$31M Capped CCZ Confirms Same Geology as $148M Capped Neighbour COB

Published 02-MAY-2018 10:00 A.M.

|

15 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

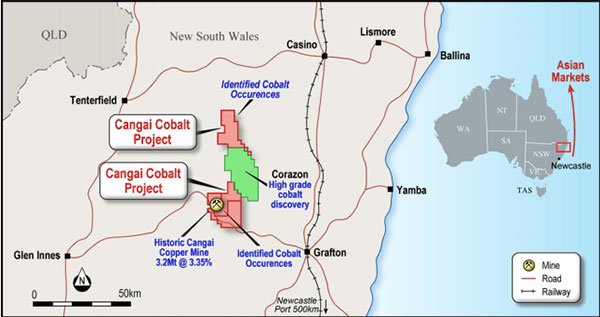

The ASX polymetallic junior we’ve got our eye on today is chasing what could very well be the holy grail of commodity cocktails: big servings of cobalt and copper, with the potent addition of zinc, silver and gold thrown into the mix.

With a sharp eye fixed on the electric vehicle-powered revolution, in which battery metals like cobalt and copper take centre stage, Castillo Copper (ASX:CCZ) has meticulously selected two major plays in covetable NSW hot-spots.

The first of these is the Broken Hill Cobalt Project, which has an immediate advantage — it sits only 2.6 kilometres away from $148 million-capped Cobalt Blue’s (ASX:COB) Thackaringa Cobalt Project JV, and shares the same land-owner and can now confirm the same geology. Interestingly, COB owns just 51% of the project, whilst CCZ has 100% ownership.

As CCZ announced to market just this week, all six highly prospective targets identified at Broken Hill display the same Himalayan Formation geology to COB’s Thackaringa deposit. This style of mineralisation makes for easy extraction and reduced operation costs.

Interestingly, COB recently inked a cobalt offtake deal with global giant, LG International, to the tune of US$6 million+.

CCZ, which is currently valued by the market at a modest $31 million, and is practically rubbing shoulders with COB’s 61,000-tonne contained cobalt deposit, is hoping for similar success.

A recently completed desktop study at Broken Hill analysed historic data, identifying promising areas of prospective cobalt mineralisation. With these six pre-selected sites in mind, a team of field geologists have been deployed for a series of high-impact exploration works, including reconnaissance mapping and rock chip sampling.

Broken Hill is a mining town, an amply mineralised location that made BHP the powerhouse it is today. It has an expansive exploration history and is now on the verge of a new (cobalt) mining boom.

CCZ has compiled a plethora of historical data, including aeromagnetic surveys and samples. Yet parts of this area have been largely unexplored on account of the presence of alluvial sands, so there could also be a whole lot of upside to be had here.

However, this is an early stage play here and investors should seek professional financial advice if considering this stock for their portfolio.

Mapping and geochemical work is well underway and when reconciled with geophysics interpretation, will be key in shaping the design of an inaugural cobalt-focused drilling program. This is critical work, especially given Broken Hill’s emerging profile as a cobalt supply chain hub.

Yet the more advanced project in CCZ’s arsenal, however, is a polymetallic play in northeast NSW.

This ASX explorer is looking to revive the historic Cangai Copper Mine as its central priority. The mine, which is part of the broader Cangai Copper-Cobalt Project in a region with known cobalt-copper systems, has been the subject of intense exploration since the early 1900s. But it was abandoned on account of unfavourable market sentiment and Rio Tinto’s takeover of Conzinc Riotinto of Australia (CRA).

Today’s forward-focused company has reopened the mine and is looking to breathe new life into it: a polymetallic resurrection, if you will.

This area has historically shown exceptionally high grades of mineralisation. If you consider that the average for copper mineralisation around the world sits at grades of around 0.6%, Cangai is something of a legend, having served up grades of some 25-35%.

Historical exploration has not really given cobalt much air-time, given that the EV-fuelled cobalt boom is a fairly recent one. However, all signs are pointing to rich cobalt mineralisation at Cangai.

An updated desktop review has recently identified new primary cobalt targets at Cangai, highlighting that CCZ’s ground has occurrences more than 300 ppm cobalt at surface.

An initial drill program has also been completed with some excellent results grading up to 2.9% copper and 2.5% zinc. And CCZ is now on the verge of kicking off a second drill program, which will begin at the end of May.

