L1M is capped at just $7.3M at the time of writing this Investment Memo. We think L1M’s valuation here is leveraged to exploration success.

ASX:L1M

Lightning Minerals Ltd

ASX:L1M

- Lightning Minerals Ltd

has engaged Next Investors to provide this service.")

$0.013

Last Price

Investment Memo:

Lightning Minerals Ltd (ASX:L1M)

- LIVEOpened: 12-Sep-2025

Shares Held at Open: 8,375,696

Options Held at Open: 3,773,077

What does L1M do?

L1M is a junior exploration company with gold-copper projects in Australia and lithium projects Brazil.

What is the macro theme?

L1M has exposure to:

- Gold - a precious metal which is often seen as an insurance against inflation, uncertain markets and as a reserve asset. Gold is trading at all time highs at the time of this memo.

- Copper - the third most widely used metal in the world, leveraged to the global electrification thematic.

- Lithium - exposure to the electrification thematic because of its use in EV/storage batteries.

Our Big Bet for L1M

“L1M discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our L1M Investment Memo.

Why did we invest in L1M?

Tiny market cap, leveraged to exploration success

Multi-commodity exposure

L1M now has a mix of gold, copper and lithium exploration projects in its portfolio. We like this, especially in a very small explorer, because it means the company can pivot to a project that the market will be willing to re-rate based on the current macro momentum in any particular sector.

Drilling to start on gold projects very soon (short term catalyst)

L1M’s QLD gold project has over 12.5km of strike that hasn’t seen any modern drilling yet. We like that L1M will be drilling the project in the coming weeks.

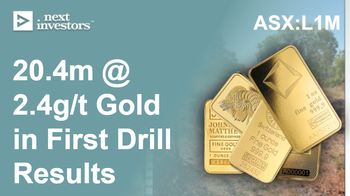

QLD project has had good gold hits before

Previous drilling on L1M’s QLD gold project has hit 16m at 3.56 g/t gold, 16.0m at 3.60g/t gold and 12m at 6.5g/t gold. We think the market will like results similar to or better than this (IF L1M can deliver them).

QLD project has multiple undrilled copper porphyry targets

L1M also has three copper porphyry targets that have already been identified on its QLD asset. We think these are strong drill targets for a company of L1M’s market cap.

NSW copper-gold asset is in the same region as majors

L1M’s NSW asset in particular, sits next to projects owned by Newmont and Evolution Mining.

Bear market lithium exposure

L1M has lithium ground in Brazil’s Minas Gerais next to heavyweights like Sigma Lithium (60km away) and Pilbara Minerals (20km away). If market interest returns to the lithium sector, L1M’s assets could suddenly become more valuable.

We have had success Investing in Brazilian lithium before

One of our best Investments was Latin Resources, which made a hard rock lithium discovery and was re-rated to a high of ~42c per share—2,332% above our Initial Entry Price.

What do we expect L1M to deliver?

Objective #1: Drilling at L1M’s gold targets in QLD

L1M expects drilling to start the week beginning 15th September.

Milestones

![]() Drilling commenced

Drilling commenced

![]() Drilling visuals

Drilling visuals

![]() Assay results

Assay results

Objective #2: Drilling on L1M’s copper targets in QLD

We want to see L1M drill its three copper porphyry targets right after the upcoming gold drilling is completed.

Milestones

![]() Geophysics

Geophysics

![]() Program of work defined

Program of work defined

![]() Drilling commenced

Drilling commenced

![]() Assay results

Assay results

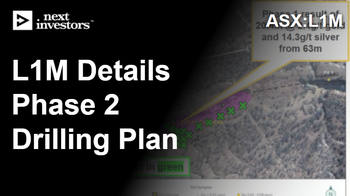

Objective #3: Target generation across the QLD, NSW and Vic assets

We want to see soil sampling, geophysics and other geochemical work completed across all of the newly acquired assets.

Ideally, new drill targets will be ranked across all projects ready for drilling in 2026.

Milestones

![]() Geochemical sampling (soils, trenching)

Geochemical sampling (soils, trenching)

![]() Geophysical surveys

Geophysical surveys

![]() Identify drill targets

Identify drill targets

Objective #4: Target generation across the other assets

L1M plans to continue working on its Brazilian lithium and WA lithium/gold assets.

We are still looking forward to seeing new targets ranked across these over the coming months. Especially on the lithium which could become interesting again if the macro sentiment changes for the sector

Milestones

![]() Geochemical sampling (soils, trenching)

Geochemical sampling (soils, trenching)

![]() Geophysical surveys

Geophysical surveys

![]() Identify drill targets

Identify drill targets

What could go wrong?

