What is safe from AI... At least for now anyway

Published 07-MAR-2026 14:59 P.M.

|

16 minute read

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

Any forward-looking statements are uncertain and not a guaranteed outcome.

Last Saturday we wrote about the sudden “AI is gonna take everyone's jobs” narrative we were aggressively being fed by social media.

Then 30 minutes after we hit send on our commentary, the USA and Israel started bombing Iran.

And Iran started bombing pretty much every country in the Gulf.

As if AI taking all our jobs wasn't bad enough...

Now we have potential World War 3 simmering.

Pretty sure I also saw “US government confirms that aliens exist” nonchalantly pass across the Bloomberg moving news ticker this week. Let's leave that one for another time...

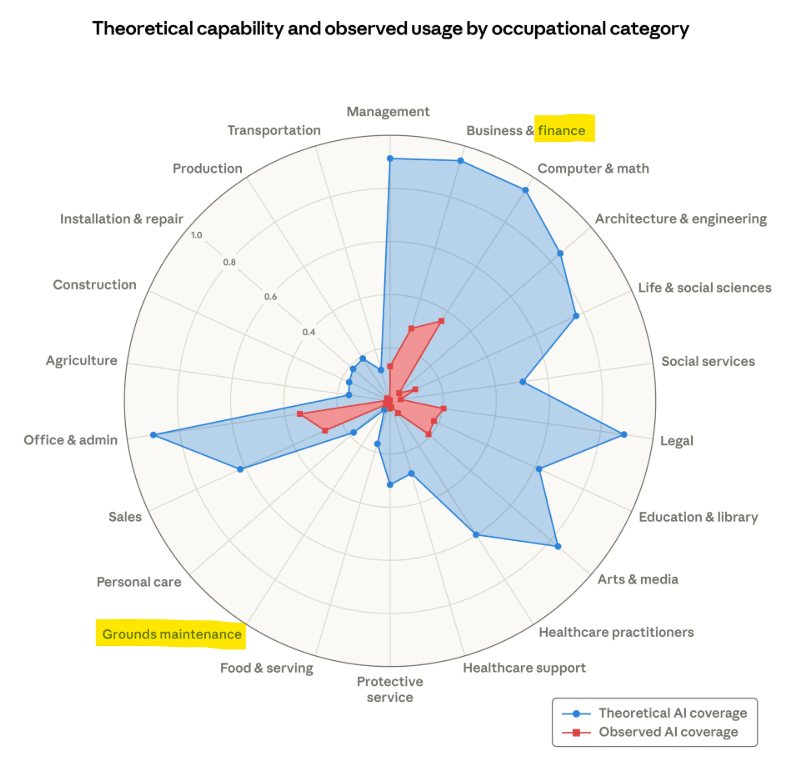

The image below was doing the rounds over the last couple of days.

It shows which industries are CURRENTLY losing the most jobs to AI (red) and which industries are FORECAST to lose the most jobs to AI (blue):

(source)

Once you’ve finished scanning this Russian roulette wheel of horror to find out how in danger your industry's jobs are from being replaced by AI, it becomes clear that there are some industries that are less affected than others.

(ironically, this data was collated and image generated by... AI)

Finance and business jobs are one of the MOST affected by AI (well that sucks for us then).

“Grounds maintenance” (gardening?) jobs look to be the LEAST affected by AI...

“Hey ChatGPT, mow my lawn and plant this tree” - nope, I can’t do that.

So is it time to put down that ASX microcap pitchdeck and keyboard...

and pick up a trowel?

Yesterday after market close, I decided to take a break from trying to set up my instance of agentic AI assistant OpenClaw (why am I trying to take my own job?).

Instead I decided to dust off my long unused gardening skills to prepare to safeguard my future earning capacity in anticipation of AI replacing my finance and writing job (right?).

Next stop was Bunnings... to buy a plant and a trowel.

”Babe, quick, come to Bunnings with me and take a photo of me buying this plant, I’ll explain in the car”

Back at home, as I was carefully inserting my new plant into a small hole I had just dug, and contemplating how moving earth and soil around appears to be humanity's last stronghold of usefulness against AI... (if social media is to be believed)

I arrived at a fairly obvious insight.

So AI struggles the most in moving earth and soil around...

Moving earth and soil, like in... mining and resource exploration.

That one seems obvious.

AI also can’t raise money to drill an exploration hole yet.

AI can’t negotiate a deal with a resource exploration project owner to list on the ASX.

OR engage with local communities.

So mining, mine development and resource exploration should be safe for now.

AI also can’t make an oil & gas discovery, mine uranium, build a solar array or a nuclear power plant.

So AI NEEDS mined minerals for its semiconductors and the data centres that house it, plus the energy to power it and infrastructure to transport this energy.

Well, well, well, so checkmate (for now) AI...

If you want the minerals, metals and energy for us to finish building you so you can take all our jobs, the small cap resource sector should still thrive.

So to try and delay participating in the dystopian future of universal basic income and every human spending all their time watching Netflix and banging their worn out VR sexbots...

We are going to stick to investing in early stage resource stocks for now.

(and writing about it)

Ironically, probably the same resource stocks that are contributing to building and powering the same AI’s that social media reckons will eventually take our jobs, right?

Leaving us with gardening...

Well, until the AI robots arrive, that is...

and can start doing physical stuff that current AI by itself can’t do yet...

And the new AI powered garden-master 3000 autonomous trowel-bot will finally extinguish the last bit of usefulness humanity can offer.

Here what it might look like (fake AI generated video from the internet):

p span[style*="font-size"] { line-height: 1.6; } p span[style*="font-size"] { line-height: 1.6; }

(Ok, fine, this is getting a bit dramatic now, just trying to illustrate a point)

At least exploration and mining stocks will be needed in the meantime to find and supply all the metals and energy needed to build and power all these AI robots.

And are endless years of “netflix and chill” (with a robot) really even that bad?

Humans will likely find something better to do with their time and energy post AI and AI robots.

AI isn't the first “technology revolution” that threatened to “take everyone's job”, created panic, changed the world and changed the way that humans work and earn income:

- Move from hunter‐gatherers to settled farming and herding

- Rise of villages, then cities, with specialised crafts and trade

- Agricultural Age: most humans working the land for subsistence.

- Industrial Revolution: factory work, machines, wage labour, urbanisation.

- Mass electrification, telegraph/telephone: coordinated, time‐disciplined office and factory work.

- Services and “white‐collar” expansion: clerks, managers, professionals.

- Knowledge/Information Age: computers, internet, knowledge workers as the core economic engine.

- Globalisation: offshoring, global supply chains, 24/7 distributed teams.

- Remote work and gig economy: flexible, project‐based, platform‐mediated.

- NOW: Automation and AI: routine tasks increasingly done by machines; humans focus on non‐routine, creative, and relational work

And humanity seemed to successfully emerge from every “job disrupting” technology leap in history so far.

Let's see if social media is right that “this time it’s different” - doubtful.

Anyway,

We have an increasingly simmering potential WW3 to survive first before we need to start worrying about AI taking jobs.

Before we get into another positive takeaway (yes there is one), let’s layer on one more doomer take onto this gloomy, hypothetical cake of despair we’ve been baking today:

If too many people lose their jobs, they won’t be able to pay their mortgages, eating into bank revenue (mortgage interest payments = bank revenue).

Banks will become unstable, house prices will go down and ... another 2008 GFC?

Meaning a lot of government money printing (again) to get through the crisis - remember zero interest rates (ZIRP)?

Banks aren’t the only entities who rely on people having jobs for their revenue.

Anyone who loses their job also won’t be paying income tax...

The US government makes about 50% of its revenue from income tax.

And with a growing ~$38 trillion government debt to service, big reductions in government revenue impact the ability to service that debt.

If government debt suddenly becomes unserviceable...

More money printing.

And now with a potential new war kicking off... wars aren’t cheap.

More money printing.

If all this does play out, it seems like printing more money is the only way to navigate these situations.

Printing money means the prices of gold and silver prices go up.

(well, technically gold and silver stay the same, it just takes more fiat currency to buy the same amount of gold and silver as currency supply increases)

The new war in Iran this week has also spiked oil prices up over 35% - now at over $90 a barrel for the first time in years.

Kinda reminds us of what we have read about the “Oil crisis of the 1970’s”

The 1970s oil crisis hit just after the US ditched Bretton Woods (when Richard Nixon announced the US Dollar will no longer be backed by gold).

Removing gold backing from the US dollar lit an inflation fire.

Then in 1973, the Yom Kippur War triggered the Arab oil embargo, crude prices quadrupled (is that what could be starting now?), and Western economies were smashed by stagflation and energy shortages.

Then the late‐70s brought the Iranian Revolution (here we go...), supply disruptions, and rising Cold War tension (including Afghanistan), reinforcing the sense that fiat and geopolitics were spinning out of control.

And during these years, capital fled “paper” money into hard money.

Gold ran from $35 to $850 by 1980, silver from about $1.50 to nearly $50, and gold–silver/oil ratios screamed that real assets were the only refuge.

Gold (1970 to 1982 highlighted):

(source)

Silver (1970 to 1982 highlighted):

(source)

Gold and silver stocks delivered true mania‐level returns (yes please), with major gold indices doing 10x‐plus over the decade while the broader market mostly churned.

(past performance is not an indicator of future performance)

But it was a brutal ride: mid‐70s and post‐1980 rate shock periods saw gold and silver smashed 40–60% and miners down 60–70% as US Fed chair Paul Volcker restored real yields and the inflation war finally turned. (always a wild ride)

So it’s not the first time we have seen this kind of setup before...

and the people who lived through it (before we were born) seemed to get through it ok.

Here’s another positive take:

This isn’t the first “the world as we know it is ending right now” crisis we have lived through in our lifetime...

And won’t be the last.

Remember Y2K? (computers can't handle the date switching from 1999 to 2000 - banks will crash, the stock exchange will break down and nukes will launch at midnight on NYE 1999...)

Then we had the dot com crash, 911, the global financial crisis, Iraq war (I and II), Afghanistan war, COVID, Zika, mad cow disease and monkeypox.

Events not in our lifetime include the Great Depression, WW1, WW2 and Chernobyl.

Going back even further, the Black Plague in London in the 1600’s

And even further back to whatever natural or man-made disasters belted the cavemen, that were never recorded and we don’t even know about.

All these disasters came, everyone freaked out for a while, then they eventually went away...

And humanity (bruised but still kicking) kept on rolling.

They always seem a lot worse than they are at the time they are unfolding.

So while this the current crisis du jour play out, our view is that the places to be Invested are:

Gold and silver (financial system instability and increased money printing from AI taking jobs, increased War)

AI metals (needed to build data centres, AI chips and energy transport)

Energy (needed to power AI)

Robot metals (needed to build the 10 billion robots forecast to be built next 10 years)

Military metals (rebuilding of militaries, equipment and ammo as world moves to war footing)

Oil & Gas (still the lifeblood of the world, which more people will realise if the price keeps going up from the new Middle East war)

We added OD6 to our Portfolio this week.

Fluorspar is a critical mineral used in semiconductor manufacturing (AI chip etching), lithium battery electrolytes, nuclear reactors, and defence electronics.

The US is 100% import reliant on fluorspar.

Fluorspar is also a mineral that the US Department of War is looking for - awarding an initial US$168.9M supply contract to a small, US based, pre-production fluorspar company to begin securing its own domestic fluorspar supply. (source)

OD6 acquired an asset in the US which has previous fluorspar production history.

It's the only ASX listed company we could find with a US fluorspar asset.

The ASX’s biggest pure fluorspar play, Tivan, is capped at nearly $1BN and it looks like it’s being positioned to supply fluorspar into Asia.

(Tivan’s big JV partner is Japanese).

We are Invested in OD6 to hopefully see it become the Tivan for the US...

Speaking of metals you’ve probably never heard of...

Urgency for domestic production of niche critical minerals in the US increased this week

On March 1st, one day before the Iran strikes, the Pentagon sent a formal solicitation to 1,500+ companies requesting proposals to mine, process, or recycle 13 specific critical minerals.

Supposedly, the contract values on offer are between $100M to $500M+ per project and all proposals are due March 20th.

That's a seriously quick turnaround...

The 13 minerals (many which China dominates supply of): Arsenic, Bismuth, Gadolinium, Germanium, Graphite, Hafnium, Nickel, Samarium, Tungsten, Vanadium, Ytterbium, Yttrium, Zirconium.

(how many of those have you ever heard of?)

(source)

No surprise seeing tungsten on that list - tungsten is used in munitions (bullets), vehicles, body armour and missiles.

All things that are probably front of mind for the US right now.

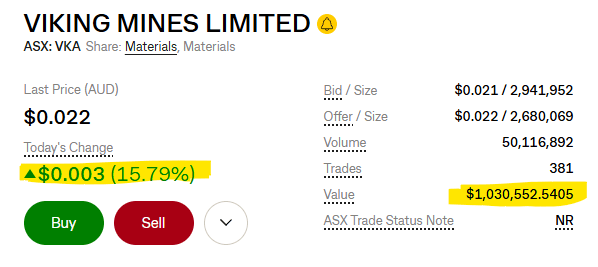

It feels like a window of opportunity has just opened up for our US tungsten Investment - Viking Mines (ASX:VKA).

VKA owns a tungsten project with historic production in Nevada, USA - where VKA is working toward building a mine restart plan around the old workings.

The market likely connected the dots on all of this - VKA was bought pretty aggressively yesterday (on an otherwise shocker of a day for the market).

The macro picture for tungsten supply is starting to get pretty dicey too...

BMO published a major research note last week saying the world has "sleepwalked" into a tungsten crunch.

(source - coverage on the report here)

China's tungsten exports have effectively fallen to zero (source) and no US or Canadian tungsten concentrate has been produced since 2016. (source)

It sort of feels like the planets are starting to align for VKA’s fast-to-market approach.

See our latest VKA note here: VKA: Ancient scrolls delivering more hits

The mineral we WERE surprised to see on the list was nickel.

Nickel rarely gets thrown into the critical minerals/defence minerals debate.

But nickel is used in autonomous AI robots plus military applications including jet engines/planes, naval ships, weapons and armour.

Okay, so I guess we shouldn’t have been that surprised.

It makes sense for the Pentagon to be looking for supply secretly - especially given Indonesia’s move to cut exports (they are the world’s biggest exporters at the moment):

Again, it feels like things are aligning for another one of our Investments - Nico Resources (ASX:NC1).

NC1 owns 100% of one of the largest, highest grade, undeveloped nickel projects on the planet.

See our latest NC1 note here: A 71% production cut at the world's biggest nickel mine - NC1 owns one of the biggest undeveloped nickel projects globally...

And finally, a reminder - the Pentagon was soliciting companies to mine, process, or RECYCLE these 13 critical minerals.

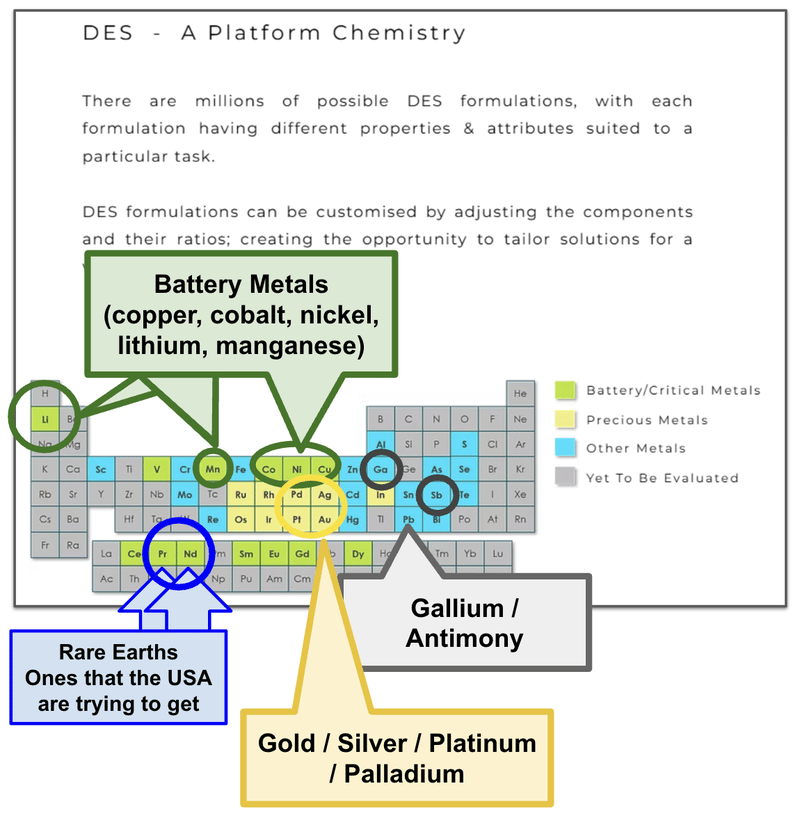

We are also Invested in IonDrive (ASX:ION) which is currently building a pilot plant for recovering nickel (amongst other battery metals) from black mass (battery waste material).

ION’s tech is also based on environmentally friendly Deep Eutectic Solvents that are biodegradable.

So maybe ION comes into play at some point here too.

Who knows what else ION’s tech can be applied to and which of those 13 minerals it could recover...

(source)

Note: this chart shows metals amenable to Deep Eutectic Solvent chemistry in general, and have not necessarily been specifically tested by ION.

Check out our latest ION note here: ION: Our Critical Minerals Recycling Stock - Targeting First Revenues in the next 24 months

What about Oil and Gas?

Given everything happening in the Middle East right now, it was always going to be hard not to write about energy this weekend.

What’s happening in the Middle East has closed the chokepoint through which ~25% of the world's oil flows and 20% of the world’s seaborne Liquefied Natural Gas (LNG). (source)

Look at how traffic in the strait changed over the course of a week:

(source)

Then there are the reports of oil and gas infrastructure being hit by Iranian drone strikes.

In response to the volatile situation, QatarEnergy suspended LNG loadings this week and some of the world’s biggest gas fields are now sitting idle.

Unable (and unwilling) to ship product anywhere.

Which tells us things could get a lot worse before we see any normalcy come back into the market.

(source)

(source)

Oil prices are up 35%, and European natural gas prices are up 80%.

Clearly, Europe will be one of the most exposed Western continents to what’s going on.

No access to oil and gas from Russia, and now halted supply from the Middle East.

To make matters worse, on December 3rd, the EU Commission signed a deal to “ensure a gradual but permanent end” to Russian gas imports.

The targets?

LNG imports phased out by 31 December 2026 and pipeline gas by 30 September 2027.

(source)

So the EU had already made a commitment to increasing reliance on LNG out of the Middle East and the USA.

We watched the following video from Peter Zeihan, where he talked about how those shutdowns in Qatar have basically locked into place a 1-month lag in bringing those fields back online.

He also says:

“The Europeans are trying to quit Russian natural gas and so to have 1/5th of the total, not just off for a day or two, but for at least a month, is kind of a big deal”.

That 1/5th Zeihan refers to is 1/5th of global Liquefied Natural Gas (LNG) output...

(source)

No one knows what's going to happen here, but we think that a whole new macro thematic could start to emerge from all of this.

The idea of “energy” being the original “critical mineral”.

(and maybe a critical minerals style push to protect/build up more domestic supply all over the world?)

The Chinese have already made their move - telling refiners to stop exports of refined products... (source)

Even in Australia, there was a video of the Minister for Resources changing tune and now talking about how the gas industry is important (genuinely surprised we saw that happen):

(source)

It's still far too early to call what might happen in energy markets, but we hold the following oil and gas Investments, which we think the market may start to look at with interest again over the coming weeks:

EXR, IVZ, 88E, CND, GGE.

Let us know if you think we should take a look at a specific energy name.

See you next week, and have a great weekend

Next Investors

Did someone forward this to you? Subscribe Here

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.