Our Latest Investment is…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,802,500 SGA shares and 1,466,250 SGA options, the Company’s staff own 50,000 SGA shares and 12,500 options at the time of publishing this article. The Company has been engaged by SGA to share our commentary on the progress of our Investment in SGA over time.

Today we introduce the latest addition to the Next Investors Portfolio.

We first started looking at this project over a year ago, in April 2021.

It will be just our fourth Portfolio addition for 2022.

Our latest addition is a giant project in battery materials - a sector where we have enjoyed past success.

Introducing...

Sarytogan Graphite Ltd (ASX:SGA) owns 100% of a giant graphite resource in central Kazakhstan.

This project has the highest grade graphite resource and second largest graphite resource of any ASX-listed company.

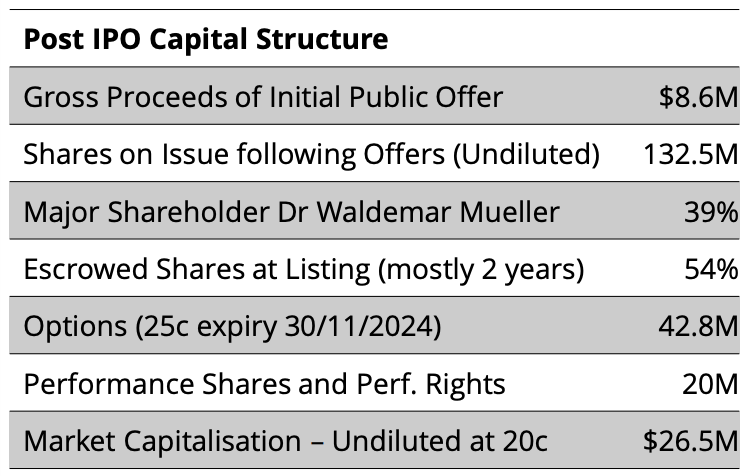

SGA began trading on the ASX this week, having raised $8.65M during its IPO. We participated in the IPO after having earlier invested during pre IPO seed raises.

We currently have a shareholding of just over 4.8 million shares or ~3.6% of the company, with 61% of our position under escrow for two years.

Our average Initial Entry Price is 16.33c.

As long term holders, our big bet is that we want to see SGA develop its giant graphite resource, which we believe has the potential to catch the interest of major miners and become a world-class graphite mining operation.

It’s early days with this ambition, of course, and there are plenty of risks along the way - hence the company’s current lower valuation.

With an Inferred Mineral Resource of 209 Mt, grading 28.5% TGC, for 60Mt contained graphite, SGA has the highest grade graphite resource of all of the graphite companies on the ASX.

It is also the second largest resource (in terms of contained graphite) on the ASX, behind only Syrah Resources.

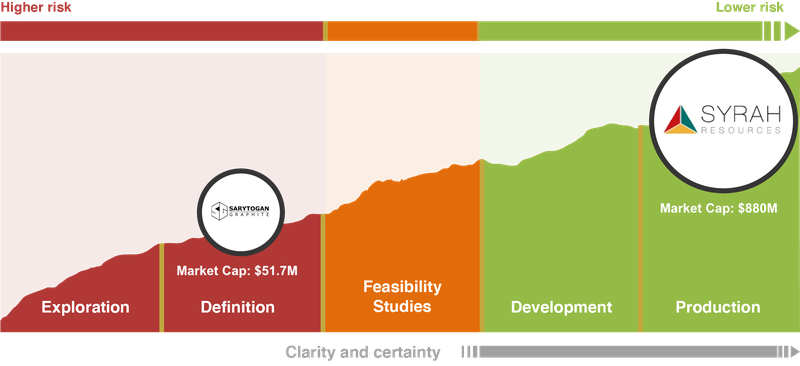

So far this week, SGA is up 95% from its 20c listing price, giving it a current market cap of ~$51.7M.

While the stock has performed well since listing, its market cap remains just a fraction of much later stage graphite company Syrah (capped at $880M), leaving lots of room to grow.

