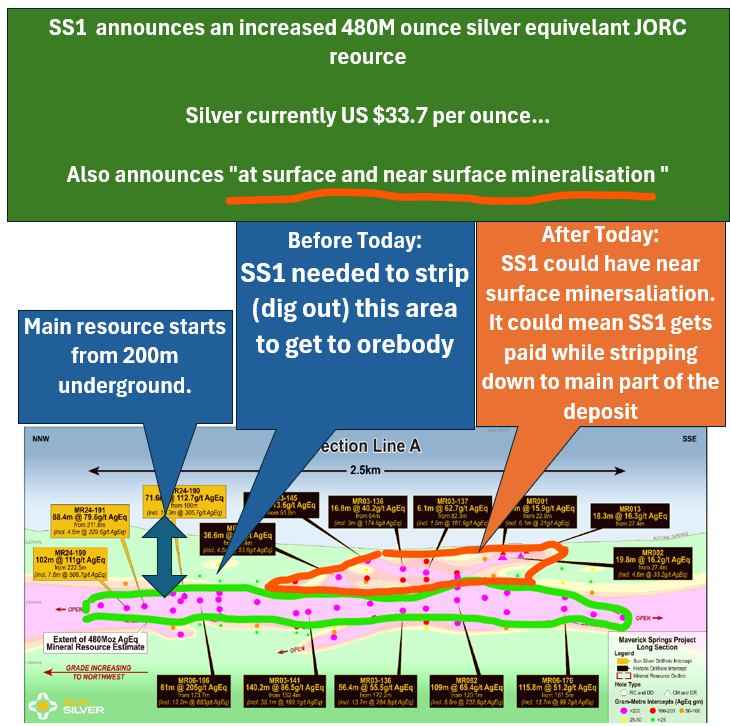

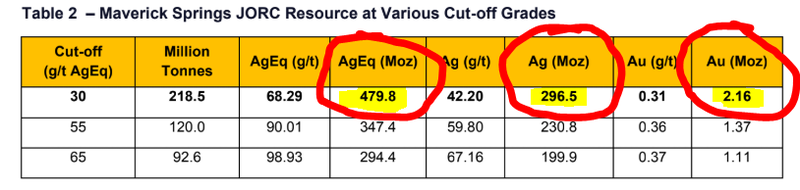

SS1: Increases to 480M ounces of silver equivalent resource… and identifies at surface and near surface mineralisation.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,685,000 SS1 shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time.

Our 2024 Small Cap Pick of The Year Sun Silver (ASX:SS1) has the largest pre-production primary silver resource on the ASX.

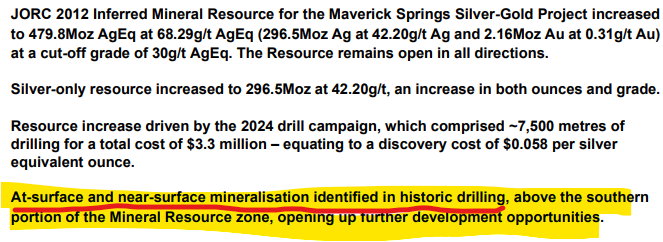

This morning SS1 announced a resource increase of 57M ounces of silver equivalent.

SS1’s resource now sits at 480M ounces silver equivalent.

(2.16M ounces of gold, 296.5M ounces of silver)

BUT...

Since SS1 listed 10 months ago, the silver price has risen US$22 per ounce to US$33.69 per ounce.

So with 480M ounces of silver equivalent...

And silver trading at US $33.69 per ounce...

Why is SS1 only capped at just ~$103M, and trading at 71c?

And what did SS1 announce today that could change this?

For us, (and we suspect for many fund managers that have looked at SS1) the “money shot” in today’s announcement is:

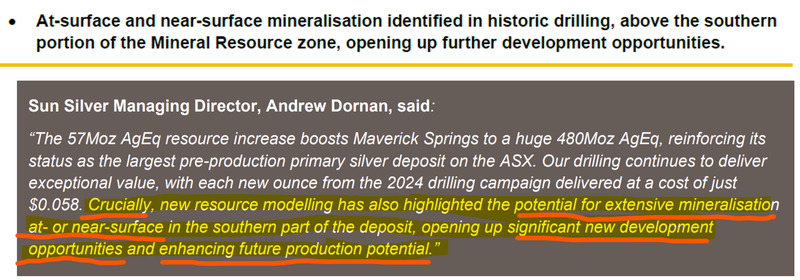

“Surface and near surface mineralisation identified in historic drilling”

(Source: Today’s SS1 announcement)

Why?

