Why do shares go down on good news?

Published 15-AUG-2023 17:12 P.M.

|

10 minute read

We’ve all seen it happen.

When a company publishes “good” results but the share price goes down anyway.

For most new investors this phenomenon can be one of the most confusing realities of the small cap stock market.

We have been around small caps for more than 20 years and have seen plenty of companies publish positive news only to get a negative reaction in the share price.

But why does this happen?

At a very high level, just like most things, the company’s share price is a function of supply and demand.

If more investors are looking to sell than are buying, then the share price goes down and vice versa.

These supply and demand drivers are all a function of expectations and sentiment.

So when good news is published, in an environment where expectations for the company are high, the results can be met with disappointment and the share price can fall.

The same can happen when good news is published when market sentiment is low.

It’s important to pay attention to the company's expectations as news is published, and not let the market price on the day of an announcement dictate the evaluation of the results.

We like to set a bull/bear/base case scenario for results before they have been published, to objectively evaluate the merits of the result.

The same results could move the share price up OR down, depending on the expectations of the market beforehand.

So, let's have a look at the key drivers of share price movement post-news.

- Buy the rumour sell the news

- Market was expecting great but the results were good

- Results were good, but delayed

- News is good, but no new information

- Reality kicks in

- Cheap shares floating around

- Market sentiment is poor

Buy the rumour, sell the news

There is an old saying in markets - “buy the rumour, sell the news”.

At its core the saying highlights that investors buy during the speculative stage before a big share price catalyst and then sell when the results finally drops.

Again, share prices are a function of supply and demand.

In the lead up to a major catalyst, particularly in a bull market, investors buy the stock that want to “bet” on the outcome of the results.

At the same time existing holders don’t want to sell their shares just before the long awaited catalyst results and the selling dries up.

Oftentimes this will push the share price up in anticipation of a major catalyst, and “price in” a good result.

On top of this, speculative buying from traders can compound the effect when a company’s share price starts gathering momentum.

Once the company announcements are published, selling occurs, REGARDLESS of the quality of the announcement as short term speculators look to “cash in”.

As a result, when a company puts out a result of a catalyst, there will almost always be a group of investors looking to sell, creating a downwards pressure on the price.

If the announcement is positive, but not strong enough to bring in more new investors to outweigh this selling pressure, then the share price is likely to fall.

The level of positivity required to keep the share price up, depends on the expectations on the results before the news is announced, and how well the news meets those expectations.

Market was expecting great, but results were good

As mentioned above, the expectation of a result can be bigger than the result itself.

This happens when a good result is “priced in”.

If the stock price runs up to the results of the key catalyst, it likely means that expectations are high, and only exceptional results will result in further share price increase.

The higher the price runs, the better the result needs to be for the company to continue to beat market expectations.

If the result is just “good” but not “great” it will likely be met with a share price drop as speculators look to exit the position and hunt for the next catalyst.

So, when the company has a technical success, gains valuable information or makes a discovery (just not a really big discovery), it can be punished if the expectations beforehand were too high.

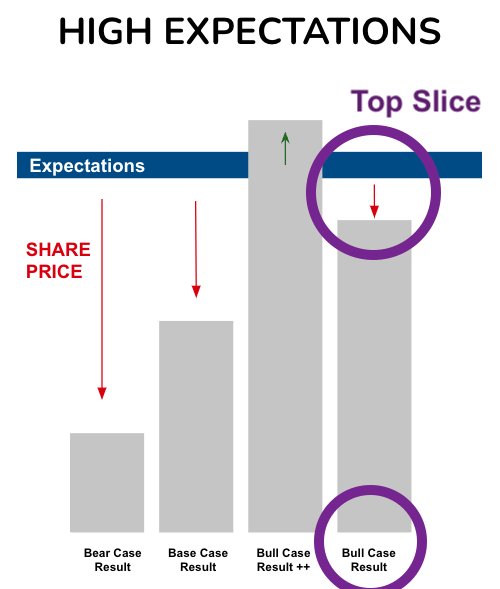

We like to mitigate expectation risk by objectively evaluating the company BEFORE the results of the catalyst are announced - when expectations are high.

