Critical Minerals and the Commodities "Supercycle"

Published 11-SEP-2023 15:00 P.M.

|

8 minute read

What are Critical Minerals

Critical minerals are a group of raw materials that governments see as important and have fragile supply chains.

Think copper, nickel, rare earths, lithium, graphite etc... largely battery materials and energy transition metals.

In a globalised world, resource supply chains have been taken for granted.

Commodities were seen as a “boring” part of trade until governments realised they needed them to keep their economies going while achieving energy independence and reaching their net zero emissions targets.

Suddenly the language around commodities changed as both governments and investors began to recognise these minerals as “critical.”

The key demand driver for much of this has been the electric vehicle revolution and electrification of energy grids all around the world.

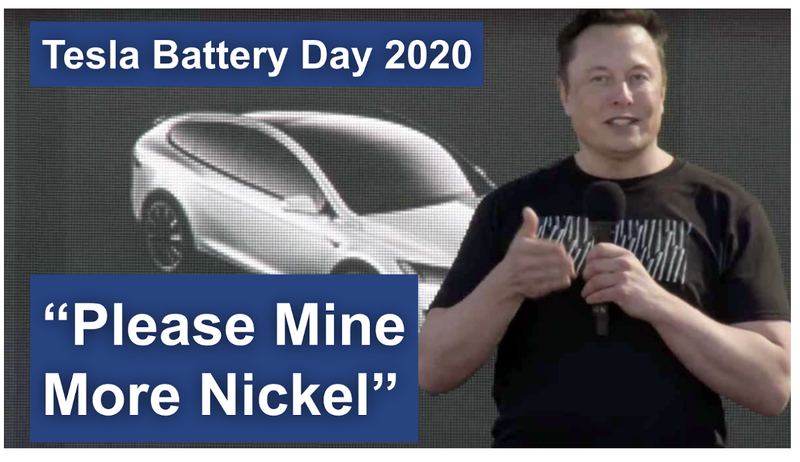

A pivotal moment came at US carmaker Tesla’s Battery Day in September 2020, when Elon Musk implored the world for more nickel and the supply risk around manganese and lithium.

Other automotive companies followed suit, with Volkswagen presenting at their own “Power Day”, announcing that they would phase out petrol cars by 2025.

But it's not only EV and battery minerals that were seen as critical.

In October of 2021 the annual green energy summit, COP 26, was probably the most important green energy summit ever.

The headline theme at the summit - critical minerals.

Reality started to dawn on the key decision makers on the global stage...

In order to make eclectic vehicles, power lines, solar panels and wind farms the world is going to need a lot more minerals.

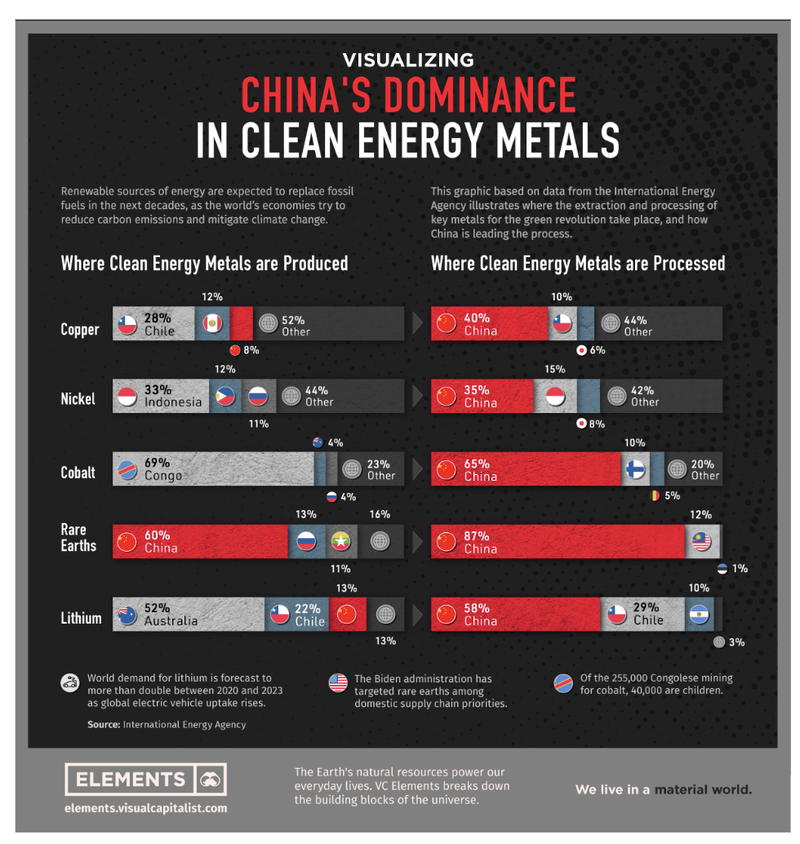

The problem is that there are not enough minerals to meet forecast demand, and most of the world’s critical minerals processing supply is dominated by one country, China.

