Tell me more: SS1 hits +100m of higher grade silver… new high grade extension?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,898,291 SS1 shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time.

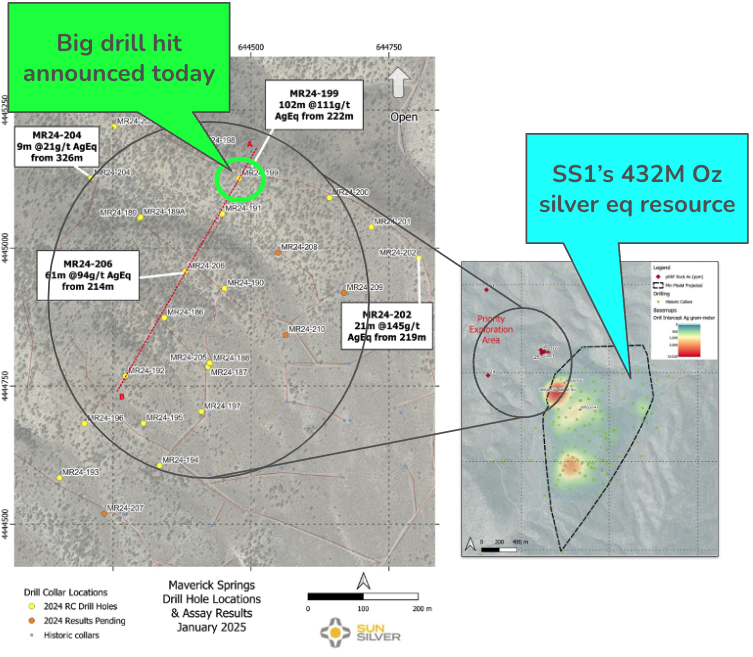

Our 2024 Small Cap Pick of the Year Sun Silver (ASX:SS1) just hit 102m of silver at an average grade of 111g/t silver equivalent.

This drill hole is part of SS1’s first drill campaign to expand its existing 423Moz silver equivalent JORC resource.

And it was at one of the furthest out extensional drill holes from the existing silver resource...

...which might mean the start of a new and high grade silver extension to SS1’s already huge silver deposit.

Next we want to see more follow up drilling to follow this new potential high grade extension:

Finding a new high grade body near an existing JORC resource can and does happen.

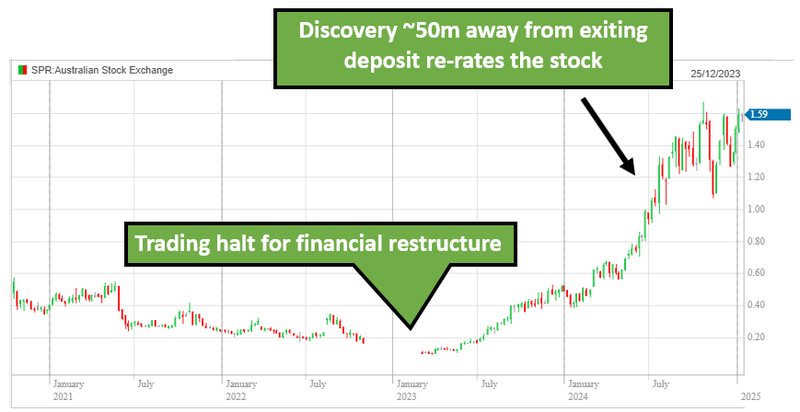

In 2022 Spartan Resources (the old Gascoyne, for anyone who remembers) decided to drill ~50m away from its existing JORC resource (which had been producing gold for years).

Spartan made a new high grade discovery, taking it from 10c to $1.59 and is now capped at ~$2BN.

So while SS1 already has a giant silver resource, today’s new high grade hit has confirmed some additional blue sky potential for SS1.

Next we want to see SS1 drill test this new, potential high grade silver extension.

Silver is part of the global uncertainty thematic we are interested in for 2025.

Silver and gold are precious metals - they are generally seen as “safe haven” investments in times of global uncertainty or war.

We already saw the silver price deliver and hold onto a material increase during 2024 when global uncertainty started ramping up.

SS1 responds well to a rising silver price.

TD Securities’ Senior Commodity Strategist Daniel Ghali recently said the market is “sleepwalking into a silver squeeze” - more on this later.

Another commodity that fits our global uncertainty thematic is called antimony.

Antimony is used in military applications.

The USA has no local supply, and last month China enacted an export ban on antimony.