Generally, the company will publish a timeframe in which to expect the results of a catalyst.

If the share price runs in anticipation of the results and the market cap of the company is larger than the value that we would expect if our “Bull Case” scenario eventuates - the expectations are likely too high.

In this scenario we like to Top Slice some of our Investment, ideally leaving us Free Carried into the result.

In this scenario we are still leveraged to success in the off chance that there is an exceptional result that beats our bull case target, but we are de-risked if the results are just good.

Once the results are published, we look to our bull/bear/base case scenario to evaluate the merits of the results, rather than the share price.

Remember, the shareprice is a function of expectations and market sentiment and there could be a number of other factors affecting it.

🎓To learn more about setting expectations for drilling read: Expectation setting leading up to drilling programs

Results were good, but delayed

In the small cap market things take time... a long time.

Drilling gets delayed, permits get delayed, clinical trials get delayed, and investor patience eventually runs out.

For companies that put out good news on a catalyst that investors have been sitting on for a long time, it provides an opportunity for “stale” holders to exit their position in a period of higher liquidity.

Sometimes it can take years for a company to secure a permit, deliver a JORC resource or conduct a clinical trial. And the longer that the results are delayed, the more frustrated the investors get.

Investors may also lose faith in the company's ability to deliver results on time and on budget, so when the news eventually does drop, the stale investors are so fed up with the stock that they sell, regardless of the merits of the results.

News is good, but no new information

When news is published, it needs to be understood within the context of the overall company strategy.

Known information will generally not gain the same amount of traction as unknown information - even if the information published is objectively “good”.

For example, let’s say a biotech company is developing a treatment for a rare disease. The company publishes data that indicates that the drug is safe.

This should be seen as “good news” by the market.

But if the company has already published data that indicates that the drug is safe (let’s say in a previous clinical trial), then the share price will not likely move on this news.

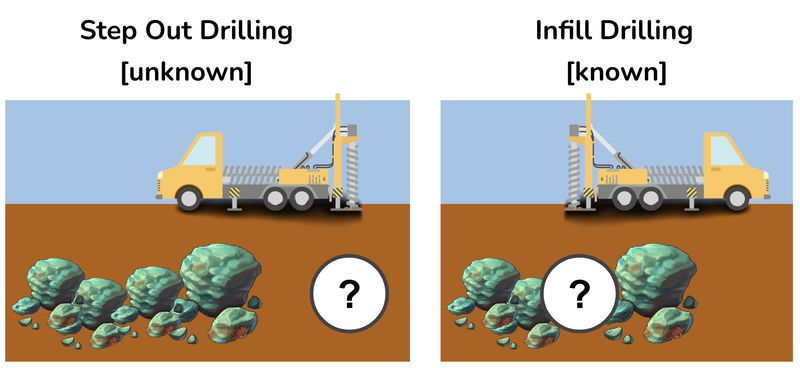

The same can be said with drill results.

Infill drilling, which is drilling in-between two existing drill holes with known mineralisation, is less exciting to the market than step-out drilling, which is away from the known area of mineralisation.

It’s important to read the results within the context of the overall project - as the information may already be known to the market.

Reality kicks in

As a company delivers progress and gains traction it moves from a high-risk, high-reward investment to a company that is more mature.

This is true across early stage companies in the resources, tech and biotech space.

Tech companies

There is a saying in tech, that pre-revenue companies are priced on potential, and revenue companies are priced on performance.

Tech companies that are still in the pre-revenue phase have unlimited upside potential in the eyes of investors.

But, when the company starts making revenue then “reality sets in” and the performance often doesn’t meet expectations.

It is important to be realistic about the company’s ability to generate revenue from its product or services.

If the market has priced the stock with unrealistic growth expectations, then the company could be one bad earnings report away from a big price drop.

