a 45% stake in Standard Lithium’s assets in the region in a deal worth up to US$133M (source).

- June 2025: $393BN Chevron acquired 125,000 acres for an undisclosed amount (source).

- TODAY: EnergyX announced its deal for 35,000 gross acres by acquiring PFE’s project for $40M

The Smackover Basin is where Exxon plans to centre its entire lithium business inside the US.

This is because the Smackover brine formation has some of the highest grade brines in North America, with grades above 600ppm.

There is an alignment of opinions from the US government and the big petrochemical players about the Smackover’s potential to become a lithium hotspot inside the US.

The US government has singled out Equinor and Standard Lithium’s lithium brine joint venture in the Smackover region as one of the first critical mineral production projects to be advanced under Executive Order 14241, which expedites the permitting review process (source).

(the US Department Of Energy (DOE) also gave US$225M in grant funding for this project).

(Source)

It isn't just the US government OR corporates that believe in the Smackover either...

Well known lithium industry expert Joe Lowry is also on the record saying he thinks the Smackover will be “where the US will have brine & DLE Success”.

(Source)

Will today’s deal flush out competing offers for PFE’s project?

PFE is the only ASX listed company with ground in the Smackover...

AND with US based assets starting to catch a bid on the ASX, we think today’s deal will put PFE’s project in play for any other companies who have been sitting on the sidelines watching the region.

Today’s deal could create some urgency and competitive tension that forces competing bids on the project...

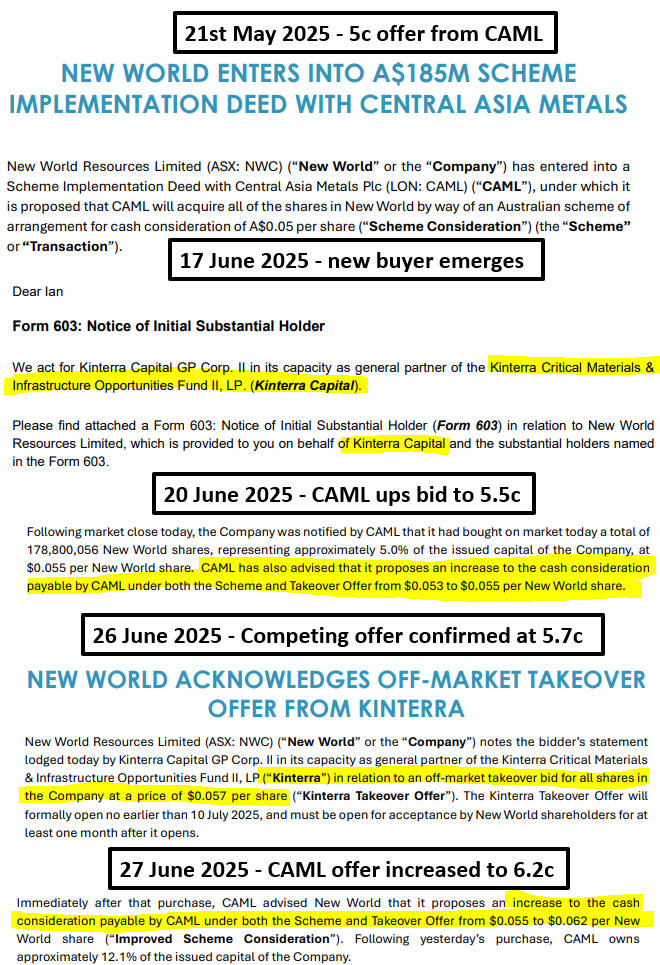

We have seen something similar to this play out with US based copper developer New World Resources.

New World’s share price touched 52-week lows earlier this year, then in late May an all-cash takeover offer for the company came in at a big premium to the company’s share price.

That deal prompted on-market buying and a higher offer from a competing bidder...

And eventually CAML (the original bidder) was forced to increase its offer several times to now sit at ~6.2c per share (1.2c higher than its first offer).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Here is the timeline of events on that New World deal:

Of course, just because there was a competitive bidding process that played out publicly for New World, pushing up the price of the acquisition, there is no guarantee that the same type of thing happens to PFE.

However, generally speaking M&A has a habit of playing out this way - where everyone sits around and waits for someone to make the first move...

