TRI - Cancer diagnostics. Ex- $5BN Telix Chief starts as CEO in 13 days

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 23,820,000 TRI Shares at the time of publishing this article. The Company has been engaged by TRI to share our commentary on the progress of our Investment in TRI over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

The battle between humans versus cancer has been raging for as long as we have existed.

Chances are you have a family member who has been affected.

So can we please hurry up and sort it out, FFS?

Our $30M capped Investment TrivarX (ASX:TRI) acquired a very clever (yet simple) cancer diagnostics tech in December last year.

It can light up even the earliest stage, usually undetectable cancer cells like a Christmas tree.

And if you can see them, you can target them...

If you can find and see them early, there is a better chance of treatment and survival.

And you’ll be surprised by how it actually does it...

TRI acquired the tech way back in December - so why are we writing about TRI now?

Because in 13 days (on June 1st), Dr Danielle Meyrick, the ex-Chief Medical Officer for the $5BN Telix Pharmaceuticals will officially start as the TRI CEO.

And a new high caliber CEO should see TRI accelerate clinical trials and ultimately bring it to market.

Telix (where TRI’s new CEO is from) was a favourite amongst small cap investors, IPO’ing $50M at 65c per share in late 2017 and peaking near $32 in early 2025 at a cap of ~$10.7BN.

(Telix, like TRI also plays in the brain imaging space)

The past performance of Telix is not an indicator of the future performance of TRI.

Dr Meyrick is a big hire for the $30M capped TRI.

After leaving Telix she was Chief Medical Officer at one of the global leaders in isotope-based therapeutics.

So she has spent 20+ years in radiotheranostics and isotope-based imaging - the exact field TRI’s new asset sits in now.

We think that as of June 1st with a new experienced CEO in place, TRI can really start to go hard at developing its new tech and ultimately try to bring it to market.

Which brings us to TRI’s new tech...

TRI’s new imaging tech targets earlier, non-invasive detection of tumour activity beyond conventional MRI limitations.

Finding cancer before it spreads and before an MRI can even see it in the brain.

(Bonus: It makes existing MRI machines already sitting in hospitals more effective - a quick win for hospitals, with no new tech, processes, training etc)

(source)

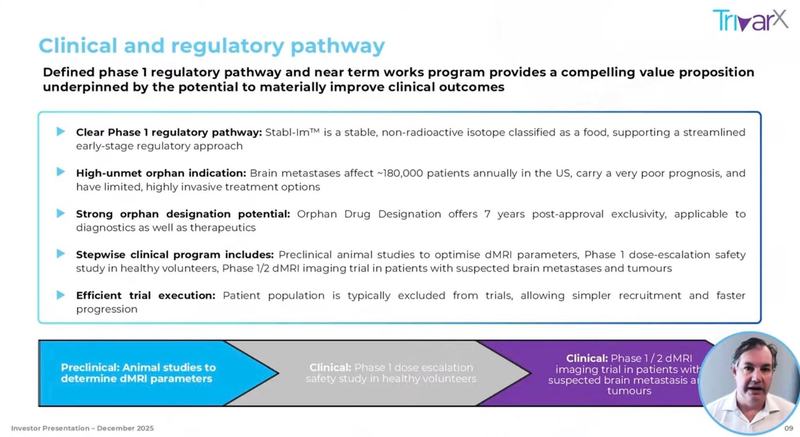

Phase 1 clinical trials are planned for this year.

We’ve had a good run with the team behind TRI.

TRI shares board, team members and shareholders with our 2025 Biotech Pick of The Year, the $127M capped Island Pharmaceuticals (ASX: ILA).

Yesterday ILA was up 21% on $1.2M of volume on an otherwise shocking day on the market.

ILA has been a great performer for us - up 183% from our Initial Entry price.

Following on from our success Investing in the $127M capped ILA, we are backing the new look, $30M capped TRI to deliver a similar win for us over time.

