$18.7BN Pro Medicus announces $20M funding for EIQ. Same Pro Medicus deal that saw 4DX rise 33x in ~8 months?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 802,332 EIQ Shares at the time of publishing this article. The Company has been engaged by EIQ to share our commentary on the progress of our Investment in EIQ over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

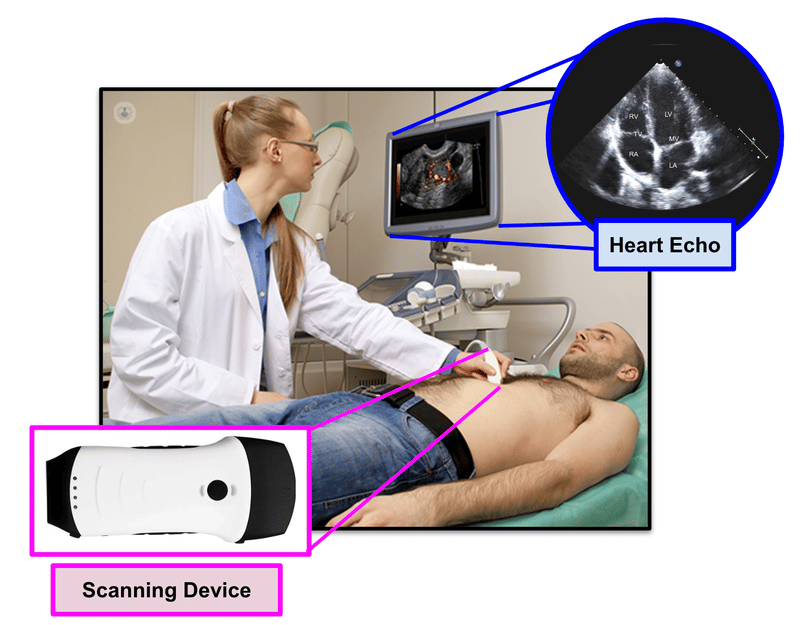

Our Investment EchoIQ (ASX:EIQ) is a heart imaging medical technology company.

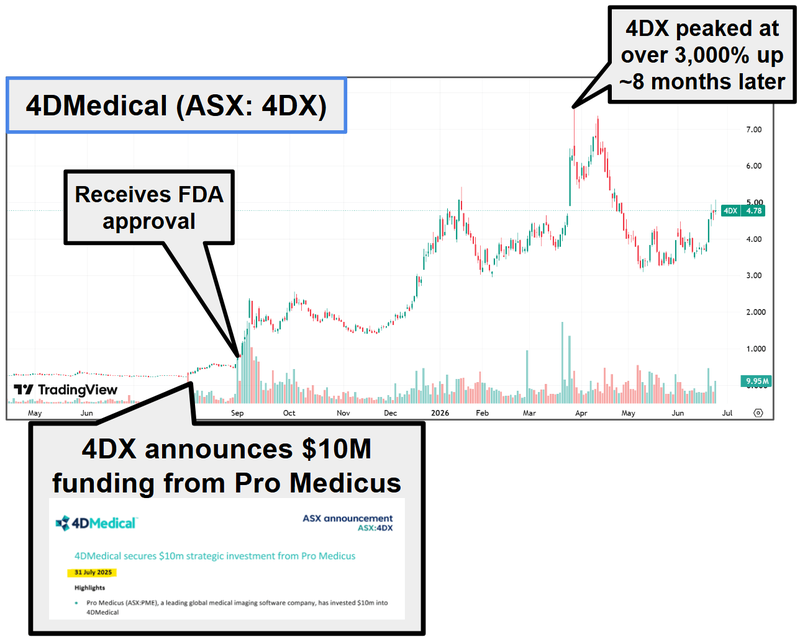

Remember when lung imaging medical technology company 4D Medical (ASX: 4DX) went up over 3,000% to a ~$4BN market cap in ~8 months?

This happened after $18.7BN Pro Medicus (one of the world’s leading healthcare imaging software companies) invested $10M into 4DX.

🚨THIS MORNING:

Pro Medicus just announced up to $20M in proposed funding into our heart imaging stock EIQ.

