3 Ways Fund Managers Invest in Small Caps

Published 02-MAY-2022 14:34 P.M.

|

10 minute read

At Next Investors, we hold long term positions in small cap companies led by top management teams that provide exposure to macro themes we think will do well in the future.

Our diversified portfolio consists of more than 20 investments in early stage companies, most with market capitalisations below $25M.

We invest with the view that two or three of these will achieve success and deliver an outsized return, thereby outweighing any companies that fail.

We hold these positions over three to five years while the company executes its plans and we seek to take some profit along the way as the share price (hopefully) re-rates higher.

For these positions, we target 1,000% gains over the long term.

In our experience, the best place to achieve 1,000% returns is by investing in higher risk, early stage companies, then holding a long term position as they work to achieve their objectives and increase “certainty” around their business.

There will be some failures along the way, but that’s part of the risk at this end of the market.

As a successful company progresses through its development stages, the following tends to occur in time:

- Investors with a lower risk profile will enter as certainty increases

- Daily trading volumes increase as more people learn about the company

- The share price sustainably re-rates higher and the company’s market cap increases

...and a $25M company (hopefully) becomes a $100M+ company.

Why do these three key metrics matter so much?

Lowered investment risk, increased market cap, and higher trading volumes are very important progress points for an early stage company, primarily because it allows for professional fund managers and institutional investors strict mandates to start investing in these companies. .

As early stage investors, one of the fundamental goals of our investment plan is to hold an investment through the various different life cycles of a company’s development, until it is deemed “investable'' by these professional fund managers who manage massive amounts of capital on behalf of investors.

Once these fund managers start to build positions they effectively reward the earlier stage investors by buying their shares off them at (what we hope is higher prices) and then they tend to hold for the long term, bringing them onto a company’s register then underpins the new higher market cap (and share price).

These fund managers then position themselves to take a company from say a $100m market cap to the next stage of growth up to $500m + market caps which will then attract capital from even bigger, later stage professional fund managers.

So why don’t fund managers invest in the early stage companies that we invest in?

These fund managers often rely on a company being “more established”, which generally translates into companies with higher market caps versus the stocks we consider to be micro caps.

This naturally means, fund managers are sidelined by their mandates in our investment universe and are simply not able to make investments for a variety of reasons:

We believe these 3 key reasons are:

- Liquidity - Related mostly to trading volumes in a particular company.

- Benchmarking - Related mostly to measuring the funds' performance.

- Position-sizing - Related mostly to the size of a company’s market cap.

1. Fund managers need liquidity

These professional fund managers often have their funds open for “redemptions” - meaning, if investors in the fund want to take out their capital at any time they can simply apply for it, and the fund managers need to free up enough cash to pay back that investors' cash call.

This naturally means the fund managers need to be able to enter and exit a stock within a reasonable time frame.

When investing in micro cap stocks, well ahead of the broader market becoming interested in them there is usually very low trading volumes as a result of the company’s early stage nature.

This lack of trading volume and publicity means these stocks become un-investable for fund managers.

let's run through a hypothetical redemption scenario to try and understand why.

Let's say one of these funds has managed to take a $500k position in a micro cap stock that has a $5M market cap. This would mean the funds shareholding would make up ~10% of the company's total shares on issue.

Now let's say that 3 or 4 of the investors in that fund have gone off and purchased a new home. They are now approaching settlement and ask the fund manager to send back their cash (referred to as a “redemption”).

Nothing has changed with respect to the fundamentals of the company that the fund held a 10% position in BUT the circumstances of the investors in the fund have.

These fund managers are now in a position where they have become “forced sellers”.

They need to liquidate some of the funds positions to make sure they can pay back the investors who have put in redemption requests.

That fund manager now logs into their brokerage account and realises they need to sell some of that $500k investment.

In some instances the market may still not have caught onto the potential of that company. quickly realised that the market is still yet to catch onto the potential of the company.

That fund now becomes a forced seller of its 10% shareholding at a time when there is very little demand for shares in that company.

