$47M capped MNB to Build ~$80M EBITDA per year phosphate mine within 10 months?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 12,026,429 MNB shares and 4,141,429 MNB Options at the time of publishing this article. The Company has been engaged by MNB to share our commentary on the progress of our Investment in MNB over time.

Our Investment, $47M market cap Minbos Resources (ASX:MNB) is about to build a phosphate mine...

That is forecast to deliver US$55M EBITDA per year over a 20 year mine life.

(phosphate is used to make fertiliser for growing our food)

MNB currently forecasts the mine build completion and first production by May 2025.

... in just 10 months.

An offtake MoU is already in place for 66% of all mine production for the first 7 years.

So then why is MNB currently trading at 5.5c and at a market cap of just $47M?

And what do we expect to happen in the next couple months that will re-rate MNB’s share price?

Well, MNB did trade as high as 17.5c last year when it looked like mine construction was about to commence ...

But the mine build was delayed by ~12 months when the contractor in charge of the build was terminated by MNB and final construction financing was still uncertain at the time.

The market didn’t like this delay back in 2023 and the MNB share price came right down, to the point of a 7c placement in April, then to now ~5.5c where it has been trading for the last few months.

All while in the midst of a “risk off” small cap bear market that definitely wasn't helping things...

MNB now has a new construction group in place.

And two weeks ago MNB announced it is close to securing the final US$24M from banks and funds including the Angolan Sovereign Wealth Fund to build its phosphate mine, plus some extra for mine operating costs.

We think the MNB share price should materially re-rate from its current levels IF:

- MNB secures this financing package, and

- MNB shows early signs of being on schedule for the May 2025 mine completion and first production timeline.

(in other words = winning back the markets trust after last year’s construction delay)

From that announcement two weeks ago, MNB announced it is close to a total US$35M in funding package (including extra for OPEX):

- US$14M loan from the IDC (Industrial Development Corporation of South Africa)

- US$11M equity investment (Sovereign Wealth Fund of Angola and/or another fund)

- US$10M working capital facility (local banks in Angola)

With the funding package in hand, MNB can demonstrate that the mine construction is back on track for May 2025.

Moving into production, the company is expecting to earn US$55M in EBITDA per year on average.

Our view is that the MNB share price has been trading so low at ~5.5c because the market still remembers the construction delays from last year and uncertainty on final financing.

As we said above, the solution for this is for MNB to get that funding package locked away and show the market early progress in sticking to its mine construction timeline.

We have been holding MNB since 2020 and we averaged down our Entry Price by participating in the 7c placement MNB did back in April.

Over the years we have added to our Investment in MNB at 3c, 8c, 11c and that most recent placement at 7c.

(We also went to Angola to visit MNB’s project and meet the in-country team back in 2023 which increased our confidence in the project)

We averaged down at 7c in April because we think the only thing standing between MNB and the market getting back behind the company is MNB securing the final US$24M required to complete the mine build and sticking to the new construction schedule.

Our MNB Average Entry Price over four years is now ~6.4c.

MNB last traded at 5.5c.

Project financing is the key thing we (and the market) want to see next.

And then for MNB to finish construction on its mine and start selling phosphate.

It is a crucial few months coming up for the company.

We are watching closely if it can execute on some key deals to bring the project online in the next 12 months and achieve our Big Bet which is as follows:

Our MNB Big Bet:

“MNB delivers a 10x return by building a profitable phosphate project AND progressing its green ammonia project to construction phase.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our MNB Investment Memo . Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Minbos Resources

ASX:MNB

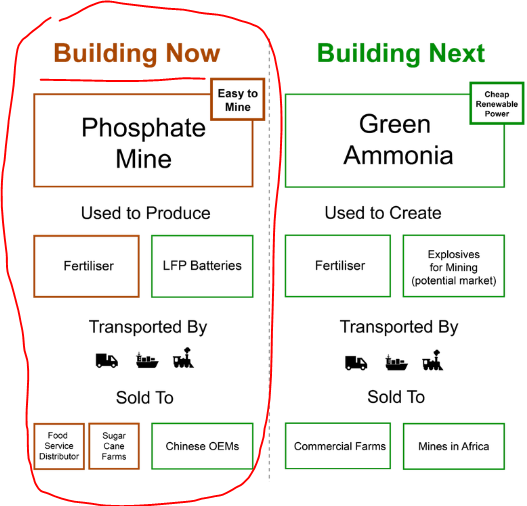

MNB actually has two key projects:

- Fertiliser project (Development Stage) - A phosphate (fertiliser) project that has an MoU for an offtake agreement with the largest agri-distribution business in Angola. This project is expected to be in production next year (and this is the one we are watching closely right now).

