SS1’s high grade antimony readings - does it run across the whole project?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,810,000 SS1 shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time.

The US needs antimony, fast.

Sun Silver (ASX:SS1) has just confirmed the presence of anomalous antimony in a number of areas of its resource in Nevada USA.

Antimony is used in infrared missiles, nuclear weapons and night vision goggles, and mostly as a hardening agent for bullets and tanks.

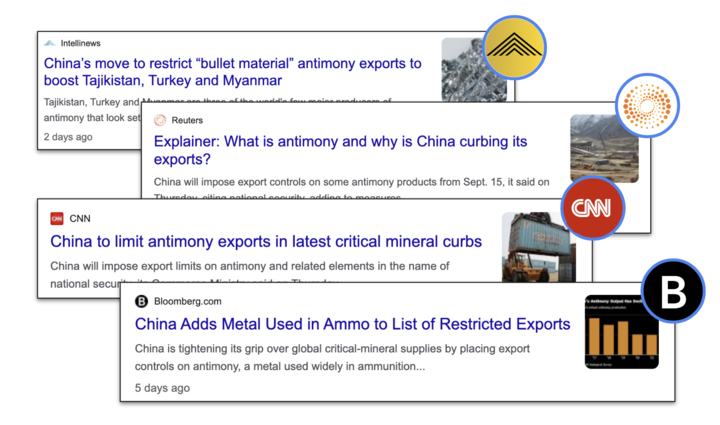

China is the world’s biggest supplier - responsible for ~63% of the world’s antimony needs.

In the USA, no domestic mining of antimony has occurred since the 1980s.

Suddenly, China has decided to restrict the export of antimony to the USA.

China's antimony export restrictions are just 5 days away from taking effect.

After 40 years of not mining any antimony, it appears that the US is very serious about its hunt for new local sources of antimony.

The DoD has already given one company ~US$60M in grants to help it build its antimony mine.

This same company has also received a ‘letter of interest’ from the US Export-Import bank to lend it US$1.8 billion to get its mine into construction and producing antimony.

(it actually happens to be a gold mine with antimony credits - this is the way most antimony is mined - we will get to that shortly...)

Even then, despite all that investment, it would only make up ~35% of US annual antimony demand and the production would only last for 6 years.

We think anyone who can demonstrate to the USA government that they have a large resource of antimony in the USA could be in the running for large amounts of funding to help build its mine.

Makes sense as to why SS1 has recently been inspecting its old drill cores for the presence of antimony...

And the best part is, it has found some.

SS1 already has a giant silver resource in Nevada USA.

It's actually the largest primary silver resource on the ASX of 432Moz of silver equivalent.

Now it's increasingly looking like SS1 could be able to pair this with a decent antimony resource - something of strategic value to the US Department of Defence.

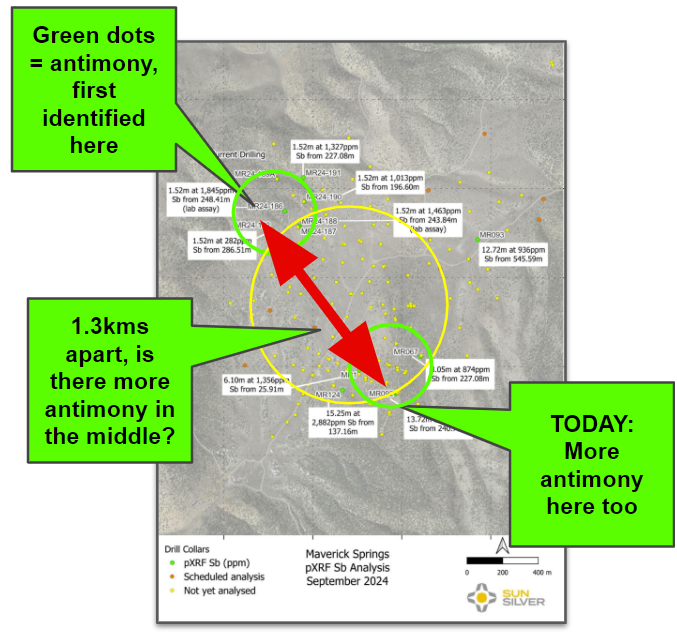

It's early days in determining just how much antimony SS1 has, but based on today’s results it appears to us that it could have antimony throughout the resource...