Then once the first move is made, FOMO starts to come into play and everyone starts to show their hands.

(but also - sometimes it doesn't play out this way...)

We think there is a chance something similar could play out for PFE’s project because:

- There is a clear interest in the Smackover from the big petrochemical companies (Exxon, Chevron and Equinor are already here) and let's not forget Tetra Technologies and Albemarle who also hold ground in the region...

- The US government is throwing grant funding and accelerated permitting at the region - US$225M in non-dilutive funding has been given to Standard and Equinor’s JV as well as accelerated permitting.

- The US wants domestic critical minerals projects to be brought online - PresidentTrump passed an Executive Order looking to increase domestic mineral production in critical minerals (like lithium).

- Trumps “Big Beautiful Bill” just passed - A bill that includes US$2.5BN for a national critical minerals stockpile and $500 million for a Department of Defence loan program to support domestic mining projects

- AND capital is finally flowing into US based assets again - ASX small caps with US assets are being bid up again. Dateline Resources was up 50x in 45 days and New World Copper attracted a takeover offer at a $200M+ valuation.

Of course that doesn't mean an investment in PFE will lead to a successful outcome. All small cap speculative stocks are risky investments.

While some US based assets are receiving a lot of interest, the lithium macro thematic is still fairly challenged at the moment.

There is no guarantee broader market interest flows into lithium, and there is no guarantee that more bidders emerge for PFE’s project.

Our take on the deal terms

If the deal is accepted what does it mean for PFE Shareholders?

- PFE will get A$6M in cash ($2M on close, $2M 9 months after closing, $2M 18 months after closing).

- PFE will get $34M worth of EnergyX common stock, priced at US$9.50/share, representing 2,344,828 shares issued to Pantera.

- According to EnergyX's latest SEC filings EnergyX had 110,437,192 Common Stock on issue, which means this deal will give PFE a 2.12% holdings of EnergyX (on a non-dilluted basis) (source).

What we like about the potential deal:

- $40M total deal size - Headline value of the deal is ~8x the current PFE market cap.

- PFE retains exposure to the Smackover - We are big believers that the Smackover will play a big part in the future of US lithium production. PFE getting 2.12% stake in EnergyX means the company still has exposure to the Smackover through its ownership in EnergyX.

- Upfront non-dilutive Cash - PFE is capped at $5.7M, the company will get $6M in non-dilutive funding over the next 18 months, including $2M on the close of the deal (90 day terms).

- The project moves into the hands of a company that might have a better chance to fund development - US based EnergyX has raised over US$130M in the past, and has attracted investment from General Motors. EnergyX has also secured US government grants from the Department of Energy and a US$690M letter of intent from the US Export Import Bank. EnergyX has also secured a commitment for US$450M funding (contingent on a public market listing).

- Is this just the first “offer”? - as mentioned above, today’s offer might create some urgency amongst others who may have been sitting on the sidelines.

What we don’t like:

- Private company, lack of liquidity - If PFE sells to a private company, it may be a challenge for PFE shareholders to realise the benefits in the short term.

- Hard to mark/value private investments - It is harder to gauge valuations of private companies because the shares are not publicly traded, generally the valuation is set by the price at which the most recent investment round was done, which may or may not be publicly disclosed.

Who is PFE’s suitor, EnergyX?

EnergyX is a privately listed US-based lithium company with lithium brine assets in the US and Chile.

The company is also developing Direct Lithium Extraction (DLE) technology with an operating plant demo plant in Chile and plans to build one in Texas, USA.

Here are some key things we found on EnergyX from its public presentation:

- EnergyX has 5 different Direct Lithium Extraction (DLE) technologies protected by over 130 patents.