- Green Ammonia Project (Feasibility Stage) - A feasibility stage green ammonia project powered by some of the cheapest green energy (hydroelectricity) in the world (this is an earlier stage project that adds some nice blue sky upside for MNB).

Since our first Investment in 2020, MNB has delivered the following:

- Secured all of the land, approvals and permits for the project (including a key mining licence that the company needed to win back in 2021).

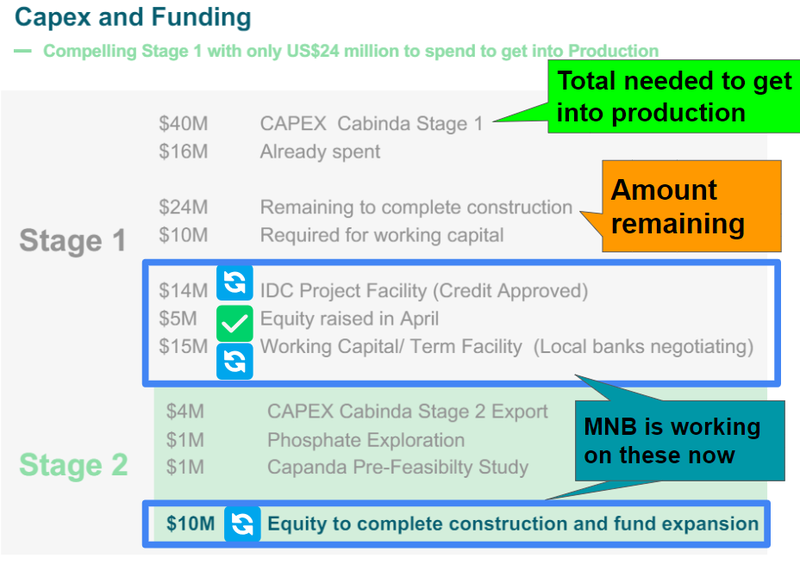

- Published a DFS that showed an NPV of US$203M with US$40M CAPEX - of that CAPEX, only US$24M remains.

- Completed engineering design and site selection for the plant.

- Secured all of the long lead items for construction.

- Signed key MoU for an offtake agreement with Grupo Carrinho for 66% of all production for the first 7 years.

- Further offtake agreements signed with large commercial farms in the region.

- Secured US$14M in conditional financing from the Industrial Development Corporation of South Africa.

- Discovered and secured a site for “Green Ammonia” project

- Signed a key power purchase agreement for the CHEAPEST renewable energy in the world (US$0.004 per kilowatt hour) for the green Ammonia project.

- Published the results of a “technical study” for the green ammonia project.

- Conducted 4 years worth of field trials to prove up and optimise its phosphate product.

Like with many companies at the “development” stage of the mining company life cycle, project delays can take the steam out of a company’s share price momentum...

Particularly when that company is looking to raise CAPEX funds in a “risk off” bear market for small cap stocks.

This is what has happened to MNB in the last 18 months.

You can see the share price movements before and after the project delays were announced:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Anyone who has been investing in early stage resource companies for over 10 years will know how hard it is to finance and build an actual producing mine.

We have been following MNB Managing Director Lindsay Reed for many years now, and have watched him overcome various hurdles in the past.

If all goes well with securing the funding package over the next couple of months, the path will be laid to finally get this mine built after many years of work and investment.

To get a sense for the sheer amount of effort that has gone into getting MNB to this point, check out these two interviews with Lindsay that were released a couple of days ago:

( Watch the Video )

Our key takeaways from the above “Part 1” of the interview with MNB’s Managing Director Lindsay Reed:

- Starts with a quick overview of the project - excellent phosphate mineralisation from surface.