An aim of the drill program is to expand the current JORC (2012) compliant Inferred Resource at Cangai of 3.2 million tonnes at 3.35% copper — as it stands, already one of Australia’s highest grade copper Resources.

Also boding well is the presence of very rare supergene ore, which suggests at the presence of an enriched copper Resource. The supergene zone is the richest part of the ore deposit and is close to surface. Mine records show that Cangai has up to 35% copper.

The presence of supergene ore means it can be shipped directly to key export markets at relatively low cost via excellent infrastructure already in place — a distinctly competitive advantage.

Also supportive of CCZ’s potential is that copper and cobalt are key ingredients in renewables technology, including lithium-ion batteries and electric vehicles (EVs). In fact, close to half of all cobalt produced is used to produce the batteries that power electronics and electric cars.

The EV-powered future is moving at a lightning-fast pace with the global EV battery market set to grow at a compound annual growth rate (CAGR) of 42% in the five years from 2017 to 2021.

With that in mind, today’s $22.6 million-capped explorer could very well be in the right place, at the right time.

Unveiling:

Castillo Copper (ASX:CCZ) is a story that’s packed with tightly honed strategy: it’s about impeccably selected commodities, high-quality fundamentals, and auspicious “nearology”.

With a focus on the thriving battery metals rally, CCZ has in its arsenal a selection of NSW projects that are highly prospective for cobalt and copper, but also show healthy signs of zinc, silver and lead mineralisation.

CCZ also has promising assets and exploration concessions in Queensland and Chile, but today’s article focuses on its NSW cobalt-copper prospects: its priority revival of the Cangai Mine, and its six key targets in Broken Hill.

CCZ’s strategy is simple but effective: to aggressively expedite production and generate cash-flow by using third-party processors within range of its project areas, and selling on the end-product.

The short video below gives a good idea of CCZ essentials:

As will become clear, CCZ is leveraging some prime real estate, and setting counts for a lot here. So let’s get straight to the crux of the matter and take a closer look at CCZ’s cobalt play in Broken Hill — the site of the most recent news...

The Broken Hill Cobalt Project: six highly prospective Himalaya-style targets

CCZ’s Broken Hill Project is situated 17 kilometres west of the historic Broken Hill mining centre. This prolific NSW region is steadily emerging as a new global supply chain hub, especially given current cobalt sentiment.

Broken Hill is considered to be the heartland of NSW mining, and is believed to contain one of the largest undeveloped cobalt reserves in the world. Previous exploration here has primarily focused on traditional Broken Hill mineral systems — zinc, lead and gold — but with the burgeoning demand for battery-grade minerals, the economics are increasingly favourable for cobalt.

Speaking of which, as we’ve mentioned, CCZ’s holdings are situated in close proximity to Cobalt Blue’s 60 square kilometre Thackaringa deposit.

Thackaringa is one of the most advanced cobalt deposits in the world, hosting 61,000 tonnes of contained cobalt, and CCZ’s tenements share the same geological formation and landowner. In fact, CCZ actually has within its grasp a larger land holding.

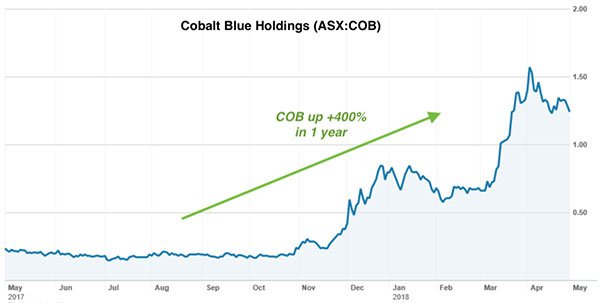

Here’s a look at how COB has performed over the past 12 months:

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

As we also mentioned, COB has clinched a strategic US$6 million partnership with major battery manufacturer, LG, aimed at sourcing long-term supplies of battery-ready cobalt...

Given that CCZ’s tenements are only 2.6 kilometres away from COB’s, this kind of high-profile deal could be a sign of things to come for this emerging explorer.

