US $191M funding from US Export Import Bank: LKY receives “Letter of Interest”

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,188,878 LKY Shares at the time of publishing this article. The Company has been engaged by LKY to share our commentary on the progress of our Investment in LKY over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Locksley Resources (ASX:LKY) just announced US$191M in potential financing support from the US Export-Import Bank (EXIM).

(Source)

The US Export-Import Bank is the official credit agency of the USA and currently has a mandate to finance projects to reduce US dependency on critical minerals coming out of China.

A big part of EXIM’s push is to help bring projects into production that can deliver critical raw materials into US industries.

At $98M market cap, as far as we know, LKY is the smallest company (by market cap) to have received EXIM support for a US critical minerals project.

The EXIM funding intent is to develop LKY’s antimony and rare earths project in California, USA.

(the main two US critical minerals that China has been leveraging again the USA)

The next steps for LKY to unlock the funding is to progress the formal application (which triggers further DD) and also secure further funding support (for example from the US Government, US Department of War or institutional support).

LKY management says they will be in Washington in a couple of weeks to advance discussions.

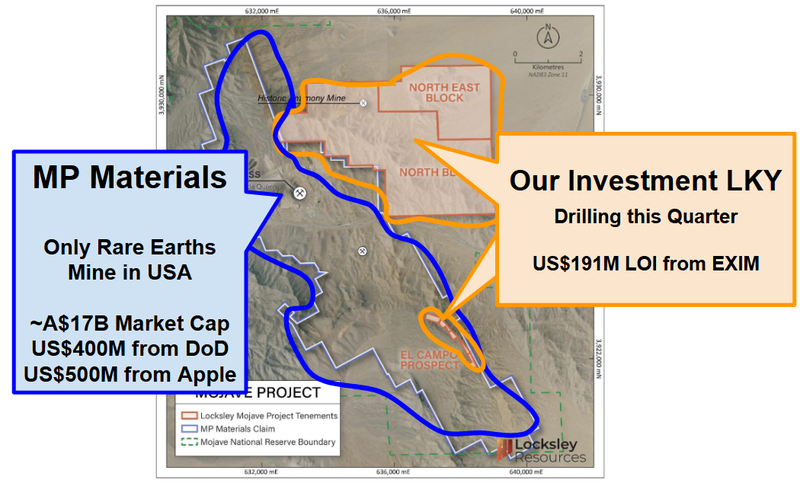

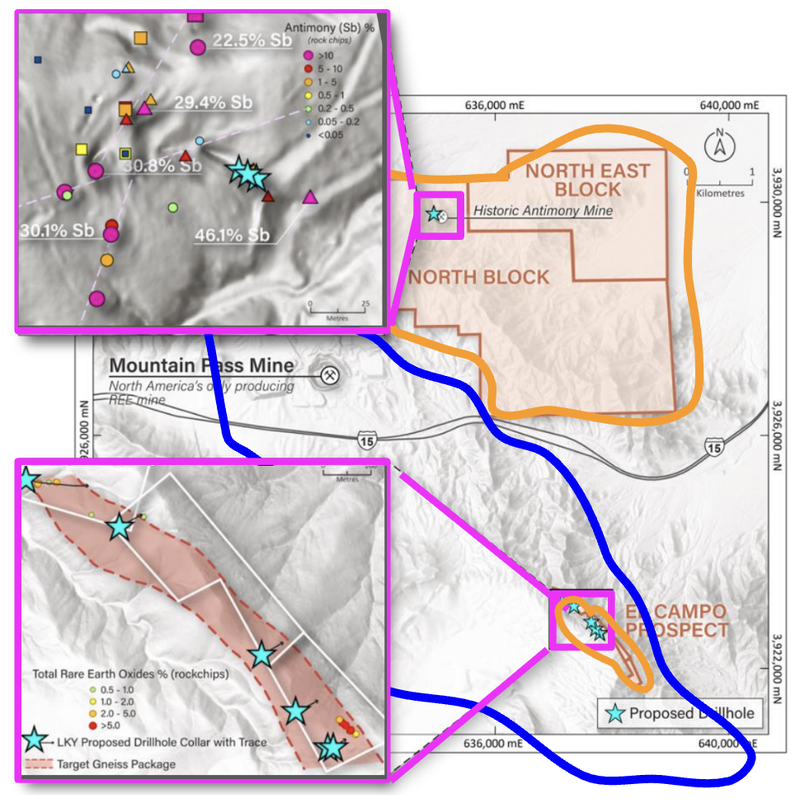

LKY’s antimony and rare earths project is directly next door to (and some of it inside of) the USA’s current (and only) rare earths mine and advanced rare earth magnets production “nation champion”, the $17BN MP Materials:

(Source)

We saw first hand just how close LKY is to MP Materials operation when we visited the project back in September

(source - read our LKY site visit)

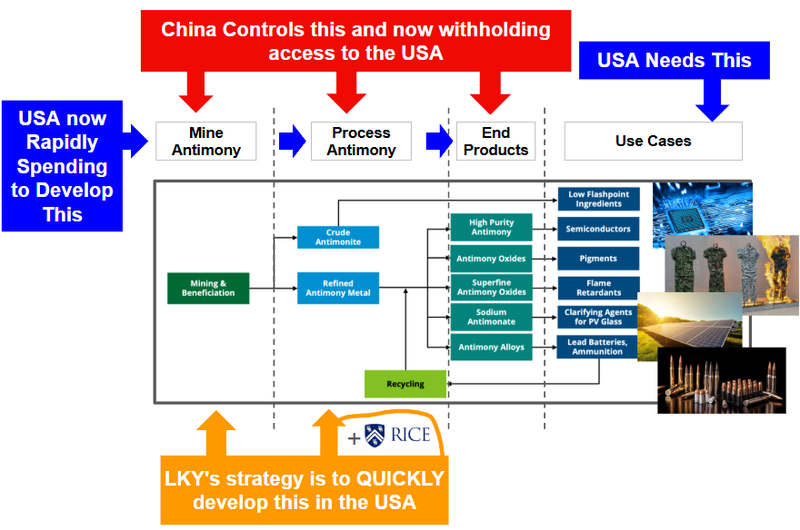

Mining raw critical minerals is one problem for the USA to solve, another is the post extraction processing technology where China also dominates.

LKY is also working on processing tech with Rice University using Deep Eutectic Solvents (green, bio-degradable, non-toxic solvents) to process its antimony concentrates and turn them into a final product.

LKY could potentially have this tech developed with Rice, that is not only applicable to its own project but also other antimony projects across the US (which would be valuable on its own).

So that is the basic summary of LKY’s rapid “mine to market” strategy for domestic USA critical minerals.

In Australian dollars, the EXIM LOI is ~A$292M in funding, for $98M capped LKY’s US antimony and rare earths project.

Which to us is early validation that the US likes LKY’s “move as fast as possible towards domestic US critical minerals production” strategy.

We also note LKY said in today’s announcement that the potential EXIM financing could be a “first step in a broader U.S. government funding pathway, opening access to programs under the Defense Production Act Title III and Department of War (DOW)”...

And that LKY execs will be attending “key meetings in Washington D.C. in mid November, to advance discussions on the Company’s U.S. mine-to-market collaboration”...

The ultimate win here for LKY would be to secure non-dilutive funding, loans and/or offtake agreements across US agencies like the:

- Department of Energy (DoE) - the DOE recently announced intent to issue US$1BN of funding - which more than half is for “minerals recycling and processing applications” (Source),

- Department of Defence (DoD), recently renamed the Department of War (DoW)

- Development Finance Corporation (DFC), and;

- Department of Interior (DOI) - LKY is in discussions with the DOI. (Source)

Interestingly... the last organisation that LKY was “in discussions with” was the Export-Import Bank of the United States (EXIM) back in August - and we’ve seen today what that resulted in.

The US$1BN available from the Department Of Energy could be a fit for the processing tech LKY is working on with Rice University to process its antimony concentrates and turn them into a final product.

Hopefully, that means this isn’t the first and only time LKY gets some sort of US funding support for its project.

14 days ago, LKY produced the first 100% US-sourced, US-processed antimony ingot in decades:

(source: LKY announcement)

We think the market dismissed the news as insignificant because it was a small sample run and didn't really take into account why it was a really strong announcement.

We said in our last note that LKY knows what the US government wants/needs right now - US sourced, US processed, antimony and most importantly... QUICKLY.

While billion-dollar antimony projects like $4.3BN Perpetua Resources are planning massive mines that won't produce for many years, LKY is taking the opposite approach of helping fill US appetite before all those big mines can come online.