There are two key features that make minerals critical:

- Use in next generation energy technologies - Resources essential for modern technology, renewable energy or national security

- Fragile supply chains - There is a risk of supply chain disruption

Identifying resources that fit both of these categories have helped countries develop “critical mineral strategies” to secure the supply of these essential resources.

These strategies are in place to reduce supply chain risks around critical minerals and reduce reliance on unfriendly nations for key mineral supply.

This is done by encouraging investment in localised resource projects through government legislation and funding.

Countries that are too reliant on unfriendly nations for resources may find themselves behind in the technology race, particularly as countries look to decarbonise and reach net-zero.

It is a national security issue that is tied to the global drive towards a renewable energy future.

Critical minerals have only recently emerged as important for governments around the world, but a struggle over resources has existed since the dawn of time.

The “Commodities Supercycle”

Whether it is control over food, water, oil or gold - the nations that control the supply of in-demand resources gain power and status in the world order.

The concept of “critical minerals” however is relatively new.

Commodities like lithium, rare earths, manganese and cobalt are starting to climb the ranks of importance on the global stage.

Over the last 20+ years mining stocks have been seen as “old economy stocks”.

Investors have shunned them in favour of technology stocks which they saw as highly scalable and leveraged to growth.

This has led to decades of under-investment in developing news mines, in particular for commodities like lithium and rare earths.

The green energy revolution has exposed how unprepared the world is to meet the raw-materials demand that is set to be unleashed over the next 5-10 years as the world transitions towards clean energy.

This is called the “Commodities Supercycle”.

Commodities supercycles have happened in the past, here is a lookback at the history of commodities supercycles:

- US industrialisation: Late 1890s through to a peak in 1917 - the US was rapidly industrialising and the supercycle peak coincided with the entry of the US into World War 1 - it continued until the early 1930s.

- World War and the rebuild: The next supercycle began in the lead up to the Second World War. The war itself and rebuilding in the aftermath required lots of materials - it peaked in 1951, and this demand continued through to the early 60s

- Cold war and Nationalisation: The early 1970s marked the start of the third cycle as commodity supply was disrupted as the Cold War saw countries nationalise industries and foreign investors pulled out. In the mid 1980s producers managed to shore up supply and the cycle faded.

- China Industrialisation: The most recent supercycle started in 2000 when China joined the World Trade Organisation (WTO) and started to modernise. The raw materials China needed to do this sparked a long bull run for commodities. The 2008 GFC put a spanner in the works but Chinese stimulus made the cycle continue through to 2014 when oil cratered on oversupply.

Source: Forbes: Are We About To Enter A Commodity Supercycle?

So, how did we get here?

A history of critical minerals

In 2021 the US published the first ever modern “critical minerals strategy”.

There was a recognition that the US lacked domestic production capabilities and was reliant on imports.

This put the US in a precarious position, particularly at a time when the global economy was shutting down due to COVID-19.

Other nations soon followed, with Australia and Europe publishing its own critical minerals strategies soon after.

Between 2020 and 2022 critical mineral supply dominated the global agenda, in particular due to the commitments made by countries to meet net-zero carbon emissions at the COP-26 global energy conference in late 2021.

The supply chain risks were also highlighted by the Russia-Ukraine conflict, as energy prices, particularly in Europe, skyrocketed.

Underdevelopment and underinvestment in traditional energy (like oil, coal and natural gas), meant that the world was going “all in” on the global energy transition.

Energy prices were going up as coal plants were shutting down and the urgency to develop renewable energy projects became ever more pronounced.

But there was a bottleneck in renewable energy and energy storage supply chains.

Critical minerals.

And who controlled this bottleneck?

China.

Western countries, in particular the US and Europe, viewed this dominance as a national security threat.

Europe in particular was reminded of their mistakes in relying too heavily on Russia for natural gas production.

Not wanting to be put in a similar position, the US introduced legislation to “friendshore” the import of certain minerals, providing generous tax cuts to friendly nations.

The Inflation Reduction Act and CHIPS Act were direct answers to the dominance of China in the resources space.

What this has meant for commodities juniors like the ones we Invest in is more:

- Access to capital from governments - IRA ~$400B in federal funds

- Access to capital from institutions - EV carmakers are now investing directly into mining companies

- Access to capital from investors - easier to raise capital and execute ideas.

There has been a specific increase in demand for minerals like lithium from EV makers with a focus on projects located outside of China.

It takes about 3 years to build up a battery factory, but 17 years to take a mine online from initial discovery.

The resources industry can’t catch up quick enough to the demand, which has pushed the price of these minerals higher and higher.

Only time will tell how long the commodities supercycle will last, but as long as there is a drive for clean energy and a drive for national security, resources will be in demand.

