Tungsten running. VKA drilling next quarter after digitisation of historical data

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 95,000,000 VKA Shares at the time of publishing this article. The Company has been engaged by VKA to share our commentary on the progress of our Investment in VKA over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

A few weeks ago the US government 12x’d its commitment to building a domestic stockpile of critical minerals.

The US government is now committing US$12BN - versus the US$1BN commitment made in 2025.

The US Department of War will be managing this stockpile.

One of the US Department of War’s top critical and strategic mineral priorities is tungsten. (source)

Tungsten is a critical military mineral used mainly in armor-piercing munitions, and is currently trading at all time highs.

The USA has zero domestic supply of tungsten.

~80% of global tungsten supply is controlled by China who imposed export restrictions on the material last year. (Source)

Two days ago Bloomberg reported US agencies have developed a critical minerals pricing floor system to reduce dependence on China for resources deemed critical to national security. (source)

We added Viking Mines (ASX:VKA) to our Portfolio late last year because we think tungsten could have an “antimony/rare earths” moment in the market in 2026.

VKA is set to drill test its tungsten asset next quarter.

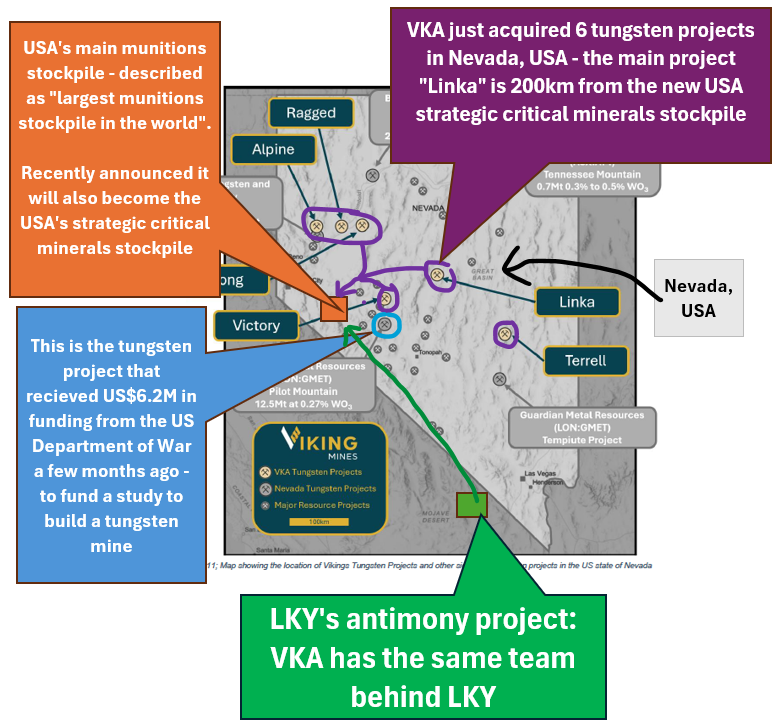

Other big reasons for our Investment in VKA were because its asset sits in Nevada (~200km away from where the US plans to place its national critical minerals stockpile) AND because the project has produced tungsten in the past.

VKA’s asset produced tungsten in the mid 1950s at ~360 tonnes per day. (source)

In total, VKA’s projects combined have historic production of ~123,000t at 0.54% tungsten oxide grades.

We think that with modern exploration, VKA can put together a mine redevelopment plan for its most advanced project (Linka) - similar to what our other Investment Locksley Resources (ASX: LKY) has done with its historic antimony mine in California.

