Investment Memo:

Patriot Resources Ltd

(ASX:PAT)

-

LIVE

Opened: 13-Apr-2026

Shares Held at Open: 18,680,000

What does PAT do?

Patriot Resources (ASX:PAT) owns a silver project in southern Peru with a 31.4 million ounce silver equivalent JORC resource.

PAT also has two non-core assets (copper in Zambia, lithium in Canada) that we think the company could deal out to fund its silver project.

What is the macro theme?

Silver is both an industrial and a precious metal.

Silver also has a prominent industrial use case in the manufacture of photovoltaic cells for solar panels - and as such can be considered important to the energy transition.

Silver just recently made all time highs and we think it is now finding a base to consolidate in before another run higher.

(of course we could be wrong - no one knows what's going to happen with commodity prices)

PAT’s projects are in Peru which is the 3rd biggest producer of silver in the world.

Our Big Bet for PAT

"PAT re-rates to a $150M plus market cap by proving up the size and scale of its Peruvian silver asset"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PAT Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Why did we invest in PAT?

We think silver is getting ready to run to new all time highs

Silver was the best performing commodity of 2025.

From its March 2025 lows of US$29/oz, it went to a peak of US$121/oz just ten months later in January 2026:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

But like most price run ups, silver needs to consolidate at a new higher level for a while - which it has been doing for the last two months.

And after some consolidation... we think it’s going higher than its January all time highs (we could be wrong though, of course).

PAT has an existing 31.4M ounce silver equivalent resource that we think can grow

PAT’s project has a JORC 31.4M ounce silver equivalent resource.

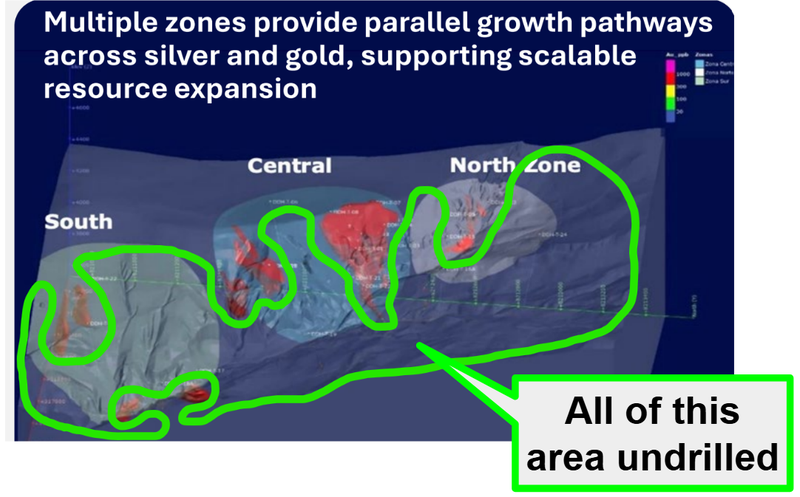

PAT’s resource is open in all directions across a ~2.8km structural corridor.

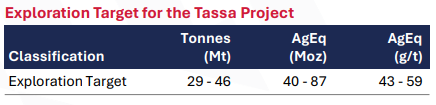

The project also has a 40-87M ounce silver equivalent exploration target. With some drilling we think PAT can get closer to that upper end (and potentially extend way beyond that number).

(Source)

Only 26 drill holes have been completed across a 2.8km structural corridor and there are IP geophysical anomalies down to ~100-400m depth that remain largely undrilled.

(and some targets to the north down to ~500m depths - completely untested)

(source)

We are backing the team from Prospect Resources here

PAT’s got the same team behind it as Prospect Resources.

PAT’s chairman, Hugh Warner, was one of the co-founders of Prospect Resources, where he oversaw the Arcadia lithium project in Zimbabwe, picking up the asset, making the discovery, then growing that into what is now the largest operating lithium mine in Africa.

(Hugh holds ~6.3% of PAT shares at last count and is one of PAT’s single biggest shareholders).