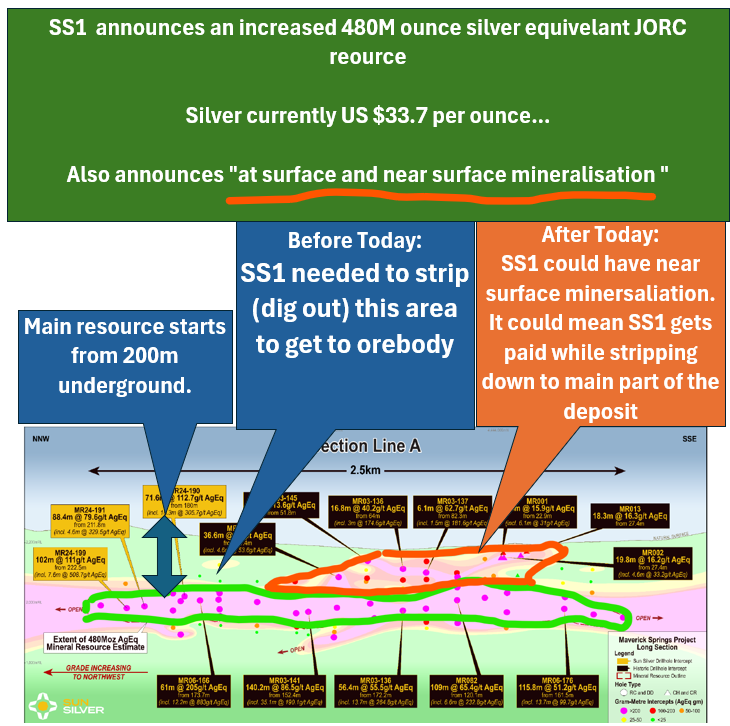

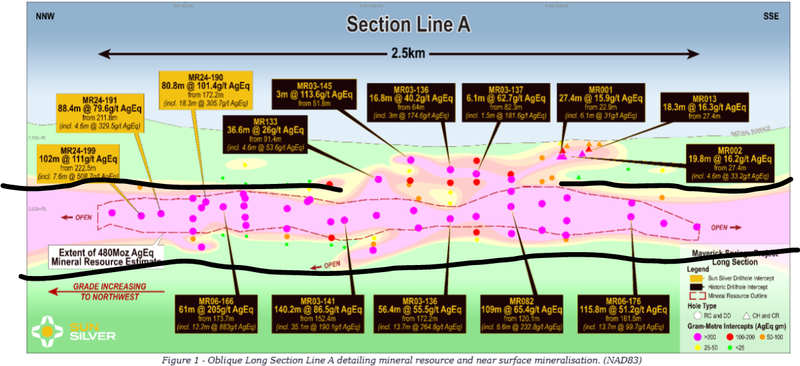

Because, SS1’s current giant silver deposit sits ~200m underground - that is relatively deep.

Yes, 480M ounces is a LOT of silver, but SS1 needs to dig a big expensive hole (pit) to reach it before they can extract and sell it.

(if silver goes to say US$50 per ounce this probably won’t matter as much, which was our original thesis with this Investment)

Today SS1 announced that analysis of historic drill cores revealed surface and near surface mineralisation.

IF proven out with more drilling, we think the near surface mineralisation would change the way bigger institutional investors & major miners view SS1’s project in a big way.

All of that material that is needed to be stripped back to get to the higher grade core of SS1’s resource could be considered “payable material”, meaning SS1 would make revenues while stripping down to the core of the resource.

Without the near surface mineralisation, all of that stripping was assumed to bring in zero cash...

It’s still relatively early days, but IF SS1 can prove up the ‘economic mineralisation from surface’ theory it would be a big positive step change for the project’s attractiveness in terms of financing, development and major institutional money...

We think the near surface mineralisation story alone could be a trigger for a re-rate in SS1’s valuation.

What could trigger a run in SS1’s share price in 2025?

For the rest of 2025, we think there are five different ways SS1’s valuation could re-rate from here (and hey it could be a little bit of all of them with a bit of luck):

- Silver price runs - The first is pretty simple, IF the silver price runs, then we would expect SS1’s share price to follow.

- Exploration success - SS1 will be drilling again in 1-2 weeks time (early April). We think extensional holes & more silver found near surface is what will get the market further interested in SS1.