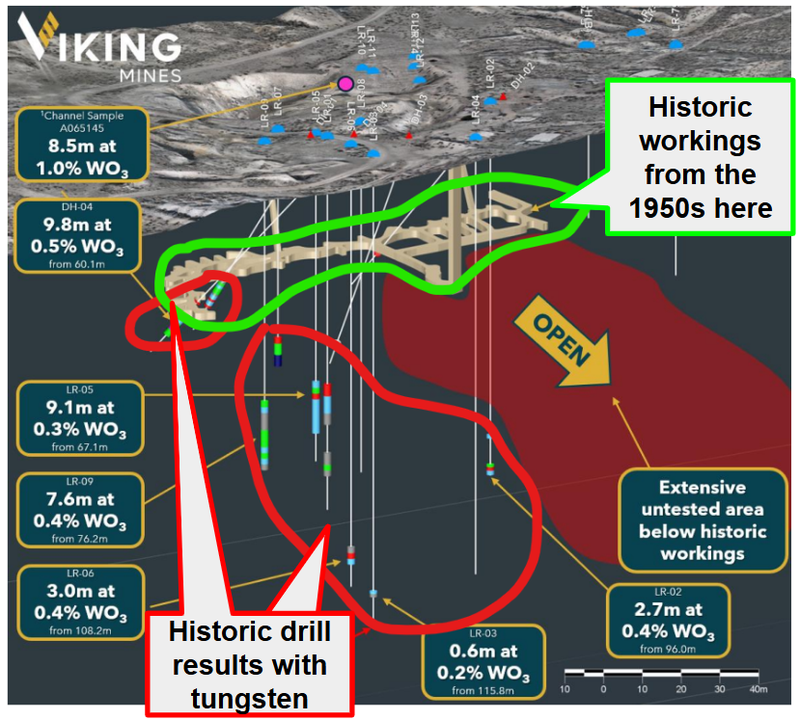

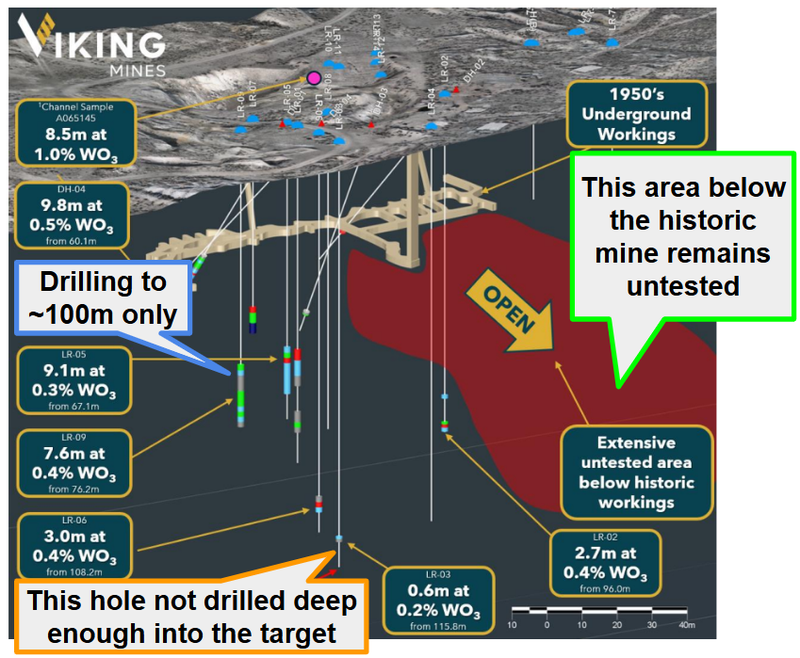

The image below from today’s announcement shows tungsten intercepts below old workings - that is a very good start - and eerily similar to what LKY was announcing a few months ago:

(source)