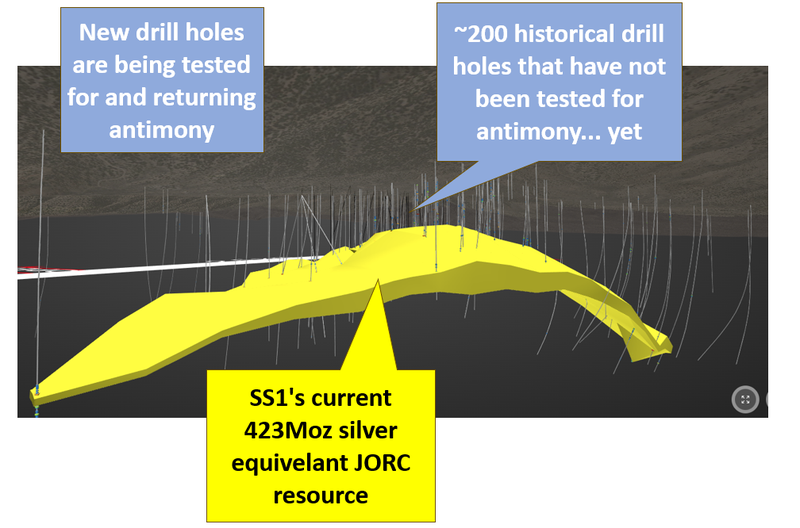

SS1 has been testing for and hitting antimony in its NEW drill holes...

SS1’s giant 423Moz silver equivalent JORC resource is made up from ~200 historical drill holes - that were tested for gold and silver but NOT for antimony.

SS1 has already initiated a project wide review of all the old drillcores to see if its project hosts an antimony resource to go with its already huge silver/gold resource.

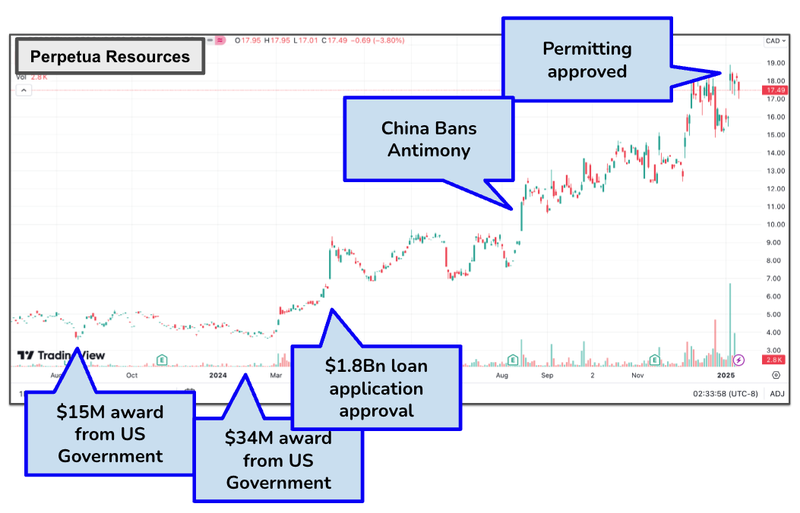

One project with an antimony angle that piqued our interest was the gold project owned by TSX listed $1.2BN Perpetua Resources.

The US Department of Defence has been very involved in Perpetua’s project, providing US$59M in funding and supporting the project through applications and a $1.8BN loan.

Our thesis is pretty simple - IF SS1 can define an antimony JORC to go with its silver resource then we would hope it opens doors for funding and faster permitting.

(and hopefully a whole new swathe of investors)

This year we want to see SS1 move to a market cap and daily volume that is big enough to meet the minimum standard for large funds to invest in SS1.

(SS1 already managed to attract a major US fund, Nokomis, onto their register last year)

Ideally we think above $150M market cap is going to get SS1 to a level that major funds can buy.

(SS1 is currently just under $100M)

We also want to see SS1 grow enough to qualify it to be added to a “market index”, which brings its own on market buying and support for the next leg of growth into a mid-sized company.

We saw this happen during the battery metals boom when VUL and LRS commenced price runs after their market caps and daily volume became large enough to qualify them for index funds (more on this shortly).

So how will SS1 get to the next leg up of a $150M plus market cap?

What could make the SS1 share price go up from here?

The pathway to the next leg up in the SS1 share price should come from we just need a few of these things (the more the better) to go our way:

- Silver price runs: if the silver price runs, then we expect SS1’s share price to follow. The silver price could run due to a hedge against persistent inflation or industrial demand.