- SS1 silver resource update - If SS1 publishes a JORC resource update that increases the level of confidence in the project (i.e. the resources move from inferred to indicated) and the size of the silver equivalent resource (above investor expectations), this could help unlock some institutional funding.

- Antimony surprise - SS1 could publish an antimony resource by re-assaying historical drill cores that were not tested for antimony. Antimony could signal to the market that SS1’s project is of ‘strategic importance’ to the US Government. (more on this here)

- SS1 hits market cap/trading volume requirements to get into an index - This one is somewhat outside of the company’s control, but as the market cap gets bigger, SS1 becomes more investable for larger institutions. We are hoping SS1 can hit the $150-200M market cap this year and get included in one of the ASX indices.

Why we are Investors in SS1

Aside from today’s resource increase and the revelation of near surface mineralisation, last week SS1 released its 2025 work programme, which gave investors a lot of ideas of what to expect from SS1 over the coming months.

We have been Invested in SS1 since prior to last year’s IPO, and we still maintain a significant position.

The company has evolved since its IPO, and the macro thematic has evolved too, so we thought now is as good a time as any to revisit the reasons for our Investment in SS1.

We have summarised them here, and we will cover in more detail later in this note.

- SS1 has the largest primary resource on the ASX

- SS1 is extremely leveraged to movements in the price of silver

- We are bullish on silver - and the price is reaching decade highs

- SS1 is reaching a size where it could possibly be included in index funds

- The US Department of Defence wants antimony, SS1 may have it

- Can SS1 be the next $1.1BN capped Perpetua Resources?

- SS1 has a Carlin-Style deposit, cheap and easy to mine

- SS1 is in Nevada USA, near some of the best gold and silver mines in the world

- JORC resource includes ~2.16M ounces of gold

- SS1 has downstream opportunities with silver paste for solar PV cells.

Keep on reading for more details...

The biggest news (for us) from today’s SS1 announcement - mineralisation could actually start from surface?

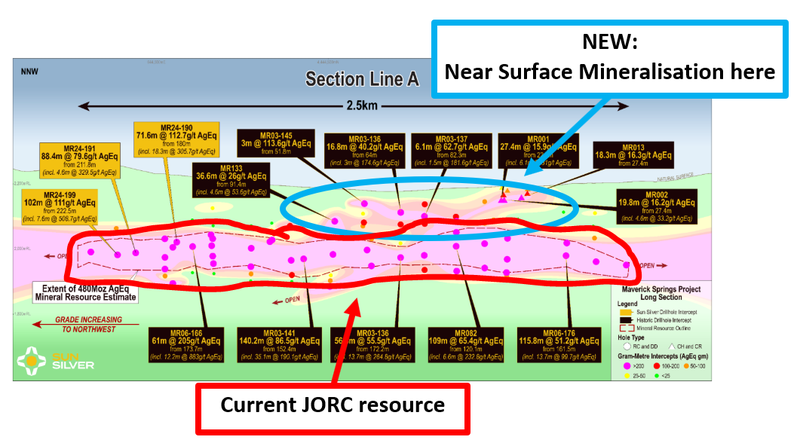

Today for the first time, SS1 showed the market that its resource may actually be starting from surface.

If the mineralisation does start from surface, this could have a positive flow on effect for the economics of SS1’s project.

Most of SS1’s current resource starts from 200m depths, but today’s news could change that...

Because the current resource starts at 200m, in order to develop the mine, SS1 would need to strip away the overburden before getting to the juiciest parts of its deposit.

That would most likely mean the payback on all the CAPEX would take longer.

BUT, if the mineralisation starts from surface, then SS1 may be able to recover some value from what was previously thought to be waste material, potentially “breaking even” as it digs towards the higher grade stuff.

In mining, a key financial metric investors, financiers and even miners themselves (when considering M&A opportunities) look at is a project's “Payback Period”.

IF SS1 can show that mineralisation starts from surface, it could mean the payback period on any CAPEX to develop is realized a lot sooner.

It could also mean SS1’s capital costs come down, as most of the stripping would happen during the mining stage and not BEFORE.

To develop SS1’s mine, one of the main challenges is to get down to the guts of its orebody... but once there, the grades start to look pretty good compared to other mines in this part of Nevada.

IF that top section of the resource is all payable material it will mean SS1 generates revenues from day 1 of mining and can help pay for all the costs.

All of this information was discovered by SS1’s new management team after re-evaluating the resources over the project (there were some new board and management appointments in February).