(the past performance of ILA is not an indicator of future performance of TRI)

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Here are the TRI / ILA connections:

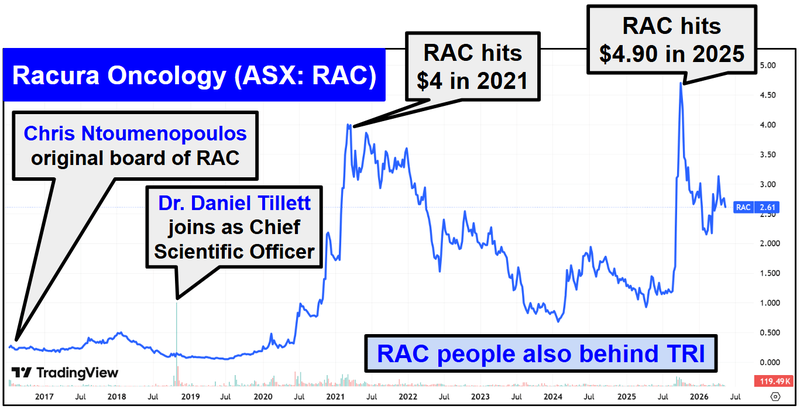

Dr Daniel Tillett:

- ILA’s 4th biggest shareholder (7.80% of ILA)

- Put $500k of his own cash into TRI back in October last year at 0.8c per share.

- The inventor of the technology

- Is TRI’s technical advisor overseeing the tech development

- Is incentivized with vendor milestone payments to see TRI get to the clinic and deliver successful Phase 1 and Phase 2 trials

- Is also the CEO & Managing Director of $522M capped Racura Oncology.

Chris Ntoumenopoulos:

- ILA Non-Executive Director

- TRI Non-Executive Director

- Part of the team that sold Resapp to Pfizer for $180M in 2022.

- Original Non-Executive Director in Racura Oncology.

So there is the Racura connection too.

Racura (formerly known as Race Oncology) was a 16 bagger for early investors going from 25c to $4 in under 5 years.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

TRI is capped at ~$30M and we think the new asset could end up being a genuine company maker for TRI.

We will explain why we think so in today’s note.

But first, what exactly did TRI acquire?