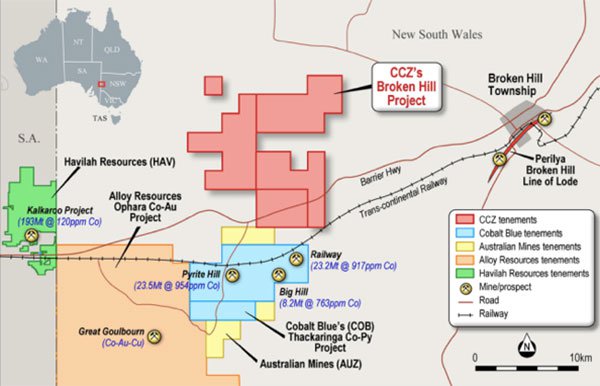

In the map below, you can see where CCZ’s holdings (marked in red) are situated in relation to COB’s (in blue):

As you can see, CCZ’s tenements are also near Havilah Resources (ASX:HAV), which has confirmed cobalt resources here. The neighbouring Alloy Resources (ASX:AYR) and Australian Mines (ASX:AUZ) have also recently revealed encouraging exploratory results in the area. HAV has reported 193.3Mt at 120 parts per million of cobalt.

Also boding nicely for CCZ is that its project is situated right on the trans-continental railway. Should the company be able to develop a first-class asset, this will be an excellent location for shipping material to market.

With the cobalt price now sitting at around US$85,000 per tonne, CCZ is keen to fast-track its exploration program to ascertain the full extent of cobalt mineralisation across the tenure, with a focus on targeting known host mineralised areas.

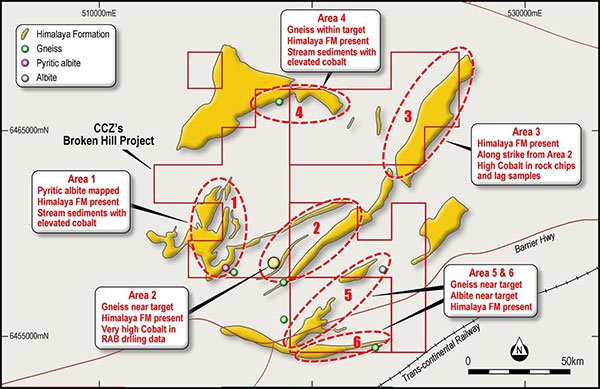

CCZ’s geology team has identified six key areas here, all with the same Himalaya Formation geological sequence apparent at COB’s Thackaringa deposit. This is favourable because this kind of mineralisation is easy to extract, making for a potentially lower cost, faster operation.

A team of field geologists have now been deployed to Broken Hill to kick off reconnaissance mapping and rock chip sampling over these six identified priority targets:

These six targets were selected after thoroughly analysing five data sets which were compared to peers’ deposits with known geology and confirmed cobalt mineralisation.

The CCZ geological team has met with the landholders and gained access for preliminary exploration. Following the completion of the initial field reconnaissance, CCZ will undertake a follow-up sampling program.

The geology team at work:

The ultimate objective here is to derive sufficient first-hand data to design an inaugural cobalt-focused drilling program.

While CCZ’s chief priority is revival of the Cangai Copper Mine, with a relatively large footprint in a region that’s rapidly emerging as pivotal global supply chain hub for speciality metals, it’s gaining a strong understanding of the underlying geology and extent of cobalt mineralisation.

Intriguingly, there’s also material exploration upside within the tenure, as some 75% is covered in alluvial sand, especially significantly where the outcrop is visible, with legacy assay results indicating the presence of cobalt.

All in all, things are tracking well here, and CCZ has the distinctive benefit of being situated in the thick of bustling mining activity.

Let’s take a look now at the more advanced project in CCZ’s arsenal...

Resurrecting the Cangai Copper Mine

As we’ve mentioned, CCZ’s first priority is reviving the historic Cangai Copper Mine in NSW, which is part of the Cangai Cobalt-Copper Project. Importantly, this project sits on an ultramafic system that is well-known for high-grade copper and cobalt.

The Cangai mine operated between 1904 and 1917. Western Mining and CRA Exploration both reviewed the mine at separate times in intervening years, but didn’t progress the project due to tough economic conditions.

A snapshot of the mine back in the 1910s:

Cangai was mined mostly by hand and by small tools, producing up to 13% of copper. For those of you who aren’t geologists, these kinds of grades are veritably off the chart.

The Cangai Project has been largely underexplored for cobalt. However, historic mining activities provide clear evidence for the presence of cobalt mineralisation. Legacy mining reports document the presence of cobalite, which resulted in its inclusion in the Mineral Resource estimate.