SGA is at a much earlier stage of development than Syrah which has an operating mine.

And while it won’t happen in the short-term, as long term investors, we hope to see SGA’s market cap start to approach that of Syrah’s as it progresses through the exploration phases towards mine development.

But it’s not just the Syrah comparison that has us thinking that SGA is attractive.

On an enterprise value/contained graphite tonne basis, SGA comes out as the cheapest of all its ASX graphite peers — even after its strong entrance onto the ASX this week.

As we mentioned above, this is a company that we’ve been looking at for over a year now as it worked towards listing on the ASX — it’s not everyday that we come across a junior explorer with such a large and potentially world-class battery materials project.

Today we will be sharing our 2022 SGA Investment Memo, in which we cover:

- The reasons why we invested,

- Our long term bet for the Investment,

- The objectives we want SGA to achieve over the coming 12 months,

- The risks involved, and finally,

- Our Investment plan.

Graphite is an in-demand battery material that is facing a looming deficit in the years and decades ahead. So from a top down perspective the graphite sector has the wind behind it.

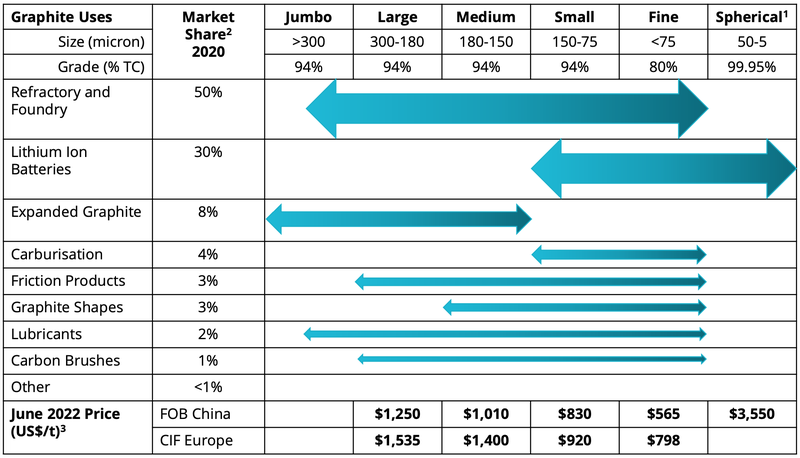

SGA is currently undertaking metallurgy work to determine the flake size of its graphite. This is an important factor that determines the end use of the graphite, and dictates how much SGA could sell the graphite for.

Here’s a snapshot of flake sizes and prices - we will delve into this in detail in future notes:

Historical work at the project suggests that a small flake graphite concentrate — the type used in battery anodes in the fast growing EV and Lithium-ion battery space — can be produced.

However, there hasn’t been any recent metallurgical testing to determine the quality and recovery of the graphite into a graphite concentrate.

Regardless, SGA appears confident that there will be a market for its graphite, whatever its flake size.

Another potentially overlooked benefit is the project’s location in Kazakhstan.

Many might assume operating in Kazakhstan is just an added risk (and yes there is sovereign risk), but it is actually a well established mining jurisdiction that’s close to infrastructure on China’s One Belt, One Road Initiative and right between EV and battery end uses in both China and Europe.

Initially scheduled to begin trading on the ASX back in March, the IPO was delayed as the ASX worked towards making a listing decision and SGA extended its exploration contract (lease).

But while the IPO itself was delayed (which had a silver lining as SGA missed out the May/June market correction), the company has continued its exploration work at the project.

Drilling is well underway and based on this, we expect to see some initial assay results very soon, which is unusual for a newly listed explorer.

All up, SGA appeals to us for a number of reasons and ticks the right boxes for it to be added to our Portfolio.

That’s not a decision we take lightly — we are seeking 1,000% returns from our Investments (which is always hard to achieve).

We run due diligence on hundreds of companies every year, with only a select few making the cut.

