How big could a Dimerix partnership/licensing deal be?

The clues are in the price...

In a big piece of news for our Phase 3 biotech Investment Dimerix (ASX:DXB), a treatment that is complementary to DXB’s DMX-200 locked in its pricing and received FDA approval for another rare kidney disease.

Not only is this indicative of the growing industry momentum for kidney treatments, we think DXB could benefit following this news.

The treatment is called sparsentan, and we think its approval and pricing guidance has major positive implications for DXB’s ability to secure a sizeable partnership or licensing deal for its lead treatment - DMX-200 for FSGS.

Our main point today is as follows…

Should DXB’s Phase 3 study on DMX-200 go well, and the interim analysis results come back positive - we think sparsentan could act as a benchmark for DXB’s pricing and potential deal value in negotiations with major pharmaceutical companies.

The complementary drug is called sparsentan.

Sparsentan was developed by Travere Therapeutics which was able to secure a long term licensing deal with Vifor Pharma with a value of up to $845M.

Vifor was in turn acquired by Australian biotech supermajor CSL for $18.8BN.

Here’s quick rundown on what happened with sparsentan:

- The FDA granted accelerated approval to sparsentan, the first and only non-immunosuppressive therapy approved to treat IgA nephropathy (IgAN)

- IgAN is a rare kidney disorder that involves the buildup of immunoglobulin A (IgA), a protein that helps the body fight infections.

- The company plans to charge $9,900 for a 30-day supply, or about $120,000 a year. Travere estimates that there are 30,000 to 50,000 patients who could get the drug when it launches.

- Sparesentan is also in a Phase 3 trial for the treatment of focal segmental glomerulosclerosis (FSGS) - the trial is called PROTECT

- Sparsentan has toxicity warning particularly related to liver toxicity, foetal toxicity and certain drug interactions - “the company will have to run a risk evaluation and mitigation strategy, or REMS, as part of the approval. It will require doctors to go through special training, and patients to be enrolled in a monitoring program, in order for the drug to be prescribed.”

And here’s why this really matters to DXB:

- Pricing will be the same for sparsentan for both IgAN and FSGS - which provides a benchmark for DXB’s treatment pricing (and consequently, partnership/licencing negotiations) pending successful interim analysis results

- We note that similar to sparesentan, DXB’s treatment is targeting ~40,000 patients in the US alone and ~220,000 patients across 7 major markets

- We think sparsentan’s approval is an important precedent for rare kidney disease orphan treatments - and DXB’s treatment could also benefit from the accelerated approval pathway.

- Comparatively with sparsentan, our view is that DXB’s DMX-200 has a well established safety profile

- If sparsentan is approved for FSGS, the monitoring required for sparsentan could inhibit sales, leaving a greater need for DXB’s treatment in the market.

All up, we see what’s happened with sparsentan as justifying our view that a successful interim analysis outcome could be a big catalyst for DXB.

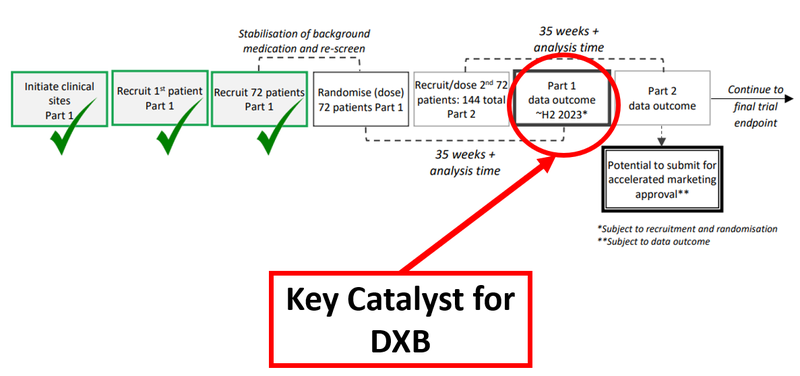

The results are due in the second half of this year:

What’s next for DXB?

We’re looking for additional patient recruitment updates on the 144 patients DXB needs to complete Part 2 of the trial which could unlock accelerated marketing approval.