VKA: First drilling at USA tungsten project in over 40 years. Tungsten price hits new all-time highs. Trumps invest in a tungsten mine.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 82,166,667 VKA Shares at the time of publishing this article. The Company has been engaged by VKA to share our commentary on the progress of our Investment in VKA over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

The state of play for tungsten in the US is still critical.

In fact, it's building up to a pretty big change on the 1st of January 2027...

Tungsten is a critical military mineral used in fighter jets, ammunition, including Tomahawk, Patriot and Precision Strike missiles.

China controls ~85% of global supply.

The USA has zero domestically mined tungsten production.

On the 1st of January 2027, new US Defence Federal Acquisition Regulation kicks in - banning the Pentagon from buying:

“tungsten metal powders, tungsten heavy alloys, or any finished component containing tungsten heavy alloy if any step of the supply chain (mining, refining, separation, melting, fabrication) happened in China, Russia, Iran or North Korea”. (source)

(Combined, those four countries mentioned produce around 90% of the world's tungsten)

So in just over seven months, 90% of the Pentagon's tungsten supply chain effectively becomes “illegal”.

US tungsten prices are already responding - up from ~US$600 per tonne to US$3,000 per tonne. (source)

The US government doesn’t really have many places to go to bring on domestic supply either.

The only company within the US that received Department of Defence funding is $900M Golden Metal Resources which also owns a tungsten project in Nevada.

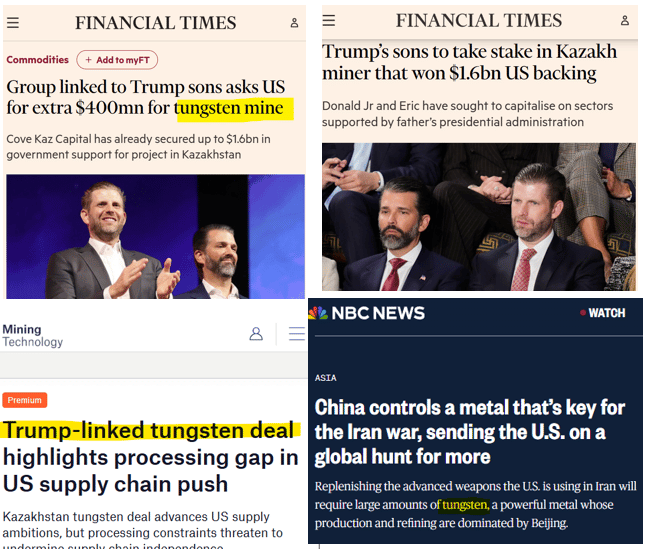

The US is so desperate to secure its tungsten supply chain it has supported a US$1.1BN tungsten mine being developed in the former Soviet nation of Kazakhstan.

A couple of weeks ago it was reported that US President Donald Trump's sons Don Jr and Eric invested in this same company:

(source)(source)(source)(source)

We think that any company that can show a credible pathway to delivering a domestic tungsten supply source, and then show that its project has scale, should be in a strong position to attract US government backing.

Which is why we are Invested in Viking Mines (ASX:VKA | OTC: VKALF).

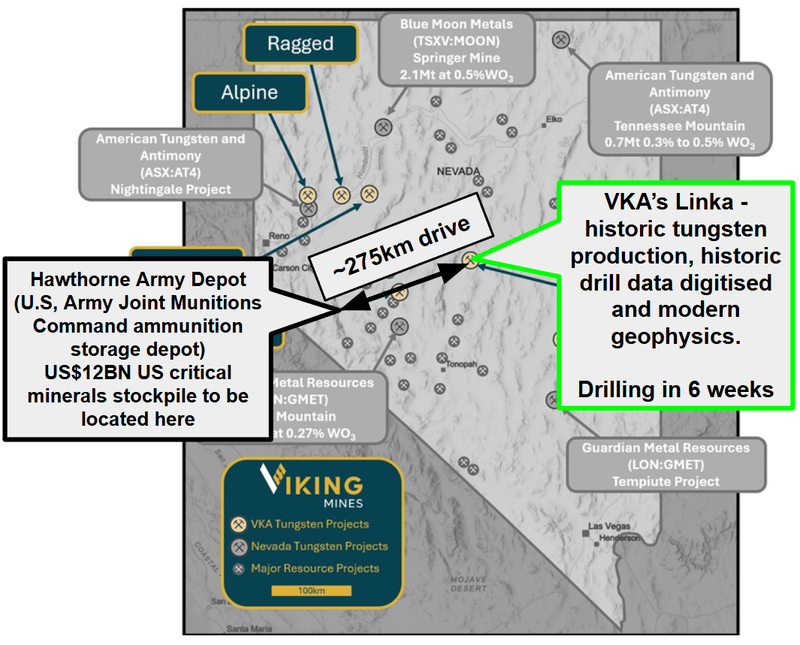

VKA’s historically producing tungsten project is in Nevada, USA - ~275km drive away from the US$12BN US critical minerals stockpile:

(source)

VKA’s project has a history of tungsten production dating back to the 1950s where ~123,000t of tungsten was produced at an average grade of ~0.54% from open-pit mining. (source)

Despite the history of production, VKA's project hasn’t been drilled in over 40 years.

And based on today’s announcement, VKA is now ~5-6 weeks away from drill testing the project.

A drill rig arrives on site in late June 2026, with drilling starting shortly after on a 63 hole RC drilling campaign.

Finally, we get to see VKA drill test the exploration model it spent the last ~6 months building.

VKA said in today’s announcement it is fully funded for the drill campaign, with $4.7M cash at March 31st, 2026.

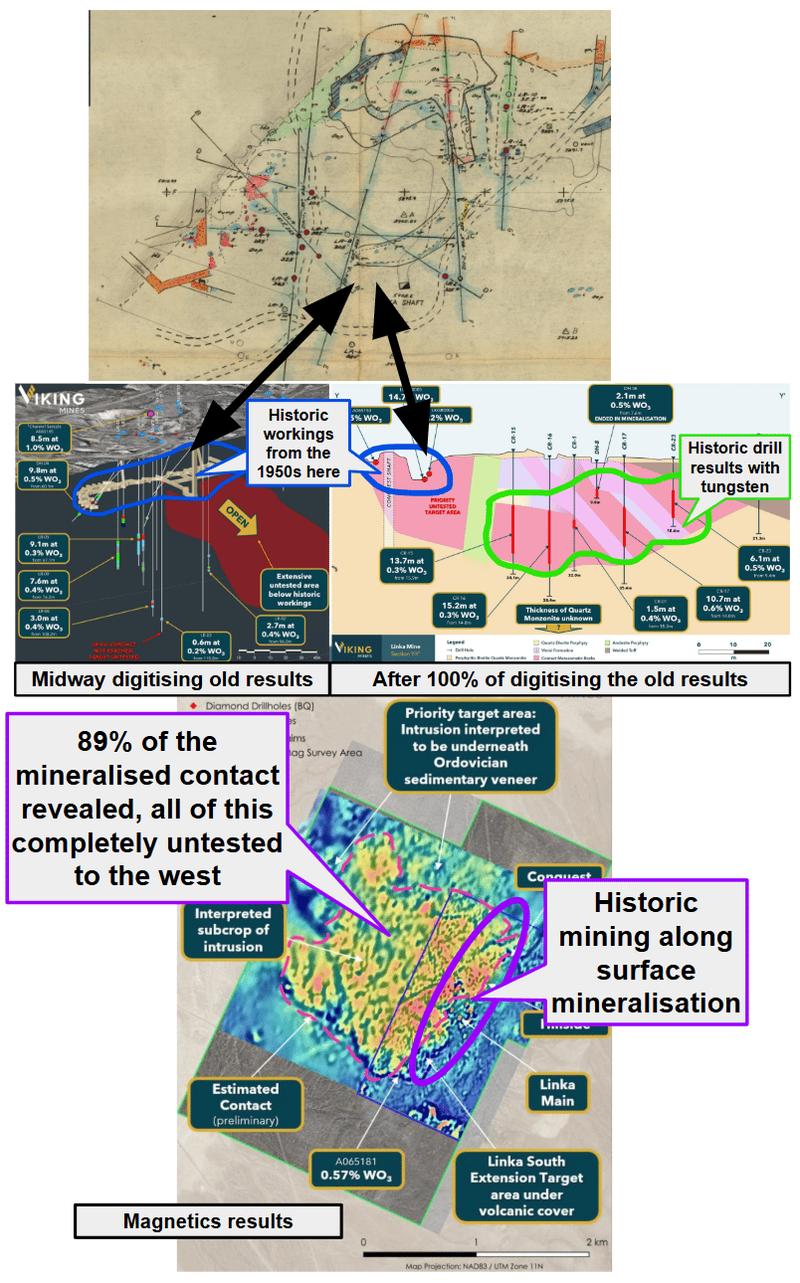

When we first Invested in VKA back in December, the project had a history of tungsten mining and just a few modern sample results.