TRI’s new brain cancer imaging tech

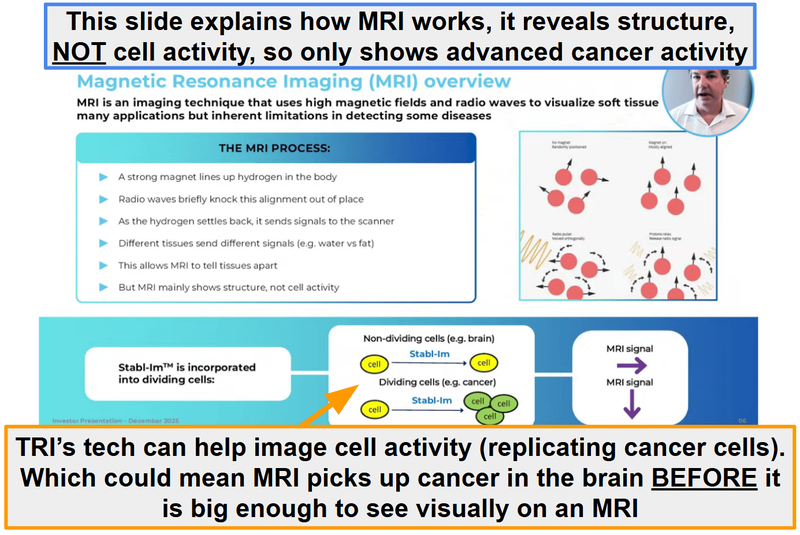

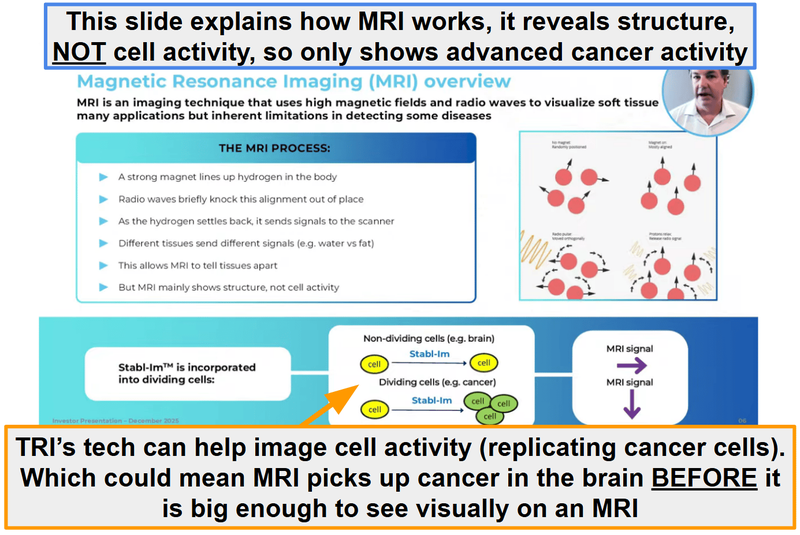

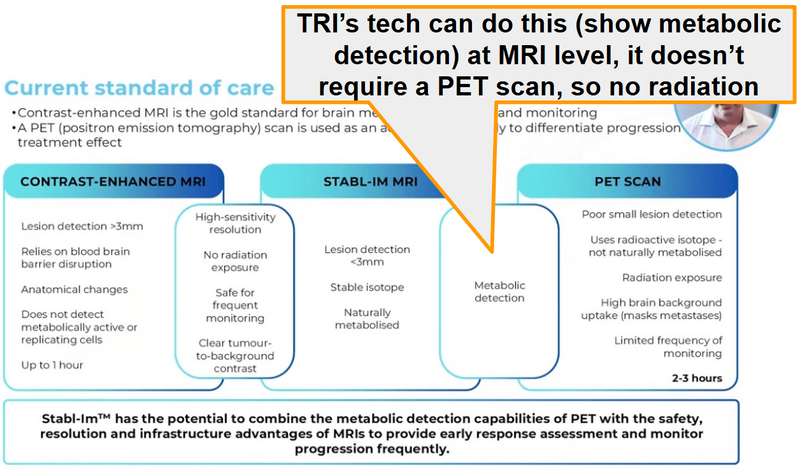

In December last year, TRI acquired a technology which uses “stable isotopes” to label cancer cells inside the brain.

The way it does that is by labelling “replicating cells” - the type of cells that indicate cancer.

In a healthy adult brain, cell replication is extremely rare.

So if you can detect cell replication in the brain, you can detect tumour activity very early on.

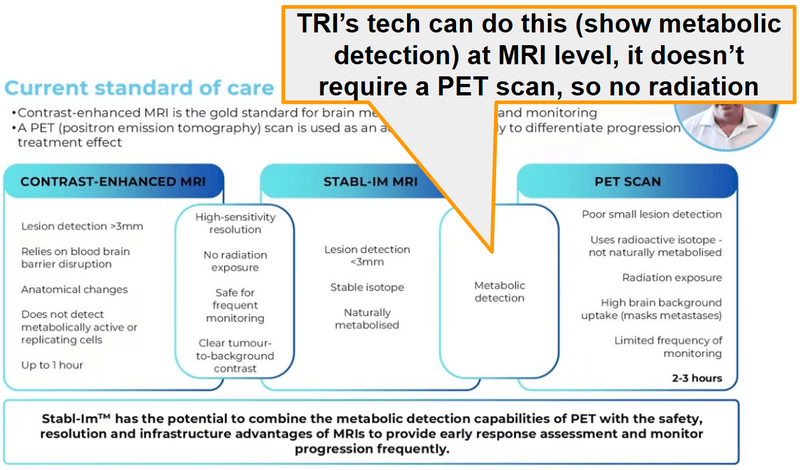

(instead of having to visually sight it - like conventional MRI, which can only detect a tumour once it's grown to 2-3mm in size - which is often too late).

(source)

Basically:

- stable isotope.

A patient swallows a small dose of a compound that's labelled with a - cells that are actively replicating.

The labelled compound is taken up by - standard MRI machine then "sees" the labelled cells, because stable isotopes have slightly different magnetic properties from their normal counterparts. A

The result:

A non-invasive, radiation-free way to see tumours early.

Imagine trying to spot a handful of troublemakers in a stadium of 50,000 people.

From a distance, everyone looks the same. But hand every troublemaker a flare, wait for them to light them up and suddenly they're easy to pick out from the crowd.

That's what TRI's tech does, it makes the cells that matter light up on an MRI, so tumour activity can be spotted at a stage where it would otherwise blend into healthy tissue.

Or if you’ve ever watched one of those bank heist movies where a paint bomb in the stolen money bag explodes, covering the bank robbers in paint, allowing police to more easily find them.

Except in TRI’s case the flares and paint are active BEFORE any trouble gets caused.