And while not every Investment pays off, we do have a track record of Investing in a number of early companies that achieved their objectives to deliver some significant returns.

We’ve particularly found success with Investments with battery materials projects including Vulcan Energy, Kuniko, and Euro Manganese (remember though that past performance is not an indicator of future performance).

SGA Investment Memo

Our 2022 SGA Investment Memo covers the reasons why we Invested, our long term bet for the Investment, the objectives we want SGA to achieve over the coming 12 months, the risks involved, and our Investment plan.

We will track the progress of our Investment over time against this memo.

Our SGA Investment Memo can be found at the link below:

Why we invested can be broken down into the following points:

1. Highest grade graphite resource on the ASX

SGA’s project sits over an area measuring ~103.92 km2 and has an inferred 60Mt contained graphite JORC resource at a grade of 28.5% TGC (Total Graphite Content).

At 28.5% TGC, SGA’s project ranks as the highest grade graphite project on the ASX.

The next highest grade project, at 18.5% TGC, is owned by the ASX-listed Talga Group (capped at $387M).

For some context, the biggest graphite producer on the ASX, $880M capped Syrah Resources’ project in Mozambique has a graphite grade measuring ~10% TGC.

The significance of the higher grades is that during the mining stage this could translate to lower mining costs with less waste material needing to be mined to get to the graphite resource.

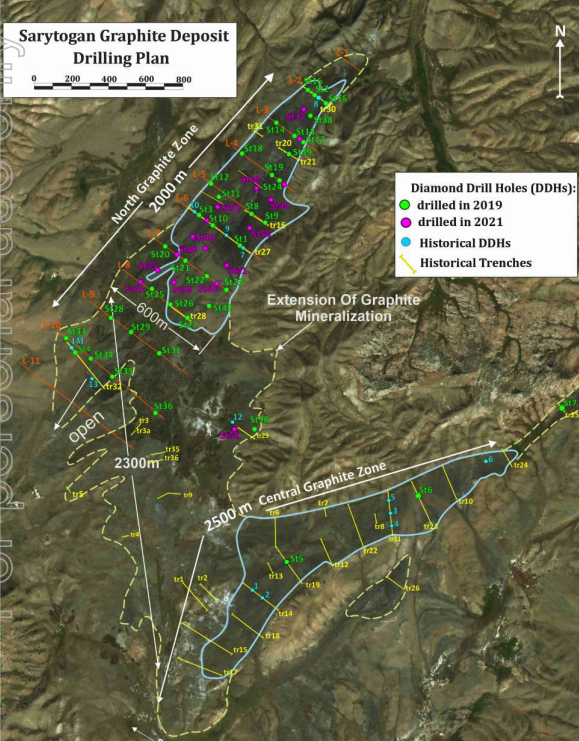

You can see below that SGA’s deposit is divided into two main zones, the aptly named “North Graphite Zone” and the “Central Graphite Zone”:

2. Second largest graphite resource on the ASX

SGA’s project also compares exceptionally well to that of its ASX graphite peers based on the size of its resource.

SGA’s JORC resource is the second largest, on a contained graphite basis (at 60Mt) of any ASX graphite project, second only to Syrah’s project in Mozambique.