Since then, VKA has 8x’ed the exploration upside on the project by (from ~800m of known strike to 7km strike):

- Acquiring a historical exploration database.

- Digitising the old drilling data (announcing hits like 12.2m at 1.3% and 22.9m at 0.6% tungsten).

- Digitising the projects geological model

- Doing some more sampling/mapping

- Shooting geophysical surveys

- Putting all of that data into a 3D geological model and identifying the highest priority drill targets.

VKA literally turned these old pieces of paper such as this:

(source)(source)(source)(source)

And over the next few months we get to see how much tungsten VKA’s project really has.

8x exploration upside - drilling in July.

The image below summarises VKA’s entire exploration model.

Previous tungsten mining on the project was on the edge of that big magnetic anomaly in a small portion of the project (circled on the map in orange).

VKA’s theory is that the entire edge of that magnetic anomaly could host tungsten mineralisation:

(The anomaly has a ~7km perimeter - with known tungsten mineralisation across only 800m of it so far)

With the 63 hole drill programme split across three target areas - we will definitely find out whether or not the exploration theory is validated:

Here are the three targets for the drill programme:

- Linka Main (36 holes): Resource-focused drilling to verify historic high-grade intercepts and chase the mineralisation down-dip beneath the old workings.

- Linka SW Extension (16 holes): Testing of the ~800m southwest extension.

- Regional Reconnaissance (11 holes): Shallow holes to validate magnetic and gravity geophysical interpretations - basically going for new discoveries.

The main thing we want to see from VKA is whether or not there is scale to VKA’s project AND whether or not the high grades are continuous across the project.

The old Linka mine on VKA’s ground operated at a head grade of ~0.5% tungsten.

Most operating tungsten mines globally run at 0.1–0.2%.

One of the biggest known tungsten deposits in the USA is owned by ~$900M Guardian Metals Resources.

This deposit averages ~0.206% grade, and is in the development studies stage. (source).

Back in July last year it received a US$6.2M grant from the US Department of Defense. (source)

IF VKA can even just replicate and extend what’s known at the old mine on its project we think things could get very interesting.

VKA’s project doesn’t need to be massive - for example Guardian Metals’ project is only based on a ~10mt resource.

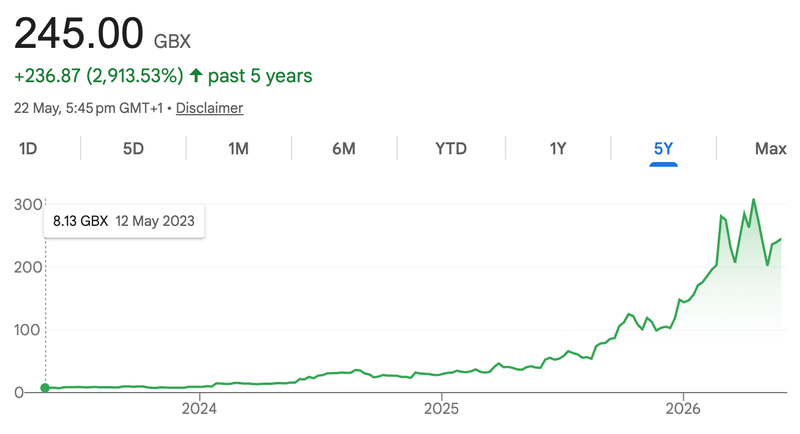

And that project alone has been enough to take Guardian Metals from a small cap listed in London to a ~A$900M market cap - up almost 3,000% in 2.5 years:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The most interesting part is that almost all of that share price appreciation was driven largely by three key drivers.

Guardian received US$6.2M from the US Department of Defence in July 2025.

Then they completed a technical study in December (incorporating drilling data from 68 old holes).

Then a US listing raising ~US$50M.

We think that after its own 63-hole programme, assuming the drilling is successful, VKA could move itself into a similar position to where Guardian Metals was last year.

(VKA is already OTC listed - so a bigger US listing shouldn’t be too difficult to do too)

We just need that drilling to come in now.

No guarantees of course though, the past performance of Guardian is not an indicator of future performance of VKA.