SS1 has antimony in the green holes below and the next batch to be tested should confirm whether or not it's widespread across SS1’s project...

The green dots in the image below have antimony in them, the yellow dots have not been tested yet and the brown dots are “scheduled for analysis”:

Only five historical holes out of ~200 have been sampled for antimony - and all delivered anomalous antimony grades.

All seven of SS1’s 2024 drillholes returned antimony, and a historical drillhole delivered a +1% grade.

The only five historic holes checked by SS1 for anything but silver and gold also returned antimony with grades as high as 1.32%.

So every single hole checked to date has returned antimony... but of course, more work is required.

And if antimony stays in vogue, and SS1 keeps finding it in its silver resource, we think this could accelerate SS1’s pathway through to development...Before we dive into SS1’s antimony news today, it's worth taking a look at the pathway an $840M capped NASDAQ / TSX listed gold company went down in recent years.

It's a clear demonstration of the US need for antimony, and the extent of funding the government can provide private companies to incentivise production.

Perpetua Resources - Can one company deliver the US all its antimony needs?

As long term SS1 Investors, we’re particularly interested in Perpetua Resources’ ability to secure non-dilutive funding from the US Government for the development of its project.

Government grants and loans), are extremely valuable to developers like SS1 and Perpetua because it more rapidly pushes these companies towards production.

Government assistance has the potential to shorten the period that a developer spends in the “securing funding” doldrums, and can lead to quicker re-rates.

Perpetua Resources is a model for what we’d like to see SS1 achieve, now that there is clear evidence that antimony can attract US Government funding.

In April this year, Perpetua Resources received a letter of interest from the US Export-Import Bank for a US$1.8BN loan over its giant gold project which just so happens to have a significant amount of antimony in the US.

If the loan is finalised, Perpetua can then use this money to build its mine.

It can also show off its letter of interest to “would-be financiers” as evidence of the merits of its project.

This comes off the back of almost US$60M in funding provided to Perpetua by the Department of Defence over the last two years.

So far, Perpetua Resources has received:

- $24.8M in funding from the Department of Defence under the DPA Investment Program to support environmental and engineering studies in 2022.

- $34.6M in 2024 under the Defense Production Act designed to support construction readiness and environmental activities on this mine.

- $1.8BN letter of interest for a loan from the US Export-Import bank to construct the mine.

This grant and funding support has meant that the US government has effectively taken this gold mine and fast tracked it through to becoming production ready.

... all for the antimony byproduct it will produce?

It seems odd that the Department of Defence would dish out so much money to a gold project, but such is the strategic nature of antimony to the US.

Right now, it is slim pickings, but the US desperately wants more supply.

In a 2022 report, the U.S. House Armed Services Committee said it "is concerned about recent geopolitical dynamics with Russia and China and how that could accelerate supply chain disruptions, particularly with antimony."

So, antimony is at the top of the priority list... and SS1 has some.

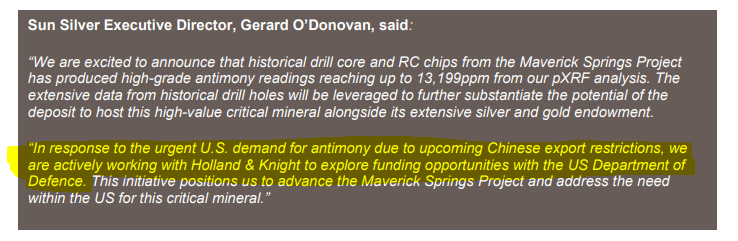

In today’s announcement we learnt that SS1 is looking at “potential funding avenues with the Department of Defence in response to the urgent demand for antimony in the U.S”.

Hopefully that means SS1 is putting itself in front of the right people to try and get funding for its project, similar to the deals signed by Perpetua.

The main problem we see is Perpetua’s mine (once in production) would only make up ~35% of US annual antimony demand AND the production would only last for 6 years.

