SGQ hits 12.61% rare earths in a discovery hole 1km east of its resource

Our niobium/rare earths Investment St George Mining (ASX: SGQ) just put out exploration results from its project in Brazil.

SGQ owns 100% of the Araxá project which is next door to CBMM, the mine that produces ~80% of the world’s niobium supply.

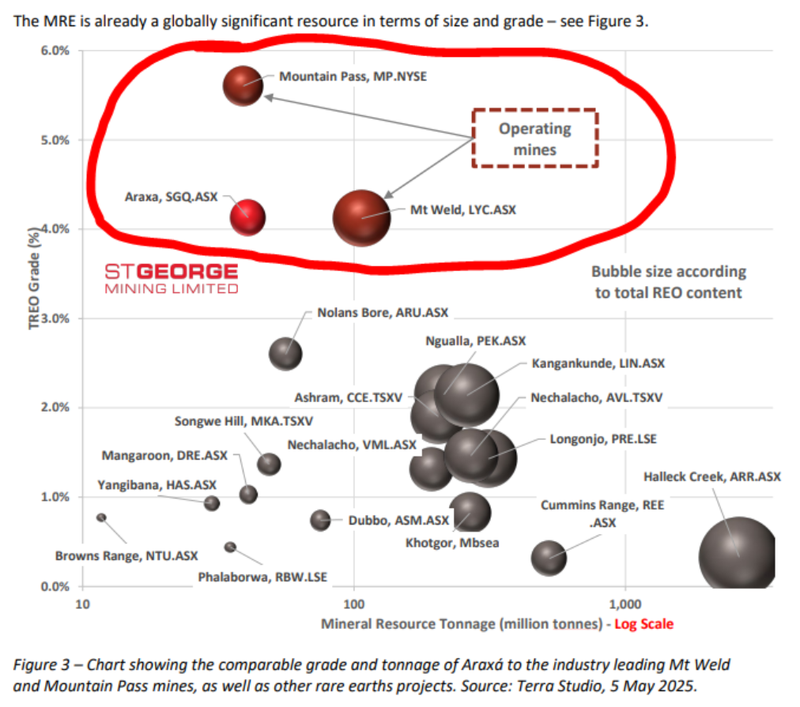

SGQ’s project is the largest and highest-grade carbonatite-hosted rare earth deposit in South America and second highest grade REE deposit globally in the Western world.

SGQ’s resource currently sits at:

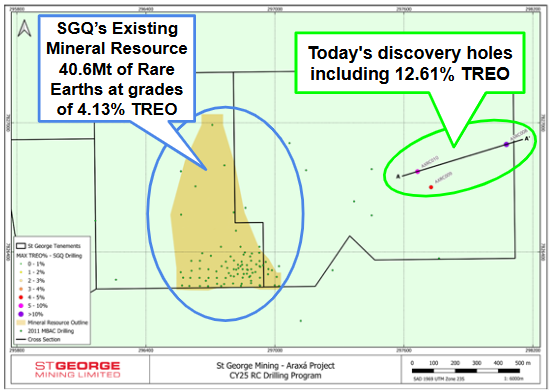

- 40.6Mt of Rare Earths at grades of 4.13% TREO (total rare earths oxide)

- 41.2Mt of Niobium at grades of 0.63%

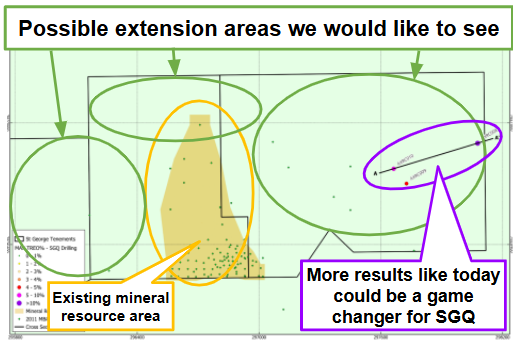

SGQ’s new discovery comes from OUTSIDE its existing resource area, ~1km east of the existing Mineral Resource

Drilling results included 48m @ 5.71 TREO from 2m… and a much higher grade core of 15m @ 12.61% TREO from 4m.

Those hits are higher than the average grade across SGQ’s current resource of ~4.13% TREO (total rare earths oxide).

And the hits come from the same part of the project where shallow aircore holes hit mineralisation to the end of hole.

We also note SGQ is drilling with over three rigs on site 24/7 - so we could see a lot more results coming in over the coming months.

(Hopefully it means SGQ is able to multiply the size of its resource).

Why the new discovery could be a game changer for SGQ

Today’s discovery hole also had higher grades of NdPr, heavy rare earths and Samarium.

Samarium has a key use in powerful samarium-cobalt magnets that are required in high temperature applications such as control rods in nuclear reactors and also military equipment such as the F-35 fighter planes.

Heavy rare earths matter because that’s where the big bottlenecks for supply are for the major western refiners.

Heavy rare earths are critical to the permanent magnet industry as they can help withstand higher temperatures in heavy duty applications including EV motors, wind turbines and defence systems.

Right now China controls nearly 100% of global heavy rare earth processing, so finding the best sources of feedstock will be crucial to give the developing western processors setting up plants the best opportunity to succeed.

Several media outlets have been covering this unfolding story recently:

(Source)

(Source)

So the news overnight out of the US that it was considering setting aside US$5BN to invest in critical minerals projects (especially rare earths) wasnt a surprise to us.