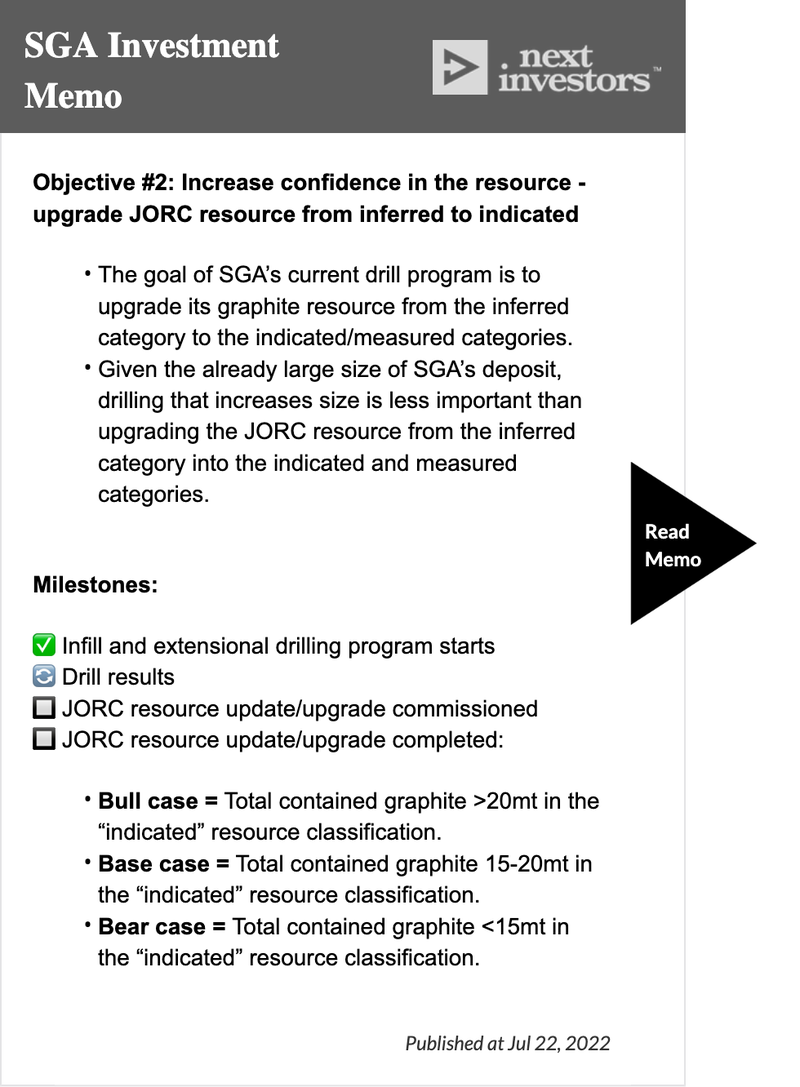

The existing inferred resource is already of a significant size, so rather than just seeing a larger resource, we are really interested in seeing SGA upgrading that to the Indicated category and getting a more detailed mineralogical classification of the resource.

This is what the current infill and extensional drilling campaign is setting out to do.

In addition to some strong high grade drill hits, which the market typically likes to see, we will be looking for important details around the graphite flake size distribution and quality over the coming months.

The enormous size of the deposit gives SGA the option of choosing to develop the highest grade, most economically viable section of its resource.

With its graphite resource outcropping from the surface, SGA’s project could potentially give rise to a low strip ratio open cut mining operation, which helps with project economics.

Here you can see that outcropping - the dark material is high grade graphite:

3. Low market valuation relative to its graphite peers

SGA also compares very well to its ASX peers on an enterprise value (EV)/contained graphite resource tonne basis.

At the time of listing, SGA has the lowest EV per tonne of contained graphite of all ASX graphite companies.

SGA had a market capitalisation of $26.49M and, with $8.65M in cash from the IPO, was trading with an Enterprise Value (EV) of $17.84M.

Since then, SGA is up ~95% and now trades on an (undiluted) EV of around $51.7M.

Based on its inferred 60mt contained graphite resource, this translates to a EV/contained graphite resource of $0.74/tonne — still the lowest of its ASX peers.

This compares with $880M capped graphite producer Syrah Resources, which trades at $5.19/tonne of contained graphite resource, while Australian graphite developer Renascor trades at $48.37/tonne.

As SGA upgrades the resource classification of its graphite resource and progresses development studies, we expect this gap to close.

We Invested to see SGA’s market cap start to catch up to its higher valued and more advanced peers, and this is the upside we see in SGA.

Of course, this earlier stage comes with added risk - hence the lower valuation right now.

SGA has a lot of metallurgy work still to do, plus scoping and feasibility studies, all the way through to having a producing mine - which is where we hope the share price re-rates will occur.

These more advanced peer comparisons are still worthwhile and provide an excellent example, or roadmap, of where SGA could be as it progresses its project.

As Investors, we welcome the opportunity for SGA to add value at every phase, from the drilling and initial metallurgy work, through to possible project development.

4. Kazakhstan: an established mining jurisdiction in a unique location

SGA’s project is located in Kazakhstan, an established mining jurisdiction, where recent reform efforts have created an attractive environment for investment in new exploration and extraction.

The country is intent on attracting large foreign companies. As discussed in this article, Honeywell — one of the 100 largest companies in the world — has localised its production in Kazakhstan, while Exxon and Chevron are there too. Other major foreign companies, including Fortescue Metals Group, plan to relocate to Kazakhstan.

The largest economy in central Asia — growing by double digits since 2002, the World Bank ranks Kazakhstan 25th for doing business, just behind Germany, Canada and Ireland, but ahead of Italy and Brazil.

We think this is an environment that favours investment, including that from foreign junior mining companies.

Interestingly, Kazakhstan’s mining legislation has been brought into line with Western Australia’s Mining Code (Standard Subsoil-Use Code in 2018) which is well understood by the global investment community. It also has a lower corporate tax rate than Australia at 20%; mineral royalty of 3.5%; and other taxes of 1.5%.

The project is located 170km from the large industrial city of Karaganda by highway, 68km from the nearest railway station. It is well serviced by nearby infrastructure (roads, railway, power, water), enabling a streamlined transition to future mining and are critical considerations for potential financiers.

And importantly, SGA’s project is ideally located to service large battery manufacturing hubs in both Europe and in China and is close to infrastructure on China’s One Belt, One Road Initiative.

Although there is obviously country risk present when considering an investment in Kazakhstan, which we outline in the risks section of our Investment memo and below.

5. Tight capital structure

SGA is tightly held, with 54% of the company’s shares escrowed for two years from the IPO.

Importantly, this escrow figure includes the 39% that are held by in-country Technical Director, Dr Waldemar Mueller.

There is therefore a limited number of shares available in the event that there is increased demand, so we think the SGA capital structure is leveraged to growth.

6. In-country experience and expertise

SGA’s single biggest shareholder, Technical Director Dr Mueller was the vendor of this project and brings extensive connections in-country, knowing all the doors that need opening and how to open them.

Dr Mueller is a Kazakh national, who happens to live in Perth, but has very deep connections throughout Kazakhstan and helped in introducing WA’s mining code to Kazakhstan.

He brings over 40 years’ experience in exploration and valuation of mineral resources for projects in Kazakhstan, Brazil, Russia, Kyrgyzstan and Georgia.

Operating in foreign jurisdictions can sometimes be challenging for ASX listed companies, hence why we think Dr Mueller will be able to navigate doing business here, and given his large shareholding, is incentivised to deliver success for SGA shareholders.

The macro theme behind SGA: Graphite

Long time readers will know some of our best Investments have been in companies developing critical minerals projects focused on the decarbonisation thematic.

Graphite is no different. We expect to see demand for graphite in line with demand for both electric vehicle (EV) batteries and grid scale storage.

What is next for SGA?

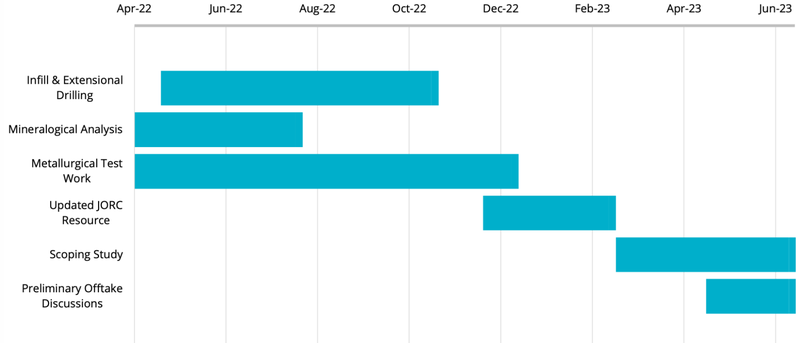

With exploration activities ongoing, including drilling currently underway, we expect a lot of newsflow over the coming months including results from drilling programs and met work.