This re-look at the data can sometimes happen when there is a material change in the underlying price of the commodity in a short period of time.

Resources are developed with “cut off grades” in mind - these are the grades of minimum mineralisation that can be economically extracted.

The higher the price of the commodity, the lower the cut off grade.

Since the last resource update, the silver price has been fairly stable but the gold price has gone from ~US$2,500 to US$3,000/oz so a lot of the gold grades that were previously overlooked near surface could now look a lot more interesting.

To learn more read: Cut-off grades explained

How does SS1’s project rank against some of the other mines in the region?

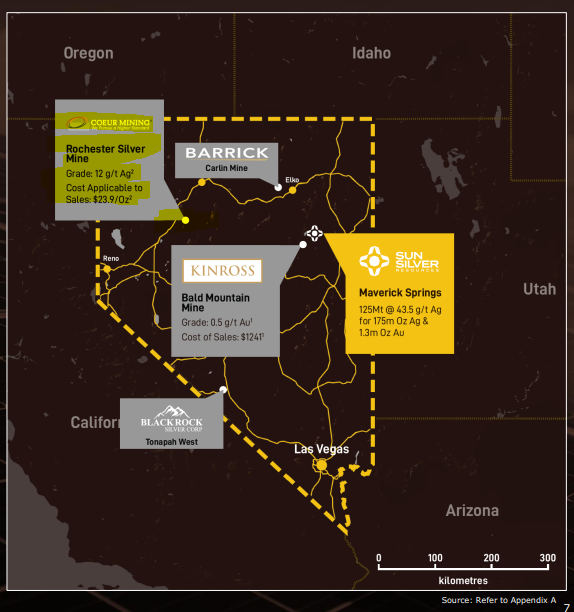

SS1 is located next to some of the largest, low-cost precious metals mines in the world.

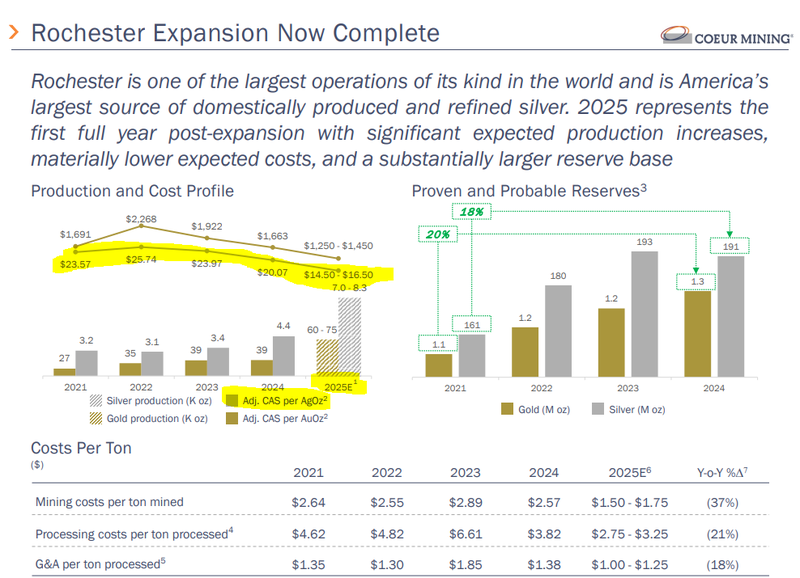

Nevada is THE precious metals state in the US and there are some good parallels between SS1’s project and the Rochester Mine, which is also in the northern half of Nevada.

The Rochester Mine is owned and operated by $4BN capped Coeur Mining which is the world’s largest silver producer.

Rochester is a very large low-grade, easy to mine, easy to process project, and in 2024, the mine produced ~4.4m ounces of silver and ~39k ounces of gold.

Rochester has been producing silver and gold at average grades of ~12g/t.

(This would be considered a very low grade by the market)

Despite the low grades, Coeur has managed to keep its average cost of production at ~US$20 per silver equivalent ounce... well below current spot prices of ~US$33.

AND Coeur is actually forecasting even lower costs in 2025... US$14.50 to US$16.50 for the year.

(Source)

The reason projects in this part of Nevada can be mined at such low costs comes down to a few reasons:

1. Because of their geology (“Carlin Style”) deposit - deposits in this part of Nevada are flat lying meaning when a company starts mining the juiciest parts of the orebody, it is big and very consistent over a large area. Size/consistency means predictable costs...

