Triple-Crown Supercycle: The 3 Incoming Global Buildouts

Published 04-APR-2026 16:39 P.M.

|

17 minute read

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

Any forward-looking statements are uncertain and not a guaranteed outcome.

On Wednesday at around 2pm AEDT I was staring at gold and silver prices (as usual).

Both had been delivering a great couple of days of gains.

So it was a fun watch.

When suddenly...

Gold down ~3%. Silver down ~6%

Oil up 6%+.

(all in a matter of minutes)

After spitting out my chamomile tea, the first thing I thought was:

"Ok what did he say/tweet now"

...and I popped over to the news and social media to see what might have happened.

Sure enough, Trump had just addressed the nation.

And the market took his comments to mean that the war would be going on for at least another 2-3 weeks AND that an escalation was possible IF a deal isn't reached soon.

Some folks proceeded to dump gold and silver (safe havens in times of war and uncertainty, right...right?) while aggressively buying oil.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Trump also said the unblocking of the Strait of Hormuz (where 20% of global oil consumed flows through) is “not America's problem”.

He said that the US imports almost no oil through the strait and won't be taking any in the future.

Other countries who depend on Middle Eastern oil should go and defend the strait themselves (Source).

Another clear signal: the USA is withdrawing from its post WW2 role as the “world police”.

(We wrote about this back in January - “the Donroe Doctrine” where the USA withdraws from being the world police and switches focus on the Western hemisphere only - read it here)

The implication is that individual countries and regional blocs now need to build out their own military and defence capabilities. Fast.

(What would you do if all the police stations in your suburb suddenly announced they were stopping their service? Go and buy a baseball bat ASAP... preferably a hard one made of tungsten or antimony)

Then (last night) French President Macron called on medium-sized powers to join forces and stand up to both the US and China.

(source)

So are we moving to a multi-polar world now?

USA and the Western Hemisphere, China and friends, Europe and friends?

Each with a “local police force”.

So not one giant global military, AI, data centre and robot buildout but three of them. Simultaneously?

Every “bloc” is going to want control of their own...

And all of that is going to need materials/energy to build and power it...

Will that build-out trigger the next commodity supercycle?

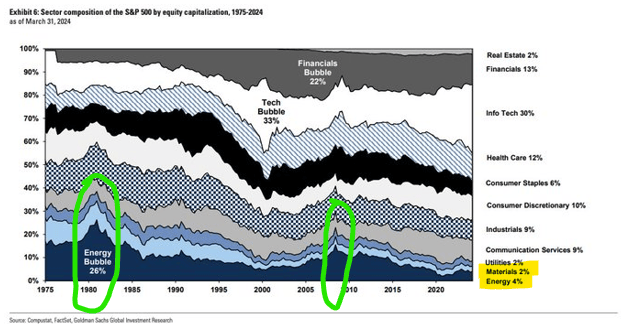

The energy and materials sector currently makes up around 6.1% of the S&P 500. (source)

During the 1970s commodity boom, energy and materials peaked at over 30% of the S&P 500. (source)

(plus gold went from $35 to $850. Silver from $3 to $50, Oil quadrupled.)

When the S&P 500 first launched (during the post WW2 USA industrial build out) energy and materials was 47% of the index (source)

Remember the China-driven commodity boom in the 2000s?

Commodity prices went up 500% from early 2000s levels.

Iron ore went from $30/tonne to $190/tonne.

China consumed 90% of the world's additional copper during 2000-2006.

(Anyone who was on the commodities-heavy ASX during the China boom knows the feeling. Everything ran. Even the dogs. Especially the dogs.)

(source)

So what gets us from 6% back to something closer to 20-30-40% range which is when we enter commodity boom territory?

The same thing has driven every single mining boom in the last 200 years: a giant global, physical buildout.

Each mining boom happened when the world needed to build something enormous.