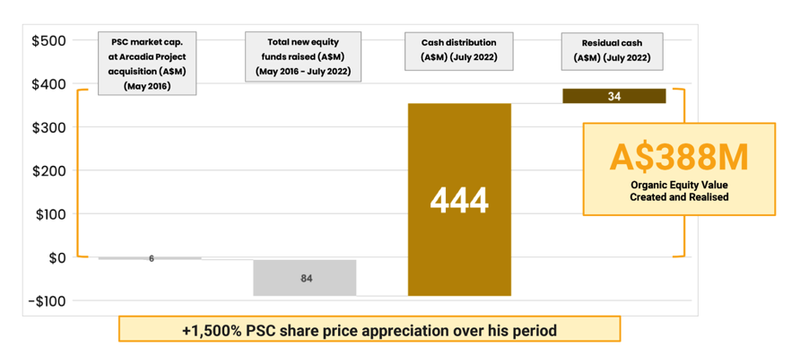

Prospect Resources ended up selling that lithium asset for US$378M in 2022 and returned ~A$444M to shareholders off the back of the sale - an incredible outcome for what started as a $6M capped explorer in 2016.

We Invested in PAT now in the early stages of its exploration as we are backing Hugh to repeat the same formula as he executed at Prospect Resources.

He has brought some of the Prospect team along with him into PAT too.

(source)

~$12M market cap and a tight capital structure.

PAT trades at an enterprise value of ~$7M ($12M market cap, ~$4.9M cash and no debt).

(That cash balance is based on our $500K we just committed to at 5c, plus $2.2M cash at 31 Dec + the $2.25M T2 placement, settled in January)

PAT also has a fairly tight capital structure with only ~290M shares on issue and high ownership amongst the management team.

The current resource underpins PAT’s valuation

PAT trades at an enterprise value of ~$7M.

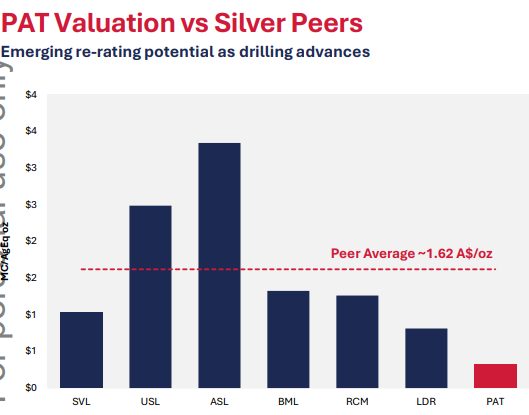

With a 31.4M ounce silver equivalent resource, PAT’s effectively trading at an EV/silver equivalent ounce of resource at $0.22 per ounce.

For context - Andean Silver (ASX: ASL), a more advanced development stage silver-gold play in Chile, trades at ~A$2.20/oz (based on yesterday’s close price).

Here is how PAT ranks against other peers:

(source - PAT presentation from March 2026)