SGA prepared the following work program timetable through June 2023.

Based on this, in order to track our Investment, we have outlined our own objectives that we hope to see SGA achieve.

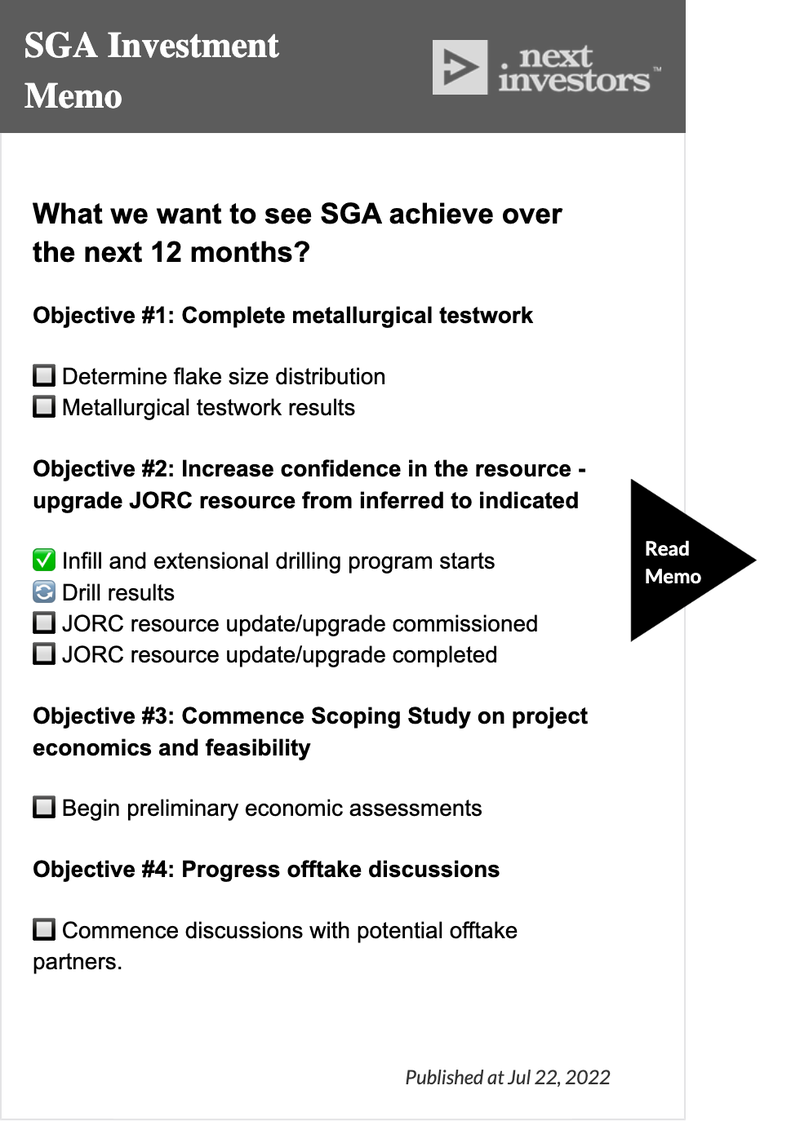

What we want to see SGA achieve over the next 12 months

As per our Investment Memo, we have set four key objectives for SGA to achieve over the coming 12 months.

We will use these objectives to evaluate the performance of SGA over that time.

To see progress being made against the key milestones for each key objective, check out our Investment Memo at any time by clicking on the image below.