- After the company acquired the project, MNB Managing Director Lindsay Reed made it to Angola, and spent 13 months in Angola during the pandemic (something which we think shows significant commitment to the project)

- The Angolan Mines Minister stepped in to ensure Lindsay could make it to the country (which we think points to strong connections between MNB and the government).

- Reed describes some of the characteristics of the phosphate rock that MNB has, and how it is amenable to a more simple production process

And below is “Part 2” of the interview with MNB’s Managing Director:

( Watch the Video )

Our key takeaways from Part 2 of the interview:

- Lindsay mentions that everything is ready to go for its phosphate project to be developed and that the only missing thing is financing - he touched on being close to two equity investments, the US$14M loan from IDC and being close to a US$10M working capital facility from local Angolan banks.

- On the sales strategy for MNB’s phosphate - Lindsay describes the need for phosphate in local markets for food security. Lindsay mentions Angola needs ~700-800kt of fertiliser and MNB will be looking to supply that need.

- This one we didn't know... Lindsay talks about how Angola was a top 10 producer of four different commodities ~50 years ago. However when MNB picked up its project it was importing over 50% of its needs.

The key takeaway from the two interviews is just how close MNB is to getting a project that has national significance into production (<12 months away).

With only US$24M in financing left to bring a project into production that would produce more EBITDA in one year (US$55M) than MNB’s current market cap (AUD $47M)...

So what has to happen next?

Get construction finance - what we want to see MNB do next

MNB has spent roughly ~US$16M so far on constructing its phosphate project - early works and long lead items ordered.

To get the project into production, the company needs to pull together another US$24M.

MNB already has a US$14M loan commitment from the IDC (Industrial Development Corporation of South Africa)

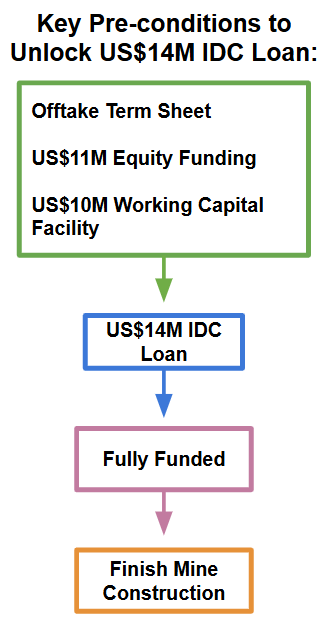

BUT for the loan to be unlocked, MNB needs to deliver four key pre-conditions:

- Project security - MNB said the securitisation process is expected to be completed in the coming weeks.

- Evidence of US$11M funding - MNB is in discussions with the Angolan Sovereign Fund (“FSDEA”) for a US$10-15M equity Investment. That on its own would be enough to satisfy this condition of the loan. MNB said site visits and due diligence were ongoing and that an update on this is expected any day now...

- Evidence of a US$10M term loan facility - MNB confirmed it had approached several banks in Angola and that the company was “well advanced in a loan application process with Banco BAI (“BAI”), one of Angola’s largest banks. MNB expects to hear back from the bank “shortly”.

- Converting the offtake MOU into a binding offtake - MNB previously announced an MOU for offtake with Grupo Carrinho ( we covered that news here ). MNB confirmed that it expected to have that MOU converted into a formal offtake agreement in the coming weeks.

Project security should be more of a formality, a legal exercise between MNB and the IDC.

However, the other three pre-conditions are key to MNB finalising the funding process that we want to see MNB announce in the coming months - in simpler terms, here’s what MNB needs:

- Complete offtake agreement with Grupo Carrinho

- Secure US$11M of equity funding

- Secure US$10M working capital facility

Once MNB closes these three key deals, it will satisfy the pre-conditions of the US$14M IDC loan and MNB will be able to commence construction on the plant, with the goal of commencing phosphate-fertiliser production in mid 2025.

In April MNB raised $5M at 7 cents per share.

We participated in this placement because we think that the MNB share price was beaten down by the 2023 project delays, plus MNB is very close to mitigating one of the biggest risks over its project - financing risk.

We think that the “project financing risk” has added to the drag on the MNB share price, and we saw the 7 cent raise in April as a good price to add to our holding.

Today, MNB is capped at just ~$47M.