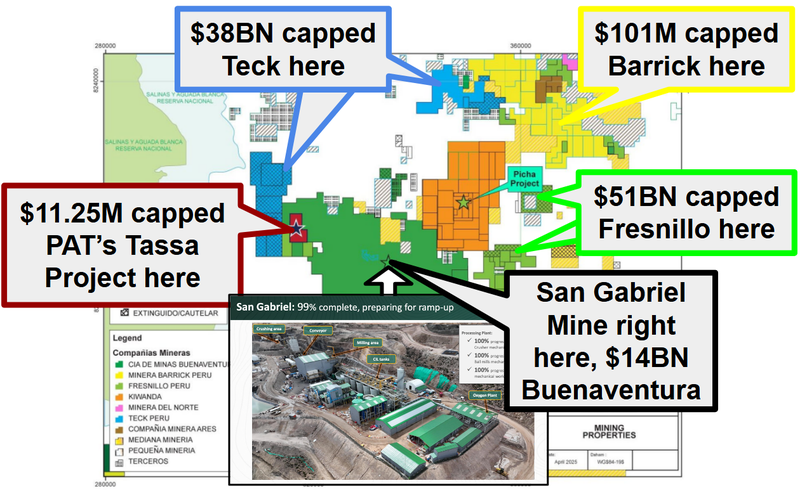

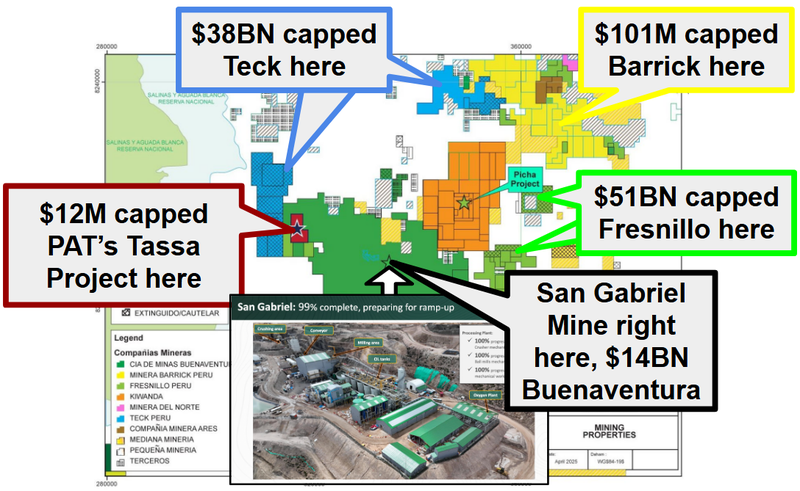

PAT’s silver asset was previously owned by $38BN Teck Resources

Teck - one of the world's largest diversified miners - had the asset for 4 years, validated the geology and secured drill permits.

Then, before a single hole was drilled Teck walked away in 2024 as the company repositioned as a pure-play copper company.

We think that if the project was interesting enough for one of the world’s biggest miners - Teck - to spend time and cash on the asset then we think it could be a potential company maker for a small cap like PAT.

PAT’s project is next door to the 1.8M ounce San Gabriel gold mine, owned by $14BN capped Buenaventura

PAT’s direct neighbour, Compañía de Minas Buenaventura (NYSE: BVM), has 1.8 million ounces of Proven and Probable gold reserves at 3.71 g.t gold and 3.1 million ounces of silver.

The San Gabriel gold mine poured its first gold bar on December 23rd, 2025.

PAT’s project gets to benefit from all the infrastructure developed by Buenaventura (and the interest that would have come into this part of Peru).

(Source)

Peru is a fertile hunting ground for silver

Peru is the third largest producer of silver in the world accounting for ~13% of global silver production.

It’s also home to some of the biggest silver mines in the world.

The area PAT operates in is active with some of the world’s biggest mining companies like $38BN Teck Resources, $101BN Barrick and $51BN Fresnillo.

(source)

Exploration upside in addition to silver (gold and copper)

We think there is also gold (and copper) exploration upside on PAT’s project.

As mentioned earlier, PAT’s project is ~18km away from the San Gabriel gold mine - which entered production in late 2025.

It's also ~16km away from the ~6M ounce gold, ~46M ounce silver Chucapaca deposit owned by Goldfields/Buenaventura.

PAT’s project has similar deep gold targets to the Chucapaca deposit, which to date, have only been tested by three holes that all hit gold (albeit at low grades) - 81.9m at 0.41 g/t gold and ~234m at 0.25g/t gold.

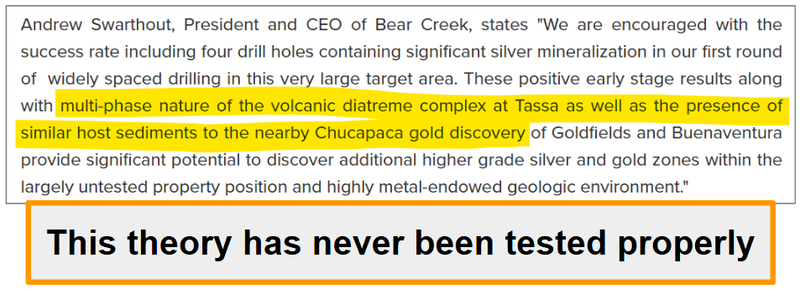

The CEO of the previous owners of the project had said in 2010 that the "multi-phase nature of the volcanic diatreme complex at Tassa as well as the presence of similar host sediments to the nearby Chucapaca gold discovery”.

So it will be interesting to see what PAT finds with some deeper drilling.

(source)

Two non-core projects could be sold to free up cash for the silver project

PAT also has two non-core assets that we think could provide non-dilutive funding for the company (IF sold):

- A lithium asset in Canada - PAT’s project sits along strike from ~$160M Frontier Lithium’s deposits - one of North America’s largest and highest grade lithium deposits, expected to come into production in the coming years.

As mentioned earlier, PAT’s team knows lithium well (from the Prospect exit), so we are backing them to get the most out of this asset for PAT.

- Copper in Zambia - PAT’s project sits ~4km from Sinomine Resources Group's Kitumba copper processing plant (which is scheduled to come online in late 2026).

