SS1: Highest Grade Antimony Result. So Far…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,502,804 SS1 Shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Sun Silver (ASX:SS1) just announced a 7% antimony interval...

Inside a larger 59m at 0.1% antimony result.

So far SS1's antimony grades are higher than the averages across $2.5BN Perpetua Resources project, which has 0.06-0.07% antimony grades.

SS1 is re-assaying for the US critical metal antimony in the ~200 historical drill holes that make up its 480M ounce silver equivalent resource in Nevada, USA.

SS1 has the largest pre production silver project on the ASX and in the USA.

Silver has been threatening new highs of late, and antimony prices are at record highs (and with national strategic importance to the US).

It's a good time for SS1 to be expanding its giant US based silver AND antimony project:

(Source)

Re-shoring US critical metals supply is a high priority for the US government and Department of Defence.

In addition to the giant silver asset, could SS1 end up also having the biggest antimony resource in the USA?

Bigger than the $2.5BN capped Perpetua Resources - the current antimony leader in the US?

Similarly to SS1, Perpetua’s project is first and foremost a precious metals (in this case gold) project, BUT...

The project's antimony content is what attracted almost US$1.9BN in funding commitments from the US government to Perpetua’s project, including ~US$80M from the US Department of Defence.

Two weeks ago, the US DoD also just invested $400M in MP Materials for its US based rare earths project.

Indications are that the Pentagon will likely be doing more similar deals to fund USA based critical metals supply.

(Source)

SS1 explicitly said last week that it was pursuing US DoD funding right now...

(Source)

SS1 just raised $30M at 92c led by global institutions, and has earmarked some of that cash to go after US government funding for the antimony potential on its giant silver resource estimate.

(We bid for $200k in the capital raise and got scaled back to ~$120k.)

A few days ago we wrote about how we think SS1 is set up to deliver a VUL style price run IF silver and antimony prices continue to surge upwards (read it here) - noting that commodity prices can go either up OR down, so it might not happen.

We also saw John Hancock (the son of Australia’s richest person Gina Rinehart) participate in last week's SS1 raise (source) - John also rode the VUL wave with us after investing at 40c before it ultimately hit highs of above $16 - more on this in a second.

SS1 keeps releasing the right results - we just need the silver price to keep moving up AND the emerging USA critical metals theme to continue growing, especially in the minds of US based investors.

Noting at the same time that this is no guarantee to keep happening.

With each new assay result released, it's increasingly looking like economic antimony mineralisation does run through SS1’s giant silver deposit...

As we noted above, SS1’s project currently has a 480m ounce silver equivalent JORC resource estimate.

But it's looking like that resource is laced with the critical and high value metal antimony too.

SS1 hasn’t got an antimony JORC resource estimate just yet, but is working toward one at the moment.

The biggest defined antimony resource in the US right now is at $2.5BN Perpetua Resources’ project in Idaho, USA.

We think there is a chance SS1’s project ends up with a bigger defined antimony resource estimate because:

- SS1 is hitting grades at or above Perpetua Resources’ average antimony grade of 0.07% - SS1’s last two holes returned antimony grades averaging 0.1% and 0.12%.

- SS1’s project is ~67% bigger than Perpetua’s in terms of tonnage - Perpetua’s antimony resource is based on 132.2mt of material at 0.07% antimony grades. SS1’s silver resource is based on 221Mt of material... 221Mt, even at the same grades as Perpetua would give SS1’s project a bigger antimony resource.

IF SS1 can prove antimony runs across that 221Mt of material at or above Perpetua’s grades then the resource could be bigger than Perpetua’s project...

We Invested in SS1 primarily as silver exposure - we think SS1 will do well as long as silver prices increase and they continue to successfully execute their plan.

BUT we think the antimony story could be a dark (and strategically valuable) horse for SS1’s project.

Maybe it attracts non-dilutive grant funding - just like Perpetua did over the last three years...

(Perpetua received over US$80M in non dilutive grant funding for its project)

OR it gets cheap debt funding from the US government - again like Perpetua has...

(Perpetua received a US$1.8BN debt commitment from the US government)

Again, SS1 explicitly said last week that it was pursuing US DoD funding right now...

(Source)

Whatever happens, we think that any major unexpected surprise could re-rate SS1 higher and give its project the nudge it needs for the market to believe it can be developed.

Noting of course there are no guarantees in small cap stock investing.

SS1 just raised $30M - led by global institutions

SS1 just raised $30M at 92c - which gives the company cash to deliver:

- More drilling - SS1 is drilling right now and recently got regulatory approvals for an additional 90 drill pads, meaning it can upsize its drilling plans now.

- Increase its resource estimate - SS1 recently announced that it was consistently getting assay results back from old holes with silver grades ~20% higher than the average grade of its JORC resource right now. Higher grades along with more drilling could mean a bigger resource upgrade.

- Antimony maiden resource? - SS1 still has a lot of work to do on the antimony front. There are still hundreds of holes to re-assay across the existing silver JORC resource estimate.

- Metallurgical testwork - in an interview a few weeks back, SS1’s Managing Director, Andrew Dornan, mentioned that SS1 is currently running met test work to see if its project is “heap leachable”. This one is important from a technical perspective - it will give the market something to chew on in terms of how the project can be processed.

What we liked about the capital raise is that it looks like the shares went to a much deeper pocketed, passive, stickier crowd of investors compared to investors with shorter term time horizons which is more typical of ASX small cap raises.