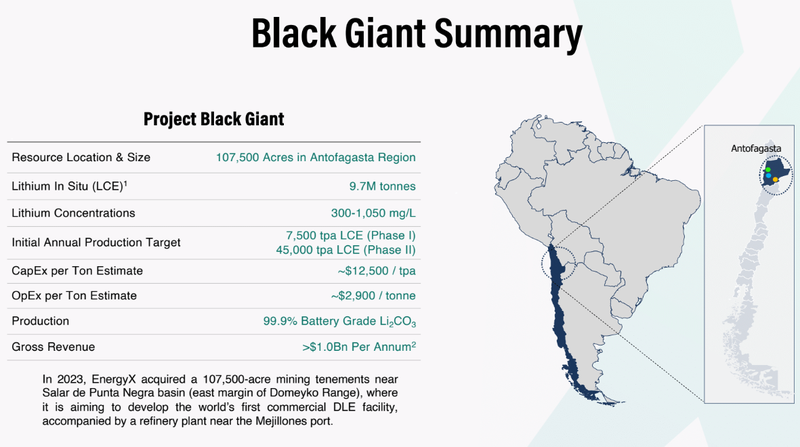

- The company has two lithium brine projects: One in the Smackover (12,500 acres before the PFE ground is considered) and another in Chile which has a resource of up to 9.7mt of Lithium Carbonate Equivalent (LCE).

- EnergyX also has three existing DLE pilot plants and two demo plants that are being commissioned this year.

- EnergyX has raised over US$130M+ the past, a commitment for US$450M funding (contingent on a listing) and a debt commitment from the US export-import bank for US$690M on its Chilean asset.

Here is a summary of EnergyX’s Chilean asset:

(Source)

And here is the existing ground EnergyX has in the Smackover, USA:

(Source)

And here is a summary of where EnergyXis at with its DLE tech and what’s to come (that last picture has a lot of Tesla gigafactory inspiration to it... also, it's just a digital render that EnergyX hasn't built yet)

(Source)

The two highlights that stood out to us are the:

- US$50M series B cornerstone by General Motors AND the fact that GM has “offtake rights” with EnergyX... (Source)

- $690M debt letter of intent from the US Export-Import Bank for its Chilean project.

Because the EnergyX investment is such a big part of this deal for PFE shareholders, it is worth reading through their corporate deck which you can find here: EnergyX Corporate Website Presentation.

What are the risks?

The main risk for PFE in the short term is “Deal Risk” & “Funding Risk”.

PFE has now announced a deal to sell its core asset.

In the short term, the deal will underpin PFE’s valuation in some form.

However there is no guarantee the deal goes ahead in its current form and there is a risk that the deal never gets completed.

If the deal were to be cancelled, we would expect PFE’s share price to be impacted negatively.

(unless of course its cancelled due to a superior offer... in which case PFE could trade higher to reflect the superior offer)

There is also a risk that the deal takes a lot longer than expected which may bring into play “Funding Risk”.

PFE is a pre-revenue micro cap stock. To progress the development of its project e it may need to raise more capital.

Capital raises, in the short term may lead to more dilution and may take place at discounts to market prices.

PFE had ~$1.3M cash at 31 March 2024 and we will get an updated quarterly cash balance which will likely be lower than that number between now and the end of this month (like we said PFE is not generating any revenue).

The first tranche of cash ($2M) from EnergyX is expected on the 1st of October 2025 (when the deal is expected to close) so there will be a fair bit of time between now and any of the cash from today’s announcement hitting PFE’s bank account, and PFE will need to continue operations and pay corporate overheads.

Funding risk

PFE is a micro cap stock and will need to raise more capital to continue expanding its foothold in the Smackover Formation. Capital raises can lead to dilution and may take place at a discount to market prices, reducing the value of PFE shares

Source: “What could go wrong? - PFE Investment Memo 4 March 2024

Liquidity risk (if PFE were to complete the deal):

If today’s deal were to complete in its current format, PFE would receive private company shares.

There is no guarantee of a liquidity event (IPO, sale, or buyback) that allows PFE to monetise these shares. If EnergyX delays listing or never lists, the value of this “equity” may remain locked up indefinitely.

EnergyX execution risk (if PFE were to complete the deal)

Because the majority of the value of this deal is in EnergyX shares, EnergyX’s ability to execute and deliver value will be a key determining factor as to whether PFE can realise value.

While EnergyX owns multiple DLE technologies,none are proven at commercial scale.

If DLE doesn’t scale as expected - or if competing technologies outperform theirs - then EnergyX’s valuation and prospects could fall sharply.

To see more risks read our PFE Investment Memo here.

Our PFE Investment Memo

Below is our Investment Memo for PFE, which provides a short, high-level summary of our reasons for Investing.

In our PFE Investment Memo, you can find the following:

- What does PFE do?

- The macro theme for PFE

- Our PFE Big Bet

- What we want to see PFE achieve

- Why we are Invested in PFE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.