We think there are three key reasons weighing down MNB’s share price right now, which we hope will shortly be mitigated:

- “Project financing risk” - the market may be pricing in MNB struggling to raise the rest of the US$24M. There are a lot of moving parts but we think that with time this will get sorted, especially considering MNB has already invested US$16M into its project...

- The construction delays - MNB had previously put out guidance to be in production by now. While we would have loved to see that happen, in all of our years Investing in the stock market we haven't seen a single project come online without any delays. We are hoping MNB can hit its new target of early/mid 2025 for first production.

- The recent capital raise - MNB’s most recent raise was a bit of a confusing one. The company went into a trading halt for a capital raise, then was suspended for a few weeks which we think may have spooked the market.

Finance and construction delays are generally expected (but not liked) from companies at this stage of the project development lifecycle.

If building a US$60M revenue per year mine was easy and without risk, everyone would do it.

But, what it does mean is a lot of volatility in the company’s share price as investors price in doom and gloom (and blue sky) scenarios along the way.

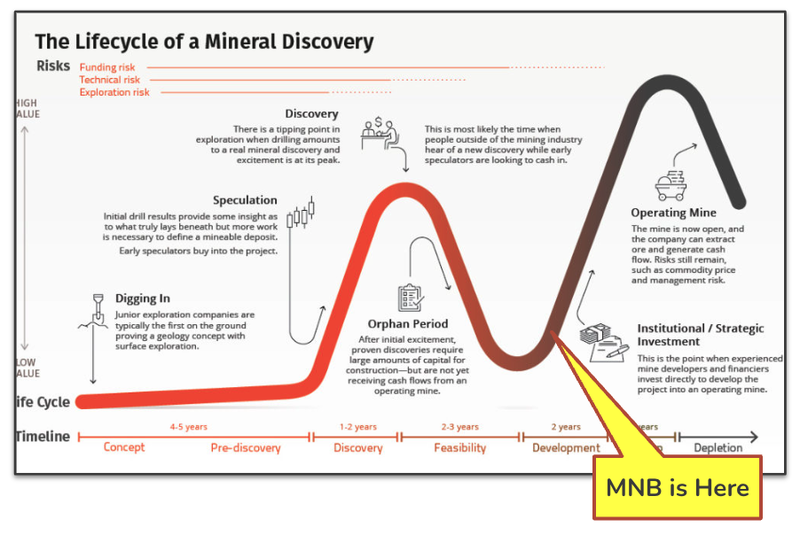

This is explained best by the Lassonde Curve, which is a model designed by famous Canadian mining executive Pierre Lassonde, that shows the typical share price cycle for mining exploration companies.

It outlines how share prices tend to rise sharply after an initial discovery, then decline during resource definition and feasibility studies before rising again as the company moves into production.

The curve helps visualise the different stages a mining company goes through from exploration to production and how the share price reacts at each stage.

MNB’s project sits right at the base at the Lassonde curve after the “orphan period” and just before “institutional investment”:

In 2023 we visited MNB’s project in Angola to tour the phosphate deposit and where the processing plant will be built.

Long lead items and key processing equipment is already purchased and waiting in a warehouse for the earthworks to be completed so it can be transported and assembled on site.

We also saw key plant parts arriving in port (this was last year in 2023):

So construction could all start happening pretty quickly, barring any further unforeseen delays.

MNB’s processing plant is not a big complex set up, so we are hoping that the construct phase is fairly smooth once the financing is secured.

here is a rendition of what the final plant will look like:

( Source )

For a deeper dive into both of MNB’s projects, check out our write up and photos of our visit to MNB’s projects in Angola here :

(Source: On the Ground in Angola: Our MNB Site Visit )

We think that there are probably a few investors sitting on the sidelines with MNB on their watchlist waiting for MNB to mitigate “project financing risk”.

Getting projects financed is always harder than expected and always takes longer than first thought.

MNB has provided guidance on funding in the past and have missed construction deadlines due to elements outside of their control.

(For example, there was trouble with the past EPCM contractor, but that is now resolved with a new Portuguese group that can be mobilised within a few weeks once the financing package is secured).

The Portuguese group is called Tecnovia which is a large construction company, with a significant presence in Angola.