And right now we think there are THREE enormous buildouts happening all at once - AI data centres, humanoid robots, and a (tri-polar?) global military rebuilds.

(not to mention a broader fiat currency devaluation that puts “fuel on the commodity price fire” - similar to the 1970’s)

We made a new Investment this week which could play a role in all three of those...

Pure Resources (ASX:PR1) - thermal management materials for AI data centres, robotics and military systems.

(yep, the three big buildouts we think are going to happen)

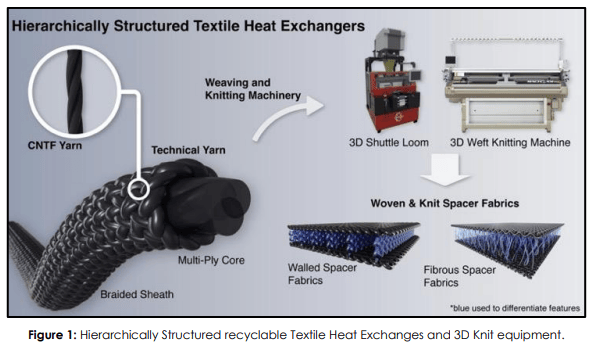

PR1 is collaborating with Rice University in Houston.

Rice University is the birthplace of carbon nanotube fibre tech which is:

- 17% more thermally conductive than copper

- 50x stronger than copper by weight

- 5.6x lighter than copper

(source - PR1 announcement)

That conductivity increase, strength and weight advantage makes it suitable for use in hyperscale AI data centres (heat management is one of the biggest engineering challenges in dense AI compute), directed-energy weapons, and autonomous defence systems.

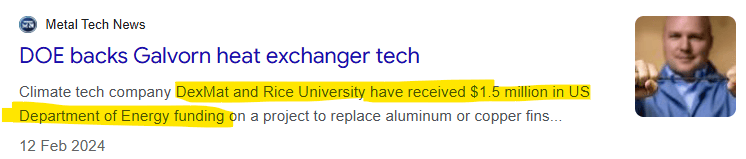

The tech has also received backing from the corporate venture capital arm of energy supermajor Shell AND funding from the US Department of Energy, NASA, the US Air Force, and ARPA-E. (source) (source)

(source)

Rice tech collaborations/deals have also been behind some of the best performing tech companies on the ASX in recent years, too:

- up ~700% at its peak. ~$750M capped Weebit Nano (ASX: WBT): ReRAM semiconductor technology

- up ~800% at its peak. ~$450M capped Metallium (ASX: MTM): Flash Joule Heating technology

- up 104% on the day it partnered with Rice Uni for Flash Joule Heating technology. ~$35M capped Environmental Clean Technologies (ASX: ECT):

- Locksley Resources (ASX: LKY) - which we are also Invested in - signed a collaboration with Rice Uni - on that day alone, LKY’s share price was up over 40%. One of our best performers of 2025

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

PR1 had a NEW presentation out on Thursday which gives a lot more colour around what the company is doing - check that out here.

PR1’s current market cap closed on Friday around ~$17.5M, our Big Bet is to see:

"PR1 re-rates to a +$200M market cap by securing a pathway into the carbon nanotube fibre thermal management supply chain, attracting strategic partnerships with major data centre or defence customers, and/or being acquired at a multiple of our Initial Entry Price."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PR1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Read our full initiation note AND why we Invested here: Our Latest Investment: Pure Resources (ASX: PR1) - Thermal Management for AI data centres, Military and Robotics with Rice University

Now, back to global buildouts driving commodity booms...

Every mining boom is born from a giant buildout - here's the history

We have been talking about a coming “every commodity” boom for a while now.

And looking at the stats we shared above, energy and materials currently make up about 6% of the S&P 500.

When the S&P 500 launched in 1957 (in the middle of the post WW2 US industrial build out), metals and materials were roughly 47% of the S&P 500 (source).

Nearly every major mining boom in the last 200 years has been driven by one thing: a giant physical buildout.