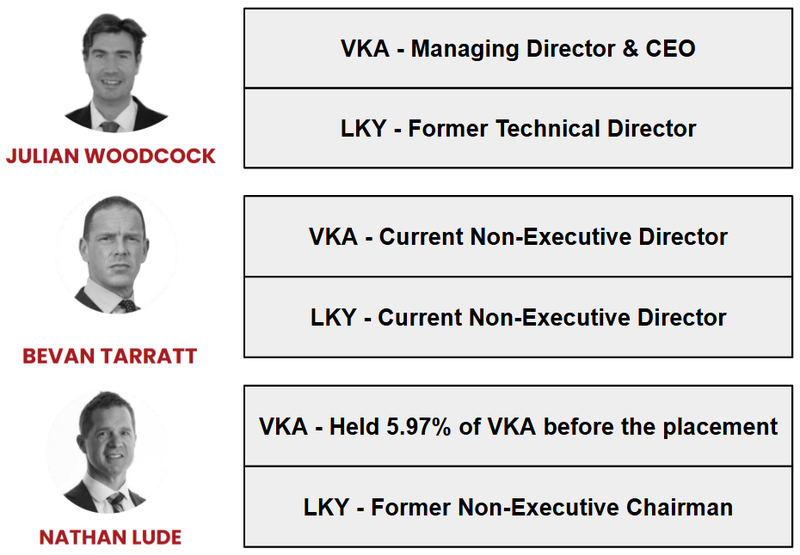

VKA is capped at ~$25M, and is backed by the same team that was involved with LKY during its 2025 run.

Inside a six month period last year, LKY ran from 1.8c to hit a high of 69c, and is now sitting at around 17c (having raised $17M at 24c per share in late 2025):

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We continue to Invest in LKY, and Invested in VKA as we hope it can grow into an ‘LKY 2.0’.

We are backing the same team from LKY to execute the same “fast to market” strategy with VKA (and fingers crossed a similar style re-rate - but no guarantees of course).

It's a fairly simple strategy of ‘following the team that made you money before’.

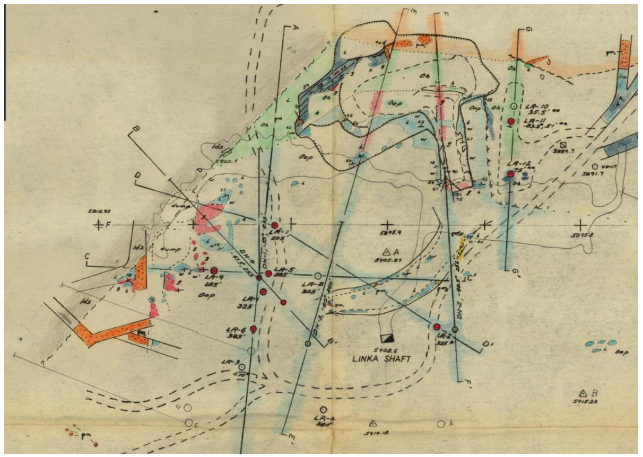

A few weeks ago, VKA acquired ~2,816m of historical drilling data - 68 drill holes (8 diamond and 60 percussion) across three of its key targets and immediately started digitising the data.

This is what those records looked like:

(source)

Looking at the above drawings, it makes sense for VKA to be running a digitisation process to bring all its data into something more appropriate for 2026.

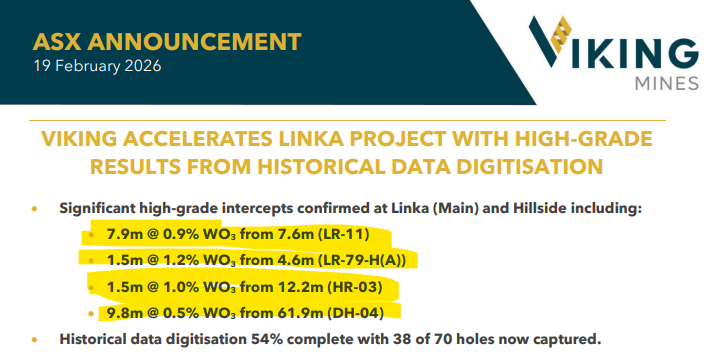

Today, VKA announced results from the first batch of results that have been “digitised” with results returning tungsten grades up to 1.2% and intercepts as thick as 9.8m.

For context on the grades - typically global tungsten mines can operate with grades as low as 0.1-0.2%.

(source)

Again, here are those intercepts below the old workings - a good sign if VKA is going to try and put together a mine restart/redevelopment plan similar to what LKY has done.

(source)

Getting all of this data means VKA can have a much better idea of where to drill and more importantly, where those old underground workings can be extended to IF VKA wants to start modelling mine restart scenarios.

We note today's announcement was only on 54% of the old datasets, who knows what else is sitting inside the rest of the old exploration data.

The next batch of data is expected "later in February”.