So it's probably more like when you were a kid and your mum said “DON’T EVEN THINK ABOUT IT” after her mum-instincts somehow detected that you were about to do something naughty.

(to this day I have no idea how she was able to do that as soon as just the thought of causing trouble entered my mind)

The reason we like TRI’s new tech is because it’s trying to solve the biggest gap in the current standard of care.

Being able to diagnose cancer early.

Once cancer cells hit the brain and start spreading, five year survival rates become ~6.1%.

But there is no reliable way to image the earliest stages of a brain tumour.

Current MRI scans can only detect a brain tumour once it has grown to 2-3mm.

By the time the tumour is big enough to be detected - it's already established, aggressive and hard to treat.

So the current “gold” standard of brain tumour imaging (MRI) can’t see if a tumour is forming.

Only if cancer already exists or not.

TRI’s tech (IF it works) would sit alongside MRI.

TRI’s isotopes would go into the patient.

Then the MRI would be done to see if those “labelled cells” can be seen.

Without adding any radiation to the imaging process.

(source)

The reason we think TRI’s tech has a real shot at being commercialised is because it involves a well understood process in the imaging sector.

Enhancing existing imaging tech is an accepted thing in the diagnostics space.

What's less accepted is replacing existing standards of care.

TRI’s tech, working alongside MRI, means theoretically there would be no risk of missing what the current standard of care would have picked up.

A patient with a suspected brain tumour would have had to get an MRI anyway.

TRI’s tech would come in and sit alongside that - enhancing diagnostic capability - not completely replacing it.

At the moment TRI’s tech is pre-clinical.

TRI’s plan is to run:

- Phase 1 first-in-human trials to determine safety

- Animal trials to optimise dMRI parameters (basically optimising for imaging quality).

TRI expects to start both of those this year.

(source)

Check out Dr Daniel Tillett talk through the tech in the following interview:

(source)

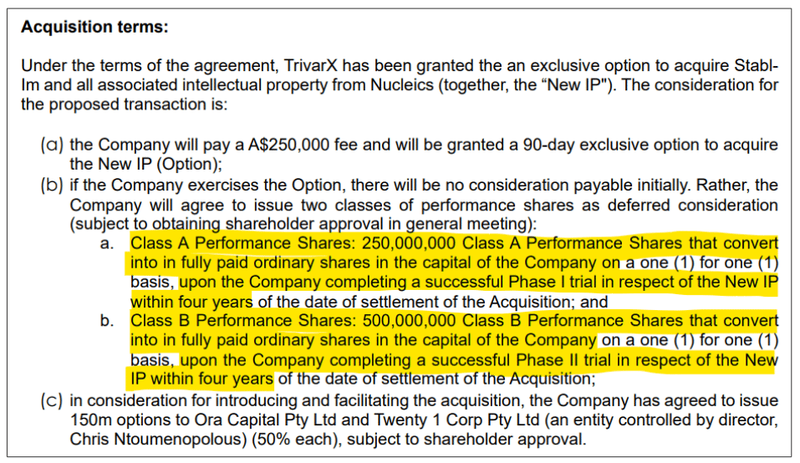

We also like that a big chunk of the acquisition payments were also all tied to clinical success.

(it’s also nice to see it’s all equity too)

Hopefully that means Dr Tillett will be motivated to see his baby be a success.

Here are those performance shares:

- 250 million shares that convert into TRI shares ONLY if TRI completes a successful Phase 1 trial within four years of settlement.

Class A Performance Shares: - 500 million shares that convert into TRI shares ONLY if TRI completes a successful Phase 2 trial within four years of settlement. Class B Performance Shares:

(source)

By the end of Phase 1 trials we think TRI could have tech that is attractive to any corporates looking to add brain tumour imaging to its portfolio.

Then by the end of Phase 2 a fairly strong idea of the commercial potential for the asset.

At that point we would assume TRI is capped much higher than what it is today.

How big is the opportunity for $30M capped TRI?