2. Because they also produce gold as a co-product - Coeur’s Rochester produced ~39k ounces of gold in 2024. It might not sound like much but it adds to the project’s economics. SS1’s resource similarly has a big gold resource too (~2.16M ounces). At current gold prices that has a big impact on the economics of projects like SS1’s.

(Source)

3. Because they are easy to process - Extraction techniques that are commonly used in the region mean that low-grade gold and silver can be easily extracted. SS1 still has some metwork to do on this front, but that is one of the goals we want to see the company kick in 2025.

The key takeaway is that mineral deposits within the Carlin Trend can be mined at extremely low cost and the Rochester Mine illustrates this.

It has ~300M ounce silver resource and ~270M ounces in reserves.

The reserves have an average gold grade of 0.05g/t and silver of ~10g/t... (somewhere in that ~12g/t silver equivalent range).

Compare that to SS1’s resource, which has 0.31g/t gold, 42.2g/t silver (68.29g/t silver equivalent).

We think in terms of size/scale SS1’s resource ranks right up there with the Rochester asset.

The obvious difference between the two is that Coeur’s asset is in production and has reserves.

SS1 is a much earlier stage with its resource in the inferred category at the moment.

Our “Big Bet” for SS1 centres around seeing SS1 take its project through the mining company lifecycle and build towards project development.

Since we first Invested in SS1, the company has delivered:

- Two resource upgrades

- Raised $20M with cornerstone investments to support the project development

- 7,500m of drilling (including some very big hits along the way)

- Discovered antimony within the project

After today’s resource upgrade and two key announcements over the past few weeks, we thought now would be a good time to reset our expectations for the company with a new Investment Memo and our Reasons for Investing.

UPDATED: 10 Reasons we Invested in SS1

1. SS1 has the largest primary silver resource on the ASX

SS1 has a 480M ounce silver equivalent JORC Resource.

This is the largest pre-production primary resource on the ASX.

There is a premium attached to being the “biggest” of any commodity in a particular market and funds or investors wanting leverage to silver (without buying the commodity itself) will ideally look to SS1 first.

2. SS1 is extremely leveraged to movements in the price of silver

Silver is generally produced as a by-product from producing base metals. But because SS1 is a primary silver producer. it means that for every US$1 per ounce that silver increases, it has a material increase on the in-ground value of SS1’s project.

This has the effect of SS1’s share price generally tracking very closely to the price of silver.

If silver goes up (and goes up in a big way) then so too should SS1.

3. We are bullish on silver - and the price is reaching decade highs

The silver price is re-testing a 12 year high at the time of writing (around US$34/oz) as silver demand is fast outstripping supply.

We think the long term macro tailwinds for silver are incredibly strong and should help SS1 as it looks to take its resource into development.

4. SS1 is reaching a size where it could potentially be included in index funds

SS1 is currently capped at ~$103M. It is reaching a size and liquidity profile where it could qualify for inclusion in the ASX indices.

Getting into an index opens up SS1 to a whole new pool of capital and it makes the company a potential investment opportunity for institutional investment funds.

If SS1 gets into an index like the ASX All Ords it could become the de-facto ASX Silver ETF and the only way for passive funds to get leveraged silver pre-production silver exposure on the ASX.

5. The US Department of Defence wants antimony, SS1 may have it

The US imports 90% of its antimony which all come from potentially hostile countries (China, Russia and Tajikistan) and it has no antimony production of its own.

Antimony is a critical mineral for various military applications including as a hardening agent for ammunition.

SS1 has identified antimony across its project from xPRF analysis and drilling data collected in 2024.

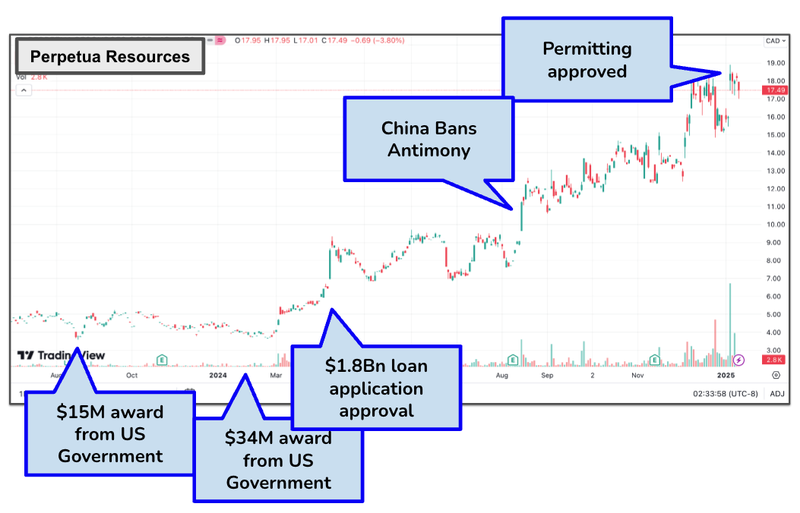

6. Can SS1 be the next $1.1BN capped Perpetua Resources?

Perpetua Resources has a gold-antimony resource in Idaho, USA.

