What we saw at LKY’s antimony and rare earths projects right next door to $20B MP Materials

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,945,000 LKY Shares at the time of publishing this article. The Company has been engaged by LKY to share our commentary on the progress of our Investment in LKY over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Locksley Resources (ASX:LKY) is going for speed.

USA sourced, USA made and USA processed antimony.

And the ~$150M capped LKY is seeking to become the first to do it.

Antimony is a critical mineral used by the defence industry, and there are no domestic sources of antimony within the USA... yet.

The US “Department of War” invested heavily into the $2.5B capped Perpetua Resources Stibine project in Idaho for its antimony, but that mine won’t come online at least until 2029.

While Perpetua is building a large scale operation, LKY wants to be first to market with a smaller scale operation.

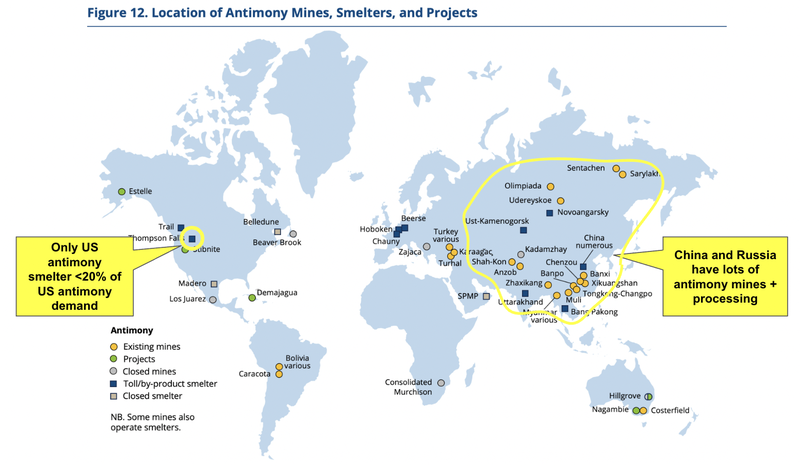

China banned antimony exports in September last year (the US gets 65% of its antimony from China), and so the US is scrambling for more supply... quickly.

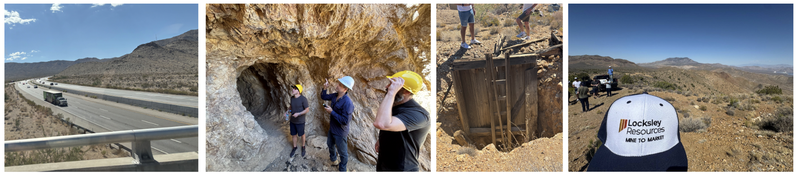

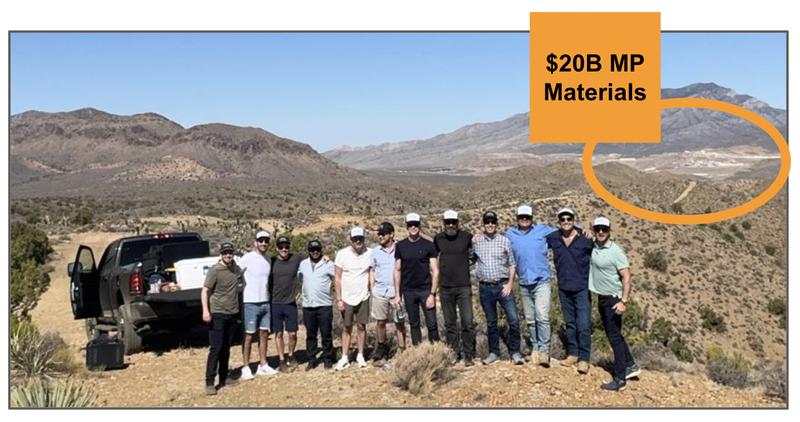

We just went to visit LKY’s site with a group of analysts and investors...

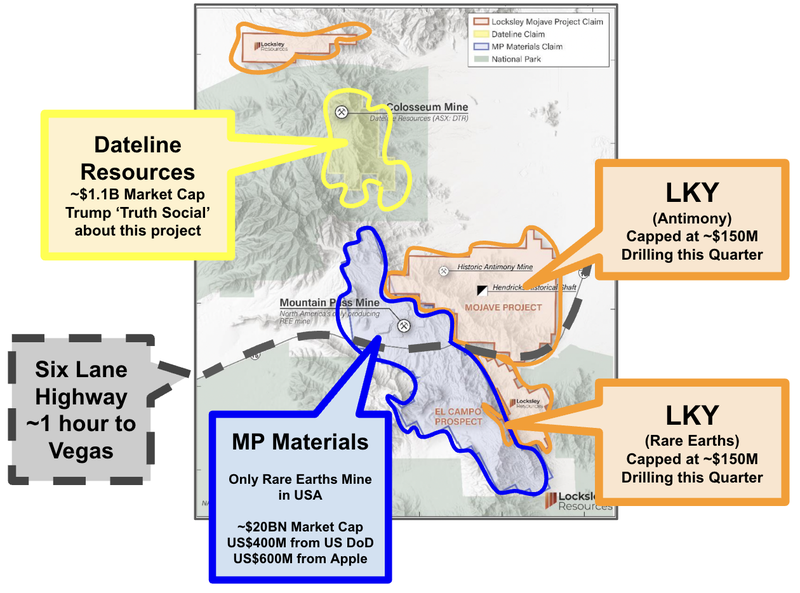

LKY’s project is right next door to another ‘US champion’ of critical minerals - the only rare earths mine in America owned by the $20BN capped MP Materials:

Here is a photo of the group with the MP Materials rare earths magnet facility and mine in the background:

This image did get memed again...

... thanks internet.

Whatever gets more eyes on the LKY story is fine with us (especially in the US).

Right now the US government is “moving at warp speed” (their own words) to build up critical minerals supply chains in America.

A lot of money has been made available to companies (like LKY) to support this agenda.

In order to put itself in the best position for funding LKY has:

- Engaged GreenMet and Drew Horn to lobby on LKY’s behalf - Drew worked in the Defence and Energy departments during Donald Trump’s first term and, after the 2020 election, founded GreenMet.

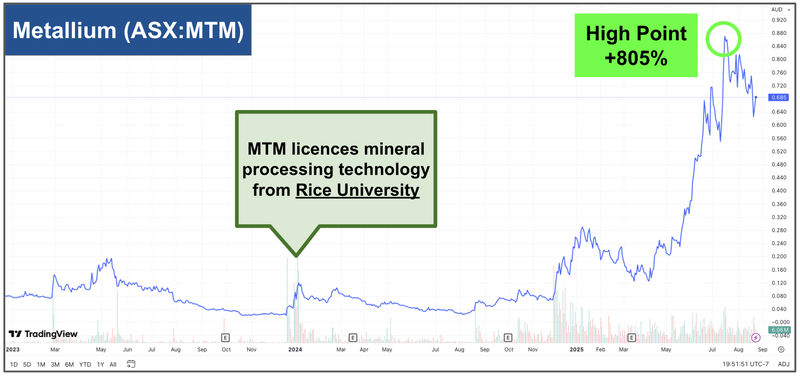

- Engaged Rice University to develop a downstream antimony processing - Some of the best technologies on the ASX have come out of Rice University including ~$600M capped Weebit Nano (ASX: WBT) ReRAM semiconductor technology and ~$400M capped Metallium (ASX: MTM) Flash Joule Heating technology.

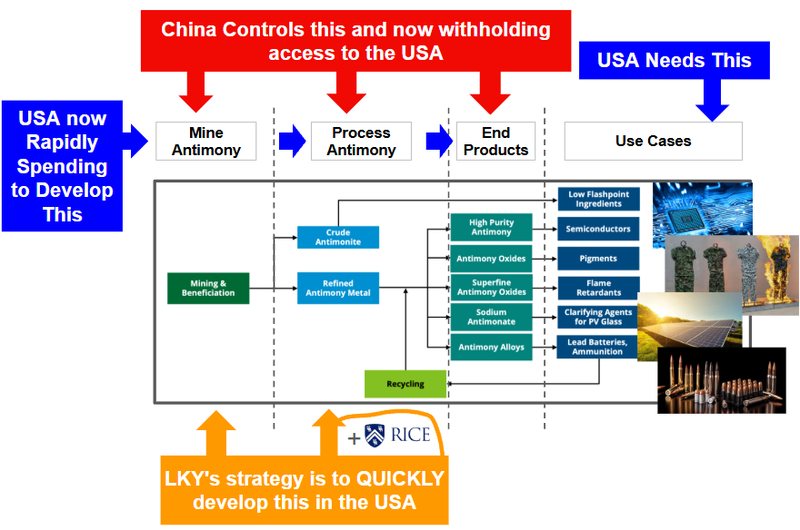

Here is LKY’s downstream strategy...

UPDATE: Today, LKY announced that it has done the first metwork testing on its antimony ore proving 82.9% - 85.9% recoveries to antimony concentrate (source).

LKY will send this concentrate to Rice University to commence testing of its Deep Eutectic Solvent processing technology.

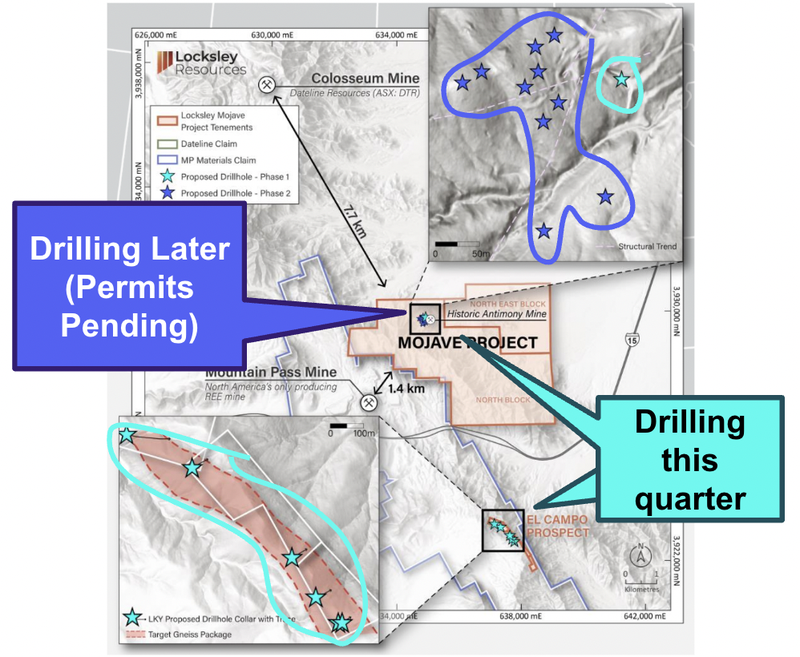

Over the next quarter LKY will be conducting its first drill program over the project, the goal of this program is to:

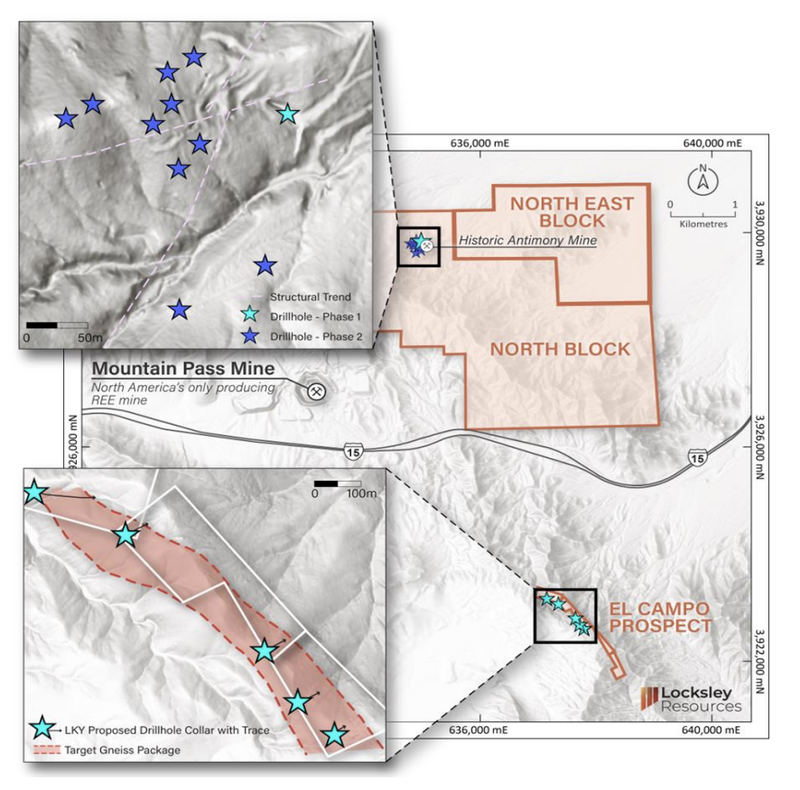

- Identify rare earths at the El Campo prospect along strike from MP Material’s rare earths mine (5 holes)

- Evaluate the antimony potential at the Mojave Project where there was an old antimony mine and smelter that operated in the 1930s (3 holes)

LKY will also look to extend drilling at the Mojave Project with permits currently pending:

We saw the location of the drill holes as well as the old antimony operations that were active during WWI and WWII.

Here is our analyst's first hand account of the visit to LKY’s rare earths and antimony project.

What we learned from visiting LKY’s antimony and rare earths project...

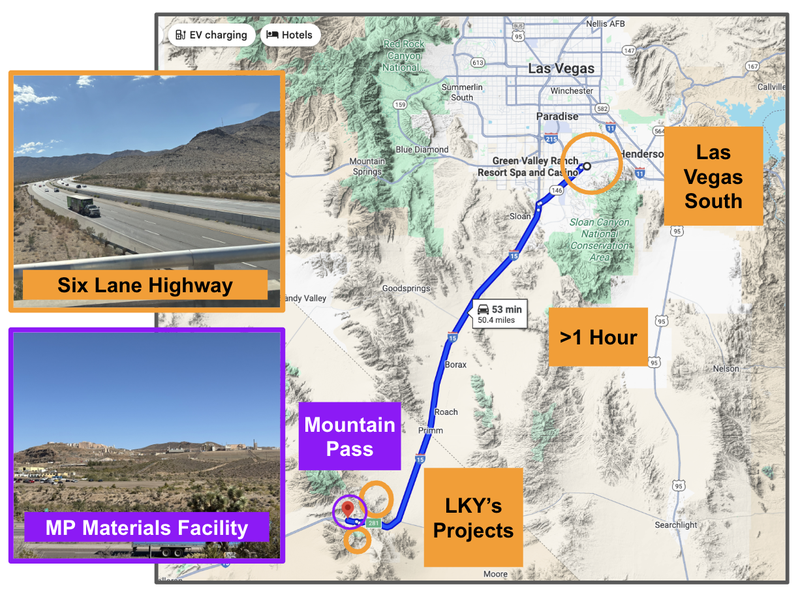

It was a short ~45 minute drive from one of Las Vegas South’s finest establishments, the Green Valley Ranch Resort Spa & Casino, to LKY’s project:

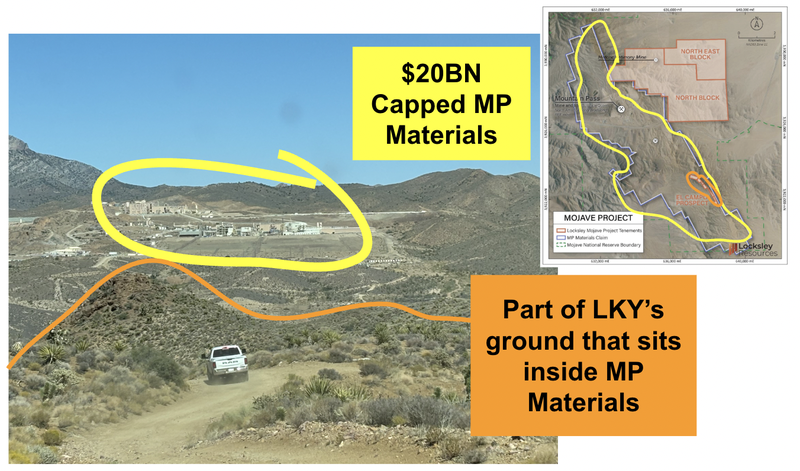

LKY has ground right next door to the $20BN MP Materials Mountain Pass Rare Earths Mine & Processing Facility.

LKY’s projects have great access to infrastructure, power, rail and a major city.

There is a six lane highway before the turnoff to LKY’s projects, and it is less than 1 hour drive from Las Vegas.

(Compared to some of the remote places in Africa and Latin America we’ve visited for site visits, this drive on a highway was paradise)

LKY has two major projects right next door to (and one even inside) the $20BN capped MP Materials ground - here’s a map again, only this time even more zoomed in:

The $1.1BN capped ASX listed Dateline Resources is also a few kilometres away from LKY.

LKY recently picked up some more ground to the north of the Dateline Resources and to the south of its Mojave Project.

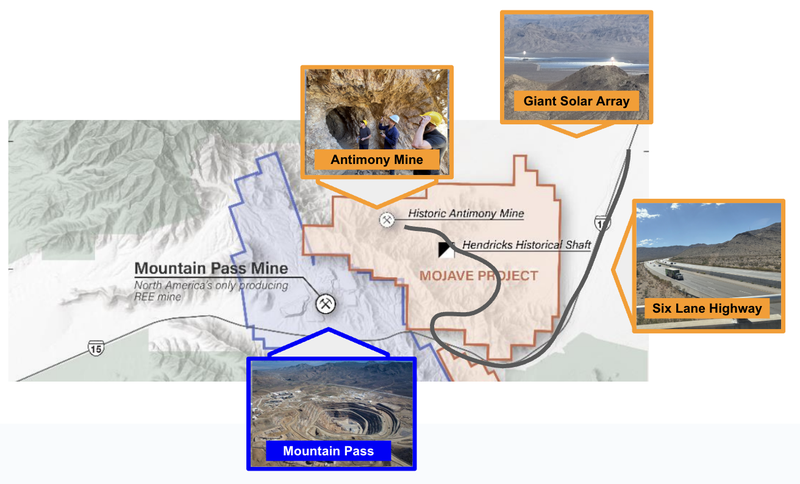

LKY’s flagship project is the Mojave Project, home to the Desert Antimony mine...

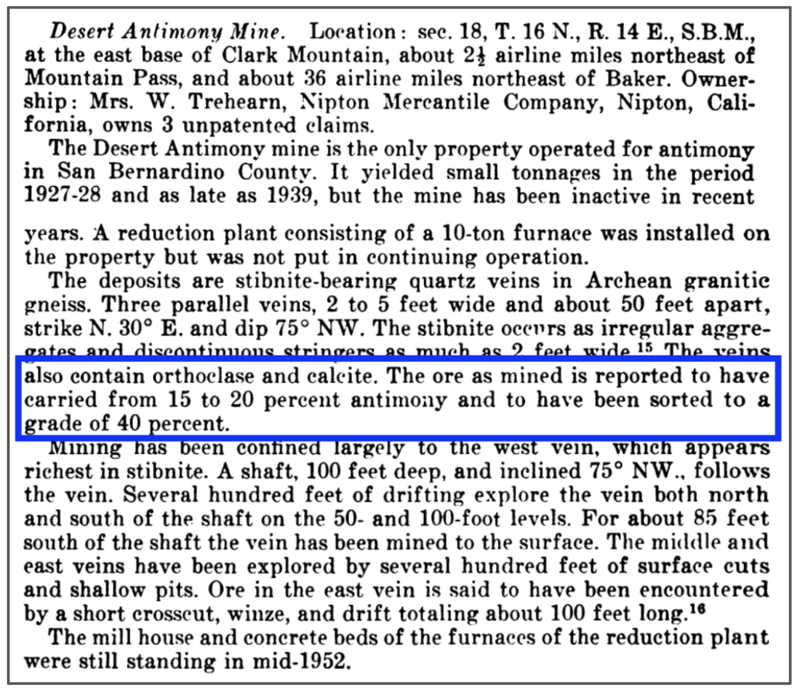

During WW1 and WW2, LKY’s Desert Antimony mine was the only producing antimony mine in the San Bernardino district of California.

We went through the old archives and found that LKY’s mine produced antimony with grades between 15 - 20% (and some as high as 40%):

(Source, California Journal of Mines & Geology 1952)

The mine was active between 1928 and 1939 and produced between 100 and 1000 tonnes of antimony.

There was an old 10 tonne furnace that we saw which was also active during this time:

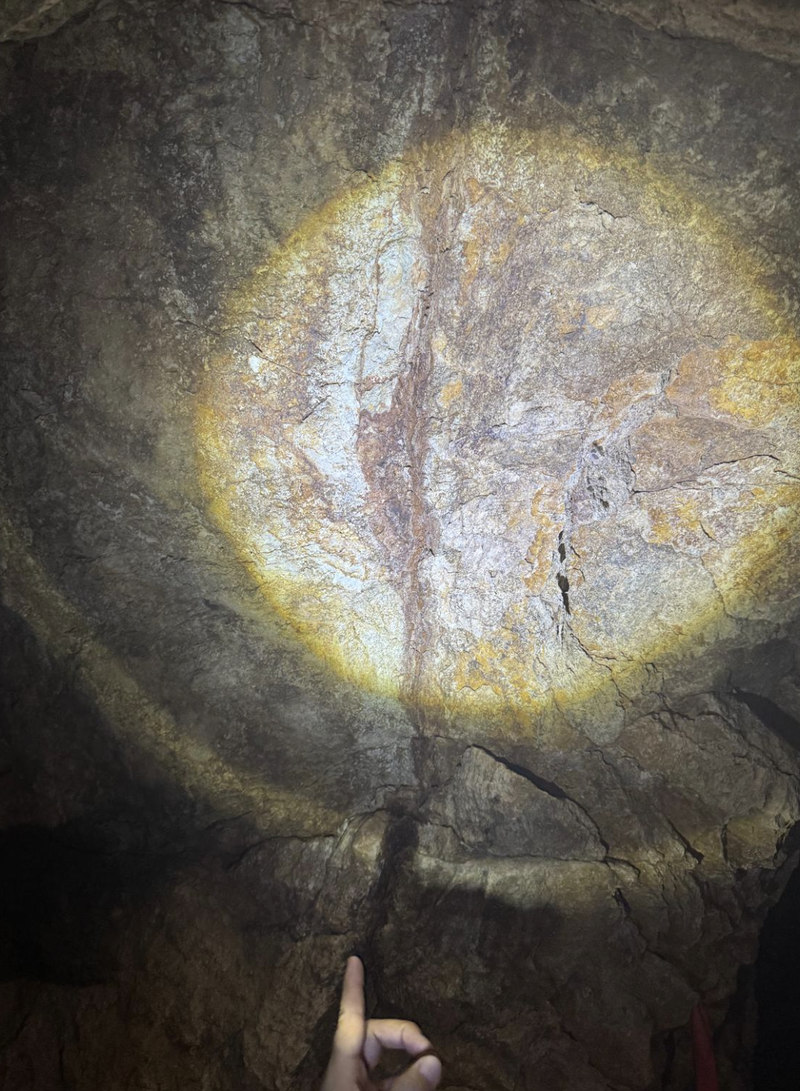

We went through a 100 foot mine shaft which follows a rich vein of high-grade antimony:

We were surprised by just how deep and detailed the mine shaft was, you can see here the vein that the old timers were chasing:

There was more exploration around the West, our equivalent to an “exploration hole” (this upper shaft was only around 10 meters deep):

LKY’s goal is to become the first producer of American made, American processed, antimony.

It is an ambitious project, and not the traditional way in which exploration and development projects are worked up.

Mine to market, with speed is key.

LKY sees the US government as its only customer, and is listening to their desires and demands to develop critical minerals in America, and quickly.

In order to advance this strategy LKY will be:

- Extending the drilling program at Desert Antimony (permits anticipated for next month)

- Aiming to secure funding from the US Department of War through its lobbyist GreenMet, led by Drew Horn, who has worked with the Trump administration before

- Develop an antimony processing technology with Rice University

There are about four years before Perpetua Resources is able to bring its giant gold-antimony mine back online.

So this is the tight window that LKY is working in to be the first to market (even with small scale production).

LKY’s Second Project, rare earths in MP Materials

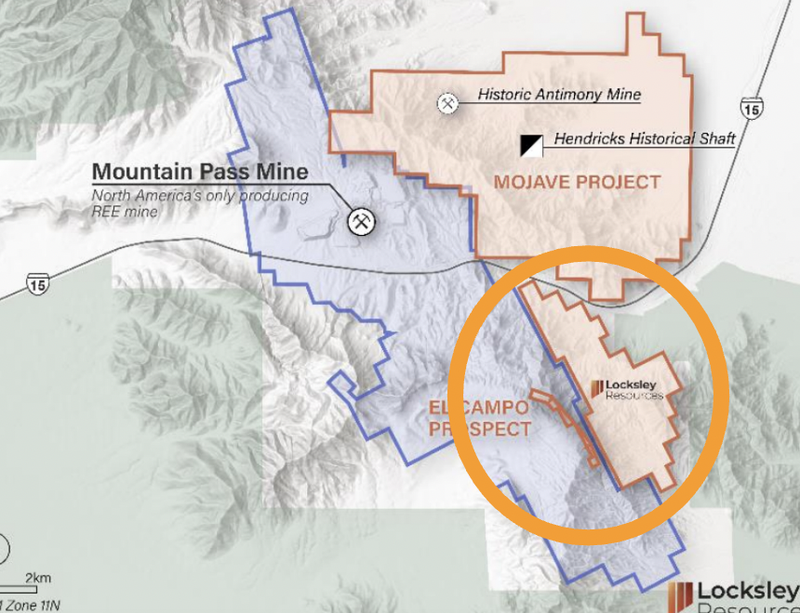

LKY’s second project is on the other side of that six lane highway, along strike from MP Materials’ Mountain Pass Mine:

MP Materials is the US national champion for rare earths, it has a US$400M investment from the US Department of War and a US$600M offtake with Apple.

MP Materials has plans to build a 10x plant facility... but the rare earths that it does have may not be enough inputs for this 10x magnet capacity (in particular MP lacks heavy rare earths - essential for permanent magnets).

The only way for MP Materials to get more rare earths later in the mine life of its current assets is to either acquire, buy or make a new discovery.

LKY’s first drill program is to explore for more rare earths in a tenement that sits within MP’s ground.

So effectively it is a ‘free option’ for MP Materials to take a look at the drilling outcome to see if there are more rare earths along strike.

If LKY finds anything interesting (and even potentially enough to build a resource), this asset could be an attractive takeover target for MP Materials looking to increase its rare earths exploration potential.

LKY’s senior geologist described how it identified the rare earths potential of the ground, by using a geiger counter to look for thorium (a pathfinder for rare earths):

LKY also recently acquired the “Southern Block” that abuts MP Materials and connects nicely with this size constrained project:

This first drill program from LKY will predominantly focus on the El Campo prospect:

We are hoping that drilling comes up trumps (especially if LKY can identify any heavy rare earths here).

Capturing the funding from the US government

LKY is navigating the extremely fast moving tailwind of US critical minerals with the goal to capture some of the funding made available.

The US is spending big.

But we think it is the projects that can deliver the speed to market will be the first in line for funding.

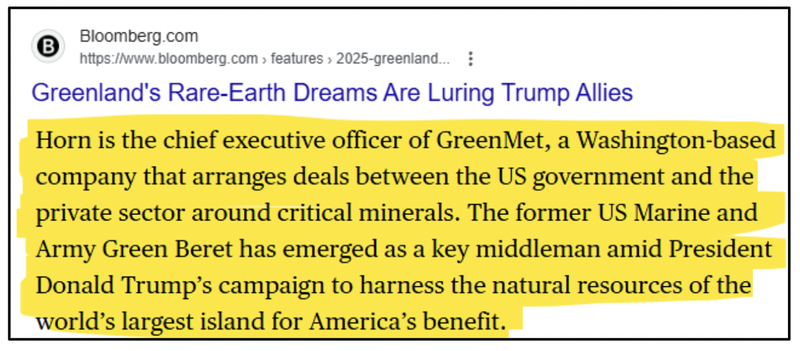

To support these efforts LKY engaged Washington DC based strategic advisory group GreenMet - led by Drew Horn.

Horn worked in the Defence and Energy departments during Donald Trump’s first term and, after the 2020 election, founded GreenMet.

According to the following Bloomberg article from August 9th, Horn’s GreenMet is a “company that arranges deals between the US government and the private sector around critical minerals”.

Read that full article here: Greenland’s Rare-Earth Dreams Are Luring Trump Allies.

LKY will be trying to capture funds from the Department Of War, Department Of Energy, the Export Import Bank and the International Development Finance Corporation.

Here is all the capital currently available from each of these organisations:

- Department of War: $7.5B in grant funding for critical-mineral supply chains under the Big Beautiful Bill (Source).

- National Defense Stockpile: $2B to purchase and hold strategic/critical minerals (Source).

- Department of Energy: $1B for battery materials processing ($500m), rare earths ($135m), byproducts ($250m), and recycling and processing ($50m+) annually (Source).

- Department of Commerce: $2B redirection of the CHIPS act funds for critical minerals projects within the US (Source).

- Defense Production Fund: $1BN available for defense-related critical minerals projects under DPA Title III (Source).

- International Development Finance Corporation (DFC): $5B proposed direct investment fund between the US Government and Orion for critical minerals projects (Source).

- EXIM (Export-Import Bank of America): Uncapped loan program for large-scale projects through its Make More in America initiative (overall lending exceeds $100B in authorised exposure across all sectors) (Source).

So there is a lot of capital floating around for companies like LKY...

We think that LKY will be an attractive proposition to get access to US government funding because it is looking to break conventional mining life cycle timelines.

Normally it takes around 17 years to get a mine from exploration into production...

LKY is looking to produce antimony (at a small scale) MUCH quicker than that.

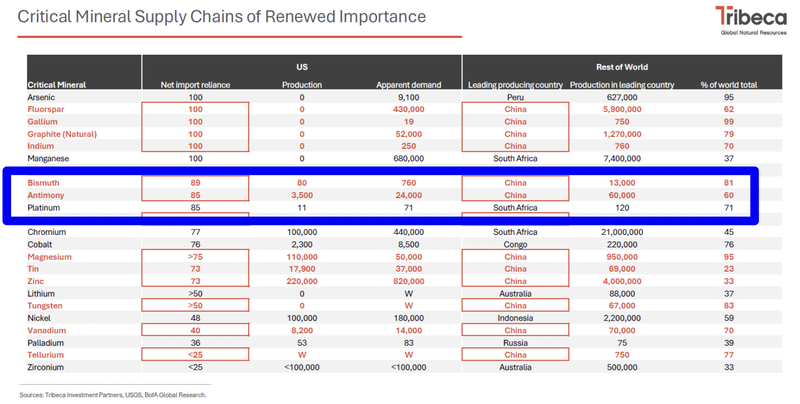

The US doesn’t need much... only around 20,500 tonnes per year according to Tribeca’s market analysis:

(Source)

So a small scale operation that could fill this urgent gap quickly, could be an attractive investment for the US Department of War.

Here are the four key reasons why we think that LKY is in a strong position for funding:

- Drew Horn has the pedigree, relationships and experience to lobby on LKY’s behalf to major US defence institutions that make capital allocation decisions.

- Location, by being next door to MP Materials and Mountain Pass, LKY can provide the government a narrative of building a “critical minerals hub” in the region.

- Historic Mine, LKY’s project has a historic antimony mine. While there is no guarantee how much un-mined antimony actually exists there, confidence can be taken from the old timers that produced ~1,000 tonnes of antimony from the project.

- Downstream Processing, by pairing LKY’s historic antimony mine with a downstream processing technology LKY can make the first ever mined and processed antimony all in America.

These are the four key pillars that LKY will be using to demonstrate to the US government that allocating it funding to progress towards its goal of being the first US antimony mine to market is a good use of public money.

LKY’s downstream strategy for antimony

Before the LKY site visit, the LKY team was in Houston to visit Rice University.

(Unfortunately we couldn't make that leg of the trip)

Here is a short video explaining the relationship between LKY and Rice University to develop an antimony processing technology.

(Source)

Rice University has been associated with some of the most successful industrial projects on the ASX in the last few years.

Rice University is the same university that developed the:

- ~$600M capped Weebit Nano (ASX: WBT) ReRAM semiconductor technology and

- ~$400M capped Metallium (ASX: MTM) Flash Joule Heating technology.

Prior to both companies’ transformative Rice University partnerships, Weebit Nano and Metallium were tiny ASX stocks.

Here is how each stock traded in the years following Rice University licencing agreements:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

And now LKY is partnering with Rice University on the development of antimony processing technology.

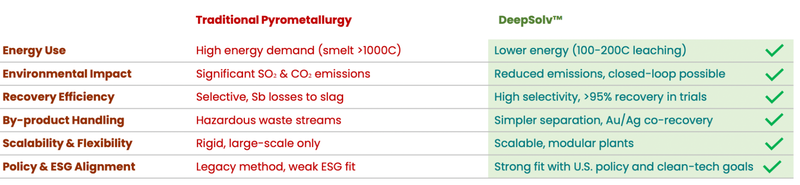

The technology that LKY is looking to develop is a Deep Solvent Technology - a low energy organic solvent technology to process minerals.

The mineral that LKY is focusing on... antimony.

LKY is already in discussions for an ore purchase agreement with EV Resources (ASX: EVR) to test this technology on its antimony ore in Mexico.

LKY will be using its own ore as well for testing.

Here is how the DES technology compares to the traditional pyromet method of processing antimony:

In terms of antimony processing, there is only ONE active antimony smelter in the US, which produces around 3,500 tonnes a year of antimony.

The US demand is currently 24,000 tonnes, which means that the US is buying its process antimony from elsewhere (mainly China).

(also the antimony concentrate comes from Mexico, meaning that the US doesn’t have any fully US-based antimony mine to market projects)

(Source)

The processing of antimony is a big challenge for the US and we think a DES technology developed by LKY and Rice University could provide a scalable solution.

It’s very early days in the development of this technology though, and success is no guarantee.

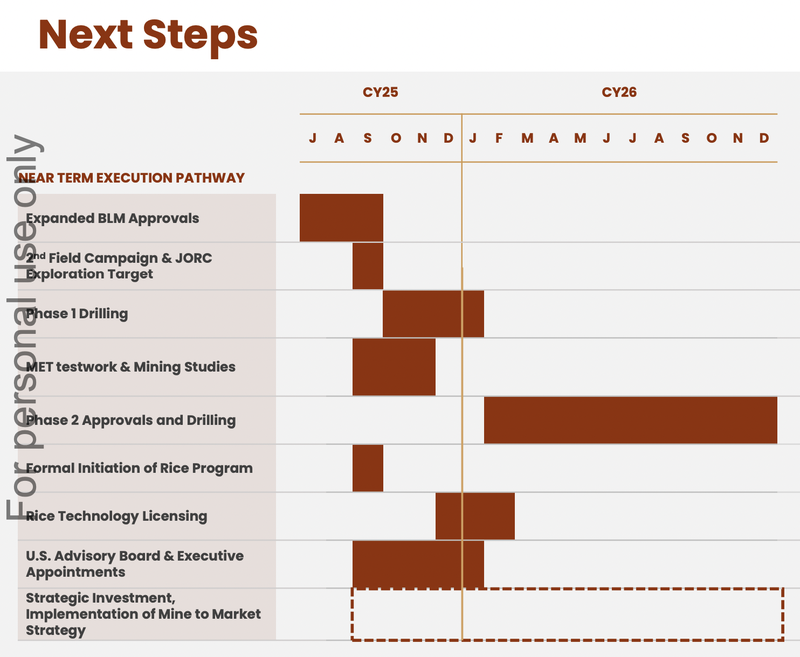

What’s next for LKY?

Drilling 🔄

LKY expects drilling to start next quarter, with first results expected before the end of this year.

Right now LKY is waiting for its expanded Plan of Operations to be approved (which is LKY expanding the size of its currently permitted drill program).

(Source)

Permitting for Phase 2 Drilling 🔄

LKY has lodged permits for an expanded Phase 2 drilling program on the North Block.

In the map below:

- Light blue stars = phase 1 drill program (fully permitted)

- Dark blue stars = phase 2 drill holes (permit pending)

Secure Licence Agreement with Rice University 🔄

Now that LKY has signed a partnership agreement with Rice University, the next stage will be to secure a larger licence deal over whatever technology is developed from the R&D agreement.

This will take some time to work out the IP sharing and mutual development of the technology.

What are the risks?

LKY hasn’t started drilling yet so the main risk here is “exploration risk”.

It is possible that LKY finds nothing worth following up on the upcoming exploration programs.

There is no guarantee that LKY’s upcoming drill programs are successful. LKY may fail to find economic deposits of rare earths or antimony in which case we would expect the share price to re-rate lower.

LKY just lodged an “expanded plan of operations” to increase the size of its already permitted drill program, so permitting risk is material as well.

There is no guarantee that this expanded program is approved.

Finally, LKY’s strategy is to seek government funding and financial support for its project, there is no guarantee that this eventuates.

For the full set of risks we have identified and accepted in making our Investment in LKY, see our LKY Investment Memo below.

Other Risks

The company's primary asset is a pre-discovery antimony and rare earth elements exploration project in California, and it is possible that LKY makes no economic discovery despite the proximity to the producing Mountain Pass mine.

LKY is highly sensitive to fluctuations in antimony and rare earth element prices.

While current geopolitical tensions have supported these prices, any easing of US-China trade restrictions or alternative supply sources could materially impact the project's economic viability and the market’s interest in exploring the project.

While LKY does have current drilling approvals in place, there is no guarantee the expanded plan of operations the company recently submitted is approved. There is also no guarantee of timely regulatory approvals which could mean delays for the planned drilling program.

Finally, despite high-grade surface samples (up to 12.1% TREO and 46% antimony), these results may not be representative of broader mineralisation at depth, and the company has yet to conduct any drilling to verify continuity.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our LKY Investment Memo

You can read our LKY Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our LKY Investment Memo covers:

- What does LKY do?

- The macro theme for LKY

- Our LKY Big Bet

- What we want to see LKY achieve

- Why we are Invested in LKY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.