Stonewall releases Scoping Study results for Theta Hill Gold Mine

Published 15-OCT-2018 11:36 A.M.

|

6 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Stonewall Resources Limited (ASX:SWJ) has announced the promising results from the Theta Hill Scoping Study. The study was released today as part of the small cap’s vision of developing a pipeline of open-cut targets.

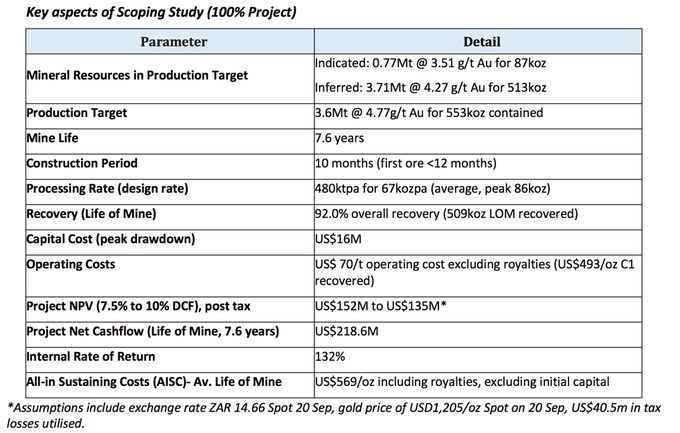

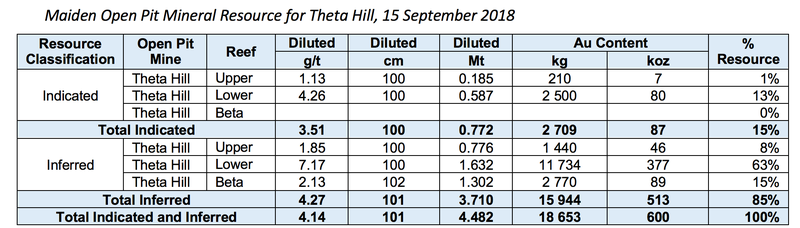

The Theta Hill scoping study shows clearly the historical mines of this goldfield have open-cut oxide gold potential. As announced by the company in September, Theta Hill contains an open-cut JORC resource of 4.48Mt at 4.14g/t gold for 600koz (Indicated & Inferred).

The company is now turning its attention to converting part of its large 5.8Moz Mineral Resource into a mining reserve. Additional drilling is underway at Theta Hill to improve the JORC confidence category to primarily Indicated ahead of reserve declaration scheduled for 1Q 2019.

Importantly, this study demonstrates the potential for annual average gold production of approximately 67kozpa for 7.6 years (509koz recovered) with LOM All-In Sustaining Costs (AISC) of approximately US$569/oz and peak capital requirement of approximately US$16 million.

Consequently, the development of the mine would have a short payback time of approximately 7.4 months and construction period of approximately 10 months. Within the parameters of the Scoping Study limitations (± 25-30% accuracy), Theta Hill shows a post-tax NPV7.5 of approximately US$152 million (approximately A$214 million) and IRR of approximately 132%.

Much of the infrastructure to restart gold production is already in place including the fully permitted tailings dam, roads, power and water. The preliminary estimate for the TGME CIL plant refurbishment is approximately US$11.1 million — this includes crushing and grinding expansion to 500Ktpa.

Other local drilling targets have been identified, which means the potential to enhance project economics through additional ounces. The next targets for drilling, outside of the immediate Theta Hill area, include Vaalhoek Open-Cut (0.62Mt at 16.9 g/t gold for 335Koz (82% Inferred, 18% Indicated) and Columbia Hill.

MD Rob Thomson commented on the news: “Our team in South Africa and Australia has been diligently working on this open-cut vision, as the first stage of a planned series of open-cut and underground developments to transform the company into a low-cost gold producer.

“We look forward to continuing to deliver on our stated commitment of delineating high grade open-cut gold deposits which can be brought into production at low cost.”