If the Department Of Defence is serious about securing domestic antimony supply it will need to look at helping a few other projects off the ground.

Following this logic, we would expect the DoD to place a number of bets on US-based projects that make financial sense on their own BUT can also produce antimony.

Perhaps SS1 can be one of them...

Perpetua’s share price rally coincides with DoD funding

Before the Department of Defence came knocking, Perpetua Resources was just another advanced gold/silver project in the US looking to lock in a big project financing package to get its project off the ground.

In August last year the company got its first tranche of cash from the DoD, then in February of this year another tranche and then finally in April this year, the US$1.8BN loan commitment.

Over that period we have seen Perpetua’s share price go from a low of ~US$2.50 per share to trade at close to ~US$8.50 per share...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

IF SS1 can get its hands on some funding from the US government, we are hoping it can generate some additional momentum into SS1’s share price, like we saw with Perpetua.

Ultimately, we think that as SS1 clears the pathway to getting its project developed, its valuation should move higher - assuming silver prices are strong.

That forms the basis for our SS1 Big Bet which is as follows:

Our SS1 Big Bet

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SS1 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why we think the antimony adds to an already strong project

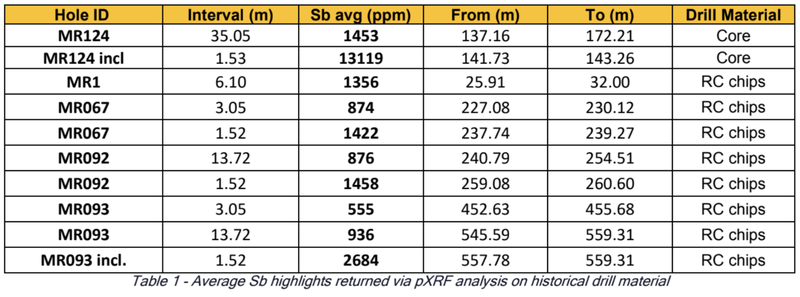

Today, SS1 published the XRF results of five historical drill holes for antimony.

Each one of these holes had antinomy.

SS1’s project contains over 200 historic drill holes, which makes up its giant 432Moz silver equivalent resource.

These holes are currently sitting a core shed facility near the site:

As soon as the company identified antimony in a step out hole, it decided to test some of the old holes in the core shed, and here’s where it has confirmed antimony:

It's still early days, but as it stands it looks like the antimony could be present across SS1’s deposit. More holes need to be sampled though.

Here is a table of best antimony grades from the holes tested:

These results are validation of the theory that SS1’s giant silver deposit contains anomalous antimony.

To further progress the “antimony” story, the company will need to invest in re-assaying many more drill cores in the core shed to identify exactly how much antimony it has and where it exists.

There is a chance that the US Department of Defence may support in funding this work, as it did with Perpetua Resources...

We’ll have to wait and see on this front but SS1 says that US law firm Holland & Knight is supporting its application funding activities.

We think SS1 will need to do more evaluation on its project to answer that question with more clarity but we think that these results are a good starting point.

SS1’s project in the right place at the right time...

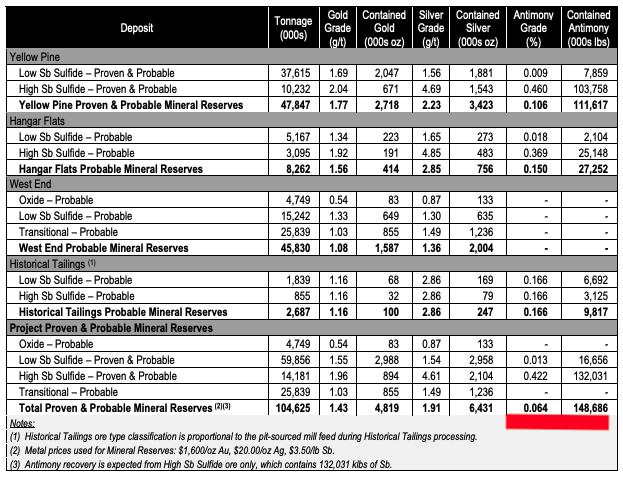

Perpetua Resources’ project has a 104Mt @ 0.064% antimony reserve (proven and probable category)...

