Is Top Coking Coal Contender PDZ Gunning for a Take Over?

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Prairie Mining’s (ASX |LSE | WSE: PDZ) resource of choice is high-grade coking coal, to be supplied to industrial steel manufacturers and other industrial users that are driving prices compared to standard thermal coal – primarily in Europe.

There is good reason for PDZ’s entry into European coking coal market.

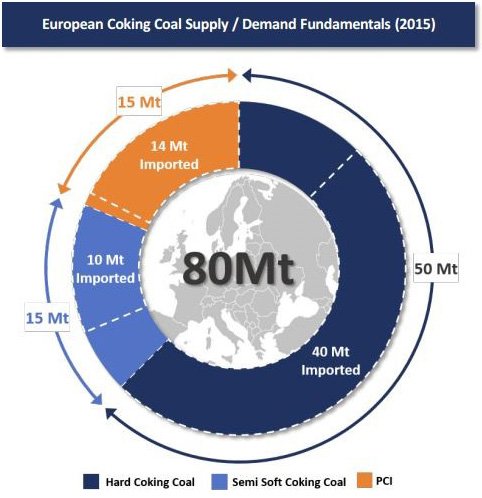

Not only has the European Union determined Coking Coal to be its 2 nd most Economically Important Critical Raw Material, but Europe imports 85% of its coking coal from abroad – including locations as far flung as Australia, USA and Russia.

In other words, the market for coking coal is currently a substantial one and this emerging tier one coking coal company is looking to capitalise.

If it can capitalise, PDZ is likely to put itself in the crosshairs of major companies who are finding it increasingly more difficult to acquire Tier 1 coking coal assets.

This was evident in South32’s abandoned plans to acquire Metropolitan Colliery for $AU265 million (£152.3 million).

The acquisition was abandoned after the Australian Competition and Consumer Commission said the deal would “significantly lessen” competition in the supply of coking coal to Australian steel makers.

So what is clear is that South32 are chasing attractive coking coal assets – but making a winning acquisition is not easy.

Could it be that some of the major miners might come knocking on PDZ’s door one day?

What could set PDZ apart and make it attractive to potential suitors is the project economics it has to propel it forward and its European location.

However, it should be noted that with all operations of this type, success is no guarantee. You should consider your own personal circumstances before investing, and seek professional financial advice.

PDZ has all the attributes to make its projects world class Tier 1 coking coal projects and itself a Tier Coking Coal producer.