(it is still very early days, but a nice start from VKA).

We want to see the VKA team execute more of that similar strategy to LKY, things like:

- Go hard and fast mapping and sampling its projects (including things like LiDAR surveys to get a full sense of what’s sitting below the ground).

- Define a redevelopment strategy (similar to what they did with LKY - a video like this for one of VKA’s projects would be great)

- Define a downstream tungsten strategy for VKA (similar to what LKY is doing with Rice/Columbia university and US based Hazen Research).

LKY’s antimony strategy is built around historic antimony workings.

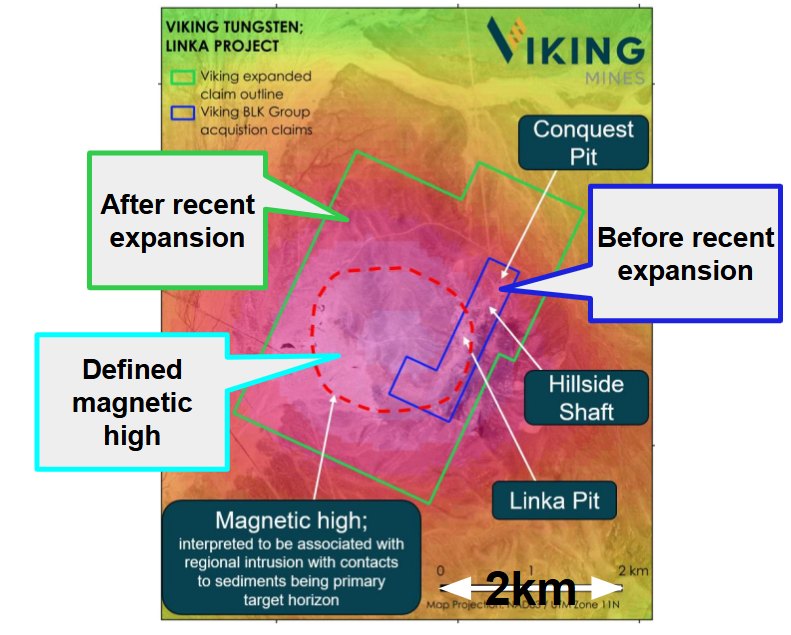

We are hoping VKA can build its strategy around the historic working on its ground (and if drilling into that geophysical anomaly discovers a monster deposit, that will be the icing on the cake for us).

(Source)

We have seen LKY execute that strategy with its historic Desert Antimony Mine in California.

One big difference between the two companies is that LKY is focussed on antimony at the same time the US government had antimony in its crosshairs for all of 2025.

IF 2026 ends up being the year of tungsten (which it's starting to look like it may be) then VKA could get swept up in the tidal wave of interest in the USA building up its own domestic tungsten supply chain.

A few big funding deals from the US government to tungsten companies and we think it will be “game on” for US tungsten assets.

We have already seen one company near VKA receive US$6.2M from the Department Of War - now we just need to see those commitments increase in size (and hopefully VKA can get some of the action too).

The map below shows where VKA’s projects sit in Nevada - relative to the project that received the Department Of War funding, the critical minerals stockpile and our other Investment LKY.

So essentially we want to see VKA roll out the LKY “fast to market” playbook - by rapidly advancing a US project during a window of heightened urgency and investor, government and market interest.

Why tungsten and why now?

In our last VKA note we mentioned the speech Special Assistant to the US president, National Security Council - David Copley gave at Saudi Arabia’s Future Minerals Forum where he said:

“Over the next few years the US government will deploy hundreds of billions in capital into the mining sector”

Then a few weeks after US Vice President JD Vance gave a speech where he started talking about establishing critical mineral price floors amongst allied countries.

In fact, Vance even mentioned that despite all of the backing the US government has given the industry to date, private capital just hadn't reacted yet (implying there is a lot more work to be done to get projects off the ground).

We covered JD Vance’s speech in detail in this section of our recent weekend note here: US critical minerals had, possibly its biggest week yet

(source)

Then a few nights ago, Bloomberg reported this:

(source)

We think the whole US critical minerals macro thematic is just getting started.