This asset is fairly early stage (trenching/sampling) BUT if a few drillholes are put in and they come in, it could become an interesting M&A target for the owners of that nearby plant.

What do we expect PAT to deliver?

Objective #1: Drill and update the current silver resource

We want to see PAT drill its silver project in Peru and confirm the existing 31.4M ounce silver equivalent JORC resource.

With the first program, we want to see the previous results confirmed with infill drilling.

Milestones

Phase 1 drill program (mostly infill drilling)

Phase 1 drill program (mostly infill drilling)

Assay results from phase 1 drilling

Updated JORC resource.

Objective #2: Drill and grow the current resource

Once PAT has run some infill drilling campaigns, we will be looking for PAT to do some exploratory drilling by stepping out and testing extensional/deeper targets.

That’s where we are hoping PAT grows its current 31M oz silver equivalent resource to the upper end of its 87M ounce silver equivalent exploration target.

By growing the resource PAT will be able to be better compared to its other silver peers on the ASX.

Milestones

Phase 2 drill program (mostly infill drilling)

Assay results from phase 1 drilling

Updated JORC resource (target: 50M+ silver equivalent ounces)

Objective #3: (Bonus): Sell non-core assets

We think PAT could also unlock capital for its silver asset in Peru by spinning out its projects in Zambia and Canada. Any deal here would be a bonus.

(PAT has a copper asset in Zambia and a lithium asset in Canada).

Exploration risk

The company’s silver project has a resource based on ~26 historical drill cores and is 100% in the inferred category.

There is no guarantee that PAT's upcoming drill programs will confirm the presence of additional mineralisation, upgrade the resource classification, or deliver the kind of results needed to justify a development pathway.

Early-stage exploration is inherently risky and many projects fail to deliver economic mineralisation.

Commodity price risk

PAT, as a silver exploration company is exposed to movements in the silver price.

Silver prices are currently near all-time highs - should silver prices fall, this could hurt the PAT share price significantly.

A silver price correction from current levels is a real and meaningful risk.

Funding risk / dilution risk

PAT is a pre-revenue explorer and so it is always reliant on access to fresh capital to fund drilling and exploration.

Further capital raises will be needed, and these may take place at a discount to the prevailing share price, diluting existing shareholders.

PAT’s silver project also has deferred cash payments attached for up to US$3M over 30 months, so PAT may need to raise to fund these payments also.

There is no guarantee PAT can access capital on favourable terms.

Geopolitical risk

Peru has experienced significant political instability in recent years, with three presidents since 2023.

The country has also had problems with illegal mining operations and social conflicts stalling new project developments.

PAT’s silver project is in the pre-permit phase for drilling operations right now and there is no guarantee that community relations or regulatory approvals will proceed smoothly.

There is also a risk that PAT gets "stuck" in early-stage exploration without progressing to scoping studies, feasibility, or attracting a development partner due to the geopolitical/political risks in country.

Delays could mean newsflow dries up and PAT’s share price drifts lower.

Market risk

Broader market sentiment could deteriorate, particularly for small-cap explorers.

If the ASX small-cap market enters a period of weakness, PAT could struggle to attract the capital and attention needed to advance its silver project, regardless of the quality of the underlying asset.

Other risks

Like any small-cap exploration company, PAT carries significant risk, here we aim to identify a few more risks.

While PAT has an existing 31.4M ounce silver equivalent JORC resource, it is entirely in the 'Inferred' category and based on just 26 drill holes.

There is a high statistical probability that infill and step-out drilling fails to replicate the grades or continuity needed to upgrade the resource classification to 'Indicated' or 'Measured', which are required for robust economic studies.

Operating across vastly different jurisdictions, Peru for silver, Canada for lithium, and Zambia for copper also stretches management bandwidth. Advancing multiple exploration fronts simultaneously requires immense capital and logistical effort.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our investment plan?

Our plan is to hold the majority of our position in PAT for a minimum of 18 months, which we hope is enough time to see PAT drill out its project, hopefully make more discoveries and the silver price to go on the run we hope it will.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates in line with our minimum hold conditions.

We intend to maintain a position in PAT for 2 to 5 years.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 18,680,000 PAT Shares at the time of publishing this article. The Company has been engaged by PAT to share our commentary on the progress of our Investment in PAT over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.