Exploration risk

L1M is still a long way from a discovery, and even further from defining a resource.

Like all micro cap minerals explorers, the risk is that L1M finds no economic mineralisation on its assets - in which case we would expect to see the share price re-rate lower.

Delay risk

L1M plans to drill two parts of its project (the gold targets and the copper targets) all before the end of the year.

There is a risk there is some slippage in these timelines and IF L1M were to have big enough delays it could lead to the market losing interest in the stock.

Significant delays could be negative for L1M’s share price as it would burn down the company’s cash balance and bring the company to a position where it needs to raise more capital and dilute existing shareholders.

Funding risk/dilution risk

As a pre revenue explorer, L1M is dependent on capital markets to fund ongoing drilling and development.

That could come at discounted prices and further dilute existing shareholders.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract.

Should gold or copper prices fall, this could hurt the L1M’s share price.

We have already seen this happen with the lithium price and what it meant for L1M’s Brazilian assets.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking L1M’s share price with it.

Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

What is our investment plan?

We are Invested in L1M to make a discovery and define a gold discovery.

Our plan is to hold the majority of our position in L1M into the upcoming drilling program.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates in line with our minimum hold conditions.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 8,375,696 L1M Shares and 3,773,077 L1M Options at the time of publishing this Investment Memo. The Company has been engaged by L1M to share our commentary on the progress of our Investment in L1M over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Investment Memo:

Lightning Minerals Ltd (ASX:L1M)

- LIVEOpened: 02-May-2024

Shares Held at Open: 6,360,712

What does L1M do?

Lightning Minerals (ASX:L1M) is a hard rock lithium explorer with projects in Brazil (and also Western Australia, which are quite interesting too).

What is the macro theme?

Lithium is a critical material used in Electric Vehicle (EV) battery cathodes.

We believe battery metals are the most compelling investment theme of this decade with lithium supply deficits anticipated through to the end of 2030.

L1M will be looking to replicate the success of other Brazilian lithium companies like Sigma Lithium and Latin Resources.

Our Big Bet for L1M

“L1M discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our L1M Investment Memo.

Why did we invest in L1M?

We have had success Investing in Brazilian lithium before

One of our best Investments was Latin Resources, which made a hard rock lithium discovery and was re-rated to a high of ~42c per share—2,332% above our Initial Entry Price. L1M is following the same exploration playbook, 20km away.

Two of Brazil’s biggest lithium projects are near L1M

L1M’s ground sits between $545M Latin Resources (20km away) and $2.3BN Sigma Lithium (60km away), both of which are the big pioneers of the lithium industry in Brazil.

Minas Gerais is Brazil’s “Lithium Valley”

The state aims to be the biggest lithium province in Brazil. The “Lithium Valley” concept was launched in the State of Minas Gerais to promote foreign investment in Brazilian lithium projects.

Rio Tinto moving into Minas Gerais in a big way

Rio Tinto has started pegging ground to the north of LRS and Sigma. Could Rio Tinto be setting up for a play on the region as a whole? Rio is already active in Argentina so South American assets are definitely not out of their remit.

L1M’s project sits on similar geology to LRS and Sigma

L1M’s ground sits on top of similar geology to where Latin Resources made its discovery (the Salinas Formation). The projects also sit within similar proximity of the granites in the region & has similar aeromagnetic data running through the ground.

Exploration “roll of the dice”

Our other Investment SLM was trying to find lithium in Brazil, and it ran from ~13c to ~$1.34 per share. Unfortunately it didn’t deliver a discovery (yet, we still hold). We are betting on L1M as another early stage “the next LRS” exploration bet to hold in our Portfolio.

Bear market pick up

L1M is picking up ground in a lithium bear market, which means the likelihood of finding higher-quality, well-priced projects is higher.

There is an existing playbook for success in Brazil

Companies like Sigma have gone from <$100M market cap explorer to a peak market cap >$4BN. Latin Resources has gone from <$20M market cap to a peak of ~$1BN. There is a proven valuation re-rate for companies that manage to make hard rock lithium discoveries in the region.

Tight capital structure

After acquiring the Brazilian assets, L1M will have ~99M shares, which means there aren't many shares on issue. The top 20 hold ~47%, and the board and management hold ~8.7% of the company’s shares on issue.

Low market cap leveraged for a re-rate on a discovery

Post acquisition at 7c per share, L1M has a market cap of ~$6.5M leaving plenty of room to re-rate off the back of a discovery, especially given the peer valuations in the region like Sigma and Latin Resources.

Good deal terms tied to success on the project

Bulk of the consideration being paid for the assets are tied to milestone payments related to defining a JORC resource, NOT the usual “lithium bearing drill intercepts” we see on project acquisitions.