(past performance is not an indicator of future performance)

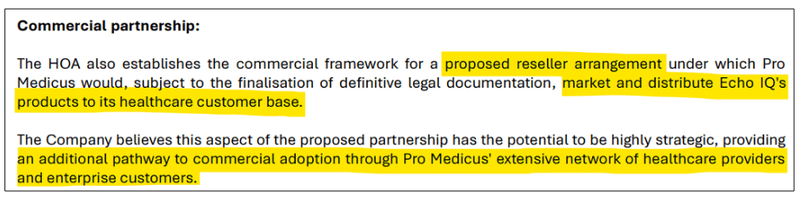

EIQ also gets a reseller agreement giving access to Pro Medicus’ global hospital client base, built over decades, under the just signed binding Heads of Agreement...

And product validation from a global leader in medical imaging enterprise-scale software solutions, one of the most successful on the planet.

So what could be next for EIQ?

Here’s the “4DX after Pro Medicus invested” timeline:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The 4DX share price tripled in the weeks AFTER the Pro Medicus investment was announced.

The price chart shows that the SECOND price run trigger after Pro Medicus invested was 4DX announcing US FDA clearance

Like 4DX was at the time of its Pro Medicus deal, EIQ is very close to finding out if it has secured US FDA clearance for its AI Heart Failure detection tech.

EIQ’s FDA decision is pending for its Heart Failure detection tech and could come in any day now...

So it looks Pro Medicus is going for a similar 4DX play book with EIQ.

A strategic investment on the cusp of a US FDA approval decision...

(Even though the past performance of 4DX post Pro Medicus Investment is not an indicator of what EIQ will do post today’s Pro Medicus Investment)

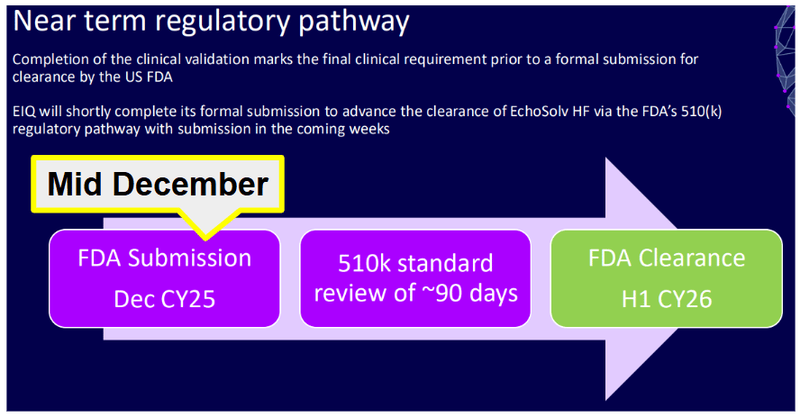

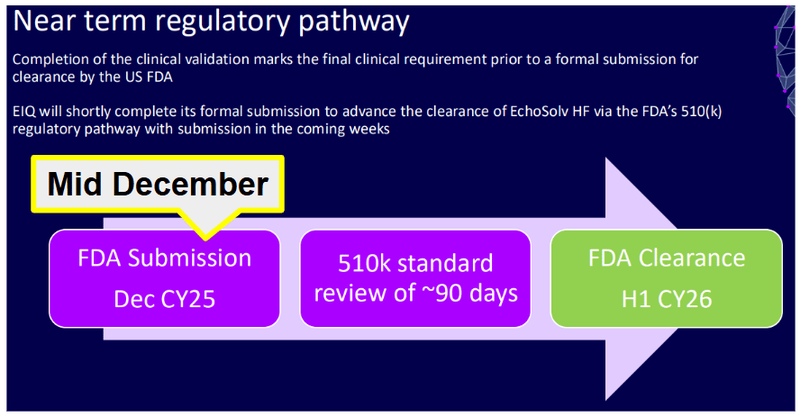

EIQ submitted its FDA application (a "510 k") for Heart Failure in mid-December 2025.

The FDA's average review window is ~90 days - that window has well and truly passed.

EIQ's guidance for a final decision was “this half of 2026”.

Technically that means we could see something over the next ~5 days.

(source)

IF the FDA clearance comes in then the reseller part of the Pro Medicus deal comes into play which would see Pro Medicus market and distribute EIQ’s products to its customer base.