With the amount of capital to come into the space we think we will see a “rising tide lifts all boats” style effect for any of the companies who positioned themselves to benefit from the capital and interest inflows into the space.

IF the markets went into a frenzy on commitments alone in 2025, then we think the markets will love it even more when the capital actually hits critical minerals companies’ bank accounts.

(that’s before we even start thinking about potential capital coming in from the US corporates)

How tungsten fits in

We think tungsten could be the next critical mineral to capture the market and US government attention.

Tungsten is an ultra hard metal with a high melting point and so has military uses in munitions (bullets), vehicles and body armour, missiles and radiation shielding.

The USA is 100% beholden to imports of this critical military mineral.

China dominates global tungsten supply (~80% of the market) and in early 2025 put export restrictions on supply out of China. (Source)

In mid-2025 the Department of War (formerly known as the Department of Defense) gave Golden Metal Resources US$6.2M to advance its tungsten project, right near VKA’s tungsten assets.

The Assistant Secretary of Defense for Industrial Base Policy - Dr Vic Ramdass said “developing a domestic source for tungsten is one of our top critical and strategic mineral priorities”:

(source)

We think the US government will need to pour a lot more than US$6.2M into the domestic tungsten industry if it's serious about rebuilding domestic supply chains.

Especially now with the size of that critical minerals stockpile 12x’d to US$12BN AND tungsten being a key priority of that stockpile. (source) (source)

... AND we hope VKA is one of the companies to be benefiting from those capital flows.

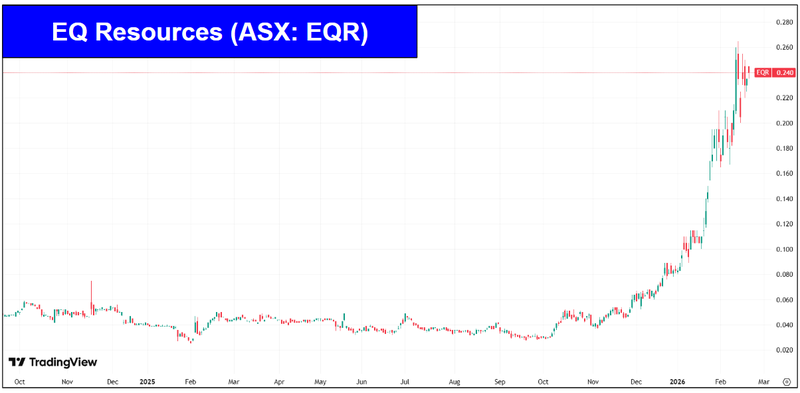

More broadly speaking, interest in tungsten names has also been on the up lately...

We have already seen some of the bigger tungsten companies run - EQ Resources hit a market cap over $1BN recently.

And another major listed on the ASX - Almonty Industries trades with a market cap of CAD$5.2BN.

Just take a look at both those companies' charts:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Eventually, we think the money made in the bigger names will find its way down into the smaller companies with interesting assets - and when it does we think the tungsten juniors (of which there are very few) will start to run.

The 9 key reasons why we Invested in VKA

Below are the 9 reasons why we Invested in VKA from our initiation note from December 16th, 2025.

You can read that December 2025 note in full here.

- Low market cap with room to re-rate higher

VKA will have a market cap of ~$11M and an enterprise value of ~$5.5M (at 0.5c post capital raise). We think the company’s valuation is currently at a level where it can re-rate to multiples of where it is now - if the US critical minerals playbook is executed well and the market continues to reward the sector.

UPDATE: VKA is currently trading at a market cap of circa $25M.

- VKA has the same team and backers as Locksley Resources (ASX: LKY).

Board, management and major shareholders of VKA are very similar to VKA. LKY at its peak was up 626% from our Initial Entry Price. We are backing the same group to deliver more wins with VKA.

Past performance is not an indicator of future performance.

- Tungsten prices trading at all time highs

Tungsten prices are currently at all time highs (source), driven by Chinese export restrictions (see reason #4 below).

We think it's a good time to have exposure to tungsten in our Portfolio.