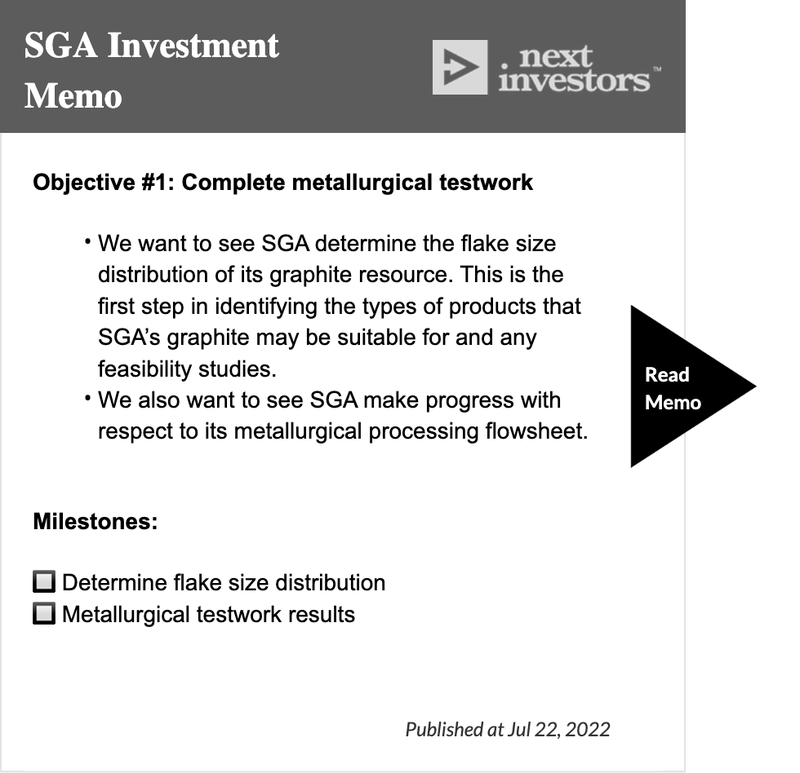

Objective #1: Complete metallurgical testwork

Determining the graphite flake size distribution and quality is a priority of the current year’s work program.

This is the biggest unknown factor of this project, and the results will clarify the potential uses of the project’s graphite.

Very little exploration has been done historically, but work done by the Russians in the 1980s indicates that SGA can achieve very high grade concentrates that are suitable for sale.

Historical testwork indicated that a small flake graphite concentrate can be produced. But there’s no recent metallurgical testing to determine the quality and recovery of the graphite into a graphite concentrate.

We are looking forward to seeing SGA conduct this work over the coming months.

Objective #2: Increase confidence in the JORC resource

The existing Resource is already of a significant size, so rather than just seeing a larger Resource, we are really interested in getting a more detailed mineralogical classification of the resources.

Additionally, exploration of adjoining zones could significantly increase its Mineral Resource.

Objective #3: Commence scoping study on project economics and feasibility

Preliminary economic assessments rely on the completion of an updated JORC Mineral Resource and more detailed mineralogical classification of the resources (including flake size distribution and quality), and as well as further environmental and topographical studies in the third quarter of 2022.

Objective #4: Progress offtake discussions

SGA expects that by late 2022 it will have generated sufficient samples for preliminary marketing discussions with potential offtake partners.

So, following the economic assessments, we are looking to see some progress in preliminary offtake discussions in 2023.

As reported in a CSA Global report, a local Kazakhstan company has already expressed interest in purchasing graphite from the Sarytogan deposit.

We will be watching with interest for any progress SGA can make here next year.

What are the risks?

Metallurgical testwork risk: With a massive JORC resource in place, SGA needs to work through the metallurgical testwork to determine whether its graphite can be produced into economically recoverable graphite. SGA is yet to determine the flake size distribution of its JORC resource, which could have implications on product suitability. Testwork could show that the graphite can not be produced economically or that the flake sizes are not suitable for its various use cases.

Exploration risk: SGA’s current JORC resource sits 100% in the “inferred” category — the lowest JORC resource confidence level. Drilling will increase the data available to upgrade the resource from inferred to indicated or measured and then to mineral reserves. As with all exploration, there is always risk that a drilling program fails to deliver the required intercepts for the resource to be upgraded.