(source)

We think that part of the deal is massive for EIQ because Pro Medicus has spent decades building up its network of customers - and overnight EIQ would get access to that network.

Pro Medicus sell enterprise-grade medical imaging software so its a pretty similar customer base to what EIQ would be looking to sell into:

(source)

So what happens now?

We think EIQ has just set itself up to deliver the exact same one-two punch combination that happened right before 4DX’s parabolic run to a multi billion dollar market cap.

In August 2025 the $10M financing deal was signed between Pro Medicus and 4D Medical. (source)

4DX’s share price went up ~42% that day.

Then in September 4DX received FDA clearance for its lung imaging tech.

And only two days later received US reimbursement for the same tech.

After those two announcements 4D Medical’s share price went up 400% in 6 days.

Again - the past performance of 4DX is not an indicator of the future performance of EIQ.

4DX kept running, closed a $150M institutional capital raise in January this year, another $89M placement at a premium to the last raise in March and made its way into the ASX 200 index and hit an all time high of $7.55 in March this year.

All of that while expanding its tech into the US and EU...

From its April 2025 low of 23 cents, that's a ~33x move in under 12 months, to a peak market cap around ~$4BN.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think EIQ has set itself up in a stronger position to where 4DX was before it received FDA clearance for its lung imaging tech.

EIQ, potentially days, before an FDA decision for its Heart Failure detection tech, has:

- A binding heads of agreement with funding from Pro Medicus for up to A$20M.

- A proposed reseller agreement with Pro Medicus (access to a customer base built over decades across the world)

- A distribution deal with Mayo Clinic - the #1 ranked hospital system in the US. That deal was signed BEFORE an FDA decision by the same hospital system where EIQ did all of its testing (a good validation signal for us)

- AN existing reimbursement code - EIQ’s already got a plan to access an existing reimbursement code that’s available for its Heart Failure tech (which means quicker pathway to revenues).

- Over 20 months of work building a distribution network in the US - which we laid out in detail in our last note here -

The only thing that needs to fall into place is FDA clearance for EIQ’s Ai Heart Failure detection tech.

And we think that an FDA decision on EIQ's AI detection of Heart Failure tech could happen ANY day now.

Technically if it's going to happen in H1-2026 then that’s within the next ~6 days.

(source)

There is no guarantee’s EIQ receives FDA clearance, but we did publish the 6 reasons why we think EIQ's tech has a good chance of getting cleared by the FDA in our last note here.

Here is a quick overview of those reasons (the details are later in today’s note too).

- EIQ has ONE FDA cleared AI algorithm already (so it knows what's needed to get a second)

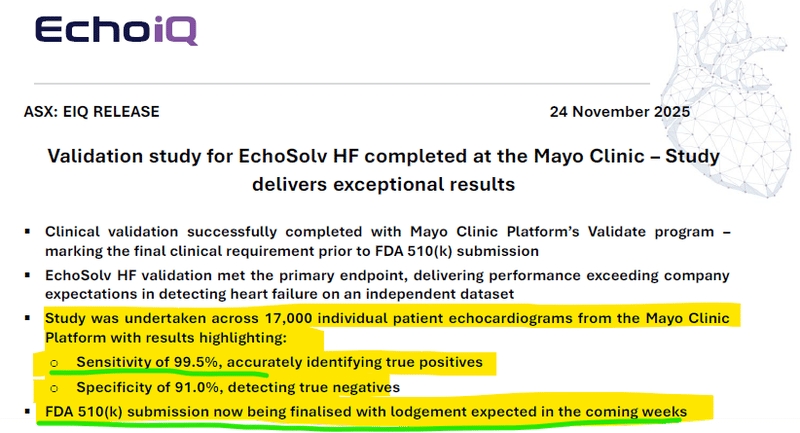

- EIQ's clinical data is strong (99.5% sensitivity, 91.0% specificity - validated by Mayo Clinic on 17,000 patient echocardiograms)

- EIQ's data looks stronger than tech that is ALREADY FDA cleared.