The US Government, through the Department of Defence, has provided over $50M in grants as well as a $1.8BN loan to help fund the development of the mine.

The US Government was particularly interested in the antimony potential of that project.

We think that if SS1 is able to develop a US-based antimony resource it could also be supported by the US Government - like Perpetua Resources.

7. SS1 has a Carlin-Style deposit, cheap and easy to mine.

SS1’s project is located in the “Carlin Trend”, an area that is home to some of the biggest gold and silver mines in the world.

In the mid-1980s Barrick made a Carlin-Type discovery at its “Goldstrike” project in Nevada (not too far from SS1).

This was the project that put the company on the map and produced around 200,000 ounces at 1.2g/t of gold and 200,000 ounces of silver in the mid-1990s.

What made this project so successful was that it was a low cost mining production.

If SS1 can prove that it can extract the gold and silver from its resource with a similar process used by Barick on its Goldstrike Project it could have a material impact on the feasibility of SS1's project.

8. SS1 is in Nevada USA, near some of the best gold and silver mines in the world.

Nevada is a big mining state and the area of Nevada that SS1 is working in is called Elko County.

There are major gold and silver mines scattered throughout this area of Nevada, and Elko County is very familiar with the mining industry.

$45BN Barrick and $14BN Kinross both own projects in the region.

This means that there is a high level of skilled labour in the area and permitting processes are well known.

9. JORC resource includes ~2.16M ounces of gold

Included inside SS1’s 480m ounce silver equivalent JORC resource is a ~2.16M ounce gold resource.

With the gold price also at record highs, the in-ground value of SS1’s project is also leveraged to the increase in the price of gold.

10. Downstream value add: “Silver paste” production (for solar) could improve economics

SS1 has a giant silver resource within the US. Silver is a key material used in solar panels in the form of silver paste.

SS1 is evaluating the merits of developing downstream silver paste processing.

The world’s solar manufacturing capacity (including silver paste production) is heavily concentrated in China. If SS1 is able to produce silver paste in the US this could add to the merits of the project.

SS1 index inclusion upside - the only way to get silver exposure on the ASX...

A key reason we have always had for being Invested in SS1 was because we had a strong opinion that SS1 could eventually become a ‘‘defacto silver ETF”.

As the silver price rises more and more institutional capital would look to get some silver exposure in their portfolios.

For a long time, the only way to get pure-play silver exposure (especially from a pre-development perspective) was ASX listed Silver Mines.

Recently, Silver Mines valuation has come off due to permitting issues at their NSW asset.

And now there is SS1 on the ASX with the biggest pre-production silver asset on the market.

For every $1 increase in the price of an ounce of silver, SS1’s giant resource becomes significantly more valuable from a “what’s in the ground” perspective.

SS1 through its resource size could essentially become the preferred way of getting leveraged silver exposure on the ASX at scale.

The most obvious way SS1 can put itself in that position is by increasing its market cap and getting included in one of the ASX indices.

To get there, SS1’s market cap will need to reach the $150-200M range and trading volumes will need to increase...

At the moment SS1 is on the right track with its market cap at ~$103M.

We wrote about how index inclusion can open up a stock to a whole new pool of capital in a weekend note a few weeks ago.

Check that note out here: Index Inclusion: A Small Cap’s Big Leap

IF SS1 gets into an index, passive funds that need to have some silver exposure will likely need exposure to SS1.

Index inclusion was something that some of our best ever resource Investments have had going into a period of strong newsflow.

Some of our best ever Investments ran to their all time highs off the back of index inclusion.

Here is what happened to Vulcan Energy Resources after it got included in the S&P All Ordinaries index:

(At its peak, VUL was up 8,225% from our Initial Entry Price)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Also Latin Resources, which went from our Initial Entry Price of 1.8c to a high of ~42c (up 2,332% at its peak):

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Both of those companies started run ups off the back of index inclusion.