Check out the media reports overnight here:

(Source)

(Source)

Why size and grade matters… SGQ becomes an M&A target?

SGQ having the largest and highest-grade carbonatite-hosted rare earth deposit in South America and second highest grade REE deposit globally in the Western world matters…

Both $13BN Lynas and $18BN MP Materials hard rock carbonatite-hosted rare earth deposits.

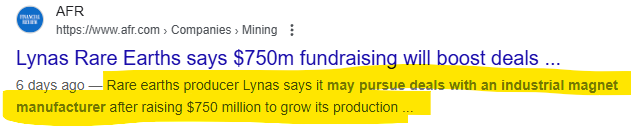

We noticed the following AFR article out recently which highlighted Lynas’s $750M cap raise and mentioned that the company is deal ready.

We did note that Lynas mentioned going downstream, but who knows what they plan to do with the funds…

Going downstream won't be an issue for someone like Lynas…

But finding the feedstock to feed those facilities will be.

IF MP and Lynas want to go upstream and take out projects that become feedstock for their refineries/processing facilities they could start looking at assets like the one SGQ owns.

And if that happens, we think the big western players like Lynas and MP will likely stick to what they know (hard rock deposits) and if they were to do a deal it would be on other assets with size/scale.

MP Materials in particular will need to do a deal after receiving a US$400M investment from the Pentagon and a supply deal with Apple worth ~US$500M.

Most of the Pentagon funds are earmarked to expand MP’s magnet production facilities.

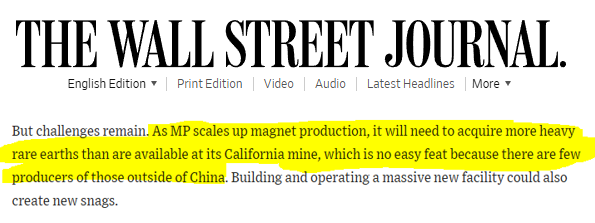

The catch though is that once MP’s magnet facilities are expanded - MP’s mine (the only one in the US) won’t be able to keep up with the rare earths supply the plant needs to operate.

MP will need to go out looking for new rare earths supply - which is hard to come by given China controls over 2/3rd’s of global supply.

(Source)

That’s where we think a winner could be a company like SGQ - even though its rare earths project is in Brazil and not inside the USA.

That’s just MP…

What Lynas ends up doing with its $750M is also in play now.

We think that as SGQ drills out and increase the size/scale of its project, it could start to become more and more attractive as either a source of supply or an outright M&A target for someone like a Lynas or MP (or any other group looking for rare earth supply from a hard rock deposit).

Of course we are just thinking out loud here, there is no guarantee any of this happens and there are plenty of other places corporates could go looking for rare earth feedstock.

Here is how SGQ’s resource compares to MP and Lynas’s:

(source)

What’s next for SGQ?

Drilling results 🔄

In the short term the main thing we want to see are drill results.

Ideally we see big extensions at depth and to the north/east/west of SGQ’s current JORC resource estimate.

Beyond the drilling 🔄

Over the next 12-18 months, a lot of the catalysts for SGQ could come at hard-to-forecast times:

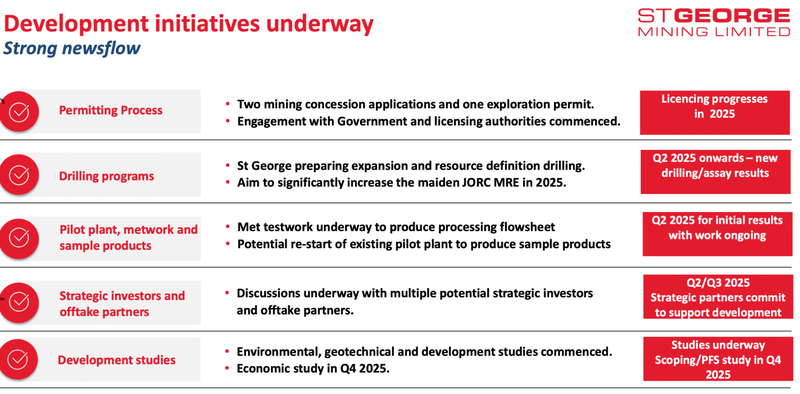

- Updates on downstream processing strategy - We want to see SGQ define its downstream rare earths strategy. We are especially looking forward to an update in relation to the US.

- Start working on development studies - SGQ has already commenced environmental, geotechnical and development studies with a view of getting to economic studies in Q4-2025.

- Pilot plant trials - SGQ has an agreement in place with Latin America’s only permanent magnet maker. SGQ is participating in the “MAGBRAS Initiative” - a program that has major automakers like Stellantis working toward building Brazil’s first permanent magnet-making facility.

- Metwork and sample production - SGQ should have results from this fairly soon. The main catalyst we are looking forward to is the re-starting of SGQ’s pilot plant so that product samples can be produced for potential strategics/offtake partners.

- Permitting - SGQ is targeting completion for permitting by Q4-2026.

- Finalise the remaining vendor payments - (US$6M due before the end of the year and US$5M due next year). Hopefully, SGQ can follow up on the $8M cornerstone investment it managed to get from Xinhai Group earlier this year.

(Source)