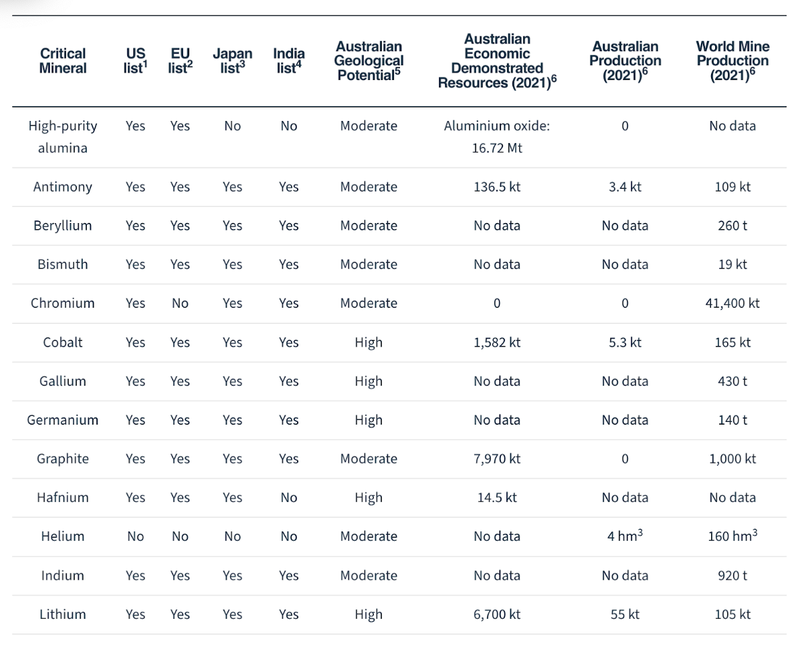

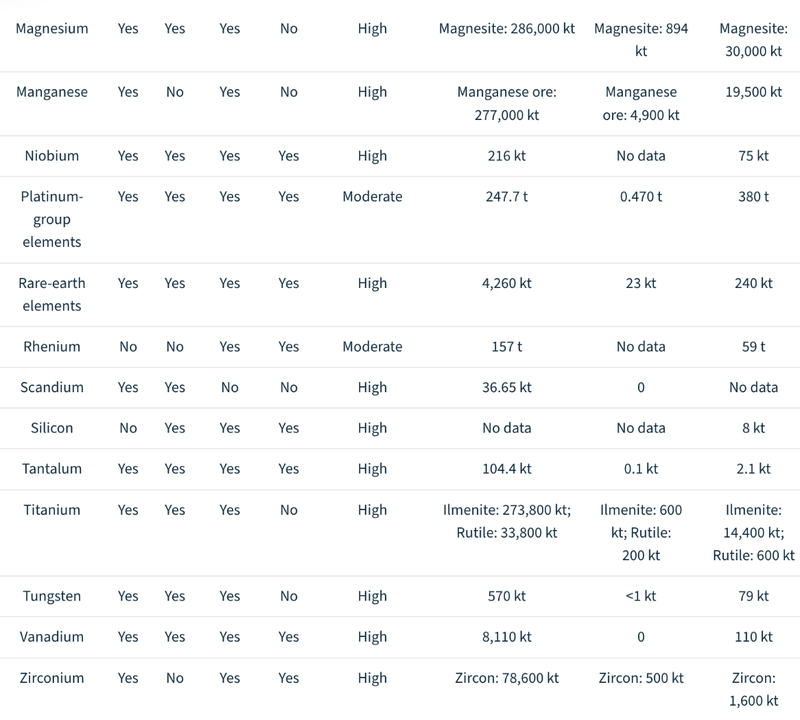

A list of critical minerals

Each country has their own list of critical minerals here is the list of minerals that Australia views as critical.

You can find the list of critical minerals in Australia here: List of Australian Critical Minerals

Part of the Australian critical minerals strategy is to be a supplier of these critical minerals to key Western allies like Europe and the US - and take advantage of the generous tax credits.

Although Australia mines a lot of these minerals, the majority of the processing is done in China, so there is a real push by the Australian government to encourage investment in processing facilities for these minerals (including the $2B Modern Manufacturing Fund).

For more information read the Australian Critical Minerals Strategy 2023.

What’s next for critical minerals?

It is hard to predict the future, particularly when it comes to commodity prices.

There is an old saying that “the best cure for high prices is high prices”.

This is most true in commodity cycles, where high prices for critical minerals encourage more supply and new technologies that use substitutes elements to reduce prices.

That said, the pace and scale at which the world intends to move to a clean energy future will require A LOT more minerals... and new supply can’t come online fast enough.

And as each nation looks to “friendshore” their own supply of critical minerals, we expect a sustained level of demand for commodities in the years to come.

There will be movements, up and down, as the economy slows or grows - but in the long term we see a bright future for commodities and have set up our Investment Portfolio accordingly.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.