Index inclusion alone didn’t spark these rallies nor does it guarantee sustained price increases, but it played a part in adding “fuel to fire” as larger pools of capital become unlocked.

Our bet is that IF SS1 can get to that $150-200M market cap range, deliver some material catalysts it could position itself as a way for the big pools of capital to get silver exposure.

That wave of institutional capital could be what triggers SS1’s valuation to re-rate higher from where it is today...

Is antimony going to be the dark horse for SS1 in 2025?

Every single hole that SS1 drilled in 2024 had antimony in the cores.

Although it was not included in today’s resource upgrade, we see antimony as a big part of the story for SS1.

Antimony is a niche critical metal that is used in various military applications.

The US imports 90% of its antimony from three countries...

China, Russia or Tajikistan.

For now, two of those countries are actively hostile to US interests (China, Russia).

And all of them are a long way away from the US.

With the spectre of conflict increasingly present in the minds of the biggest players in geopolitics, the US wants to shore up its antimony supply chain pronto.

That’s because there is no current local mine supply in the US and last year China announced a ban on the critical mineral.

Last week, US President Donald Trump signed an Executive Order that made mineral production in the USA a strategic priority.

In particular “critical minerals”.

To evaluate which “critical minerals” are most at risk there are two things that we look at.

- How important is the mineral to the US?

- Where does the majority of supply come from?

First, on importance.

Antimony is very critical to the US, it is used as a hardening agent in ammunition and various other military applications.

Evaluation: very important

Second, on security of supply.

The antimony supply chain is extremely at risk. The US imports the majority of its antimony with a limited amount coming internal through recycling.

China has placed an export ban and the Department of Defence needs reliable in-country resources.

Evaluation: very high risk.

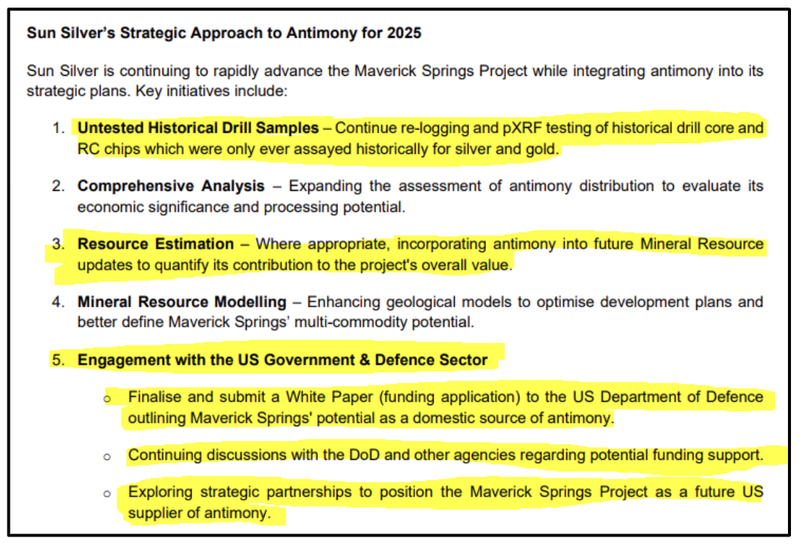

SS1 has publicly stated that it is working with Holland & Knight as well as the Department of Defence to evaluate funding options for SS1 to develop an antimony resource within the US.

The next stage for SS1 is to finalise and submit a white paper to the Department of Defence outlining the antimony potential of the project.

We are hoping that some funding support will flow from these discussions which are now made more urgent through President Trump’s Executive Order.

With the funding SS1 will be able to undertake an even more comprehensive analysis over the project.

So far SS1 has been able to conduct xPRF readings over a number of holes on the project.

A more comprehensive analysis could involve re-assaying some of these old drill holes to start building out a resource.

If SS1 publishes a large enough antimony resource, it could provide the incentive for continued funding from the DoD.

This has been done before.

In 2023 and 2024 the US DoD provided financial support in the form of grants and eventually a $1.8BN loan to Perpetua Resource for its gold-antimony project in Idaho.

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Our thesis is pretty simple - IF SS1 can define an antimony resource to go with its silver then we would hope it opens doors for funding and faster permitting.