BUT the main economic driver for the project is the 4.8 million ounces of gold and 6.4 million ounces of silver.

(Source)

The reason these relatively low % antimony grades are likely to make sense for Perpetua is because the resource is backed by a giant gold/silver resource that on its own is likely to make a lot of financial sense to develop.

We think that SS1’s project may also fit into this bucket - a potentially economic silver resource on its own, with added antimony credits - and we’ll be keeping a keen eye out for additional work on firming up the project antimony potential.

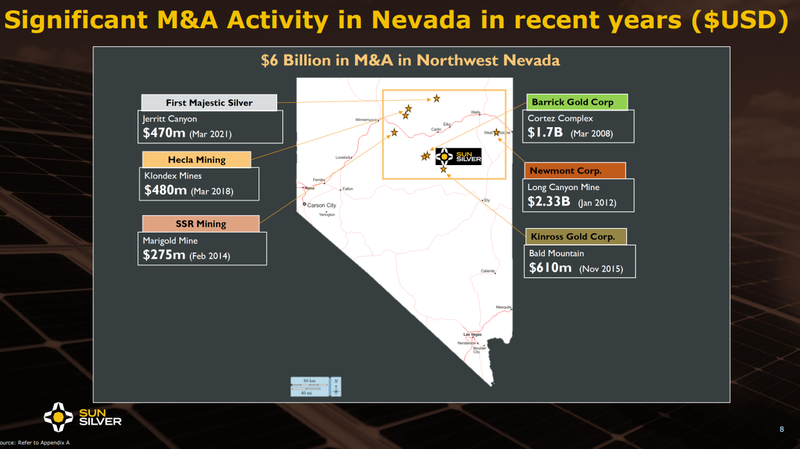

It’s a great jurisdiction for silver mines...

SS1’s project sits in Nevada, USA - the biggest silver producing state in the US.

SS1’s project is surrounded by some of the world’s biggest silver producers, companies like:

- Barrick Gold (capped at ~US$51BN)

- Kinross Gold (capped at ~$16BN)

- Coeur Mining (capped at ~$3BN)

The gold and silver projects here are giant and are all operating profitably at far lower grades then SS1’s resource.

SS1’s silver equivalent grade across its latest Inferred JORC Resource is ~67.25g/t.

Whereas Coeur Mining’s Rochester asset is operating at average silver grades of ~12.5g/t...

Barrick is operating one of the projects that put the company on the map because of how BIG and how low of a cost the mine was able to be operated at...

All of these projects have billions of dollars of sunk cost into existing silver and gold processing infrastructure - which makes new deposits interesting from a takeover target perspective...

And we have seen ~US$6BN in M&A in recent years...

If you want to learn more about the geology of the projects that sit in this part of Nevada check out the following video:

(Source)

Ultimately, what makes a good grade depends on the type of deposit.

Easier to mine, the lower the commercial grade.

So for the types of deposit SS1 has what you are really looking for is scale and size.

Credits from antimony, at scale, would also be a big bonus.

More on antimony

Antimony is used in infrared missiles, nuclear weapons and night vision goggles, and mostly as a hardening agent for bullets and tanks.

90% of all antimony comes from three countries: Russia, China and Tajikistan.

Antimony was first put on the US’s radar as a strategic material in 2022 when the Russia-Ukraine conflict emerged.

However, it has increasingly been in the spotlight when China announced export controls over the material.

As we said, these export controls come into effect in 5 days.

This means any Chinese business seeking to export six antimony-related products and separation technologies will have to apply for a licence from China’s Commerce Ministry.

We’ve seen these types of geopolitical manoeuvres before...

Applying geopolitical pressure by restricting battery materials or energy supply is one thing, but messing with military supply chains is next level.

While the US government is clearly moving quickly - previous export restrictions on graphite and rare earths have not seen sizable shifts in supply chains of these critical raw materials.

Western governments can often talk a big game about developing their own mines, but often fall short on action.

Whether antimony is about to become central to the critical minerals push over the long term or it fades into obscurity once more - it's simply too early to tell.