- More silver discovered from drilling - after today’s assays, we think it is clear where SS1 should drill next. If SS1 can continue to build on this identified silver mineralisation, we think that it could follow a similar path as Spartan Resources - which discovered and defined a giant gold resource in a short period of time.

- SS1 silver resource update - If SS1 publishes a JORC resource update that increases the level of confidence in the project and the size of the silver equivalent resource (above investor expectations), this could be a big catalyst for the company.

- Antimony surprise: SS1 could publish an antimony resource by re-assaying historical drill cores that were not tested for antimony. On top of this, if SS1 is able to secure any US DoD funding for this project (it happened for Perpetua - more on this below) it could be a big signal to the market that SS1’s project is of ‘strategic importance’ to the US Government.

- SS1 hits market cap/trading volume requirements to get into an index: Once a company enters an index then ETFs will be required to buy up the stock and certain funds will be able to take positions in the company. This opens up a whole new market of capital that tends to be more patient and more predictable than retail investors.

A closer look at the SS1 results from today

So, the biggest primary silver deposit on the ASX looks like it's getting bigger...

SS1 just hit 102m of silver at an average grade of 111g/t silver equivalent.

102m is roughly the size of a ~35 story building...

The intercept occurred outside of the existing 423M silver equivalent JORC resource, and it was at the outer bounds of where SS1 has drilled to date:

With today’s assays, we are starting to get a clearer picture of what mineralisation has been uncovered from SS1’s drilling outside of its giant 423Moz resource.

SS1 still has 4 more assays to come that are largely infill holes that will support the confidence levels in the resource model.

SS1 is planning on putting out a resource upgrade this year.

Next, we want to see SS1 continue to drill to the northeast along this strike.

Drilling further to the northeast could unlock an entire new high-grade discovery...

It’s happened recently before - Spartan the most recent example on the ASX

This is what happened with Spartan Resources (for those who remember - the old Gascoyne Resources).

Spartan decided to drill ~50m away from its existing JORC resource (which had been producing gold for years).

In 2022, stepout drilling made a high grade discovery that changed the fortunes of the company in a huge way...

Like SS1, Spartan Resources was looking to build confidence in and grow its economic resource.

Spartan wanted to get its resource to a level that justified the re-start of its mine.

What Spartan didn’t fully expect was making a high-grade gold discovery that helped the company raise hundreds of millions from institutional investors.

Spartan Resources is now capped at $1.7BN.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

This is what can happen if a company makes a big, new, unexpected resource discovery.

Of course, it doesn't happen every day - this is speculative resource exploration and development.

After the hits from SS1’s first drilling campaign, and especially the hit announced today, we think there is continued upside potential for SS1 as it continues to drill test the resource beyond where today’s 100m intercept was struck.

An unexpected discovery of more high-grade mineralisation is the ‘dream’ when it comes to definition drilling.

We are hoping that this is what could happen for SS1 as it undertakes more drilling to the northeast of the existing and known mineralisation.

Could SS1 be a good candidate for ‘index fund inclusion’ in the near term?

A bigger pool of investors re-rates SS1 higher from its current market cap.

One way we think it can get there is by becoming a ‘defacto silver ETF’.

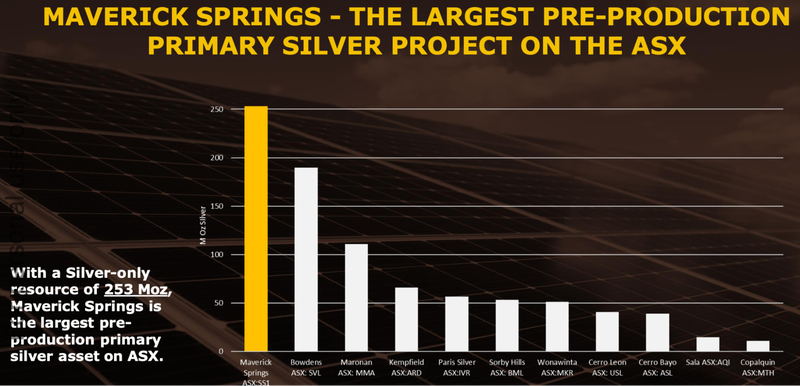

We already know that SS1’s Maverick Springs is the largest pre-production primary silver project on the ASX:

There is a premium attached to being the “biggest” of any commodity in a particular market.

In the case of SS1, it's silver on the ASX.

It means that funds and investors wanting leverage to silver (without buying the commodity itself) will ideally look to SS1 first.

So far SS1’s share price appears to be closely correlated with the silver price:

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

So we think that if the silver price runs to all time highs, SS1’s price should follow.