The Cangai Copper Mine has an exceptional high-grade JORC 2012 Inferred Resource derived from 3D modelling of legacy data at 3.2mt at 3.35% cobalt, representing circa 108,000 million tonnes of contained copper.

Here’s a very short tour of the mine:

And here’s where CCZ has set its sights:

CCZ’s initial drilling program produced some exceptional results, with significant massive sulphide mineralisation drilled at the historic mine. Outstanding drilling logs confirmed that seven out of eight and a half drill-holes intersected sulphide mineralisation, with the best intersecting 30 metre thick mineralisation in an untested area, between two known JORC modelled lodes.

Finfeed.com (a related entity of S3 Consortium) reported on this first drill program back in February:

A recently updated desktop review also identified new primary cobalt targets, which builds on currently known occurrences.

Promisingly, that review revealed that CCZ’s ground has occurrences more than 300ppm cobalt at surface — that’s 150ppm higher than CCZ’s neighbour Corazon’s (ASX:CZN) latest soil sampling program across four new target areas (you can see where CZN is situated in relation to CCZ in the map above).

The new primary cobalt targets were the culmination of an onsite strategic review at the project. While CCZ is focused on reopening the Cangai mine, it’s also keen to garner a greater understanding of the extent of cobalt mineralisation across the entire tenure.

With high cobalt soil anomalies in the project area, CCZ is in a prime position to aggressively explore these zones. Using a similar strategy deployed by CZN at its Cobalt Ridge tenements, CCZ plans to expand the geochemical soil sampling across the combined Cangai cobalt-copper tenure to identify incremental cobalt targets and extend the current focus areas.

Moving forward, the next steps here are reviewing geophysics, follow-up geochemistry and field geological mapping.

A second drill program will kick off at the end of May, and there are still more assays to come from the first drill program. All of this translates into a torrent of news flow for CCZ, so this could well be a company we track closely in the months to come.

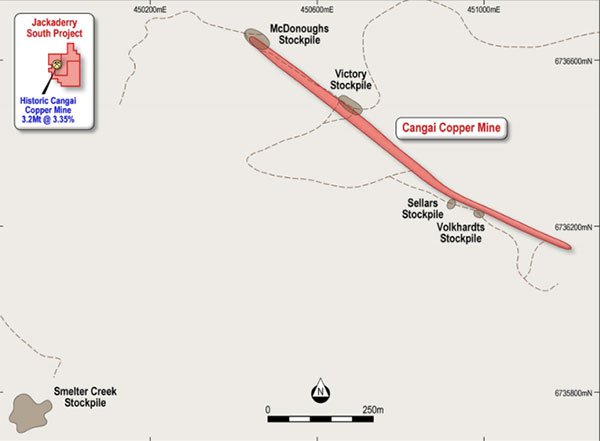

A competitive edge: monetising legacy stockpiles and supergene ore

As we touched on earlier, a significant point of difference for CCZ is the presence of supergene ore at Cangai, whose discovery is a game-changer.

Mine records show that supergene ore occurred with azurite and malachite ore grading at 20% to 35% copper, 10% zinc and elevated cobalt levels. The ore occurred close to surface, passed into chalcocite ore with a similar grade below surface, and is open in all directions — this translates to significant exploration upside.

Another advantage? This supergene is similar to that held by the $1.25 billion-capped Sandfire Resources (ASX:SFR), the second largest copper-gold producer on the ASX.

Of course, CCZ remains a speculative stock and investors should seek professional financial advice if considering this stock for their portfolio.

Sandfire’s DeGrussa operations have had six years of consistent, safe and profitable production and is now looking at 63-66kt of production this year.

The supergene ore, in turn, can be easily transported to Newcastle port via excellent infrastructure already in place, saving significantly on operating costs.

As CCZ hones in on additional longer-term exploration at Cangai and revives the historic mine, legacy stockpiles could provide a direct route to early cashflow generation in the meantime.

There are five stockpiles along the line of lode and at the historic smelter, with high-grade mineralisation. Given that pXRF readings from one stockpile returned up to 18% cobalt, 7.9% zinc and 1,300 ppm copper, these will all be bulk sampled in the near future.

The five legacy stockpiles at the Cangai mine are shown in the map below:

To maximise value from these legacy stockpiles, CCZ has appointed Hetherington Exploration and Mining Title Services to navigate the fastest route to monetisation.