The Scoping Study was delivered by South African consultants Minxcon, and undertaken in accordance with the JORC (2012) Reporting Code.

It highlights that the previous focus on underground mining potential by past operators and miners can be examined in new light with a view to developing low cost open-cut mines, which has been the recent focus of SWJ.

Potential for Theta Hill to be ‘robust mine with low technical risk’

SWJ’s Scoping Study determined that the Theta Hill open-cut development represents a potentially robust mine with low technical risk. The strategy involves in-pit waste emplacement and strip-style mining of three gold-bearing seams using surface miners amongst standard mining equipment, including dozers, rock-breakers and minimal drill and blast.

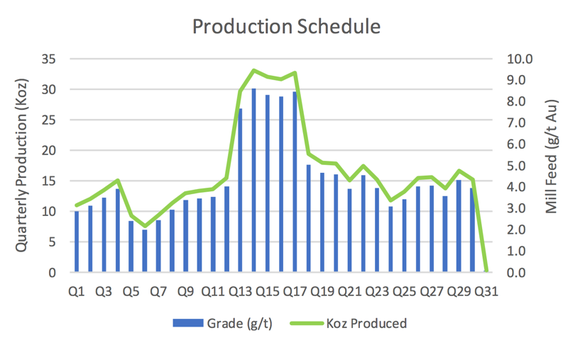

The site is situated within 2km by road of the existing, fully permitted CIL plant with a US$11.1 million capital upgrade planned. The company considers the project is potentially economically viable based on its ability to rapidly pay back project start-up capital (7.4 months from first cashflow) and potential ongoing positive operational cash flows for up to 7.6 years as demonstrated by the preliminary mining schedule.

The current mining inventory assumes 58% of ounces mined from Indicated Mineral Resources (37% of tonnes) during the first nine months of production where in excess of 35,000 ounces of gold is produced. Further, detailed monthly scheduling has been run for the life of mine.

A ratio of 83% Inferred and 17% Indicated resources were adopted in the Scoping Study model referenced in this report.

Mining and production schedule for Theta Hill Gold Mine

As per the Scoping Study, the proposed mining method for Theta Hill is an open-cast, bench style mining involving contour strip mining. The method involves progressive strip mining using a variety of standard earthmoving equipment, with surface ore miners used to extract the ore.

In the words of the company, “despite the higher strip ratio (due to the narrow gold seams) large volumes of material can be removed efficiently”. Waste is placed back in the pit once the ore is removed, and it is also planned that the rehabilitation will be progressive.

Further, the company anticipates only minimal drill and blast required at the site due to the highly broken and fractured ground. This method is anticipated to be low cost, at around US$0.90/t of ore and US$1.27/t of waste moved.

SWJ confirmed its commitment to progressing the project towards Decision to Mine (DTM) in 2019, and consequently has a full feasibility study planned. Following that, it is anticipated financing can be secured and DTM made.

The company listed the following works to be completed in coming months and into CY2019 as part of the feasibility work:

- Further drilling to upgrade areas of Inferred resources in the current mine plan to Indicated

- Additional drilling of other nearby identified areas of resource potential with a view to potentially adding to the mine plan

- Detailed design of the CIL Plant refurbishment, to within Feasibility study accuracy (±15%) ahead of commencement of plant refurbishment in 2019 (subject to financing)

- Further refinement of the mine planning work, including ore and waste schedules, with a view to maximising profitability, particularly during the first year when capital is to be repaid (assuming debt funding)

- Geotechnical and Metallurgical studies to support both the mine plan and processing design

- Studies and plans including Environmental Management Plans to ameliorate any potential impacts of open-cut mining on the local community, including water, dust, noise and traffic management

This information is general financial product advice only and you should consider seeking professional advice before making any investment decision. All indications of performance returns are historical and cannot be relied upon as an indicator for future performance.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.