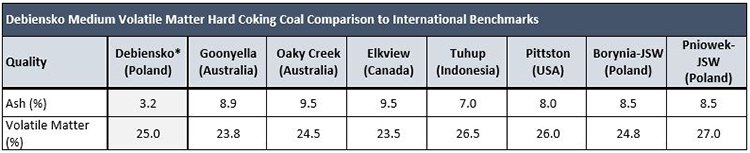

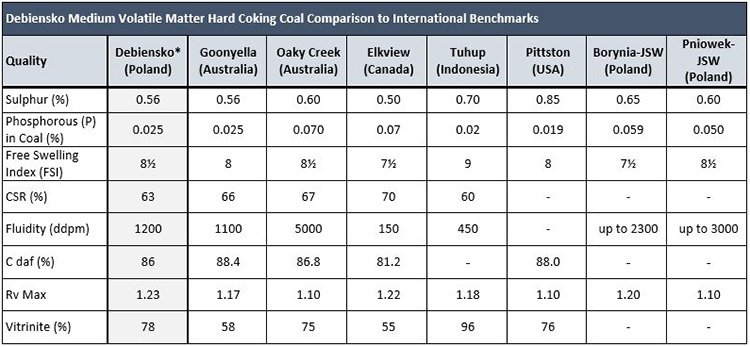

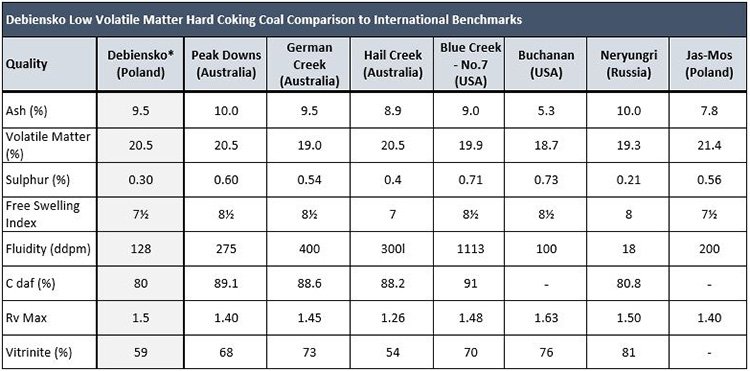

As you can see by the table below its Debiensko and Jan Karski Projects stack up better than any of its peers.

PDZ has multiple tier one coking coal projects, a combined NPV of US$3.3BN (pre-tax) and projected annual EBITDA of $US630 million.

And what a great place to be for a coking coal producer.

Europe consumes over 75Mtpa of coking coal per year of which 85% is imported.

Clearly Europe needs an internal supplier to keep costs down and PDZ looks to be smashing producers in other regions out of the park by being the lowest delivered cost supplier of hard coking coal into Central Europe.

Having completed a successful equity raise which has brought several high quality shareholders to the register and put over AU$7 million in the bank, the chatter rooms have lit up.

Could PDZ be ripe for a takeover?

Without further ado, we update you on:

![]()

LSE:PDZ

WSE: PDZ

We’ve been hot on the heels of Prairie Mining (ASX|LSE|WSE: PDZ), since we first brought our readers the story in the article Could this Emerging Stock Deliver a Major European Coking Coal Hub?

This AU$90 million/ £51 million capped coking coal miner is proving to be a solid performer amongst a flock of aspirational small-cap mining companies.

Check out PDZ’s recent market performance – up by over 300% over the past 12 months:

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

A number of UK analysts have covered PDZ, with price targets at multiples of PDZ’s current $0.55 share price, with Cenkos being the most bullish, targeting a share price at a 280% premium to PDZ’s current price:

However, a word of caution, analyst targets are never a guarantee to come true, so invest with caution and not simply on an analyst recommendation alone.

Let’s go through some of the elevational factors supporting PDZ’s chances of moving into production and generating cash flow in Europe

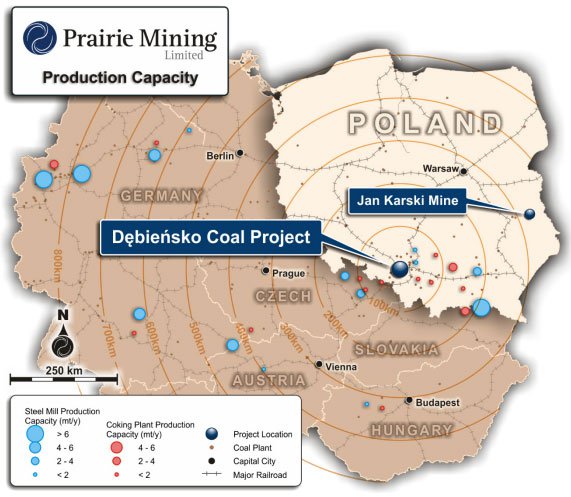

As we mentioned in the introduction, PDZ has two prime avenues to coal-market commercialisation both located in Poland: Debiensko and Jan Karksi.

At PDZ’s other primetime project (Debiensko), PDZ has recently received a freshly completed Scoping Study...

...indicating that the lowest-cost coking coal could soon be hitting European markets.

Here are all the details tabled:

Debiensko’s premium hard coking coal will have large pricing and cost advantages when selling to steel makers across Central Europe and wider EU. For PDZ, this represents its bread-and-butter source of revenues over the coming years.

Yet, how much of the market PDZ would be able to attract remains to be seen and as such investors considering this stock for their portfolio, should seek professional financial advice.

Despite the fact that PDZ is still working through technical studies and economic viability considerations, the current estimated cost to deliver coal from Debiensko stands at US$4.60 per tonne — a price level that provides PDZ with a superb cost advantage compared to imported hard coking coal.