Resources companies

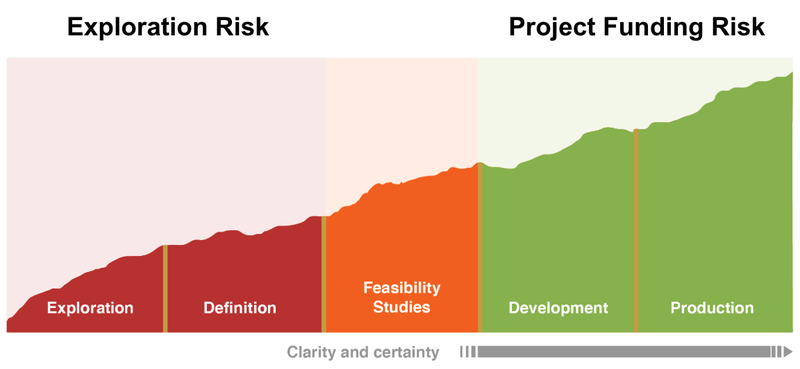

A resource company lifecycle moves through Exploration → Definition → Feasibility → Development → Production.

As resource companies grow from exploration through to production the key risks changes from “Exploration Risk” to “Project Funding Risk”.

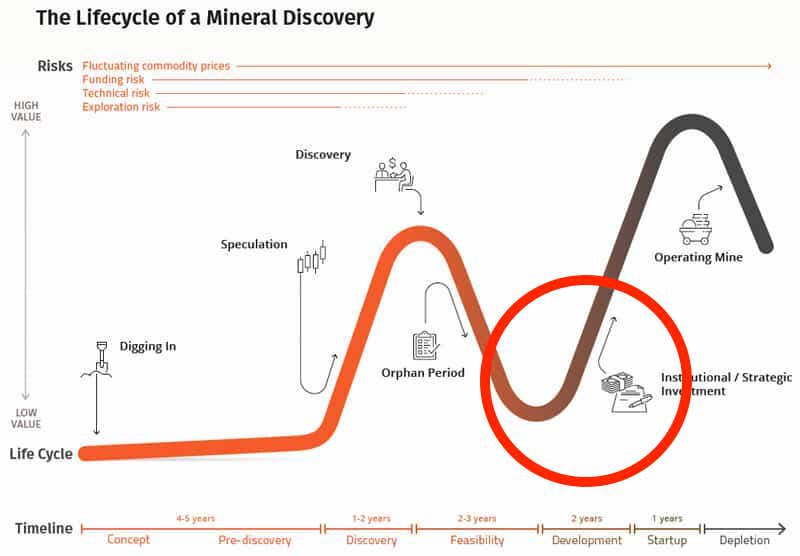

The excitement from a discovery can wane if it is not followed up with further discoveries and the realities of funding a commercial mine become apparent.

Oftentimes, the types of investors who back small cap companies don't have the patience to hold for the long term and will look to exit positions as the companies grow through the resource company lifecycle.

While the headline feasibility numbers may be extremely strong, the reality of how difficult it will be to get the project/product developed and producing real cash means investors are brought back to reality.

This can create a downwards selling pressure on the stock as the reality sets in for the company.

Here is how the cycle generally plays out, where the red circle is reality setting in for the investor:

The excitement picks up again for the company once it secures the funding to produce, but until then it can be left in development purgatory, waiting for the underlying commodity price to grow.

🎓 Read more about the mining company lifecycle: The Mining Company Life Cycle Explained

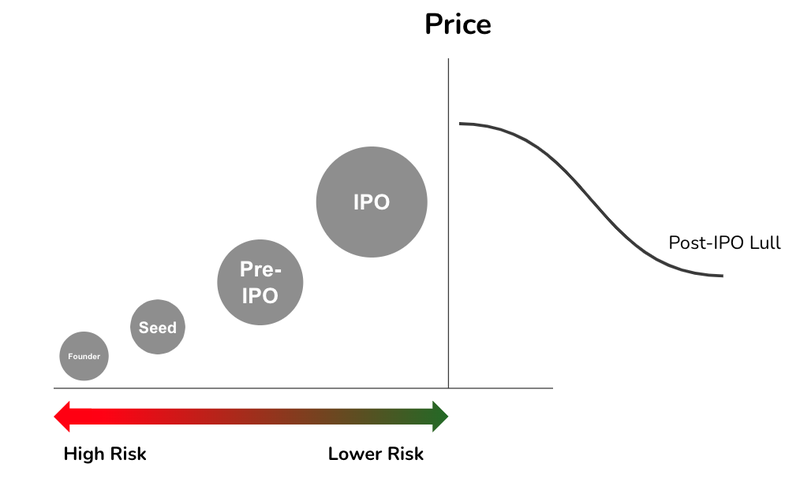

Cheap shares floating around

For companies that have recently listed OR recently raised capital, this is highly relevant.