- EIQ's tech is much better than the current standard of clinical practice (which catches only ~50% of heart failure cases)

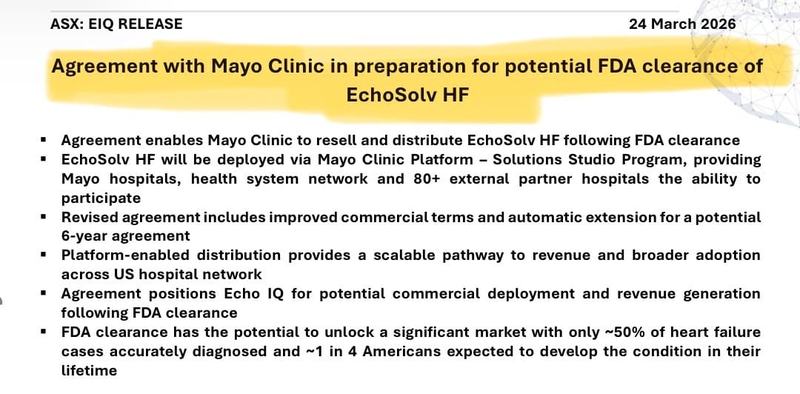

- Mayo Clinic signed a distribution deal BEFORE FDA approval (to resell EIQ's Heart Failure AI across 80+ partner hospitals)

- Cardiology is the #2 most-cleared FDA category for clinical AI (200+ algorithms cleared)

The Heart Failure could be EIQ’s second FDA cleared product

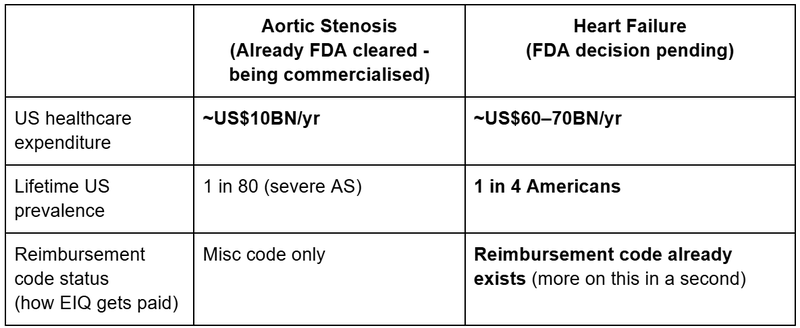

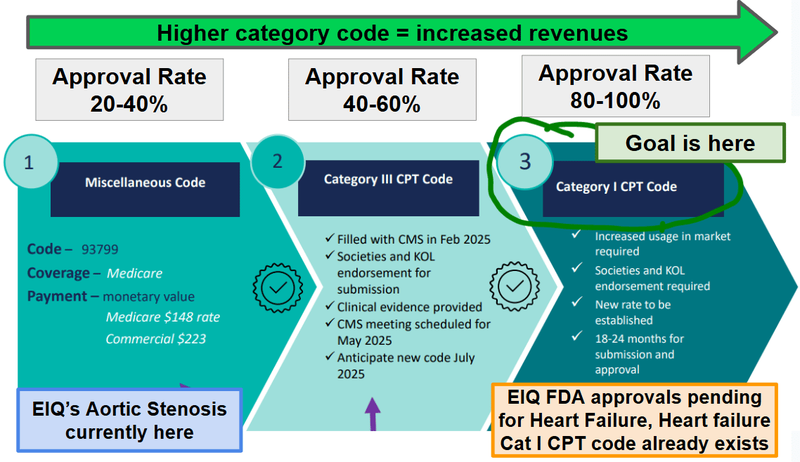

EIQ’s already got FDA clearance for its Aortic Stenosis detection tech which it’s currently rolling out across the US.

(The FDA cleared that tech back in October 2024)

Aortic stenosis is a type of heart valve disease where the aortic valve narrows, preventing it from opening fully.

Heart Failure detection could be the game changer for EIQ because of how much bigger a market it is for EIQ.

Here they are side by side for some context:

So the size of the prize for Heart Failure is a lot bigger (a lot bigger).