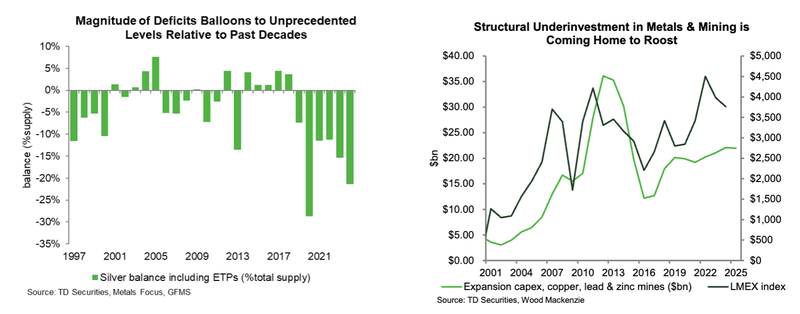

Silver Squeeze coming?

Daniel Ghali, Senior Commodity Strategist from TD Securities in Toronto recently published his latest ‘Market Musings’ on silver, titled ‘Sleepwalking Towards a #SilverSqueeze’ which we managed to see a copy of.

The note shows how there is a big supply crunch on silver that has led to silver deficits, and a big move in the silver price over the past 12 months (while investment in mine expansion remains depressed):

(Source - TD Securities)

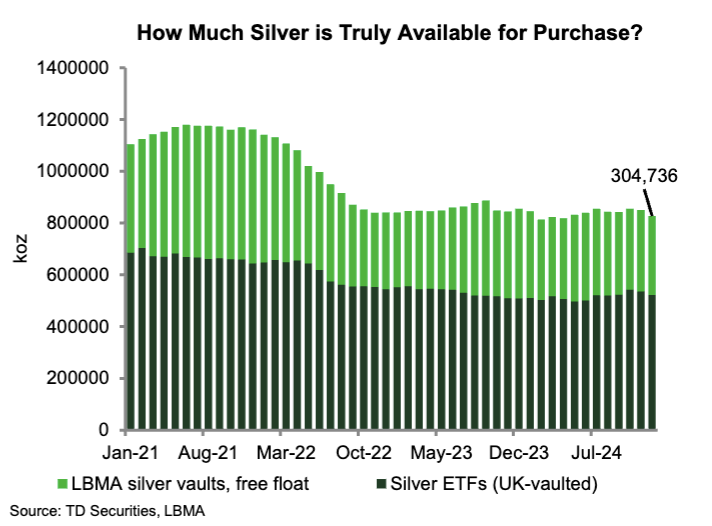

The TD Securities note goes on to show that this is combining with depleting silver inventories:

We have written about the potential for a silver squeeze before.

We think the set up is all here for a silver price rally.

This is a big part of how we think SS1 could become a “defacto silver ETF”.

Particularly if SS1 is able to secure index inclusion...

Index Inclusion - we have seen before in our Portfolio stocks

Index inclusion was something that some of our best ever resource Investments have had going into a period of strong newsflow.

AND in both cases, index inclusion happened before a big run up to all time highs for the company’s share price.

Here is where Vulcan got included in the S&P All Ordinaries index:

(Source)

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Here is where Latin Resources got included in the S&P All Ordinaries index:

(Source)

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Both of those companies started their runs to their highs off the back of index inclusion.

We are hoping that (with some more drilling luck and a silver price run) SS1 can pull off something similar.

Betting on the defence-critical minerals for 2025

We think that defence-critical minerals will be a big investment thematic for 2025.

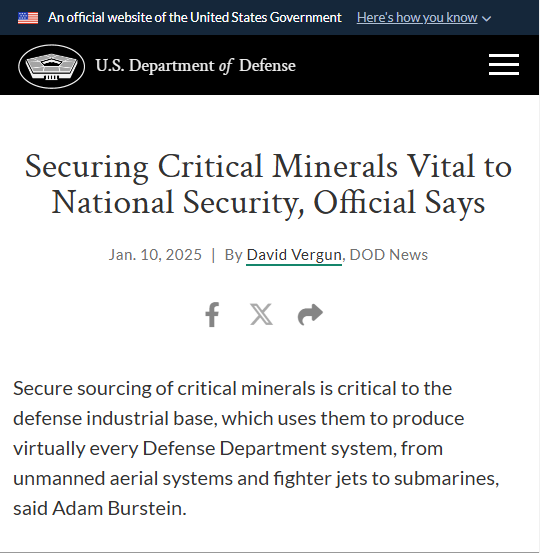

Just last week a White House Official spoke about the urgency to build "resilience in supply chains for critical minerals”.