Typically, when a company is newly listed there are a bunch of founder, seed stage and pre-IPO stage investors who are invested at much lower share prices than the company’s listing price.

Similarly any company that has just recently raised capital has investors who participated in a capital raise at a discount to the current share price.

These investors who hold shares averaged at much lower share prices than where the company is trading after a good news announcement will look to sell some or all of their shareholdings.

Oftentimes these investors will have been holding for multiple years and will be looking to simply get back some of the money they invested in the company.

The selling then creates excess supply which can lead to share prices moving lower despite the positive news put out by the company.

In these scenarios the good news needs to bring in NEW investors who are willing to buy otherwise the selling from EXISTING shareholders creates a supply/demand imbalance.

Read more about capital structures here: Shares, Options and Performance Rights Explained

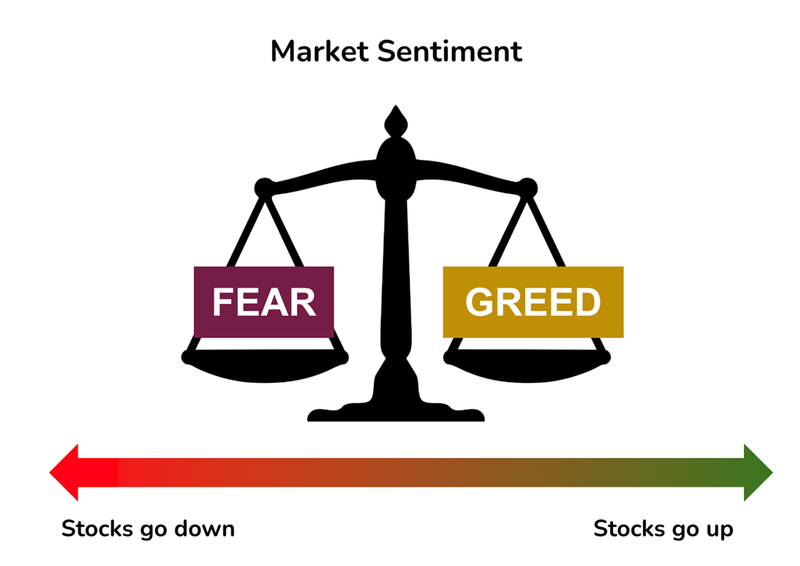

Market sentiment is poor

This is perhaps the most obvious of the factors.

When market sentiment is poor, investors are looking for the exits regardless of the strength of any news the company puts out.

When markets are looking dire (inflation is high, interest rates are high, recession, etc...) many investors choose to reduce their stock market exposures.

When the market is in a state of “fear” investors are looking to sell, and far fewer investors are looking to buy which creates a structural high supply, low demand scenario.

When the market is in “greed” mode, the opposite is true.

In a market full of “fearful” investors, all news, no matter how positive, is typically sold into, leading to share prices moving lower.

Conclusion: why share prices go down on good news

The stock market is an unpredictable thing, and although the company published good news, the share price might go down.

Getting an understanding of the expectations that drive share price movements once an announcement is made is critical to small cap investing.

We try to stay objective with our Bull/Bear/Base case scenarios, but even then, can be caught up in the hype of a small cap market catalyst - good or bad.

If expectations are not met, the share price will generally go down and if expectations are exceeded, then the share price will generally go up.

On top of all of this - broader market sentiment is important too.

The market tearing higher can amplify good news, or on a terrible day it can put a dampener on even the best news.

We hope this clears things up, and explains why share prices can go down on good news.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.