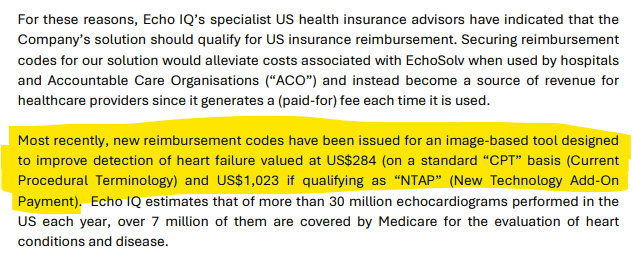

But the much bigger positive difference to EIQ is that there is an existing reimbursement code EIQ can piggy back off of.

More on what a reimbursement code is later in today’s note, for now, think of it as the government paying for each time EIQ’s tech gets used.

(Sort of like when you go to see a GP, show them a medicare card and just walk out and the GP still gets paid)

Having an existing reimbursement code in place means EIQ COULD skip a process that could have taken years to get to.

AND it means EIQ can start generating revenues every time its tech is used.

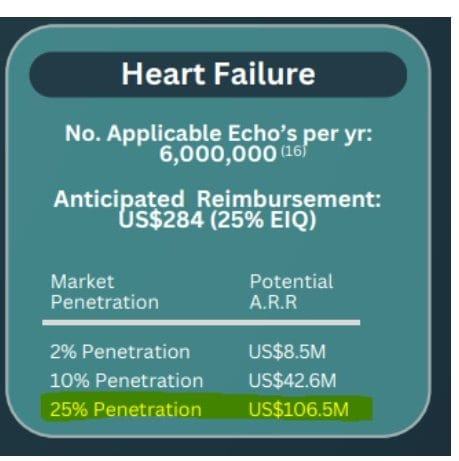

For heart failure, the existing reimbursement rate is ~US$284 for “an image-based tool designed to improve detection of heart failure tech” and US$1,023 if qualifying as (New Technology Add-on Payment).

(Source)

Even if we take the lower US$284 rate, with EIQ receiving 25% of that fee (the rest going to the hospitals/clinics using it).

Based on the ~6,000,000 echocardiograms done every year in the US, assuming 25% of scans use EIQ’s tech that is US$106.5M in revenue to EIQ per year...

(source)

Of course this is just potential revenue on market size and some assumptions on reimbursement. It is entirely speculative - EIQ has not really turned on the revenue tap at all yet, and there’s still things that can go wrong here.

IF EIQ can start to prove to the market those revenues are achievable it could start to attract the sort of valuations 4DX and Pro Medicus have attained.

Especially considering EIQ has already flagged that its tech that can be adapted to other heart diseases after that - hypertension, hypertrophic cardiomyopathy and more.

4D had $5.9M revenue in FY25 and trades at a $2.85BN market cap. (source)

Pro Medicus had $213M revenue in FY25 and trades at a $18.7BN market cap. (source)

Both are good examples of what the markets are willing to pay for growth in the medtech space.

IF EIQ can get anywhere near those revenue numbers from earlier on its Heart Failure tech then the market might start applying a similar revenue multiple to the stock.

(and surely there would be an AI premium for EIQ too)

However there are no guarantees EIQ will grow like 4D Medical and Pro Medicus have done.

Why we think EIQ could start to deliver revenues a lot quicker than the market is expecting

As mentioned earlier, EIQ already has its Aortic Stenosis detection tech cleared by the FDA.

(since October 2024)

Ever since then EIQ’s been building out a distribution network across the US for that specific technology.

18 months on the road selling AI tech to the same group of customers who would be interested in the Heart Failure tech.

(Cardiology clinics, hospitals and health networks)

Here is how its played out:

- DONE: Get FDA clearance for Aortic Stenosis. (Done - October 2024.)

- UNDERWAY: Quietly roll out the Aortic Stenosis tech across as many US hospitals and imaging networks as possible. (18 months and counting)

- DUE ANY DAY: Get FDA clearance for Heart Failure. (Decision pending - could land any day now.)

- NEXT: Switch on Heart Failure across the entire Aortic Stenosis distribution network. (Pre-positioned - instant rollout once clearance lands.

It’s almost as if EIQ’s been pre-selling the Heart Failure tech for the last 18 months...

And here is the distribution network EIQ’s put together:

- Mayo Clinic - (pre-signed) Heart Failure reseller across 80+ external partner hospitals.