This is the worst case scenario for a longer term investor where, A) the fundamentals of the company have not changed and B) you are forced to sell shares at a time where the market isn't showing an interest in that particular company.

This level of selling pressure can kill a company’s share price and may mean that the $500k position is sold at a deep discount - crystallising losses in a company which the fund manager may still think is a good “long term investment opportunity''.

As a result of this “liquidity” issue, professional fund managers can’t afford to take on investments in small companies and need to have certainty about their ability to exit a stock.

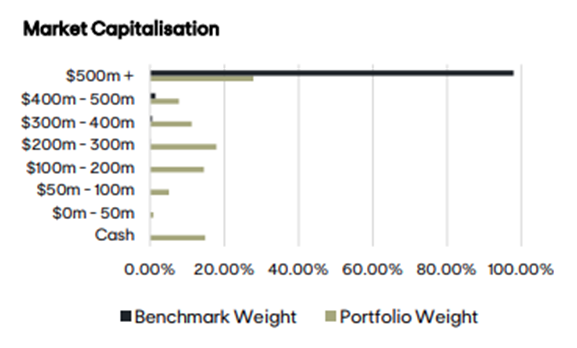

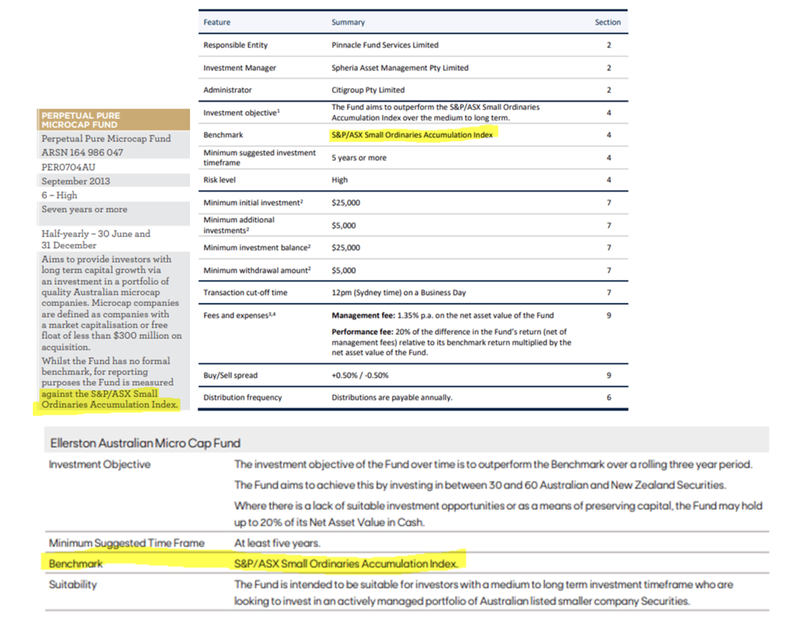

Below is an excerpt from Perpetual’s PDS (Product Disclosure Statement) which shows they are required to invest only in companies with higher market caps & more trading volumes:

Inherently this means the fund manager is forced to look at larger companies.

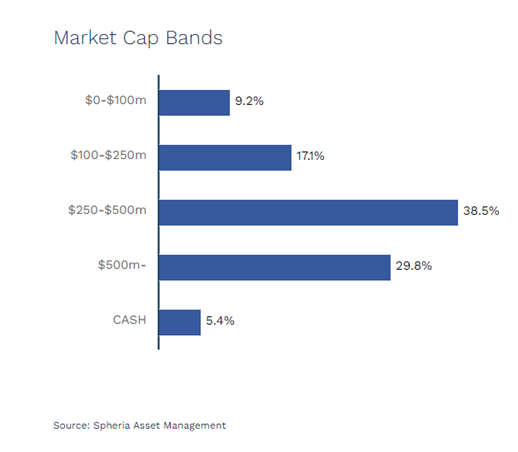

Below you can also see the bulk of other “Micro Cap fund” holdings are in companies with market caps well above the $100M mark:

2. Fund managers performance is measured relative to a benchmark

Professional fund managers live and die by their performance relative to a certain benchmark.