(Source)

SS1’s project may have one of those minerals critical to the US-defence industry... antimony.

Antimony wasn’t on the radar of investors or SS1 when we first Invested in the company at the start of 2024.

But, it turned out that antimony was the best performing commodity of 2024, beating out gold and silver.

Antimony prices were up 192% in 2024 and we expect this commodity to be a big player in 2025.

So what happened?

Antimony is a critical raw material used in various military applications including ammunition.

The US has no domestic antimony supply and currently imports 100% of its antimony supply.

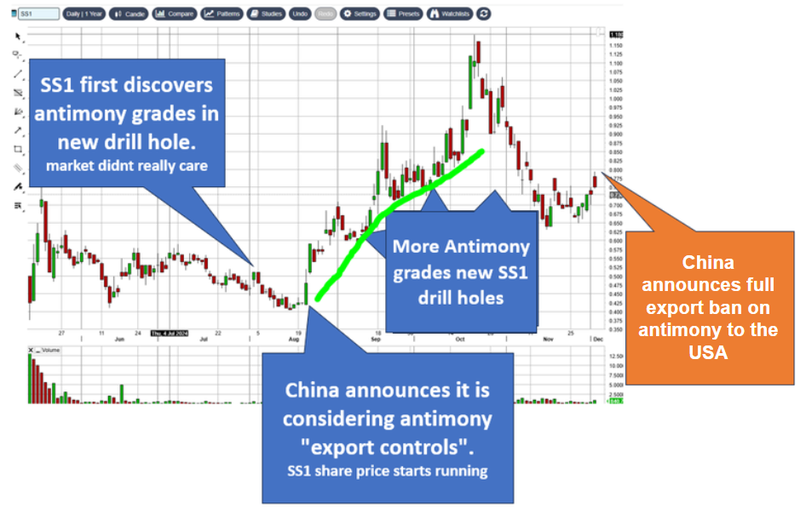

After China announced an export ban of the critical mineral, the price skyrocketed.

Just 10 hours BEFORE that ban was announced (and antimony became ‘cool’) SS1 had put out some pretty solid antimony grades from its drilling program.

We think that antimony is a mineral to watch as tensions between the US and China continue to fester under a Trump administration.

For SS1 it was a matter of right place, right time to be discovering antimony over the project:

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Over the last six months, SS1 has continued to hit solid antimony grades and initiated a project wide review of all the old drillcores to see if its project hosts an antimony resource to go with its already huge silver/gold resource.

There is only one existing antimony resource in the US, a project in Idaho which is owned by TSX-listed $1.2BN Perpetua Resources.

The CEO of Perpetua Resources recently spoke about securing final permitting for the project:

The US Department of Defence has been very involved in Perpetua’s project, providing US$59M in funding and supporting the project through applications and a $1.8BN loan.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Our thesis is pretty simple - IF SS1 can define an antimony JORC to go with its silver resource then we would hope it opens doors for funding and faster permitting.

(and a bigger pool of investors who want exposure to SS1...)

Our SS1 Big Bet

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SS1 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What’s next for SS1?

(Source)

- 🔄 Assay results from 7,500m infill/extensional drilling - There are 4 more assay results still to come. We want to see these published to get a complete picture of SS1’s resource growth potential.

- 🔄 Upgrade Resource - we want to see SS1 publish a resource update/upgrade over its project.

- 🔄 Further update on US government funding - We want to see SS1 put out an update on the US$60M grant application the company is working on for its silver paste business.

What are the risks?

In the short term, the risk we see for SS1 is “exploration risk”.

SS1 is currently running an infill and extensional drill program.

There is no guarantee that the drilling will deliver extensions OR confirm the existing mineralisation.

Exploration risk

There is no guarantee that SS1’s upcoming drill programs in Nevada are successful and SS1 may fail to find economic silver-gold deposits.

Source: “What could go wrong?” - SS1 Investment Memo 18 May 2024

The next risk is “silver price” risk.

SS1’s share price is very correlated to the silver price. Any material degradation in the silver price may negatively affect SS1’s share price.

Finally, SS1 is a resources development company, and does not generate any revenue at this point in time.

The company is reliant on raising capital (hopefully at higher and higher prices to avoid dilution to early investors) or securing government grants or partners to progress its projects.

If some of these efforts stall then the company may need to inject capital into the business at less favourable terms. This is an ever present risk for all early stage resources companies.

Our SS1 Investment Memo

For a full rundown of our investment thesis, read our SS1 Investment Memo, where we share:

- What SS1 does

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.