If all that wasn’t enough, PDZ also has independent estimates confirming strong feasibility:

The highlights of the report include an edge in PDZ’s project economics. While Australian, US and Russian coal runs up costs of around $26-$38 per tonne (depending on the source), PDZ is aiming for a delivery cost of US$4.60 per tonne — a whopping 7x cheaper compared to Australian coal imports at around $38 per tonne.

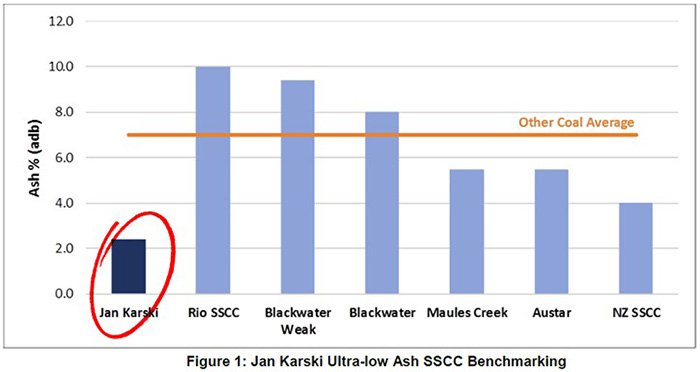

And what about Jan Karski?

Jan Karski has already been confirmed to have robust project fundamentals including producing over 6Mt a year of semi soft coking coal and thermal coal at an average cash operating cost of US$24.96 per tonne.

...that would be the lowest cash cost for coal delivered into Europe, period.

The Jan Karski Mine is a large scale premium quality coal project with a current JORC Resource Estimate of 728Mt spread across four coal exploration concessions.

Here is PDZ’s Jan Karksi site laid out and mapped in greater detail — pay particular attention to the swathe of historical drill holes (yellow dots), PDZ’s new concession area (blue dotted line) and PDZ’s very-own drillholes (red dots).

And here are the all-important figures, independently sourced and verified:

The results of an enhanced coal-quality analysis program indicate a strong likelihood PDZ will be able to produce high-value low-ash coking coal with a 75% product yield.

Furthermore, boreholes drilled in recent weeks suggest PDZ could achieve a 10% premium to international SSCC benchmark prices, due to several superior qualities.

One other very noteworthy point for early investors, is that PDZ’s work at Jan Karski is being heavily supported by China Coal. China Coal is a $10 billion goliath (China’s second largest coal miner) that builds more coal mines than the rest of the world’s coal developers combined.

China Coal has built more than 300 major shafts around the world, including shaft sinking at Vedanta’s Sindesar Khurd Lead-Zinc Mine in India .

PDZ has signed a provisional agreement with China Coal that will see the two companies complete a BFS at Jan Karski by mid-2017.

This is in order to entice a consortium of Chinese banks to fund the project further into infrastructure construction and eventually, coking coal sales.

This is the kind of aspirational targets we like our small-cap stocks aiming for in earnest.

But to ensure both Debiensko and Jan Karski make it past the finish line of steady production (and sales revenues), PDZ’s supply of project funding must be in order.

On this front, PDZ is not wasting any time.

PDZ has just attracted a further AU$2MN ((GBP1.1MN) in funding from a “cornerstone investor” otherwise known as ‘CD Capital’, and has hauled in a further AU$5.2MN (GBP2.99MN) from existing institutional investors in the UK.

As we said earlier, both the retail and institutional market contingents seem to like this stock; PDZ is currently listed in three different territories globally, which is a great sign from a funding perspective.

The circa AU$7MN (GBP4.02) in additional funding will accelerate both of PDZ’s current coal projects, and could potentially shorten the time to PDZ seeing its first trickle of sales revenues.

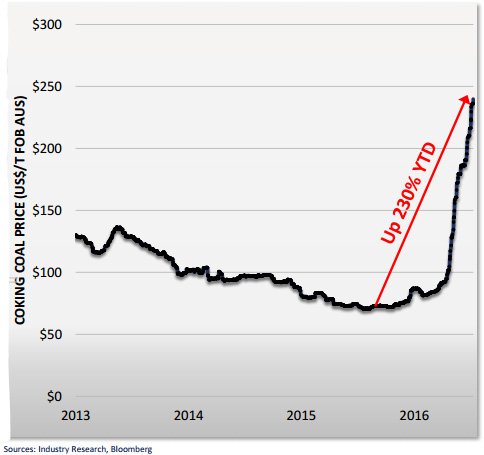

If we take a brief look at the global coal market, we can see it’s simmering to a boil

Coal is undergoing what several other commodities are with regards to price dislocation according to grade and quantity.