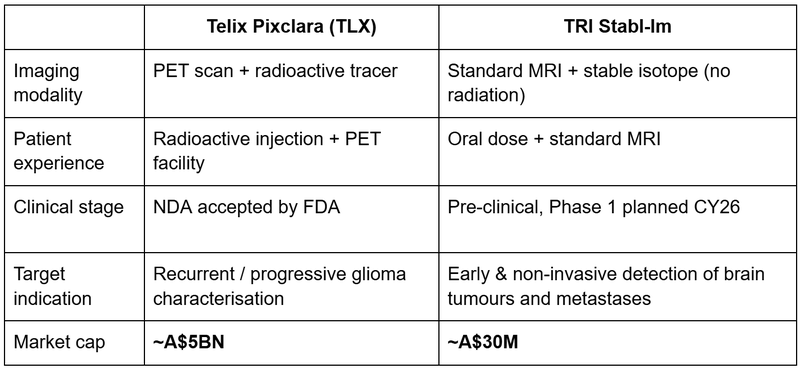

We think ~$5BN capped Telix Pharmaceuticals is a pretty good example of what success would look like for TRI.

Telix’s lead product is also a brain-tumour-imaging product.

The difference between the two technologies is that Telix’s one sits alongside PET imaging and is specifically focused on characterising recurrent or progressive tumours.

Whereas TRI’s would sit beside MRI imaging.

In April 2026 the FDA accepted Telix's New Drug Application (NDA).

So Telix is approaching commercial launch on a brain-tumour-imaging product right now.

Telix also generates ~$804M in revenue per year. (source)

Obviously this is high risk small cap investing, and it took years for Telix to get to this point, and TRI may not succeed.

Here's how TRI sits relative to Telix on the brain-imaging side:

Coming back to that image from earlier - Telix’s product is a radioactive injection that works with a PET scan.

TRI’s tech could combine the “metabolic detection” (cell imaging) of a PET scan with the safety (no radiation) of an MRI.

Obviously TRI is at a much earlier stage (pre-clinical) but the Telix story gives us a good idea of what success for a small cap like TRI looks like.

AND...

TRI just appointed Telix’s ex-Chief Medical Officer

In late April TRI appointed Dr Danielle Meyrick (PhD, MD) as CEO of TRI.

As mentioned earlier in today’s note she starts at TRI on the 1st of June (in 13 days).

Dr Meyrick was Telix’s Chief Medical Officer (APAC) and Global Head of Clinical Science between Jan 2021 and July 2022.

After leaving Telix she was Chief Medical Officer at ITM Isotope Technologies Munich - one of the global leaders in isotope-based therapeutics.

So she has spent 20+ years in radiotheranostics and isotope-based imaging - the exact field TRI’s new asset sits in now.

Dr Meyrick’s long-term performance rights are also tied to clinical success:

- Phase 1 trial in ≥30 subjects beyond imaging - OR FDA Fast Track / Breakthrough / Orphan designation

- FDA Investigational New Drug status as a brain tumour imaging agent

- Completion of a Phase 2 imaging study in ≥50 subjects within 3.5 years

- FDA Investigational New Drug status beyond brain imaging (So TRI could apply its tech to more than just brain tumours)

Her entire incentive package is built around getting TRI’s tech to a stage where it gets FDA validation.

You can check out what she had to say about TRI’s tech here:

(source)

Now that TRI’s new direction is set (into brain tumour imaging) we have put together a new Investment Memo which covers:

- What does TRI do

- What is the macro theme

- Our TRI Big Bet

- Why did we invest in TRI

- What do we expect TRI to deliver?

- What could go wrong

- What is our investment plan

- But first, here are the 8 reasons why we are Invested in TRI.

8 reasons why we are Invested in TRI

1. Dr Daniel Tillett has delivered in the past for ASX investors - we are backing him again here

Dr Daniel Tillett is the inventor of TRI's new tech (Stabl-Im) and the CEO & Managing Director of ASX-listed Racura Oncology (ASX: RAC) - currently capped at ~A$400M+.

Tillett put $500k of his own money into TRI at 0.8c per share to fund the Stabl-Im acquisition.

He is also signed on as ongoing technical advisor through the clinical program.

Past performance of Racura Oncology is not and should not be taken as an indication of future performance of TRI.

2. Same backers behind our 2025 Biotech Pick of The Year

TRI shares board members and major shareholders with our 2025 Biotech Pick of the Year - Island Pharmaceuticals (ASX: ILA).

ILA is up 163% from our Initial Entry Price.

Dr Daniel Tillett (ILA’s biggest shareholder) is also a major shareholder in TRI AND vended in TRI’s new tech.