Commodity price risk: The outlook for graphite pricing remains positive in the near term, but as with all commodities, the price is volatile. Graphite is an opaque early stage market. New graphite supply may come online and therefore demand may be lower than anticipated. A projected 74% of future graphite demand is forecast to come from EVs, presenting a high technology concentration risk that could impact on graphite pricing.

Funding risk: The funds raised in the IPO are expected to cover two years of operations. Given SGA has no revenue and is still progressing its project towards development, it is likely to be reliant on capital markets for future financing rounds. Once these funds are exhausted SGA may need to raise capital which would dilute existing holders.

Sovereign risk: Kazakhstan’s legal system is less developed than some more established jurisdictions, resulting in higher sovereign risk including in obtaining all required permits and approvals. Kazakhstan borders both Russia and China and so any geopolitical escalations in the region could have spillover effects on Kazakhstan. We also note the civil unrest in Kazakhstan earlier in the year which could reappear at any stage in the future.

Environmental, Social and Governance Disclosures

We believe that best in class ESG companies attract more capital, better customers and top talent – this leads to better shareholder returns over time.

We want all our Investments to provide ongoing ESG improvement and disclosures via quarterly ESG reporting.

SGA’s ESG disclosure report from Socialsuite can be accessed here.

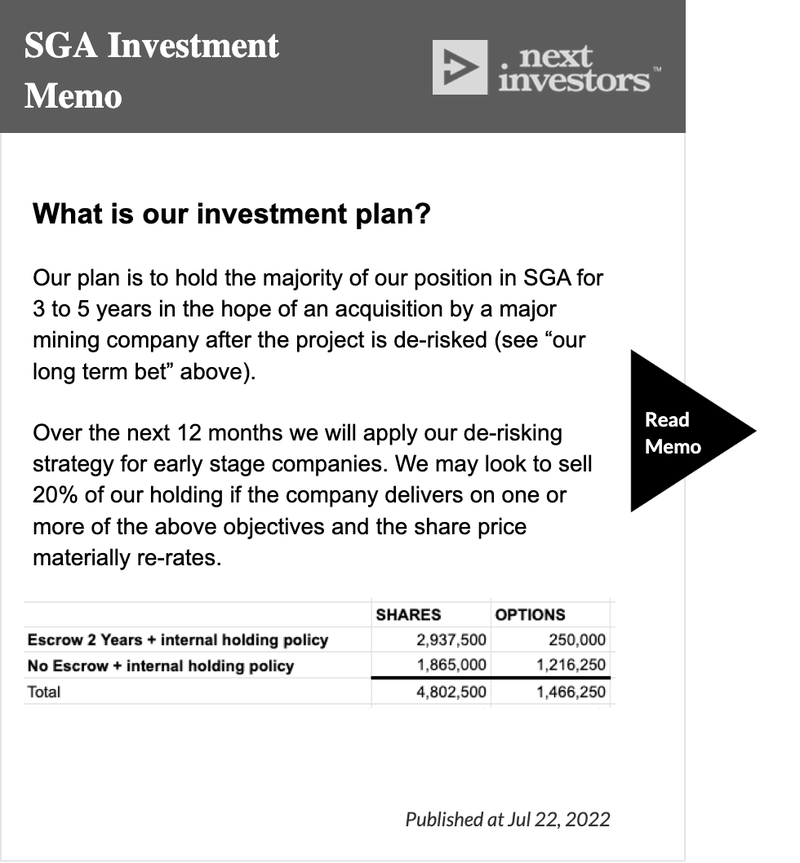

What is our investment plan?

To see our internal holding policy click here.

SGA 2022 Investment Memo

We have also today released our 2022 SGA Investment Memo, found here.

The SGA Investment Memo covers:

- What SGA does

- A macro view

- Our long term bet for the Investment

- Our reasons for investing in SGA

- The key objectives we’ll be watching for SGA to achieve this year

- The key investment risks

- Our investment plan, including when we would Take Profits

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.