Whereas thermal coal prices remain weak due to plentiful supplies and low demand...

...coking coal (or metallurgical coal) is benefitting from a supply gap globally and growing demand from the major industrial regions such as Europe and Asia.

Yet commodity prices do fluctuate both ways, and caution should be applied to any investment decision here and not be based on spot prices or predictions alone. Seek professional financial advice before choosing to invest.

These market dynamics suit PDZ down to a tee and could put it in the crosshairs of major players looking for a tier 1 acquisition.

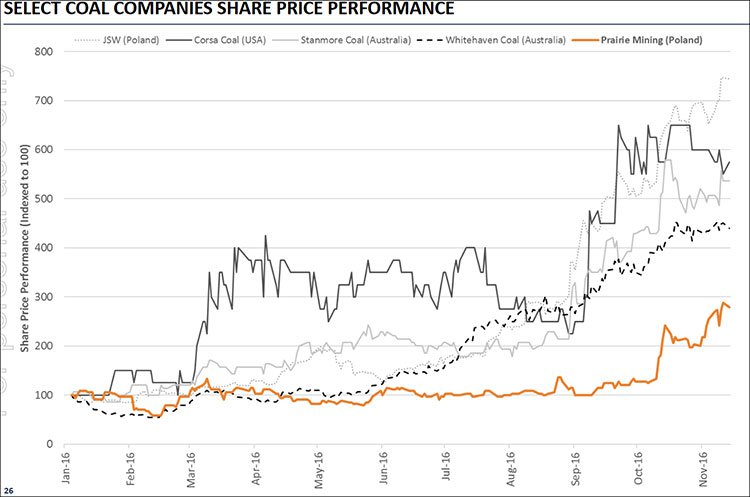

If we also have a gander at what some of the other coking coal market players are up to, it’s clear that the big boys are also sniffing around for opportunities:

But what could explain the surge in coking coal?

It may have something to do with the fact that coking coal is a non-substitutable commodity, which means there are literally few alternatives when it comes to making steels, alloys and carrying out specialised metallurgical processes which require carbon-rich coal.

The bigger point to make here, is that coking coal is quickly engendering itself with the parallel boom in lithium/zinc/cobalt demand.

Why?

Well, you didn’t think all those flashy electric cars and glitzy gadgets could be manufactured into reality without a huge lift in steelmaking (the largest component of cars, construction and infrastructure-building which is now rampant globally.

You can thank the protectionism that’s seems to emanate from all G20 countries, for the sharply higher steel-consumption estimates.

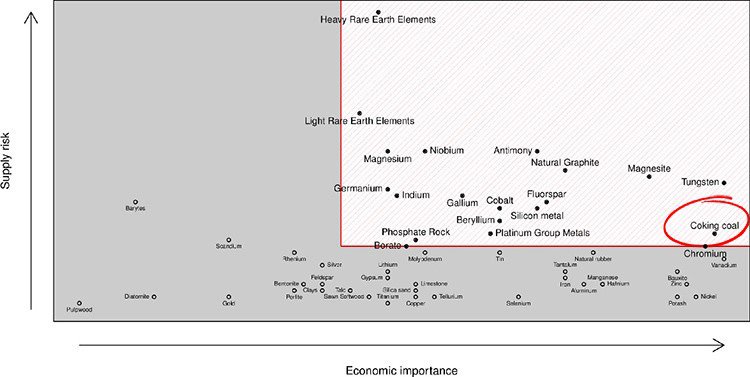

Here’s how coking coal stacks up to other commodities when considering ‘supply risk’ in proportion to a commodity’s ‘economic importance’.

As you can see, there are some commodities that are considered essential for global economic activity, which includes coking coal, tungsten and chromium.