If they underperform, investors will ask for their capital back and if they overperform they attract more capital.

This leads to fund managers tracking the composition of these benchmarks closely as opposed to building a portfolio from scratch.

This creates a tendency to focus less on absolute returns and more on avoiding big periods of underperformance (relative to the benchmark).

Another way of summarising all of this is that the fund managers are incentivised to track the benchmark that their performance is measured against and sometimes the risks of trying to be unique are just not worth it for them.

Most of the funds that are marketed as “Micro-cap” Funds will be benchmarked against the ASX Small Cap All Ordinaries Index (ASX: XSO).

Reading through this index’s eligibility criteria we can see that only stocks above a certain market cap and with trading volumes that are “Institutionally investable” make the cut.

This pushes these professional fund managers towards investing in companies that are far more advanced than pure play micro-caps and will mean that preference is made for companies that are either already profitable, revenue generating, or simply put, have a much larger market cap.

This leaves a large part of the micro cap universe (sub-$100M market caps) as uninvestable to these fund managers.

This is where we think the opportunity lies for early-stage investors like us.

Naturally, our analysis is focussed on identifying companies that these professional fund managers will one day be looking to buy, at much higher share prices, once the company has delivered on certain business objectives and becomes large enough for these professionals to add to their portfolios.

Below are images in some of these funds' PDS showing the funds benchmark.

3. Fund Managers take larger positions

This brings us to the last of the reasons: position sizing.

Believe it or not, having a lot of cash to invest is not always a good thing.

These professional fund managers typically invest in excess of $50M across a portfolio of stocks.

This inevitably leads these funds to shun smaller, less liquid companies, simply because they can't take a big enough position without significantly moving the share price or simply because there just isn't enough “liquidity” (shares available for sale) for a position to be built.

Let's run through another hypothetical scenario:

If a fund with $50M in funds under management wanted to allocate 5% to invest in a particular stock, this would be a $2.5M investment.

Now let’s say that investment is a $10M-capped junior exploration company, this would translate to the professional fund manager trying to build a position that makes up ~25% of the explorer's market cap.

As you can see, an investment of this size simply isn't possible without moving the share price by +50-100% as the buying pressure simply outweighs the amount of shares for sale.

No matter how tempting, these types of investments are almost never done at the fund-level due to the above mentioned “Liquidity” and “Benchmarking” issues.

Fund managers must wait until this exploration company delivers results that move its market cap and trading liquidity into “investable” territories. Often this means buying it at a share price well above where we would have made our initial Investment.

In essence, these professionals are limited by the sheer size of the funds they manage.

They can’t take positions in early stage, high-risk, high-reward companies with market caps below a certain level.

What does this mean for early stage investors?

Bringing this all together, there are obvious advantages to allocating capital to a professional fund manager — they charge a small fee and do all of the work for you.

But they also face limitations, particularly when investing in small, early stage companies.

These are the companies that we prefer to invest in — what we consider true micro cap stocks, with market caps of less than $50M to $100M.

This is where we think we have an edge, as many funds are limited by their investment mandates and can’t invest in the early stage companies we look at...

We think by doing our research and investing whilst the market is yet to catch onto microcap companies' potential, we can back the companies that one day these professionals can invest in at much higher prices.

Naturally, this means that the ultimate aim for early stage investors like ourselves is to invest in companies with high quality future prospects and hope that they can grow large enough that these professional funds start to take an interest and invest looking to take them through their next stage of growth.

We maintain a diversified portfolio because early stage investing is high risk with a lot of uncertainty around execution.

Most small companies we invest in will fail to achieve enough of their objectives to progress to a stage that becomes investable by professional fund managers, but for the few that do we expect to deliver significant returns.

We seek to identify early stage companies that we think have the highest chance to deliver their business plan and move to a stage that can attract institutional capital.

Our aim is to hold a position along this journey from $25M market cap to $100M, then to $500M, and hopefully beyond, as progressively bigger institutional funds join us along the way.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.