Importantly, Tecnovia has an existing concrete plant operation in the Cabinda province in Angola (where MNB’s deposit and mine is located) so we think they will be well suited to construct MNB’s phosphate project. ( Source )

So, let’s take a look at how each part of MNBs financing package pre-conditions are tracking:

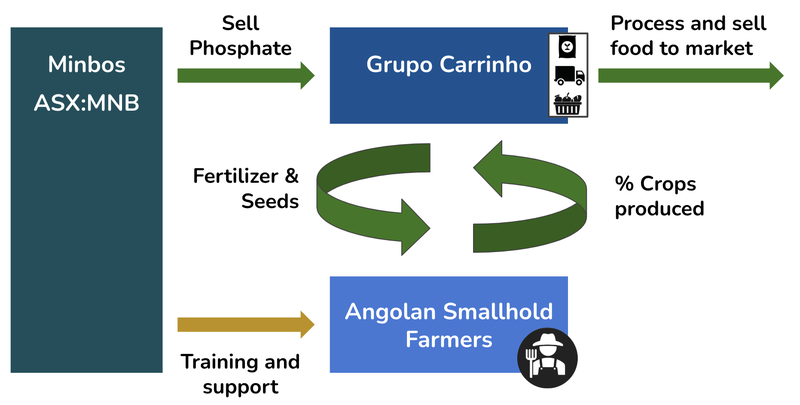

Step 1: Finalise offtake agreement with Grupo Carrinho

In July last year MNB signed an offtake MoU with Grupo Carrinho to supply up to 869,000 tonnes of Cabinda Phosphate rock over the first 7 years of production (to 2030).

The Carrinho Group is a private agri-distribution business, developing a vertically integrated supply chain in the Angolan food and agriculture industry.

Carrinho has relationships with the millions of small hold farmers in Angola that will soon (hopefully) use MNB’s fertiliser to grow crops.

This is how we see the relationship working:

This deal is big for MNB as it provides them direct access to millions of small hold farmers in Angola, but MNB only needs to deal with one central supply point.

MNB will need to convert the MoU into a formal offtake agreement, which is expected “in the coming weeks”. ( Source )

Our view is that the way the conditions are structured, MNB will probably have to finalise this one before any of the others get done, i.e without a signed offtake the banks might be unwilling to lend.

So, once we get news regarding one of the offtakes, the rest should hopefully all start to come in too...

We think the offtake will be the first key catalyst - giving other financiers certainty on forward revenues.

AND the investment by the Sovereign Wealth Fund of Angola is the second key catalyst to unlock the rest of the financing deals...

Step 2: Finalise US$11M of Equity Funding from Angolan Sovereign Wealth Fund

MNB is looking to raise US$10-15M from the Angolan Sovereign Fund.

MNB’s CEO Lindsay Reed published a video on his LinkedIn last week that shows members of the fund undertaking a site visit on the project (with Foskor, another potential offtake partner):

( Source )

According to MNB’s funding package update this month, a proposal is set to be forwarded to the investment committee of the fund by mid-July and we would hope that answer would be given soon.

From a strategic perspective, it would make a lot of sense for the Angolan Sovereign Wealth Fund to make an investment in MNB.

Angola is set to heavily invest in the agricultural sector over the next decade to diversify the country's revenue away from oil and gas - and MNB is at the forefront of agricultural innovation in the region.

Also, from a foreign investment perspective, Angola needs companies like MNB to make a return on investment as a case study of foreign investment success in the country.

At the Mining Indaba conference in Cape Town in 2023 we listened to the Angolan Minister for Mining, Resources and Petroleum talk about the importance for the country to become self-sufficient through both phosphate and ammonia.

As well as the importance of foreign investment in the country.

We have high hopes that MNB will be able to close the deal with the Sovereign Wealth Fund, given the importance of the project to the country.

In parallel, MNB has engaged an emerging market fund as an alternative or a co-investor. ( Source )

If MNB is able to secure funds from both parties it may be able to advance the phase 2 expansion of the plant set out in the DFS

The expansion is set to cost around US$3M but will double the capacity of the plant - so this will be news to look out for.

Step 3: Secure US$10M Working Capital Facility From Banks

MNB will also need to secure a US$10M term loan or working capital facility.

The company says it has met with a number of banks in Angola and is in advanced loan application with Banco BAI (one of the largest banks in Angola).

At the same time MNB is looking to get guarantees from the FGC (Angolan Credit Guarantee Fund) as part of the loan application process.