Peer-to-peer comparison

To give you an indication of PDZ’s market position, in relation to some of its larger peers, take a look at this chart showing PDZ’s projects ranked according to vitrinite content and coal quality:

PDZ’s Jan Karski and Debiensko Projects are nestling nicely in amongst projects belonging to much larger industry names such as Rio Tinto and BHP Billiton — but with the advantage of being more cost-effective.

With PDZ’s market momentum continuing to grow, now could be a good time to look ahead for upcoming catalysts

First off, PDZ plans to commence a focused in-fill drill program to increase JORC measured and indicated resources to support future feasibility studies for Debiensko.

Soon after, the plan is to deliver a re-engineered mine plan to produce a feasibility study to international standards with a focus on near term production at Debiensko.

After that, there will only be offtake deals to negotiate and sales agreements to sign.

At Jan Karski, PDZ’s relationship with China Coal is the pivotal factor that is likely to determine future project progress and PDZ’s valuation over the coming months.

On this front, we are quietly confident that China’s second largest coal development company worth US$9BN will assist PDZ with any potential hurdles, and ensure it will offtake all of PDZ’s production.

China is desperate for access to high-quality coal, both close to its own domestic smelting industry, but also, lining the Silk Road on which China plans to traverse on its destination to paving its long-term economic supremacy.

China Coal has agreed to take Jan Karski through to the BFS stage, and then work to secure the necessary project funding to bring Jan Karski online at high rates of annual production. According to PDZ, the Jan Karski BFS will be published later this year, showing detailed project economics and feasibility, and very importantly for investors, could heighten PDZ’s valuation.

This Little Prairie is gunning for a big house

We’ve said it before, and we’ll say it again.

In order to haul abnormal returns in today’s uber-competitive commodity markets, small-cap players like PDZ may just be the ticket.

PDZ is on course to bring online two of the lowest cost coking coal mines in the heart of Europe’s steel industry.

The broader story here is not just PDZ’s ability to be prolific in its exploration. What’s also adding to PDZ’s market momentum is its long-term plan of mining its Eastern European haven for the next 20-30 years — that’s just a simple indicator of the potential locked up in Poland.

Europe’s demand for coking coal and steelmaking continues to grow, with around 85% (40Mt) of coking coal having to be imported each year.

If PDZ can alleviate Europe’s need for overseas coal, it will likely stand to benefit from the strong margins already being seen in sales negotiations between existing producers/consumers.

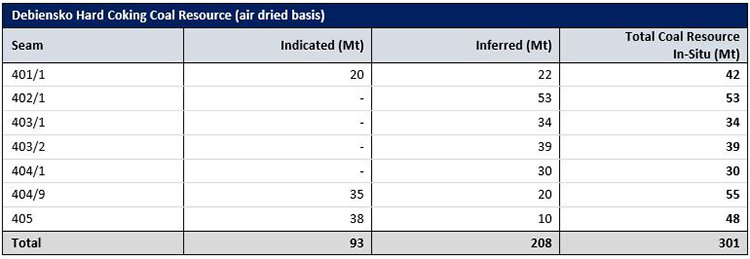

PDZ has a Maiden Coal Resource Estimate of 301Mt comprising of 93Mt Indicated and 208Mt Inferred coal resources

Seeing that PDZ has literally sandwiched itself right in the middle of converging macroeconomic, geo-political, microeconomic and energy-security themes — suggests that PDZ is well positioned to potentially make good on its long-term promises to investors.

Already, PDZ wields comparable projects, locations and economics to much larger peers, but has the trump-card of potentially blossoming into one of the lowest-cost coal producers anywhere in the world; beating even ultra-low-cost regions such as Russia and China – who benefit greatly from state funding and protectionist measures we might add.

If PDZ can cut the mustard in its own right, by its own merit, and at the currently lucrative time when coking coal sales agreements are being renegotiated for the next cycle...

... what could PDZ’s potential reach, once all its infrastructure is factored in and the final viability jigsaw puzzle-pieces fall into place?

PDZ is a company with a fine blend of superficial allure and below-the-surface substance, yet to be discovered and commercialised to its full extent. But with coking coal making a swift comeback, PDZ is on course to potentially impress market analysts over the coming years.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.