- China dominates the global supply and has placed export restrictions on tungsten

China controls ~80% of the world’s tungsten mining and processing supply chain. In February 2025, the Chinese government put export controls on tungsten imports out of China. (source)

The US has no domestic production and is 100% reliant on imports for tungsten, which we think makes projects like VKA’s (inside US borders) valuable.

- VKA’s tungsten assets are in Nevada, USA

We like Nevada as a mining jurisdiction within the USA because it's home to some of the biggest, lowest cost mines in the country, and we have had some good wins in Nevada before (SS1, BKB).

(past performance is not an indicator of future performance)

- Very few companies with tungsten projects on the ASX - even less with projects inside the USA

There are very few tungsten-focused companies on the ASX - especially ones with projects inside the US.

IF US tungsten companies go on a run it could mean a lot of capital looks to flow into a handful of companies of which VKA will be one.

- VKA’s projects have produced tungsten in the past

Across the six assets VKA is acquiring, there has been ~123,000 tonnes mined from open pits, and underground adits.

One project also has a 360 tonne per day mill in place. Channel sampling from VKA’s project returned grades of ~2.11%. The biggest tungsten deposit inside US borders (also in Nevada) has average grades of 0.25% tungsten.

- Capital is flowing into US critical metals macro thematic

We think VKA’s US tungsten assets could attract increased capital flows both on the ASX and from North American investors/governments/institutions.

Funding from US government agencies could be from places like the Department of War, Department of Energy, Department of Interior.

Alternatively, VKA’s project could attract capital from tungsten end users or big financiers like JP Morgan who is just starting to become active in the critical minerals space.

- VKA can follow the “US critical minerals playbook”

There is a playbook for ASX stocks to attract more attention and capital to projects that are based in the US. VKA isn’t yet listed in the US, and we think that if its project gets any traction it could go for a US listing that opens up the project to North American investors.

Our VKA Big Bet:

“VKA re-rates to $100M+ market cap with a fast to market tungsten production and downstream strategy, as well as continued interest and capital flows into the USA critical metals thematic”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our VKA Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for VKA?

🔄 Target generation work (mapping/sampling)

We want to see VKA digitise the historical drilling and previous sampling data on the project, which VKA has confirmed today that it is now 54% of the way through.

After that we want to see the full data set get integrated into a modern 3D model.

We also want to see the project mapped with LiDAR to reveal the full extent of the underground workings on the project.

Milestones:

🔄 Mapping and sampling (soils and rock chips)

🔄 Geophysics/LiDAR (geophysics commenced a few weeks ago) (source)

🔲 Drill targets confirmed

🔲 Drilling (planned for April) (source)

🔄Early metwork testing

VKA recently sent off a bulk sample to test its viability for processing.

In particular there is a focus on exploring the viability for this to be used in an early production opportunity scenario, with results from this expected in February. (source)

What are the risks?

Like any small cap exploration company, investing in VKA involves a range of risks, some known, some unknown (this is the nature of investing in early-stage companies).

Here we aim to identify some of the key risks.

VKA’s new tungsten projects rely heavily on historical data, production records, and sampling from the 1940s and 1950s. There is a risk that VKA is unable to verify this historical data with modern exploration work.

A key part of our Investment Thesis relies on VKA successfully executing the "US market listing playbook" (including US listings, appointing lobbyists, and securing downstream partnerships).

There is a risk that VKA fails to execute these corporate strategies effectively or that they do not generate the anticipated interest from US investors.

Although the US government is actively funding critical minerals projects, there is no guarantee VKA will receive any government grants or strategic funding.

VKA will need to secure permits for its planned drilling programs and any future development in Nevada. VKA may face regulatory delays that could slow down exploration.

Finally, the market for tungsten is relatively opaque and dominated by China. Any changes in Chinese export policies or global demand could impact the underlying commodity price and investor sentiment toward the sector.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our VKA Investment Memo

You can read our VKA Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our VKA Investment Memo covers:

- What does VKA do?

- The macro theme for VKA

- Our VKA Big Bet

- What we want to see VKA achieve

- Why we are Invested in VKA

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.