(Perpetua has a funding commitment of US$1.8BN from EXIM too, by the way)

LKY’s strategy is to:

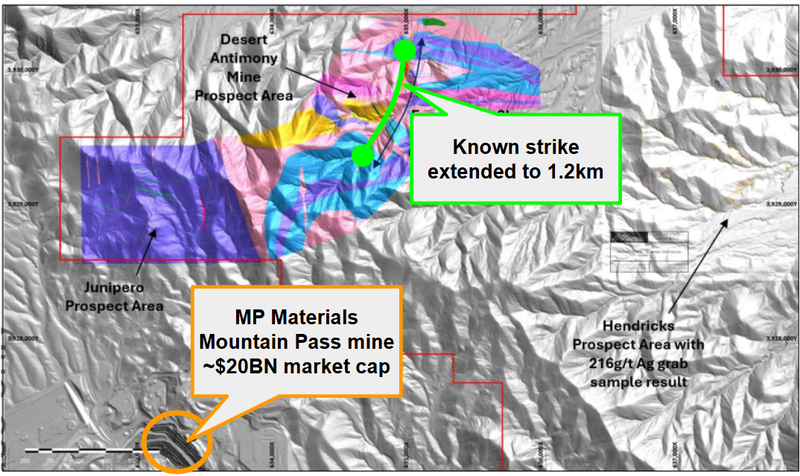

- Get its historic antimony mine back into production - LKY’s Desert Antimony Mine (DAM) was previously in production during WW1 and WW2 producing between 100 and 1000 tonnes of antimony. (Source). It’s one of the highest grade known antimony occurrences in the US.

- Drill and make a rare earths discovery next door to $17BN MP Materials.

- Process that ore and turn it into antimony (or rare earths) that is ready for end users

- Attract government funding or buying for its supply...

The strategy seems to have worked enough to the point where the US EXIM bank is willing to indicate potential financing interest of up to US$191M to LKY’s project...

Again, as far as we know, LKY is the smallest company (by market cap) to have received EXIM support for a US critical minerals project.

With US government support - will corporate support be next?

We think there is a chance now, with LKY armed with potential US government funding support for its project.

We think US corporates who are looking for antimony feedstock may all of a sudden look at LKY as a potential supply source.

The Pentagon recently set aside US$245M of its US$1BN critical mineral stockpiling fund to buy antimony from the USA’s only antimony smelter operator US Antimony Corp:

(Source)

Off the back of that news US Antimony Corp’s market cap rallied to a high of ~US$3BN...

(Its share price is up almost 1,800% in the last 18 months).

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

There’s a catch though - currently the US Antimony Corp. is putting non-US ore through its smelters.

After that Pentagon deal, it immediately went out to try and backfill its smelter to meet that order...

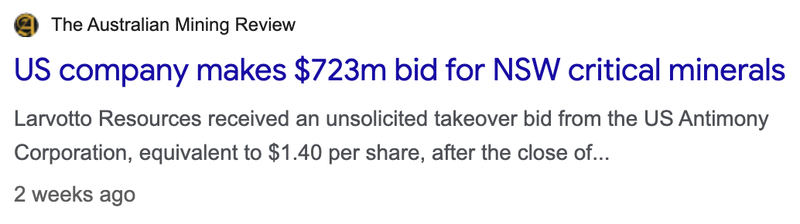

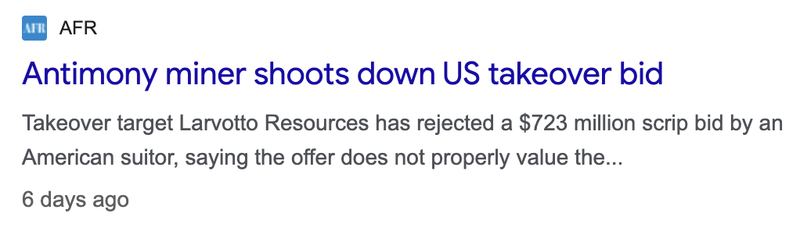

US Antimony Corp tried to acquire Australian antimony developer Larvotto Resources.

(That takeover bid was rejected, but it shows how “motivated” US Antimony Corp is to secure “friendly” antimony feedstock to fulfil their Pentagon contract).

(Source)

(Source)

Now here's where it gets interesting for LKY...

LKY already has one of the highest grade known occurrences of antimony in the USA.

LKY has already proven its Mojave Project can produce high-grade antimony concentrates (68.1% antimony).

LKY has already proven that those concentrates can be turned into antimony ingots suitable for US military specifications.

Whilst its early days in LKY determining how much antimony it can mine, surely now, LKY's domestic USA project is in the conversation as a potential feedstock option for US Antimony Corp - or any other buyer of locally-produced antimony concentrates.