(yes for the Heart Failure tech - before FDA approvals... more on this one in a second)

- Mount Sinai Health System - most recent deployment, NY's #1 cardiology hospital network with 400 outpatient practices and over 3,760 years beds

- SARC MedIQ - reseller agreement covering 300+ US healthcare facilities and clinics, 1,500+ physicians.

- Beth Israel Deaconess Medical Center (BIDMC) - Top 1% for cardiology in the US. ~30,000 echocardiograms annually.

- ScImage - Enterprise imaging platform with ~1,200 active users across the US.

- MedAxiom - Commercial partnership (in conjunction with ScImage) across 36 affiliated hospitals and practices.

- Cassling Diagnostic Imaging - Imaging services across the US Midwest, South and West.

- Respiri - licensing agreement integrating EchoSolv into Respiri's US Remote Patient Monitoring offering, focused on the Accountable Care Organization (ACO) sector treating Medicare patients.

- And then TODAY: A proposed reseller agreement with $18.7BN Pro Medicus - who have spent decades building a network to sell imaging software all over the world.

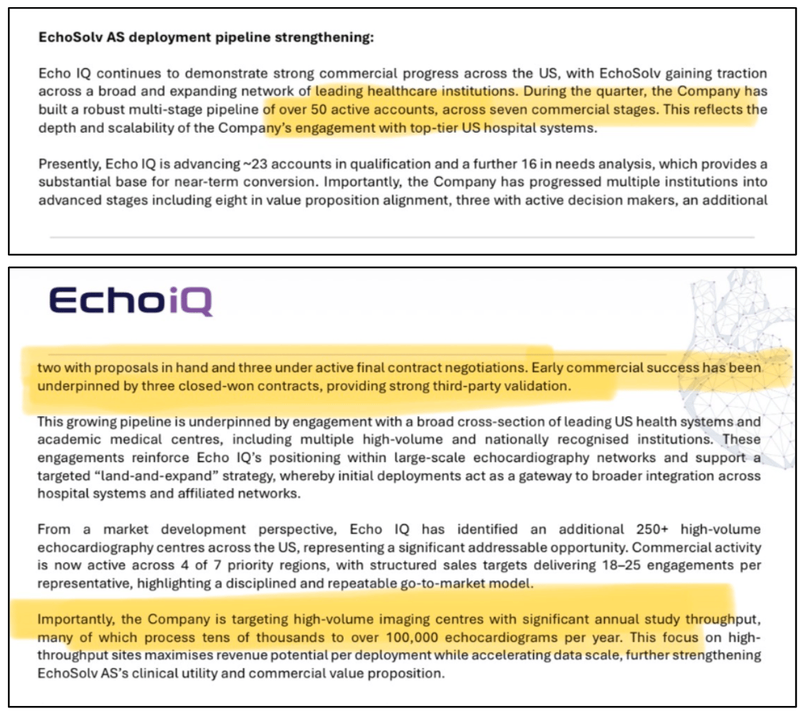

On top of all of that, EIQ’s latest quarterly showed 50 active accounts in its sales pipeline and said it was explicitly targeting networks where echocardiograms were in the 100,000s.

(source)

As soon as EIQ gets approvals for its Heart Failure detection tech it can plug and play it all into the above networks.

Which puts EIQ in a position to switch on revenues a lot quicker than it has done for its Aortic Stenosis tech.

As mentioned earlier the Heart Failure tech already has a Category 1 reimbursement code which is the holy grail (where reimbursement approval rates are 80-100%).

EIQ’s Aortic Stenosis is currently being billed under a "Miscellaneous" code (93799) which requires more paperwork and has a far lower reimbursement approval rate (~20-40%).

(source)

The risk is that EIQ’s tech is not eligible to piggy back on that code but given the code is for “an image-based tool designed to improve detection of heart failure” tech. (source)

We are liking EIQ’s chances.

Why we think EIQ’s Heart Failure tech is in a strong position to get FDA clearance in the coming weeks

So whilst it's a major positive share price catalyst if EIQ gets FDA clearance, at the same time the obvious risk is that the FDA does not clear its Heart Failure technology.

