SGQ announces maiden JORC niobium & REE resource

Our Niobium Investment St George Mining (ASX: SGQ) just put out a maiden JORC resource for its project in Brazil.

SGQ’s project is next door to the world’s biggest niobium mine owned by private company CBMM.

CBMM in a previous funding round back in 2011 was valued at ~US$12.5BN.

(And that was way before niobium became the centre of market attention)

CBMM’s deposit supplies ~80% of world niobium & has resources in place to keep the mine running for multiple decades.

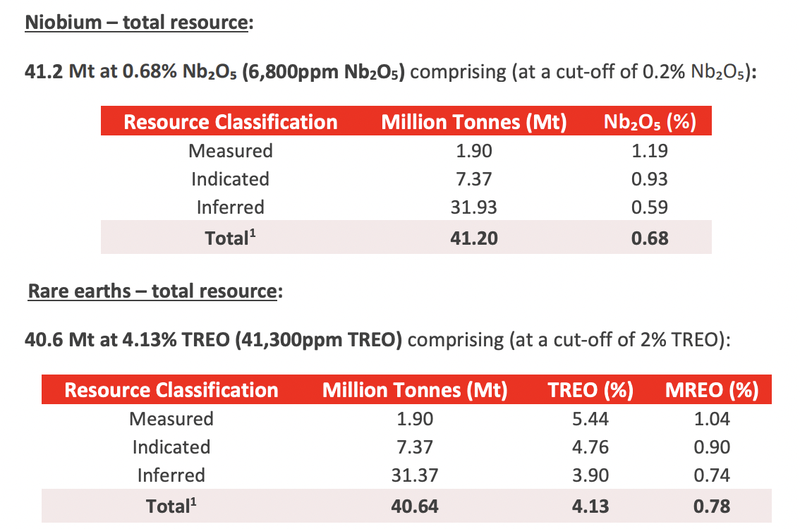

Today, SGQ announced its maiden JORC resource of 41.2Mt at 0.68% niobium and 40.6mt of rare earths at 4.13% TREO (total rare earths oxide).

After today’s news, the market has a way of comparing SGQ’s resource to other companies on the ASX that are going after niobium…

Including current sector favourites like WA1 Resources and Encounter Resources, here is how SGQ compares to both those companies:

- WA1 Resources (Capped at ~$830M) with a 200Mt at 1% niobium inferred resource

- Encounter Resources (capped at $112M) with no JORC resource yet.

- SGQ capped at $53M with a JORC resource of 41.2Mt at 0.68% niobium.

(Source)

Of course, a company’s resources should never be the only thing compared when looking at relative valuations.

We think another reason SGQ stands out from its Australian peers is because of how close the company’s asset is to existing infrastructure and human capital…

This was one of the main reasons we Invested in SGQ:

Project sits next door to the largest niobium producer in the world

SGQ is next door to CBMM, which supplies 80% of the global niobium market. SGQ’s project sits on the same geology as CBMM.

Source: “Why did we Invest in SGQ?” - SGQ Investment Memo 6 August 2024

Having access to all that infrastructure and workforce on its doorstep means it is much faster and cheaper to bring a mine into production.

SGQ’s rare earths grades are also high…

SGQ’s project’s rare earths potential was also a big part of the reason we first Invested in SGQ.

We mentioned it in our SGQ Investment Memo here:

Rare earths, with high grade TREO.

SGQ’s project also contains ultra high grade rare earths with TREO grades >10% in 10-60m intercepts. SGQ’s project sits on the same type of geology (carbonatites) as Lynas’ giant Mount Weld rare earths mine

Source: “Why we are Invested in SGQ” - SGQ Investment Memo 6 August 2024

In today’s announcement SGQ announced a 40.6mt of rare earths at 4.13% TREO (total rare earths oxide).

That came as a surprise to us both in terms of tonnage & grade…

For some context on the grades - $6.5BN Lynas Rare Earths, the number one rare earths exposure on the ASX has a resource of ~106.6Mt at 4.12% TREO.

Lynas is currently producing out of the high grade ore reserve at its project where grades are ~6.44%.

(Source)

Lynas’ project’s grades are as high as they come in terms of hard rock rare earth assets.

We think SGQ’s project having rare earth grades that are almost identical to Lynas’ adds a second source of value to SGQ’s project.

What’s next for SGQ?

🔄5,000m Drilling program

Now that SGQ has put out a maiden JORC resource, we are looking forward to the 5,000m drill program the company has planned for this month.

SGQ has previously said drilling would start in April.

🔄 Metwork updates

We’re also on the lookout for an SGQ metwork update, which is due in Q2 of this year.

Beyond these two catalysts, we are also looking forward to the project being progressed from a permitting perspective & from a funding/offtake perspective:

(Source)