VKA is also going for a rapid restart of its project

Another reason we think VKA could end up doing a Guardian Metals is because it’s going down the unusual (for ASX small cap explorers) route of planning a rapid restart of its project BEFORE announcing a JORC resource.

IF the drill programme comes in and VKA is able to define a resource.

Then it will already have a lot of the information it needs to start presenting a rapid restart of the project - which is when we think VKA’s case for US funding support strengthens...

VKA’s Managing Director Julian Woodcock ran through the strategy in a lot of detail at his recent RIU Resources conference in Sydney two weeks ago:

(Viking Mines’ RIU presentation replay)

For those who prefer reading, here is our TLDR:

- 53-fold metallurgical upgrade - VKA has processed 1.2% tungsten feed material into a 63.6% WO3 saleable concentrate through simple gravity separation.

- (about 300,000 tonnes of material processing a year) Flowsheet finalised for a 43t per hour operation

- Modular plant design - VKA’s plan is to build modular structures that are bolt-on and can be scaled to match demand.

- More metwork optimisation is ongoing (flotation cleaning & ore sorting) - these could improve recoveries.

- Potential to reprocess material from the old tailing dam on site AND existing surface stockpiles (material the 1950s miners left over).

We think that with the January 1st deadline coming up the US will be in a position where it's willing to back domestically sourced and processed tungsten producers.

And with a bit of luck, our Investment VKA can capture some of that US government attention (and fingers crossed funding)...

Past performance is not and should not be taken as an indication of future performance.

A big part of our VKA Big Bet is the Linka project being brought back into production with a rapid restart plan which is as follows:

Our VKA Big Bet:

“VKA re-rates to $100M+ market cap with a fast to market tungsten production and downstream strategy, as well as continued interest and capital flows into the USA critical metals thematic”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our VKA Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What's next for VKA?

🔄VKA’s first drill programme at US tungsten project

Here are the milestones we are tracking for the drill programme:

- Earthworks contractor mobilises - coming weeks, ahead of the rig. 🔄

- 🔄 Drill rig mobilisation to site - late June 2026.

- 🔲 Drilling starts - (July for a six week programme)

- 🔲 Assay results (should start to land in August/September)

🔄VKA’s rapid restart plan

We also want to see VKA progress its rapid mine restart strategy.

Here are the milestones we are tracking on that front:

- 🔄 Assay results from stockpiles + tailings dam (expected in June)

- 🔄 Processing study results (CAPEX & OPEX estimates, development timelines, 3D plant design)

- 🔄 Metwork optimisation (Ore sorting + flotation testwork).

🔄 US engagement

This is more of a corporate milestone we want to see VKA hit.

It’s hard to predict when any of these might happen, but we are hoping VKA can attract some sort of US government funding to help finance its project AND/OR attract strategic interest from inside the US.

What could go wrong?

In the short term, the key risks will be from when VKA starts drilling its project.

Exploration risk

There is no guarantee that VKA's upcoming drill programmes will be successful. VKA may fail to find economic deposits of tungsten in which case we would expect the share price to re-rate lower.

Source: “What could go wrong” - VKA Investment Memo 16 December 2025

Other risks

Like any early-stage exploration company, VKA carries significant risk, here we aim to identify a few more risks.

VKA has spent months digitising old paper records and production data from the 1950s to build its current 3D geological model.

However, relying on historical data carries a real risk that the old information is inaccurate or unrepresentative of what is actually left in the ground.

The company is also pursuing an unusual strategy by planning a rapid mine restart before defining a formal JORC resource estimate.

This aggressive timeline increases execution risk, as the team could be designing a processing plant without a modern, independently verified understanding of the entire ore body.

A core pillar of the investment thesis relies on VKA capturing the attention and funding of the US government due to tightening defense regulations.

If federal backing or strategic funding falls through, the company will likely need to raise significant capital through the market, resulting in shareholder dilution.

While early metallurgical work successfully upgraded the tungsten feed through simple gravity separation, implementing modular plant designs at a commercial scale remains unproven.

Any unexpected complexities in the ongoing flotation and ore sorting tests could hurt overall recoveries and increase eventual operating costs.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our VKA Investment Memo

You can read our VKA Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our VKA Investment Memo covers:

- What does VKA do?

- The macro theme for VKA

- Our VKA Big Bet

- What we want to see VKA achieve

- Why we are Invested in VKA

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.