Whether it ends up directly shipping the ore or transporting it to domestic third-party processors, CCZ will benefit from the mine’s close proximity to pre-existing transportation infrastructure.

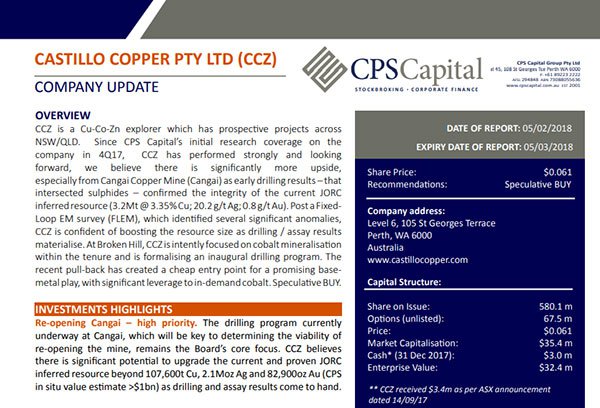

CCZ a “Speculative Buy”

While CCZ has a market cap of just $31 million, it has attracted broker attention. In February, stock broking firm CPS Capital published a research report on the company, tagging it with a ‘Speculative Buy’ recommendation.

It should be noted that broker projections and price targets are only estimates and may not be met. Those considering this stock should seek independent financial advice.

The report notes CCZ’s high quality fundamentals including:

1) upside at Cangai as the drilling program progresses that should materially build on the >$1bn in situ resource value; and,

2) leveraged exposure to in-demand cobalt through significant exploration upside at the Broken Hill assets.

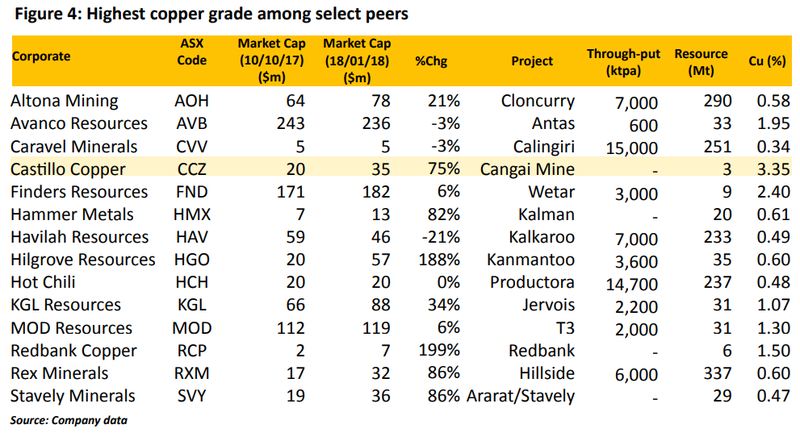

The broker also highlighted that fact that CCZ has the highest copper grade amongst its peers...

A cobalt boom

Also in CCZ’s favour is a thriving cobalt rally that doesn’t seems to be in danger of slowing down any time soon, with demand far outpacing supply.

We’ve written extensively about the rapidly expanding EV and lithium battery markets here at The Next Mining Boom, and you probably already know that cobalt — one of the key lithium-ion battery ingredients — plays a central role in this movement.

After a powerhouse performance in 2017, cobalt prices have risen steadily since the beginning of the year, driven by tight supplies and strong downstream demand from the aerospace and medical sectors, as well as EV production.

Current cobalt sentiment is echoed in headlines like these:

Of course commodity prices do fluctuate and caution should be applied to any investment decision here and not be based on spot prices alone. Seek professional financial advice before choosing to invest.

Given this highly favourable commodity climate, CCZ’s timing could scarcely be more apt... and it’s looking for this high-demand metal in two abundantly mineralised regions with considerable exploration upside, one of which is currently emerging as a new supply chain hub.

The polymetallic future...

...is looking bright as can be for CCZ.

It’s still early days for this $31 million-capped ASX polymetallic junior, but as you can see, the fundamentals are all in very good shape.

This company has in its arsenal some first-class assets in two renowned mining districts, sharp leverage to COB’s ample Thackaringa discovery, and a finely honed strategy for early cashflow generation.

All of this comes together nicely for CCZ as it looks at a cluster of near-term catalysts square in the eye — these include drilling approvals for Cangai, remaining assays to return from the initial drilling phase, and a second high-impact drilling program. And here at the Next Mining Boom, we’ll be hanging out to see what this canny ASX junior does next.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.