Here are the 6 reasons why we think EIQ’s tech has a good chance of getting cleared:

(Before we begin - we are biased as optimistic shareholders and could be wrong)

1. EIQ has ONE FDA cleared AI algorithm (so the company knows what needs to be done to get a second)

EIQ's Aortic Stenosis (AS) AI algorithm was FDA cleared in October 2024.

Companies that have already been through the FDA 510(k) process once are statistically more likely to get through it again.

2. EIQ’s clinical data is strong

EIQ's Heart Failure clinical validation study was run by Mayo Clinic (one of the most prestigious hospital networks in the US) on 17,000 individual patient echocardiograms.

The results:

- 99.5% sensitivity - When EIQ's AI says you have heart failure it's right 99.5% of the time.

- 91.0% specificity - When EIQ's AI says you DON'T have heart failure it's right 91.0% of the time.

(Source)

Very high sensitivity (and good, but not perfect specificity) is what we want to see with screening/detection technologies because the overarching goal is to make sure every single case is picked up (even if it means there are a few false positives).

Higher sensitivity means very few people ‘slip through the cracks’.

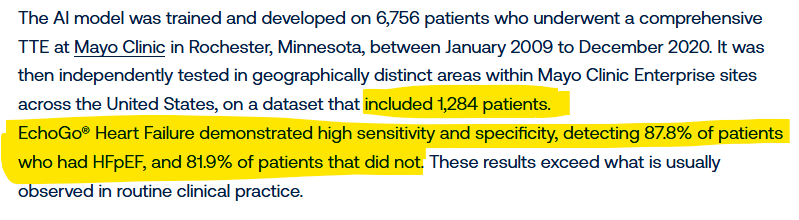

3. EIQ’s data looks stronger than an already FDA cleared tech

When it comes to detecting Heart Failure, here is how EIQ’s tech stacks up against already FDA cleared tech owned by Ultromics.

This is the only other AI heart failure detection software used in the market today which delivers - sensitivity of 87.8% and specificity of 81.9%. (source)

(Source)

Now, we are not cardiologists, so we can’t verify how the two companies' technology differs technically.

But EIQ’s data looks stronger.

EIQ has demonstrated sensitivity of 99.5% and specificity of 91.0% - and EIQ’s study was done on a dataset ~13x bigger than Ultromics.

4. EIQ’s tech is much better than the current standard of clinical practice

As mentioned above when EIQ's AI says you have heart failure it's right 99.5% of the time.

When EIQ's AI says you DON'T have heart failure it's right 91.0% of the time.

That’s a lot better than cardiologist only diagnostics, which have only 50% of heart failure cases being accurately diagnosed in normal clinical practice.

So EIQ’s AI paired with a cardiologist doubles the accuracy of echocardiograms.

- Mayo Clinic signed a distribution deal BEFORE FDA approval.

Last month, EIQ expanded its agreement with the Mayo Clinic - one of the top-ranked hospital systems in the US - to resell EIQ's Heart Failure AI through Mayo's network of 80+ external partner hospitals once FDA clearance lands.

The same Mayo Clinic that ran the validation study just signed a distribution deal...

BEFORE the FDA cleared the tech...

(source)

We take that as a strong indicator they are confident there is a strong case for approvals (and they would know given they ran the clinical study for EIQ).

6. Cardiology is now the #2 most-cleared FDA category for clinical AI, behind only radiology.

The FDA has now cleared over 200 cardiology AI algorithms. (source)

29 new cardiology AI products were cleared by the FDA between June and December 2025 alone.

And the CMS (Centers for Medicare & Medicaid Services) established a new national billing code and payment for AI cardiac imaging analysis in April 2026.

EIQ is sitting in the middle of the most-approved AI category in healthcare.

Look, we could be wrong here, it's impossible to know for sure what happens with the FDA submission and there is always a risk it doesn't come in.

We won't have to wait too long to find out - as shareholders we hope it does.

Our EIQ Big Bet:

“EIQ re-rates to a >$1BN market cap on successful commercialisation of its heart disease detection technology and/or an acquisition at a multiple of our Initial Entry price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our EIQ Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

How does EIQ’s tech work?

For anyone new to the EIQ story - here is a quick overview of what EIQ does.