Chris Ntoumenopoulos is director of both TRI and ILA and he was part of the team that sold Resapp to pharma giant Pfizer for $180M.

These two are part of the same team driving ILA, our 2025 biotech Pick of The Year.

3. Brain-tumour imaging that could be a game changer

TRI’s tech uses stable (non-radioactive) isotopes to label replicating cells in the brain which can then be detected using standard MRI.

5-year survival for cancers that move from one part of the body into the brain is 6.1%, compared with 71.5% for cancer patients where the cancer never reaches the brain.

Current standard-of-care MRI imaging can only detect tumours once they reach 2-3mm - by which point the tumour is already structurally established in the brain.

There is no approved non-invasive imaging method capable of identifying tumour cell replication at high levels of sensitivity. (source)

TRI’s tech (IF it works) will be able to solve that early detection problem.

4. The ASX understands these stories.

The ASX has a strong history of pricing breakthrough diagnostic / imaging biotechs.

Telix Pharmaceuticals was a favourite amongst small cap investors, IPO’ing at $50M at 65c per share in late 2017 and peaking near $32 in early 2025 at a cap of ~$10.7BN.

Another one was Clarity Pharmaceuticals which IPO’ed at $358M at $1.40 per share in 2021, peaking near $9 in 2024 at a cap of ~$3BN.

So the ASX understands and is willing to re-rate companies that have success in this space.

5. A peer comp is approaching a ~$5BN market cap

~$5BN Telix Pharmaceuticals has its brain-tumour-imaging product Pixclara which has received both Fast Track and Orphan Drug designations from the FDA

The FDA accepted Telix’s New Drug Application (NDA) and should be making a call on approvals before the end of the 2026

We think that validates the regulatory pathway for TRI.

AND it shows how the market may value a company developing brain tumour imaging tech successfully.

Past performance of Telix is not and should not be taken as an indication of future performance of TRI.

6. TRI just appointed Telix’s ex- Chief Medical Officer

Dr Danielle Meyrick (PhD, MD) starts as CEO on 1 June 2026.

Previously Chief Medical Officer (APAC) and Global Head of Clinical Science at Telix Pharmaceuticals (ASX: TLX, ~A$5BN).

Before that, CMO at ITM Isotope Technologies Munich (a global leader in isotope therapeutics).

We think Dr Danielle has the right CV to advance TRI’s tech.

We also like that all of her incentives are tied directly to clinical & FDA milestones.

7. Small market cap relative to addressable opportunity

TRI's market cap is currently ~A$30M.

The neuro-oncology diagnostic market was ~US$650M in 2025. (source)

The bigger market is for treatments when cancer moves from one part of the body into the brain (brain metastases).

That market is forecast to be ~US$8.5BN by 2035.

So an early detection tool could be valuable both in diagnostics and for companies providing treatments.

8. Free hit on TRI’s AI for detecting Current Major Depressive Episodes.

TRI still has its AI algorithm for detecting current Major Depressive Episodes (cMDE) using sleep data (MEB-001).

TRI is looking to commercialise the tech right now.

IF anything comes from this it will be an added bonus for us.

Ultimately, we are hoping a combination of the eight reasons above contribute to our TRI Big Bet as follows:

Our TRI Big Bet:

"TRI re-rates to a $300M+ market cap on successful clinical trial progress for its cancer diagnostics IP, and/or is acquired for multiples of our Initial Entry Price."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including clinical trials, commercialisation and regulatory risks - just some of which we list in our TRI Investment Memo (see below).

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Our NEW TRI Investment Memo

Date opened: 19-05-2026

Shares held: 23,820,000

What does TRI do?

TrivarX (ASX:TRI) is developing cancer diagnostics IP.

TRI's technology uses stable isotopes to label replicating cells inside the brain (the type of cells that help identify cancer) - detectable via standard MRI.

What is the macro theme?

Finding cancer early.

5-year survival for cancers that move from one part of the body into the brain is 6.1%, compared with 71.5% for cancer patients where the cancer never reaches the brain.

Current standard-of-care MRI imaging can only detect tumours once they reach 2-3mm - by which point the tumour is already structurally established in the brain.

There is no approved non-invasive imaging method capable of identifying tumour cell replication at high levels of sensitivity. (source)

We are Invested in TRI to try and develop a solution.

