SGQ secures $20M in funding for advanced Brazilian niobium/REE asset

Our Investment St George Mining (ASX: SGQ) is back trading on the ASX again, having put out an update on its plans to acquire the Araxá niobium/REE project in Brazil.

We Invested in SGQ when the deal to acquire the project was first announced in August last year.

The company went into suspension in October to finalise a $20M capital raise.

Today SGQ has confirmed that the raise terms have been re-cut from what was a 2.5c capital raise with no options, to a 2c capital raise (with 1:2 free attaching options with ex price of 4c, 2 year expiry).

We like SGQ’s project for a number of reasons (you can read our full initiation note here) including:

- The project is an existing discovery - drilling has hit niobium grades of up to 8% and the project has only been drilled on ~10% of the project area.

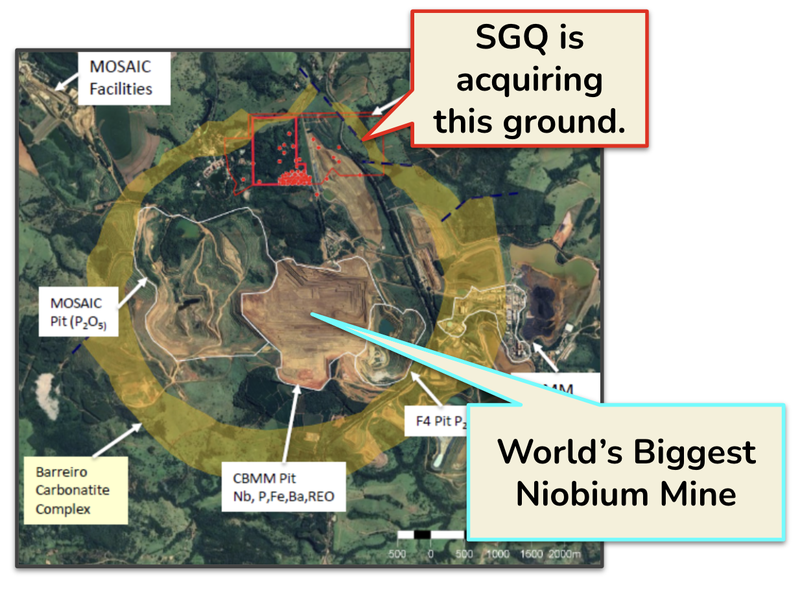

- The project sits next door to the world’s biggest niobium mine - next door to CBMM’s niobium mine which is producing ~80% of global supply. As well as the mine, there is existing infrastructure and a skilled workforce nearby.

Since August, SGQ has already delivered some solid newsflow including:

- A cooperation agreement with the State of Minas Gerais to expedite project approvals

- A partnership agreement for potential downstream processing

- The appointment of industry leading environmental consultants.

- An MoU with Global trading house SKI Hong Kong. The MoU also included some provisions to discuss potential offtakes from SGQ’s project.

- The establishment of a highly qualified in-country team with more than 40 years’ combined experience in the niobium business. Two key appointments are both ex-CBMM - the owners of the producing Niobium mine next door.

- Raised $3M at 2c per share.

For the past few months SGQ has been in suspension as the deal to acquire its project was getting finalised.

Today we got an update on SGQ’s funding plans and on when the deal is expected to be completed.

First the capital raise.

Initially SGQ was looking to raise the $20M at 2.5c per share with no free attaching options.

Now SGQ has secured firm commitments for $20M at 2c per share with 1:2 free options (4c exercise price with a two year expiry).

The second update was for the deadlines to complete the acquisition:

Initially, SGQ had guided for the deal closing in September/October 2024.

That’s when the first US$10M payment was supposed to be paid to the vendor of the project.

After today’s announcement SGQ has until the 15th of March 2025 to make that initial US$10M payment.

The remaining deferred consideration of US$6M is due 9 months after that date, and another US$5M is due 18 months after that date.

Our take on today’s announcement

We Invested in SGQ in August of last year, as we were particularly attracted to the advanced stage nature of the project - this is not a greenfields exploration play.

Our view is that SGQ’s project has a much higher likelihood of making it into production relative to other early stage exploration / discoveries on the ASX.

We still stand by that in the medium/long-term.

As mentioned earlier, SGQ’s project has over 500 drill holes with niobium grades above 1% and some hits over 8% niobium - all of this from drilling on just 10% of SGQ’s project area.

On top of that, SGQ’s project is right next door to the world’s biggest niobium mine and all of the associated processing infrastructure that project has.

From our point of view, the re-cut of the terms from 2.5c to 2c per share isn’t that big of a deal BUT the attached options will likely mean there is some short term pressure on the share price.

Any good news could be met by some selling as the share price gets closer to 4c per share and some investors look to free carry their options.

It’s also frustrating for those shareholders that bought on market following the news of the deal, as SGQ was trading at higher levels prior to the October suspension.

We would now expect the share price to hover around the 2c mark until the transaction is completed.

This is a long term Investment for us - the short term pressure from cap raises is less relevant in the longer run.

We are Invested in SGQ to see it hopefully achieve our Big Bet for the company which is as follows:

Our SGQ Big Bet:

“SGQ defines a niobium/rare earths deposit large enough to take into development or attract corporate interest via a takeover at a market cap of >$500M”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGQ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for SGQ?

The two main milestones we want to see SGQ complete over the coming months are:

- Complete the $20M capital raise - we want to see the cash hit SGQ’s bank account, and the new shares trading on the ASX.

- Make the initial payment to the vendors of the asset and finalise the acquisition - this one should be done before that deadline date of 15th March 2025.

Read our first note on our SGQ Investment below, which covers our Investment Thesis in detail: