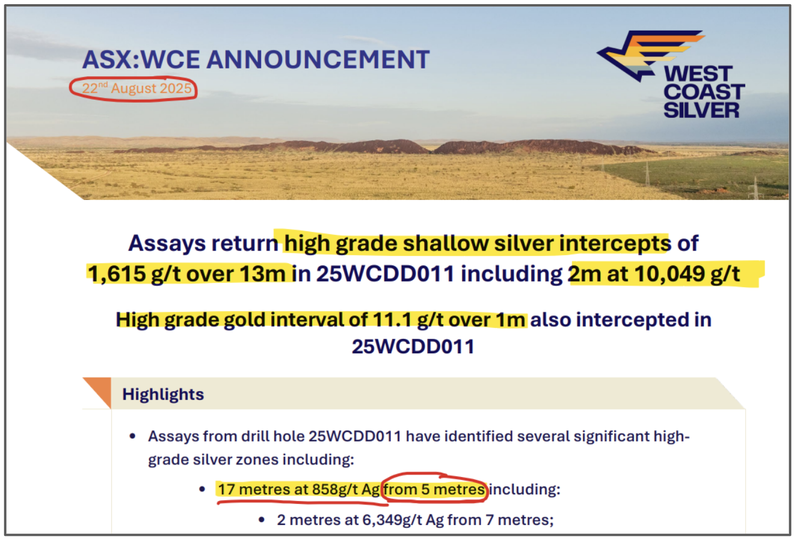

WCE hits 2m at 10,049g/t silver

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,863,000 WCE Shares at the time of publishing this article. The Company has been engaged by WCE to share our commentary on the progress of our Investment in WCE over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

High grade silver starting 5m below the surface...

West Coast Silver (ASX:WCE) just hit a 17m silver pod with average grades across that whole section at ~858g/t silver...

(Source)

And it starts ~5m below the surface - almost shallow enough to dig out with a shovel...

(ok fine, probably a bobcat - point is its very shallow so low cost and easy get to)

AND a bonus 1 metre 11.1g/t gold intercept too... we weren't expecting that.

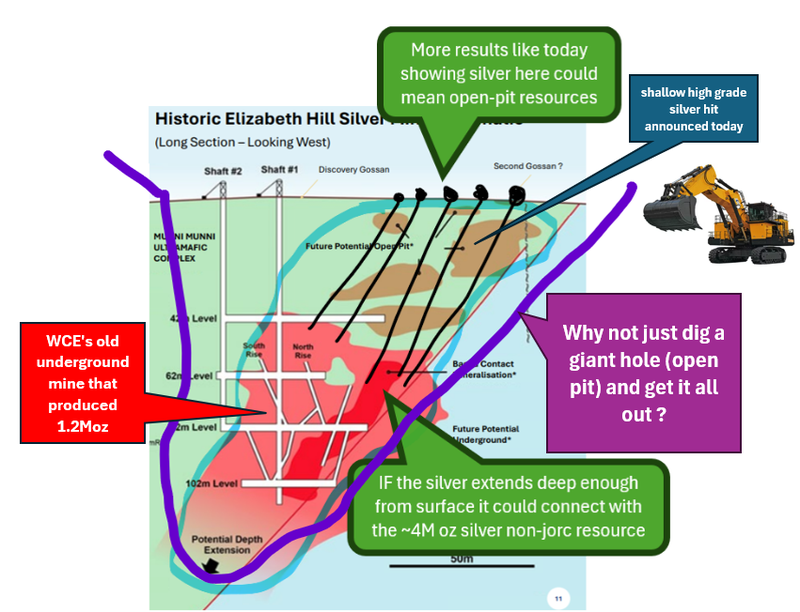

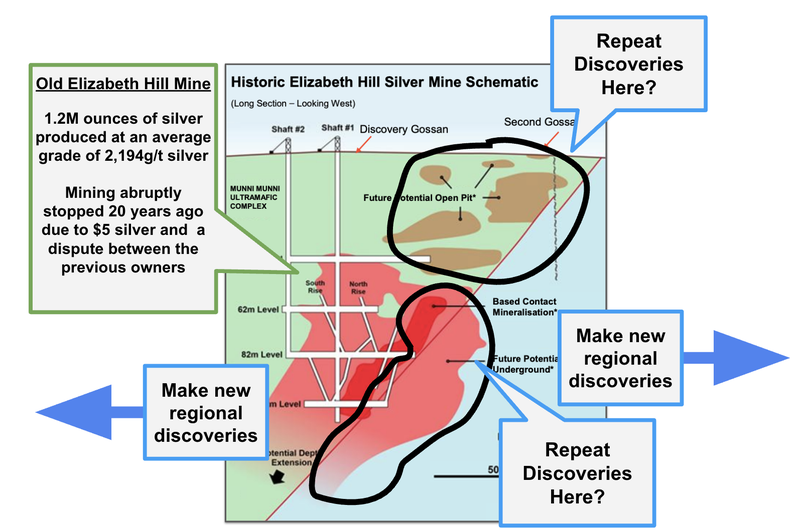

Today’s hits came just north of WCE’s Elizabeth Hill mine, which produced ~1.2M ounces of silver from (at average grades of ~2,194g/t) over a 12 month period 25 years ago.

That production run happened between 1998 and 2000 and was abruptly stopped when the owners at the time had a disagreement and silver had fallen to US$5 per ounce...

Today, a hard and fast production run like that would be worth ~US$46M (at US$38.10 per ounce).

(which is exactly what we want to see WCE do - find easy to reach high grade silver, quickly mine and sell it, into a surging silver price - we think the silver price is going a lot higher)

And remember, that previous production run was all done by underground mining methods. - which are usually more expensive but more suitable for high grade ore that is deep below the surface.

Today’s drill hits start from just 5m depths and have grades that are almost 20x the average silver grade in most silver mines around the world.

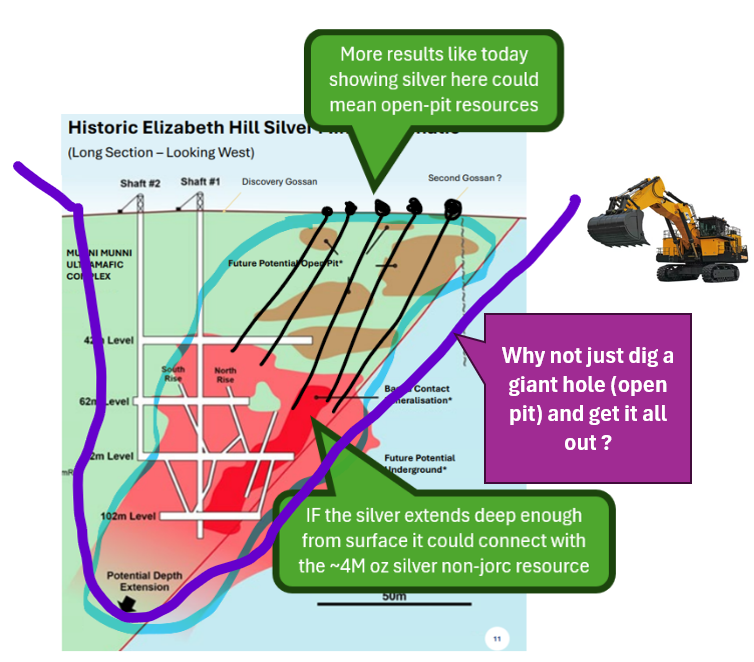

If WCE hits more shallow high grades like this they could decide to just dig a giant hole and start extracting the high grade silver (open pit mining).

The previous owners of WCE’s asset had estimated a non-JORC compliant resource estimate for the leftover remnant ore underground of ~46.8kt @ 2,700g/t silver for 4.05Moz of silver (source)

After today’s high grade shallow hit results, it’s looking like there is a chance the “old timers” (is 25 years ago really that old?) left a lot of silver untouched near surface, as well as underground...

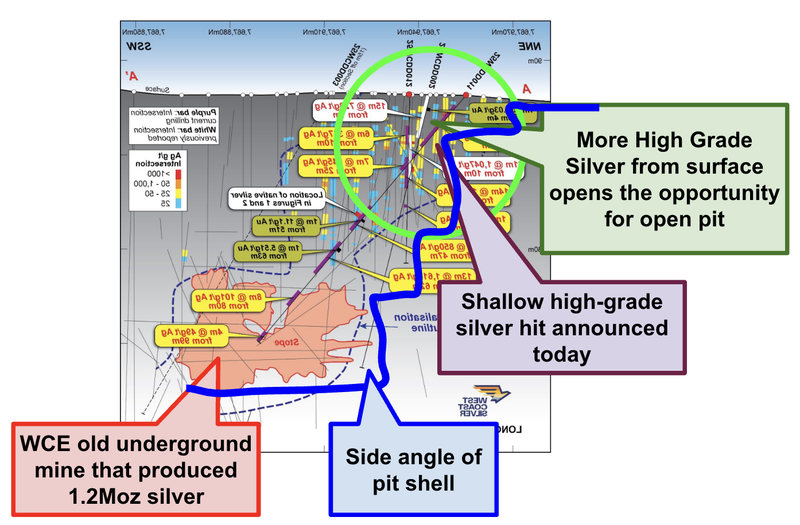

Here is how it could look on the drill intercept map (we’ve flipped the orientation to better match the perspective of the mine as shown in the above diagram):

We are obviously not pit shell engineers so this is just to illustrate the concept.

Open pit mining is cheaper than underground mining because it requires less complex infrastructure, using large-scale equipment to extract minerals directly from the surface.

Underground mining (like the previous owners did) involves costly tunneling, ventilation, and safety systems to access deeper deposits.

So seeing high grade near surface results like today’s from WCE that are above the previously mined ore body (before it was abruptly halted) is encouraging.

With 6 drill results still to come we hope to see more like today’s from WCE.

The other big takeaway from today’s announcement:

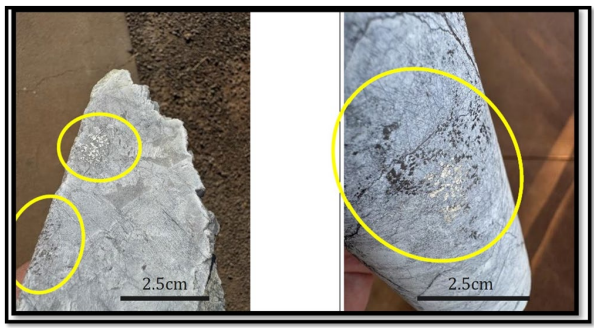

WCE is finding the same type of silver - native silver - which means the near surface stuff could potentially be processed in a similar way to how it was done at Elizabeth Hill 25 years ago.

(Source - WCE announcement 22 August 2025)

“Native” silver (visible silver nuggets) can be easily separated from the surrounding rock using a gravity circuit.

Think of it like nuggets of silver just sitting there in the rocks.

At a very high level, a gravity circuit uses a very simple processing circuit that lets the heavier gold and silver settle to the bottom and separate from the lighter rocks surrounding it.

(At least that’s how the previous producers at Elizabeth Hill did it in the late 90’s)

No need for chemicals or any other more expensive processing routes... (which means things were likely to be lower cost too).

The end result - if WCE finds enough of this type of “native” silver in those near-surface sections, it could mine and process it at relatively low costs...

(and hopefully our prediction of a generational silver price happens, which of course it may not)

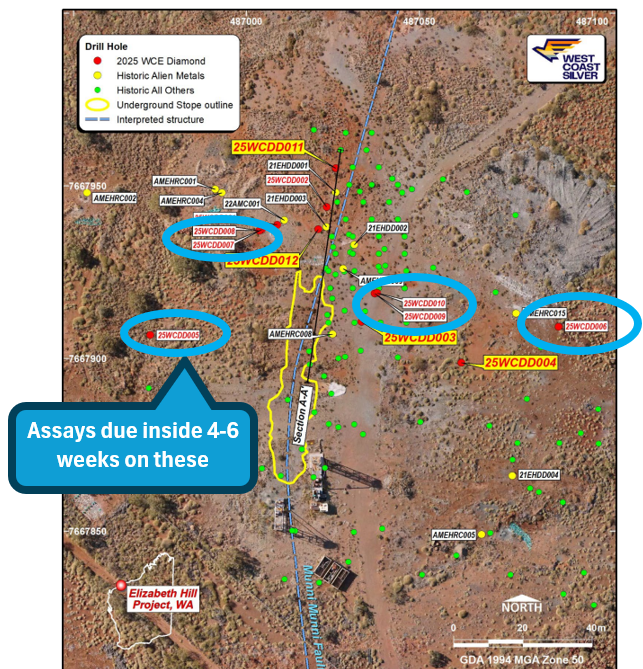

WCE still has assays pending on ~6 more holes

WCE drilled a total of 12 holes and has so far reported 6 of them, with 6 more results still to come.

What we have learnt so far:

- There’s still a lot of high grade silver here that wasn’t mined out.

- There are high grades starting from surface - could potentially connect up with the remnant stuff leftover by the “old timers” that abruptly stopped mining due to an owner bust up 25 years ago and $5 silver price.

The previous owners of WCE’s project (Alien Metals who are also major shareholders in WCE) had previously stated a Pre-JORC Compliant Resource estimate of 46.8kt @ 2,700g/t Ag for 4.05Moz Ag. (Source)

The next batch of results should give us a much better idea of whether or not there is more silver near surface and how far down it extends...

A good result would be if the silver near surface extends far enough to connect with the underground resource... That would change the way we can look at how the silver here could be mined.

Here are the holes where results are pending from:

(Source - WCE announcement 22 August 2025)

Ultimately, we think the major re-rate to WCE’s share price will come from either:

- WCE finding enough high grade silver near surface (with more results like today’s hit) to put together a resource near surface.

AND/OR - Finding a repeat of Elizabeth Hill across one of its ~20 regional targets...

Can WCE find an Elizabeth Hill repeat?

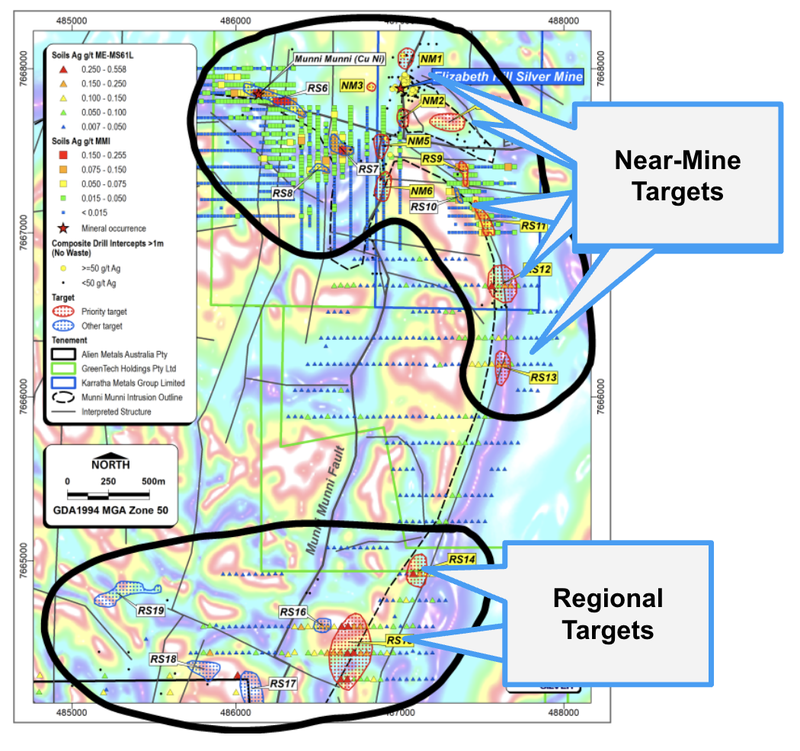

So far, all of the newsflow from WCE has been on its near mine exploration targets.

A big part of the reason we are Invested in WCE is for its regional targets too.

WCE has over 20 regional targets which have seen hardly any modern drilling.

A few weeks back WCE ranked ~12 high priority and 8 earlier stage regional targets. These are the targets where we are hoping to see a repeat of the high grades at Elizabeth Hill.

Earlier this week WCE ranked a total of ~20 near mine targets - 12 being high priority and another 8 that are slightly earlier stage. (Source)

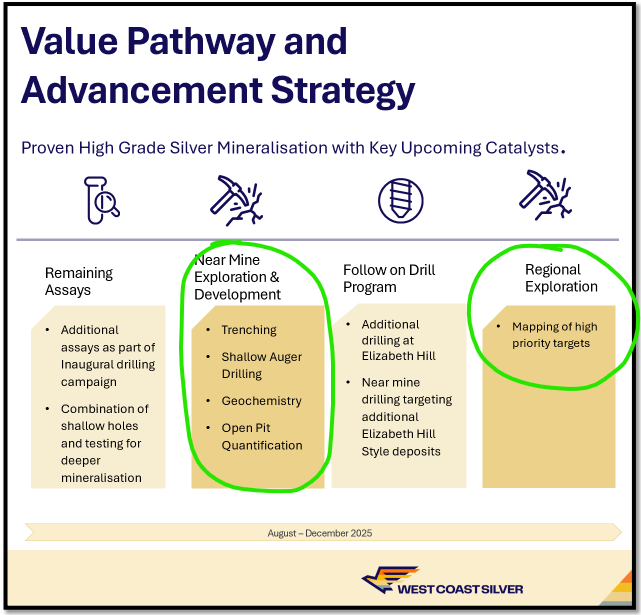

Follow up work on the highest priority targets is next:

And here is the larger regional opportunity:

Trenching and shallow auger drilling is next for the near-mine targets, and mapping across the regional targets:

(Source - WCE announcement 22 August 2025)

Ultimately we think any discovery or operation resembling the old Elizabeth Hill mine could re-rate WCE’s valuation higher from where it is today - which forms the basis for our WCE Big Bet.

(especially with silver trading where it is today at ~US$38 per ounce - remembering that the project WCE owns now was suspended when silver was at US$5 per ounce...)

Our WCE Big Bet:

“WCE re-rates to a market cap of $300M by bringing the Elizabeth Hill mine back online OR making a new discovery that is as big (if not bigger) than Elizabeth Hill into a strong macro silver theme.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our WCE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

West Coast Silver

ASX:WCE

9 reasons why we are Invested in WCE

We only just added WCE to our Portfolio on the 8th of August, at the time we published our 9 key reasons for Investing in WCE.

Here is a quick reminder of those reasons:

- We are bullish silver - We believe silver is heading to new all-time highs. A breakout could push prices well above US$50/oz, much higher than historic averages. Two of our top four positions in our Portfolio are silver companies right now.

- WCE’s project was one of Australia’s highest-grade silver mines - WCE’s project had historic production of ~1.2M ounces of silver at average grades of ~2,194g/t silver. A typical high grade project has grades around ~100g/t silver...

- WCE’s project sits on a granted Mining Lease - this gives WCE optionality with respect to getting its project back into production. IF the silver price gets high enough, WCE can get its project into production quicker than other greenfields assets.

- Historic production had cheap, simple processing - Historic mining used simple gravity processing because the ore contained visible silver nuggets easily separated from the surrounding rock. No need for chemicals or any other complex (expensive) processing routes.

- Near mine exploration upside - WCE’s project hasn’t been systematically drilled for over 25 years. We think there is potential to make new discoveries near the old Elizabeth Hill Mine - with lookalike targets along strike.

- Already hit very high grade silver in the first few drillholes - WCE has already hit a 21m intercept with silver grades of ~1,047g/t silver (including a 1m intercept grading 15,071g/t silver). Post-results, WCE’s share price has gone from ~4c to a touch a high of 17.5c. (Remember past performance is not indicative of future performance.)

- WCE has 10 assays pending right now - WCE still has 10 assays pending from its first drill program, any strong results (similar to what came in from the first hole) into a rising silver price could be good for WCE in the short term.

- 20 regional targets ranked, exploration starting soon - There is very limited modern exploration over WCE’s regional targets. WCE just identified ~12 high priority and 8 earlier stage regional targets. These are the targets where we are hoping to see a repeat of the high grades at Elizabeth Hill. Air-core/channel sampling to start on these very soon.

- Record 145kg native silver nugget came from WCE’s mine - this is more a bonus reason really, it doesn’t drive the Investment decision but it certainly got our attention onto the project when we saw it in real life at the Perth Mint.

(Source: our photo from the Perth Mint of the largest Australian native silver nugget in existence - from WCE’s project)

What’s next for WCE?

Final batch of assays 🔄

As mentioned earlier, six assays are pending from the first 12 holes drilled near the old Elizabeth Hill mine.

WCE said in today’s announcement that those results would come in the next 4-6 weeks.

(Source - WCE announcement 22 August 2025)

Near-mine and regional exploration 🔄

After the assays are out, we want to see WCE work up the rest of its near-mine and regional targets.

We think the big re-rate for WCE could come from a repeat Elizabeth Hill being discovered.

(Source - WCE announcement 22 August 2025)

What are the risks?

In the short term the two key risks to our WCE Investment is “Exploration risk” and “Commodity Price risk”.

WCE has assays in the lab which means exploration results could drop any minute now.

Any results that are below the market's expectations could have a negative impact on WCE’s share price.

At the same time, WCE is doing pre-drill target generation work on its regional targets. WCE’s share price could have some expectations from those built into it at its current level so any bad news there could also have a negative impact on WCE’s share price.

Exploration risk

There is no guarantee that WCE’s upcoming drill programs are successful. WCE may fail to find economic deposits of silver.

Source: What could go wrong? - WCE Investment Memo 8 August 2025.

Commodity price risk is also a factor here, with the silver price having come down in the last week or so from when we first announced our Investment.

IF the silver price goes any lower, we could see sector wide selling which would naturally impact WCE too.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver prices fall, this could hurt the WCE share price.

Source: What could go wrong? - WCE Investment Memo 8 August 2025.

Other risks

Like any stock market investment, investing in WCE carries a range of risks that could affect the value of the company, some of which cannot be foreseen (this is the nature of risks).

Here we aim to identify a few more risks.

WCE’s primary project is centred on an historic silver mine, and there is no guarantee that drilling will lead to new economic discoveries or that remnant mineralisation can be extracted profitably.

WCE is highly leveraged to movements in the silver price. A sustained downturn in silver could reduce the project’s potential value and restrict the company’s ability to raise fresh capital.

As a junior explorer with a ~$60M market cap, WCE remains a speculative investment. Even with recent drilling success, the current valuation may already be factoring in future upside.

Like all small-cap explorers, WCE is reliant on capital markets to fund exploration. Any future capital raise may be done at a discount and dilute existing shareholders.

Finally, while WA is considered a safe mining jurisdiction, there are always regulatory, environmental, heritage and permitting risks which could delay or impede development.

Investors should carefully consider these risks and seek professional advice tailored to their personal circumstances before investing.

Our WCE Investment Memo

In our WCE Investment Memo, you can find the following:

- What does WCE do?

- The macro theme for WCE

- Our WCE Big Bet

- What we want to see WCE achieve

- Why we are Invested in WCE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.