In June, as part of its due diligence, BAI visited the Cabinda mine and fertiliser production sites and inspected all imported equipment. The FGC also visited the Cabinda sites in early July 2024.

Again, we think that the importance of the project to the Angolan agricultural sector will be a big factor in the approval of the application.

MNB has not provided a timeline on when it will be approved but expects to hear back from them “shortly”. ( Source )

The next steps will be for the bank’s credit committee to approve the loan subject to security and other conditions.

IF MNB completes these three steps, what then?

Once MNB has secured these three key deals, it will unlock the US$14M loan facility with the Industrial Development Corporation of South Africa.

Together with the equity raise and working capital facility, this will give MNB enough funds to construct the plant and operating costs to run the mine, plus some working capital.

MNB has said in previous announcements that only US$24M remains to construct the project and bring it into production.

MNB can mobilise construction of the plant within two weeks of securing the funding package.

So, it is all coming to a head for MNB, and we hope that Lindsay can pull through for the final sprint towards the development finish line.

...and first production of phosphate from the mine.

What’s next for MNB’s Fertiliser Project?

The goal is for MNB to commence construction on its fertiliser in the next month or so.

In order for that to happen it will need to secure US$24M in funding.

Of this US$14M will come in the form of a loan by the International Development Corporation (IDC).

The remaining US$10M will come from institutional investors which we expect to be the Angolan Sovereign Fund.

MNB will also need a working capital facility of at least US$10M, which will come from local banks within Angola.

The pathway to construction is clear, it is now about whether MNB can execute on these deals before the construction can commence.

🔲 Complete Funding US$24M

- 🔄 Raise of US$11M from Angolan Sovereign Wealth Fund

- 🔄 Secure a US$10M term loan with Angolan Bank

- 🔄 Convert Grupo Carrinho MoU into a signed offtake agreement

- 🔄 Finalise US$14M loan with the IDC

🔲 Commence Construction

According to the interview that Lindsay Reed did with Crux Investor , MNB will use a local Portuguese group to undertake the construction of its flagship fertiliser plant.

Although no contract has been signed, Lindsay is confident that the team can “be mobilised within two weeks” to commence construction, once the funding has been secured.

Once all of the funding is in place, construction can start straight after.

🔲 First production from phosphate fertiliser project

MNB is targeting first production in Q2 2025 in order to ensure Grupo Carrinho has the majority of its product requirements for the 2025/26 growing season.

Ultimately we hope that as MNB ticks off these catalysts and brings its project into production, the company’s share price re-rates higher as per our Big Bet which is as follows:

What are the short term risks to MNB?

Phosphate / Fertiliser Project

For MNB’s phosphate/fertiliser project the short term risks are “project financing risk” and “delay risk”.

MNB has a relatively small CAPEX funding gap that needs to be filled and so will need to try and secure additional funding to complete construction works and get its project into production.

There is a risk that the final funding package takes longer than expected to secure OR isn't secured at all, which forces MNB to pivot in its development strategy.

Any delays from a funding perspective could impact the time it takes for MNB to get to first production (and revenues) from the project.

Delays with construction could also further hurt the MNB share price. MNB has faced delays before and the market may punish MNB if further delays happen.

Green Ammonia Project

In terms of MNB’s green ammonia project - the key short term risk is “project feasibility risk” and “funding risk”.

With MNB entering the feasibility stage, the biggest risk comes around technical and commercial aspects of the project such as:

Big infrastructure projects, such as an ammonia plant, are complex to design and construct.

So, after completing a PFS, MNB may find itself in a position where it needs to find a large financing partner to commit large amounts of capital to get the project off the ground

This funding risk is relevant for all large projects of this kind.

Therefore, MNB will need to demonstrate that the project economics stack up AND all of the technical, environmental, legal and feasibility risks are mitigated.

For a deeper dive into both of MNB’s projects, check out our write up and photos of our visit to MNB’s projects in Angola here :

(Source: On the Ground in Angola: Our MNB Site Visit )

Our MNB Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time

Below is our MNB Investment Memo , where you can find the following:

- What does MNB do?

- The macro theme for MNB

- Our MNB Big Bet

- What we want to see MNB achieve

- Why we are Invested in MNB

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.