Our TRI Big Bet:

"TRI re-rates to a $300M+ market cap on successful clinical trial progress for its cancer diagnostics IP, and/or is acquired for multiples of our Initial Entry Price."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including clinical trials, commercialisation and regulatory risks - just some of which we list in our TRI Investment Memo (see below).

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

8 reasons why we are Invested in TRI

- Dr Daniel Tillett has delivered in the past for ASX investors - we are backing him again here

- Same backers behind our 2025 Biotech Pick of The Year

- Brain-tumour imaging that could be a game changer

- The ASX understands these stories.

- A peer comp is approaching a ~$5BN market cap

- TRI just appointed Telix’s ex- Chief Medical Officer

- Small market cap relative to addressable opportunity

- Free hit on TRI’s AI for detecting Current Major Depressive Episodes.

What do we expect TRI to deliver?

Objective #1: Phase 1 human safety trial

We want to see TRI’s tech tested in patients with confirmed brain tumours, to demonstrate safety, imaging precision, and reliability.

Here are the milestones we are tracking:

🔲 Complete trial design

🔲 Manufacture stable isotope compounds

🔲 Animal efficacy studies & results

🔲 First-in-human dose

🔲 Phase 1 trial completed

🔲 Phase 1 trial results

Objective #2: Phase 2 Imaging Study

Assuming phase 1 is successful we want to see TRI run a phase 2 imaging study.

Milestones:

🔲 Phase 2 study design

🔲 Phase 2 trial commencement

🔲 Phase 2 trial completed

🔲 Phase 2 results published

Objective #3: FDA Regulatory Pathway

While the trials happen we also want to see TRI go through the regulatory process with the FDA.

Milestones:

🔲 Pre-IND (Investigational New Drug) meeting with FDA

🔲 IND application submitted

🔲 FDA approved IND for TRI’s tech

🔲 (bonus) FDA Fast Track / Breakthrough / Orphan designation

Bonus objective - Commercialisation & Strategic Outcome

We don’t really have a timeframe for this one but ultimately, a big win for our Investment in TRI would be to see a re-rate through either a takeover or a licensing/partnership deal.

Milestones:

🔲 Licensing or partnership discussions with global imaging / pharma majors

🔲 Strategic investment from a bigger company or an outright takeover.

What could go wrong?

Clinical trial risk

TRI’s new technology is pre-clinical.

There is no guarantee that Phase 1 delivers safe, well-tolerated dosing - OR that any subsequent Phase 2 trial delivers statistically significant efficacy. Many pre-clinical biotechs fail at first-in-human studies.

Regulatory risk

FDA approvals are not guaranteed. The agency may require additional data, longer studies, or different trial designs. Adverse outcomes from regulators could materially hurt the TRI share price.

Funding & dilution risk

TRI is pre-revenue. Phase 1 / Phase 2 trial costs typically run into millions of dollars per program. Additional capital raises are highly likely and may dilute existing shareholders, potentially at a discount to prevailing share prices.

Market risk

Speculative biotechs are highly sensitive to broader market sentiment. If the biotech sector or small-cap sentiment sells off, TRI's share price could drift regardless of operational progress.

IP / Patent risk

The IP being acquired covers "all intellectual property associated with novel brain imaging technology, the Stabl-Im metastatic brain technology." There is no specific patent number or jurisdiction reference in the announcement - investors should not assume granted patents in all major markets.

Other risks

Like any small-cap healthcare technology company, TRI carries significant risk, here we aim to identify a few more risks.

First, because the newly acquired Stabl-Im technology is entirely pre-clinical, there is an inherent risk that upcoming Phase 1 trials may fail to demonstrate human safety.

Any negative trial data or unexpected toxicity could halt development before the platform ever reaches commercial viability.

The company also faces intense adoption and commercialisation hurdles even if the technology achieves regulatory clearance.

Navigating medical sales cycles and competing against established giants like Telix Pharmaceuticals means capturing commercial market share is far from guaranteed.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our investment plan?

Our Investment Plan for TRI is to hold on to a majority of our position to see the company execute on its business strategy over the next two to three years.

If the company’s share price materially re-rates in the medium term due to the results of the Phase 2 clinical trial results, a commercialisation deal, a macro triggering event or any other reason, we may look to sell up to ~20% of our holding. See our general hold policy for more details.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.