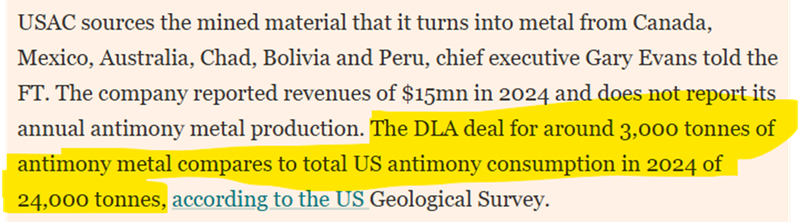

Even if someone like a US Antimony Corp was to find feedstock elsewhere, that Pentagon deal was for only ~3,000 tonnes of antimony... whereas annual consumption is closer to 24,000 tonnes...

So that “Pentagon stockpile” is going to need a lot more antimony... which means more smelters and more feedstock will be required...

(Source)

LKY is also working on clean antimony processing tech

LKY also has a processing “X factor” too.

LKY is working on tech with Rice University using Deep Eutectic Solvents (green, bio-degradable, non-toxic solvents) to process its antimony concentrates and turn them into a final product.

LKY could potentially have this tech developed with Rice, that is not only applicable to its own project but also other antimony projects across the US (which would be valuable on its own).

LKY put out an update on that partnership last week, where:

- So far the initial processing parameters have been established to develop a pilot plant to test higher volumes of material.

- Research so far has shown potential for selective dissolution (extracting only what is wanted) from the antimony ore.

AND NEXT that LKY would start testing ore samples from its own Desert Antimony Mine to form the basis for design of a pilot plant.

The big kicker here is that the processing tech could open the door for different types of funding that is being made available from the US government...

4x major catalysts that could play out for LKY over the next 6-9 months

Between now and the end of the year, we think that LKY could re-rate higher off one of the four catalysts:

- Drilling results from the antimony prospects that show the potential for an economic mining operation.

- A rare earths discovery right next door to MP Materials, the only rare earths mine in America.

- A tech breakthrough with Rice University to develop US-based, environmentally friendly antimony processing tech.

- Another surprise funding announcement where LKY receives a commitment for non-dilutive funding to advance either exploration on its projects or its downstream business.

No guarantees of course, this is speculative small cap investing and success is no guarantee.

Ultimately, our Big Bet for LKY is as follows:

Our LKY Big Bet

“LKY to re-rate to $200M market cap on the back of strong drill results and maiden resource, plus continued interest and capital flows into the USA critical metals thematic”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our LKY Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for LKY?

Drilling (this quarter) 🔄

LKY expects drilling to start in December this year. (Source)

With the rare earths drill program, LKY plans to test areas where a number of high grade rock chip samples were found, grading 1.20% to 6.87% TREO (rare earths).

With the antimony drill program, LKY plans to test for the extent of mineralisation near the historical antimony mine.

Here is where LKY’s initial drilling program is scheduled:

(Source)

We are especially looking forward to seeing if LKY can prove whether or not its Desert Antimony Mine extends over the entire 1.2km of strike recently mapped...

(Source)

Secure licence agreement with Rice University 🔄

Now that LKY has signed a partnership agreement with Rice University, the next stage will be to secure a larger licence deal over whatever technology is developed from the R&D agreement.

This will take some time to work out the IP sharing and mutual development of the technology.

What are the risks?

LKY hasn’t started drilling yet so the main risk in the short term is around “market risk”.

LKY’s valuation is where it is today because of the interest in US critical minerals stocks.

Any drops in market sentiment toward the macro thematic could impact LKY’s valuation negatively.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking LKY’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Source: “What could go wrong” - LKY Investment Memo 01-Aug-2025

For the full set of risks we have identified and accepted in making our Investment in LKY, see our LKY Investment Memo below.

Other Risks

The company's primary asset is a pre-discovery antimony and rare earth elements exploration project in California, and it is possible that LKY makes no economic discovery despite the proximity to the producing Mountain Pass mine.

LKY is highly sensitive to fluctuations in antimony and rare earth element prices.

While current geopolitical tensions have supported these prices, any easing of US-China trade restrictions or alternative supply sources could materially impact the project's economic viability and the market’s interest in exploring the project.

While LKY does have current drilling approvals in place, there is no guarantee the expanded plan of operations the company recently submitted is approved. There is also no guarantee of timely regulatory approvals which could mean delays for the planned drilling program.

Finally, despite high-grade surface samples (up to 12.1% TREO and 46% antimony), these results may not be representative of broader mineralisation at depth, and the company has yet to conduct any drilling to verify continuity.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our LKY Investment Memo

You can read our LKY Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our LKY Investment Memo covers:

- What does LKY do?

- The macro theme for LKY

- Our LKY Big Bet

- What we want to see LKY achieve

- Why we are Invested in LKY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.