What do we expect L1M to deliver?

Objective #1: Find high priority drill targets

We want to see L1M conduct geochemical and geophysical surveys and determine the best drilling spots at its Brazilian lithium project.

L1M kicks off Brazilian lithium exploration program

[24-Jul-2024]

L1M working up Brazilian lithium targets [04-Oct-2024]

L1M: Drilling in coming weeks - following up ~4% lithium found in artisanal mine [17-Jan-2025]

L1M working up Brazilian lithium targets [04-Oct-2024]

L1M: Drilling in coming weeks - following up ~4% lithium found in artisanal mine [17-Jan-2025]

Milestones

![]() Geological mapping

Geological mapping

![]() Rock chip sampling

Rock chip sampling

![]() Soil sampling

Soil sampling

![]() Define high-priority drill targets

Define high-priority drill targets

Objective #2: Drill high priority targets

We want to see L1M drill its best targets.

L1M kicks off Brazilian lithium exploration program

[24-Jul-2024]

L1M: Drilling in coming weeks - following up ~4% lithium found in artisanal mine [17-Jan-2025]

L1M: Drilling in coming weeks - following up ~4% lithium found in artisanal mine [17-Jan-2025]

Milestones

![]() Drilling permits

Drilling permits

![]() Drilling starts

Drilling starts

![]() Drilling completed

Drilling completed

![]() Assay results

Assay results

Objective #3: Exercise option to acquire Brazilian lithium project

After de-risking the project, we want to see L1M exercise its option and acquire the project

Milestones

![]() Exercise the option to acquire the project

Exercise the option to acquire the project

Objective #4: Drilling at WA lithium project

We want to see L1M do some more sampling work before drilling one of the priority targets at its WA lithium asset (Dundas)

Milestones

![]() Geochemical/Geophysical surveys

Geochemical/Geophysical surveys

![]() Drilling starts

Drilling starts

![]() Drilling completed

Drilling completed

![]() Assay results

Assay results

What could go wrong?

Exploration risk

L1M’s project is an early stage exploration asset. There is always a risk that L1M finds no targets worthy of drilling or that, even after drilling, the company fails to find any economic lithium mineralisation. As a result, exploration risk is one of the primary risks for L1M.

L1M drilling booked in - 2 weeks to go

[06-Feb-2025]

Microcap L1M going for a new discovery… up the road from billion dollar producers [21-Feb-2025]

Microcap L1M going for a new discovery… up the road from billion dollar producers [21-Feb-2025]

Deal completion risk

L1M’s Brazilian assets are yet to be acquired and will still need to have the “option to acquire” exercised. L1M will also need to get shareholder approvals for the transaction which is never guaranteed to proceed. There is always a risk that the deal isn’t completed and L1M ends up with no asset ownership. In that scenario, L1M’s share price would likely be impacted negatively, and it will likely seek other assets to complement its existing ones, which could take time.

Financing risk

L1M does not generate revenues and relies on raising capital to fund its exploration programs. If the market is unwilling to fund the company, it risks being unable to drill its project or offering large discounts to its share price when raising capital.

L1M drilling booked in - 2 weeks to go

[06-Feb-2025]

Microcap L1M going for a new discovery… up the road from billion dollar producers [21-Feb-2025]

Microcap L1M going for a new discovery… up the road from billion dollar producers [21-Feb-2025]

Commodity price risk

The lithium price is very volatile, given that the market is still in its infancy. There is a risk the lithium price fails to recover, and the valuations for greenfields explorers or new discoveries aren't as high as they would have been in a stronger price environment. Low lithium prices will impact L1M’s share price in the long run.

Market risk

Investors may shy away from high-risk investment opportunities like junior explorers if the broader market sells off. During market downturns, investors will look to pull capital away from high-risk investments. L1M is a junior explorer and may be impacted by these market-wide sell-offs.

What is our investment plan?

Exploration is high risk and share prices often can swing up and down before, during and after the drilling event.

Our plan is to hold the majority of the position into the drill results (in case L1M can deliver a “Latin Resources style” result), if the drill results are excellent or the price runs in the lead up to drilling we may Top Slice 20% of the position in line with our trading policies which you can read here.

If the drill results do not deliver, we are happy with the cap structure and back the management team to further test the West Australian assets or acquire a new project.

Disclosure: Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 6,360,712 L1M Shares, 3,180,357 L1M options, and 1,400,000 Bengal Mining shares. The Company has been engaged by L1M to share our commentary on the progress of our Investment in L1M over time.

Our Investment Summary

Date of Initial Coverage

22-Apr-24

Inital Entry Price

$0.070

Returns from Initial Entry

-81%

High Point

79%