EIQ’s product “EchoSolvTM” is a machine learning, AI-based decision support software that, when used together with a cardiologist, is able to detect heart diseases at a much better rate.

Cardiologists are specially trained doctors that are able to interpret heart conditions from 2D images that are presented from an ultrasound (known as an echo):

EIQ’s EchoSolv product can provide an actual 3D interpreted image of the heart, and provides assistance to the cardiologist in detecting heart related issues.

You can check out a short video overview of how the technology works here:

(Source)

What's next for EIQ?

🔄 Heart Failure FDA decision (any day now?)

Next is all about FDA clearance for EIQ’s heart failure detection tech.

As mentioned above, we are expecting to hear back from the FDA this half - which is literally inside the next ~6 days.

🔄 Aortic Stenosis commercialisation

The key metric we will be tracking in the short term is how many integrations EIQ can secure for its Aortic Stenosis tech.

In the short term we want to see more distribution deals - either through strategic partnerships or reseller deals.

Here are the milestones we are tracking:

- 🔄50 active contracts in the sales pipeline

- 🔄 Resubmission for a Category III reimbursement code

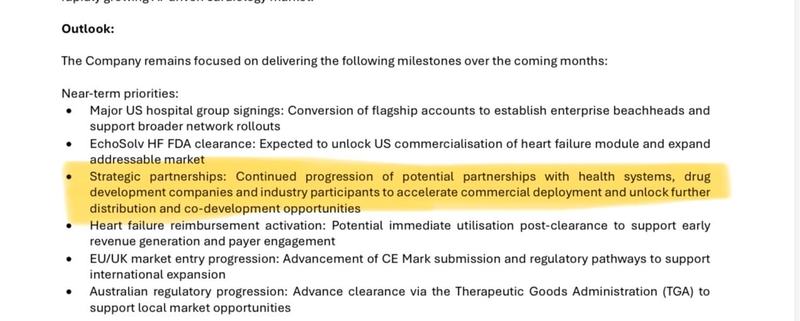

🔄 Australia and NZ pilot program

EIQ has previously mentioned that this program is being run with a ”leading global structural heart innovation company”.

We want to see some more news on this front because we think it could help advance EIQ’s licensing revenue pathway and be a “proof of concept” study that EIQ can take into the US.

We note strategic partnerships was teased in the recent quarterly again - so we wait to see what happens on this front:

(source)

What could go wrong?

The single biggest risk right now is without a doubt “Regulatory risk”.

The market has been pricing in a positive Heart Failure FDA outcome (the share price chart tells you that).

IF the FDA rejects, asks for additional clinical work, or delays the decision, EIQ's share price would likely re-rate sharply lower.

Regulatory Risk:

There is no guarantee that the FDA will provide clearance, and applications made by EIQ may be rejected. Also, EIQ's strategy is reliant on securing reimbursement for its product. If EIQ is not able to secure a reimbursement deal then its commercialisation strategy may need to pivot.

Source: "What could go wrong" - EIQ Investment Memo

Other risks

Like any small-cap medical technology company, EIQ carries significant risk, here we aim to identify a few more risks.

While a Category 1 reimbursement code for heart failure already exists, there is a risk that EIQ’s software may not qualify to use it. Failing to secure this specific code could force the company back to lower-paying miscellaneous codes, significantly impacting revenue targets.

Commercial growth is heavily dependent on distribution partners like Pro Medicus and Mayo Clinic to successfully market the software. If these external networks fail to deliver high-volume usage or if hospital adoption cycles take longer than expected, EIQ may struggle to achieve its commercial goals.

Competition in the AI medtech space is intensifying rapidly, with hundreds of cardiology algorithms already receiving FDA clearance. EIQ will need to constantly defend its market share against well-funded competitors who might offer cheaper or more advanced alternative technologies.

Expanding a sales and distribution network across the US requires significant operational expenditure and could lead to a high cash burn rate. If the company cannot scale to profitability quickly, it may require future capital raises that would dilute current shareholders.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our EIQ Investment Memo

You can read our EIQ Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our EIQ Investment Memo covers:

- What does EIQ do?

- The macro theme for EIQ

- Our EIQ Big Bet

- What we want to see EIQ achieve

- Why we are Invested in EIQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.