And a giant, global build out = bigger market caps for mining/energy companies.

Here a quick overview of the ones in the past:

The Railroad Era (1840s-1870s)

The US railroad network went from 4,800km to over 115,000km in 30 years.

That required millions of tonnes of iron and steel, coal to run the trains, and timber for the sleepers.

Mining companies and mining towns (and mining countries with mining heavy stock exchanges?) were big winners.

The losers: Canal workers, barge operators, and the entire horse-and-coach transport industry.

Electrification (1880s-1920s)

Edison, Tesla, Westinghouse - the great electrification of America and Europe.

Copper wiring ran to every home, every factory, every streetlight.

Global copper demand tripled between 1880 and 1920.

Again miners and mining towns did extremely well.

The losers: Lamplighters, gas companies, and the massive ice delivery industry.

Post-WW2 Industrial Buildout (1945-1970)

The Marshall Plan rebuilt Europe.

America built the interstate highway system (~66,000km of new road).

Suburbs exploded.

Every house needed steel, copper, concrete, aluminium.

The Korean War and then Vietnam kept military metals in permanent demand.

Materials and energy hit at ~20% to 30% of the S&P 500 in the early 1970s.

The 1970s Stagflation / Commodity Supercycle (1968-1982)

(note, this is NOT a build out, but shows how rapid currency devaluation turbocharges hard commodity prices, worth mentioning given the upcoming buildouts we are watching could happen under a depreciating currency environment)

Nixon closed the "gold window" in 1971 — the US dollar was no longer backed by gold.

Overnight, every commodity on earth repriced against a falling dollar.

Then OPEC cut off oil supply during the 1973 Yom Kippur War. Oil went from $3 to $12 in months. The Iranian Revolution doubled it again to $40.

Gold went from $35 to $850. Silver from $3 to $50. Sugar from 5c to 65c. Everything ripped.

The Barron's Gold Mining Index surged 1,247% in 11 years. The S&P 500 did 43% over the same period.

By 1980, seven of the top 10 biggest US companies were oil and energy firms.

Mining and energy peaked at over a third of the US stock market.

(Then Volcker hiked rates to 20%, killed inflation, and commodities crashed for two decades. Boo.)

China's Industrialisation (2000-2012)

The biggest construction boom in human history - this one happened in our lifetime.

China built the equivalent of every American city, simultaneously, in about 15 years.

Iron ore went from $30/tonne to $190/tonne.

BHP went from $5 to $50. RIO $15 to $122. FMG from 10c to $12.

Copper hit record highs.

Junior ASX explorers became 10-baggers on the back of iron ore and coal.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

So the pattern always looks very similar.

A physical buildout of extraordinary scale drives extraordinary demand for metals and minerals.

And when enough capital chases that demand, the materials and energy sector goes from ~6% of the index to 20% plus.

(the ASX is always heavily weighted on materials and energy, but we are focusing on bigger global markets here - this is where a serious commodity cycle will be driven from, and ASX resources stocks will be swept up with it)

The S&P 500 are at 6% right now.

So what could get it from 6% to 20% plus?

The current buildout to drive the “every commodity” boom? - three of them, actually

The three parallel buildouts driving the commodity boom:

- Military rebuild - every country re-arming independently

- AI data centres - the world's biggest infrastructure build since electrification

- Humanoid robots - billions of metal bodies needing copper, lithium, nickel, rare earths

All three need many of the same metals.

All three are happening simultaneously.

And mining CapEx is at record lows going into all of it.

(Or it could all settle down next week and we'll look silly - always a possibility. Though the geopolitical situation doesn't feel like it's heading that direction.)

AND with some global currency devaluation sprinkled on top to turbocharge things?

We think that setup creates one of the biggest capital rotation opportunities of our lifetime.