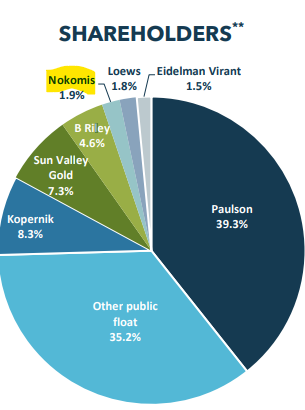

Interestingly, SS1 recently managed to attract a new substantial shareholder to the register - Nokomis Capital.

Nokomis now own ~6.5% of SS1.

We did a bit of digging and found that Nokomis Capital were also shareholders of Perpetua (Nokomis held ~1.9% stake in Perpetua Resources).

This was from Perpetua’s January 2023 presentation:

(Source)

Two weeks ago, SS1 put out an update on its broad antimony strategy.

Importantly, SS1 will move its old core to a new facility, which will make it much easier to relog all of the old core:

With that information, SS1 will have a much better idea of the economic significance of its antimony potential (and potentially secure some funding from the US government).

Check out that full announcement here:

(Source)

Our new SS1 Investment Memo

With the JORC Resource Upgrade published, SS1 has closed out the majority of the objectives that we wanted to see completed under our original Investment Memo.

With the 2025 program of work set it is now time for a new Investment Memo.

Investment Memo: Sun Silver (ASX:SS1)

Date Opened: 26th March 2025

Shares Held at Open: 3,685,000

What does SS1 do?

Sun Silver (ASX:SS1) is developing a 480M ounce silver equivalent JORC resource in Nevada, USA.

What is the macro theme?

Silver is both an industrial and precious metal.

As a precious metal silver can be used as a hedge against inflation, which remains persistently high at the time of this memo.

As an industrial metal silver is used in the manufacture of photovoltaic cells for solar panels and can be considered important to the energy transition.

Antimony is a critical metal in a variety of military applications, and is seen as vital to the national security interests within the United States.

Our SS1 Big Bet:

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SS1 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Why do we continue to hold SS1?

- SS1 has the largest primary resource on the ASX

- SS1 is extremely leveraged to movements in the price of silver

- We are bullish on silver - and the price is reaching decade highs

- SS1 is reaching a size where it could possibly be included in index funds

- The US Department of Defence wants antimony, SS1 may have it

- Can SS1 be the next $1.1BN capped Perpetua Resources?

- SS1 has a Carlin-Style deposit, cheap and easy to mine

- SS1 is in Nevada USA, near some of the best gold and silver mines in the world

- JORC resource includes ~2.16M ounces of gold

- SS1 has downstream opportunities with silver paste for solar PV cells.

What do we expect SS1 to deliver?

Objective #1: Drilling Program for 2025

We want to see SS1 continue to drill out its project over the next 12 months.

We especially want to see SS1extend the mineralisation towards the shallower North West of the resource leading to a further resource upgrade.

Milestones

🔲 Drilling Commenced

🔲 Assay results

🔲 Resource Upgrade (Size)

🔲 Resource Upgrade (Classification)

Objective #2: Evaluate Project Feasibility

SS1 has signalled its intention to enter feasibility studies, which would provide a first pass assessment of the project’s economic viability.

As part of the feasibility studies we will be keeping an eye out on the metallurgical testwork SS1 completes.

Milestones

🔲 Metallurgical testwork results

🔲 Commence Feasibility/Scoping Study

🔲 Feasibility/Scoping study delivered

Objective #3: Define an antimony resource

We want to see SS1 define an antimony resource over its project. SS1 has hired Holland & Knight to help apply for government support from the Department of Defence.

Milestones

🔲 Re-log and re-assay remaining historical drill cores

🔲 US Government Funding

🔲 Publish antimony resource

What could go wrong?

Commodity Price Risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should the silver price fall, this could hurt the SS1 share price.

Exploration risk

There is no guarantee that SS1’s upcoming drill programs in Nevada are successful and SS1 may fail to find economic silver-gold deposits.

Funding risk/dilution risk

As a small cap, SS1 is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, SS1 could struggle to access capital on favourable terms. These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Market risk

There is always the possibility that broader market sentiment gets worse and shares as a whole trade lower, taking SS1’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Development/delay risk

Should any or all of the above risks materialise, SS1 could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on SS1.

Met Work Risk

SS1 is still yet to evaluate the metallurgical feasibility over its resource. Ideally, it is very easy for SS1 to extract the gold and silver from its resource, but there is no guarantee that this happens.

Investment Plan

We are Invested in SS1 to see it expand its resource and progress its project into development.

Our plan is to hold the majority of our position in SS1 for 3 to 5 years which we hope is enough time to see SS1 to move towards development (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.