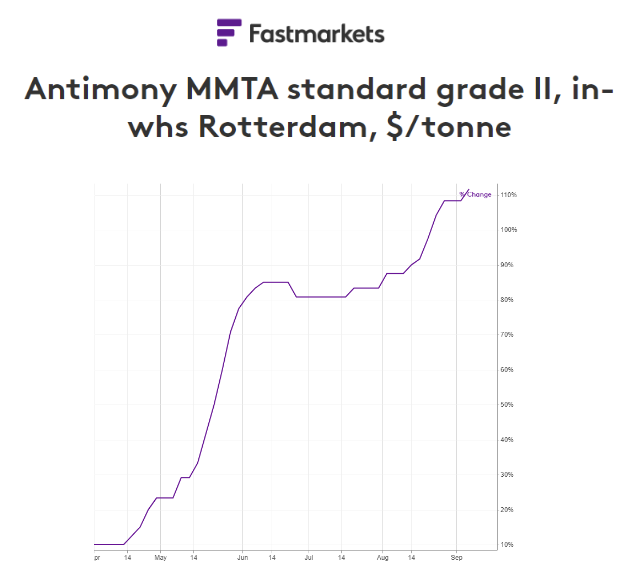

And yet, the price is certainly moving quickly...

By one measure, the antimony price is already up more than 100% in the last few months and could increase further as these export controls come into effect.

(Source)

This is not the first time that antimony has been used as a means to strategically weaken an opposing nation.

During World War 2 the Japanese cut off antimony supply from China to the US which sent the US scrambling to find and fund domestic antimony supply to support the war effort.

Now, the US is again in catch up mode without any domestic supply of antimony.

What could go wrong?

In the short term, the risk we see for SS1 is now “development/delay risk”.

With a very large resource already, we want SS1 to quickly progress its project through development, but are conscious that slow newsflow and delays could hurt the share price.

Development/delay risk

Should any or all of the above risks materialise, SS1 could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on SS1.

Source: “What could go wrong?” - SS1 Investment Memo 18 May 2024

Our Investment Memo was initially focussed on silver–gold exploration risk - our attention is now drawn to antimony related exploration risk. We simply didn’t know there was antimony on the project.

Exploration risk

There is no guarantee that SS1’s upcoming drill programs in Nevada are successful and SS1 may fail to find economic silver-gold deposits.

Source: “What could go wrong?” - SS1 Investment Memo 18 May 2024

But it's always possible the antimony potential doesn’t live up to market explorations...

Antimony exploration risk

So another risk that sits outside of our SS1 Investment Memo is related to the antimony potential of SS1’s project.

Up until now, the only indication we have that there may be antimony prospectivity is from portable XRF results which SS1 only announced a few weeks ago and today’s historical drillholes - which are also portable XRF results.

XRF readings are usually not 100% accurate and so there could be variances in the final grades once the much more definitive assay results are announced.

SS1’s handheld pXRF results are preliminary only and were reported to indicate semi-quantitative analysis of drill material.

Drill cores can, for example, display higher spot readings with pXRF.

There is a risk that the antimony grades were only across tiny intervals which might mean there is no broad based mineralisation across SS1’s project.

Ultimately the final assay results COULD reveal lower than expected antimony grades and/or a tiny / sub economic amount of mineralisation.

Commodity price risk

Chinese export restrictions have not always translated to sustained underlying commodity price rises.

Rare earths export restrictions in 2010 helped Lynas get off the ground, but since then there have been few new entrants to the market.

Graphite export restrictions in 2023 did not see a sustained price rise for graphite, and many graphite projects remain stranded.

With a dominant market share, China can also flood the market to hurt the viability of projects that have antimony by-products, along with a range of other critical minerals.

As a result, commodity price risk is a factor that we’re conscious of with SS1:

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver and gold prices fall, this could hurt the SS1 share price.

Source: “What could go wrong?” - SS1 Investment Memo 18 May 2024

To see other risks to our Investment Thesis check out our SS1 Investment Memo here.

Our SS1 Investment Memo

For a full rundown of our investment thesis, read our SS1 Investment Memo, where we share:

- What SS1 does

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.