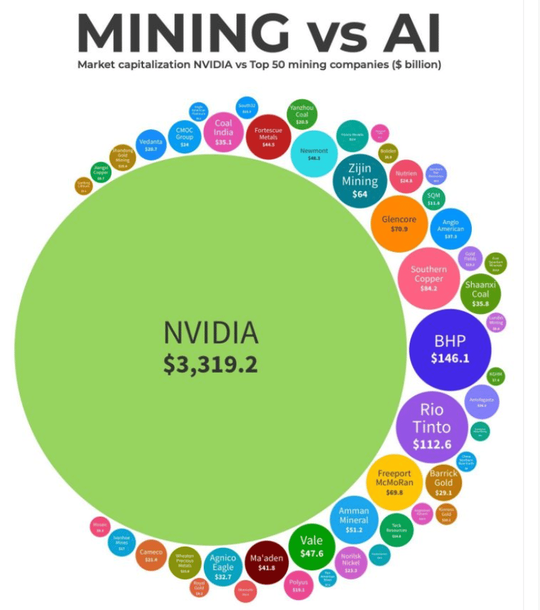

The one image we keep referring back to as a strong way to visualise what could be coming is the market cap of NVIDIA being bigger than the top 50 mining companies COMBINED.

(Source, Mining.com October 28, 2024)

Out of companies that AI and robotics can disrupt - and into the hard, physical assets that AI and robotics actually needs to exist.

Major robot buildout coming? What happened in the robotics sector this week

Every week we see more amazing (and terrifying) developments coming out of the robotics space.

And the more I see the more I'm convinced that robots are going to become widely adopted, sooner than we all think.

I've been on a pretty heavy dystopian sci-fi diet my whole life.

Robocop. Terminator 2. The Matrix. Altered Carbon. Blade Runner. I, Robot. Ex Machina. Westworld. Black Mirror.

My entire historical consumption of robot content has created a mental model that is basically: robots bad, humans naive, dystopia inevitable.

But at the Tesla AGM in November 2025, Elon Musk described his vision for a future where robots do all the work and humans live lives of leisure.

(source)

He said it was "kind of Banksian" - a reference to the late sci-fi author Iain M. Banks, who wrote the Culture series.

The Culture Series is ten books about a post-scarcity civilization run by benevolent superintelligent AI’s called "Minds" while humans just... do whatever they want.

Sounds good and I’m glad one of the key minds driving the AI robot revolution is filling his brain with this utopian vision of the future of AI and robotics...and not the dystopian version presented in The Matrix.

I'm going to start reading the Culture series this week. There are 10 of them so it's going to take me a while to get fully robot-positive. But I'll try.

While I work on my attitude, here's what happened in robotics this week:

I did notice a lot of positive robot developments (which I’ll start with) and of course finish up with the latest in terrifying, AI driven, autonomous gunwielding murder-bots.

New in utopian robots

Robots caring for elderly humans.

(source)

Upgraded Unitree G1 humanoid doing household chores - independently. (sounds good to me)

A Shenzhen startup added an "advanced robot brain" to the Unitree G1.

The result: the robot waters plants, opens curtains, cleans surfaces and moves objects around the house, all without human input.

(source)

Robots doing manual labour (does any human genuinely like doing manual labour?)

LimX's Oli robot autonomously unpacks itself from a shipping container and starts walking and working.

(source)

Autonomous mining? Keeping humans safe from dangerous places.

China deployed 100 fully autonomous electric mining trucks in mid-2025 - and is scaling to 10,000+ by 2026.

(source)

Now back to dystopia...

New in dystopian robots:

Soldiers running military drills alongside robot troops - with the robots leading the breach.

(source)

China's robot wolves - equipped with micro-missiles and grenade launchers - running simulated street battles.

(source)

Synthetic skin covered robot arm - seen that before...

Stanford researchers published work on synthetic self-healing skin for robots - a flexible material that senses temperature, pressure and humidity, and repairs itself when damaged.

(source)

Most of us remember this from Terminator 2:

In fact, the Cyberdyne Systems Series 800 Model 101 (T-800) in the movie had skin that couldn't repair itself...

So modern technology has already surpassed it (facepalms).

And yet - a robot that can repair itself in the field?

That is useful for both industrial and military applications.

So for good or bad, better or worse, utopia or dystopia...

The robots are coming.

Every single one of these robots needs metals. Copper for motors and wiring. Nickel and cobalt for batteries. Rare earths for the motors and sensors. Aluminium and titanium for frames. Lithium for energy storage.

And whether it's a utopian robot deciding what time it needs to bring lunch to your grandma, or a dystopian robot deciding which weapon to shoot you in the face with, every robot will need to make decisions...

And to make decisions, it will need an AI-powered brain.

Which brings us to the AI and AI data centre build-out.

AI and AI Data Centres

AI and AI data centres are the third parallel buildout driver of the commodity boom we are predicting.

A single megawatt of AI data centre capacity requires 60-75 tonnes of minerals - copper, aluminium, steel, rare earths, specialised materials.

A modern AI chip contains around 300 different materials.

And new mines take, on average, well over a decade from discovery to production.

The world's data centre capacity is supposed to roughly double by 2030. The minerals don't exist yet at the scale required.

Which is where the opportunity sits in the junior resource space (which our Portfolio is heavily weighted towards).

(We wrote a whole note on this here if you want the full thesis in one place.)

Now add in currency debasement...

Currency debasement throws fire to the fuel of a commodity boom.

And turbocharges gold and silver...

We listened to these two interviews this week, worth a listen.

The first is with macro strategist Tavi Costa:

Here is a TLDR, for those who prefer to read:

- Tavi thinks the US Fed is trapped - basically that they can't raise rates without blowing up the bond market (US debt interest payments already 4-6% of GDP), and they can't cut without re-igniting inflation. The quote was "The biggest ballistic missile hitting the US economy is not Iran - it's rates going higher."

- Mining capex is at all-time lows (adjusted for gold prices) - No M&A frenzy. Exploration budgets at 3-4 year lows. Tavi said, "I would challenge anybody to show me one time in history that the mining cycle ended with capex at all-time lows. Never."

- The US government plans to spend $200 billion on critical mineral reserves - more than the entire mining industry is worth...

- He called this a generational buying opportunity(at US$4,500-$5,500 gold and ~US$70 silver). We haven't even seen the mania phase yet.

The second is with Macro analyst Lyn Alden:

Again, here is the TLDR:

- Lyn says the fiat money system "must grow or die" - meaning money supply growth at ~7% per year is structural and has to happen otherwise the system doesn’t work.

- Lyn thinks the winners in this system are the ones who "short the currency" - borrow cheap, own scarce things. Corporations, governments, and the wealthy all do it. Everyone else gets their savings quietly eaten alive.

- Gold's supply grows ~2% a year. US dollar supply grows ~7%. That gap is the entire thesis for owning hard assets over holding cash.

- AI doesn't fix any of this - it's a productivity boost that extends the runway before the next inflationary reset, but it doesn't change the structural debasement. "You can't print new homes. You can't print healthcare. You can't print energy."

- The system can go on for decades longer... unless war and energy shortages blow it up first. (Sound familiar?)

The two podcasts come at the whole debasement theory from two different angles but its hard to disagree with 99% of the points both are making.

We (also) think the gold and silver mania hasn't properly started yet...

(AND yes, this could be our confirmation bias seeking subconscious, making us say this)

Despite how much we agree - no one really knows what will happen with gold and silver prices (or any commodity prices in general) - nobody has a crystal ball...

At this stage, we think its the most important to be ready to alter our opinions based on changes geopolitically and economically.

If oil prices go to US$300-400 a barrel then everything changes...

See you next week, and have a great weekend.

Next Investors

Did someone forward this to you? Subscribe Here

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.