Over the last few months we have seen institutional buying in SS1 slowly pick up - especially after seeing the Sprott Silver ETF (SLVR) add SS1 to its ETF and continue buying on market.

Back in May, Sprott Silver ETF (SLVR) held 392,350 SS1 shares (source)

Today they hold 1,182,353 SS1 shares - meaning the Sprott Silver ETF has been buying on market, nearly tripling their holding of SS1.

(Source - you can see Sprotts daily SS1 holding here)

We think the Sprott buying could be a precursor for other indexes/ETF’s to follow into SS1.

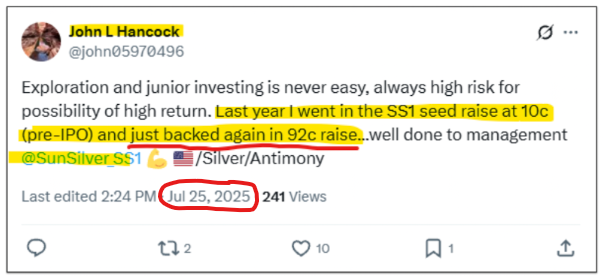

We also saw John Hancock (the son of Australia’s richest person Gina Rinehart) come in to the raise, he tweeted this last Friday:

(Source)

Hancock’s take in the raise reminds us a lot of the early days of our best ever Investment - Vulcan Energy Resources (ASX: VUL).

At its peak VUL was up 8,225% from our Initial Entry Price.

Back before VUL’s big run to $16, John Hancock popped up on the VUL’s shareholder register with 5.23%.

This revealed that he had invested in the 40c VUL raise and was adding to his position on market (source).

(Source)

Days after his involvement in VUL was made public, Gina also appeared on the VUL register.

(Source)

We are hoping that SS1 is shaping up to do something similar to VUL - we just need the silver and antimony themes to do the right thing, which unfortunately we or the company can’t control.

6 ingredients that worked for VUL - will they work for SS1?

The main reason VUL was able to run as hard as it did was because the lithium price went parabolic in 2021-2022.

Which meant the market was willing to re-rate material news that VUL put out.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Now we just need SS1 to deliver the news it says it will with the cash raised last week.

AND for the silver price to run to levels higher than most in the market expect.

Any increase in the silver price matters a lot for SS1 because of how big its resource is...

You can do your own maths on what every incremental increase of US$1 per ounce in the silver price means for the potential in ground value of SS1’s 480 million ounce silver equivalent resource estimate.

Of course continued uptrend of the silver price is no guarantee to continue.

Antimony prices are also increasingly relevant to SS1 now...

The antimony price started to run when China placed export restrictions on antimony in early 2024 and then really started to take off when China totally banned the export of antimony later that year.

Antimony prices are up by over 300% over the last 12 months...

We are hoping to see antimony prices stay up, while SS1 shows the market more of the antimony potential on its project.

Noting again that antimony is a commodity subject to wild fluctuations like any other - there’s no guarantee the price will stay up.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

On the weekend, we put out a note going through the “6 ingredients” SS1 will need to create the same tailwinds for a VUL style run.

The biggest and perhaps most important ingredient is #6 - the silver price which needs to rally so that a wave of capital can come into the sector and want to buy (and hold) SS1.

(OR now with SS1’s continued successful antimony results, the USA critical metals theme to keep gaining traction.)

Read that full note here where we go through how SS1 ranks across those six ingredients:

- Acquired the project in a down cycle - SS1 picked up its silver project in August 2023 when the price was low and interest in silver was minimal.

- Project size and scale is big - SS1 now has the largest pre-production silver asset on the ASX and in the USA, with growing resources (and a possibly antimony resource)

- In an emerging hot theme - For VUL it was battery metals and lithium. For SS1 it is the booming US precious/critical metals theme, thanks to its silver and antimony potential.

- In a country with demand for the end product - Located in Nevada USA, which is a key region for domestic critical minerals supply.

- Be the first mover - SS1 IPO’d early in 2024, ahead of the silver and antimony price runs.

- Then wait for that commodity price run.... - Silver and antimony prices have already had a bit of a run.

You can read more about these “ingredients” here: The final ingredient SS1 needs in our "recipe for an 8,000% VUL style price run"... but ingredient #6 is the hardest one to get...

Ultimately, we are hoping that a combination of these ingredients help SS1 achieve our Big Bet which is as follows:

Our SS1 Big Bet:

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our SS1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Sun Silver

ASX:SS1

Can silver “do a gold” and run to new all time highs?

We think it can.

The silver price over the next year is still the wild card for SS1 that we hope will work in our favour.

So far, the silver price has already been doing a great job, but what we really need is a “generational price run” like we saw lithium deliver back in 2020.

Of course this aspect is a ‘wild card’ and a ‘generational price run’ for a reason - they are not guaranteed to eventuate, and even if they do it might take longer than anyone can predict.

As mentioned in our weekend email, we think the silver price will be one of the most important factors determining where the SS1 share price goes next.

Being the largest pre-production silver resource on the ASX, SS1’s price generally tracks closely to the silver price - up and down.

The direction of the silver price has been basically correlated with the direction SS1’s share price moves:

(SS1 / Silver Chart)

Any increase in the silver price matters a lot for SS1 because of how big its resource estimate is...

You can do your own maths on what every incremental increase of US$1 per ounce in the silver price means for the potential in ground value of SS1’s 480 million ounce silver equivalent resource estimate.

(It’s actually not an easy calculation, and a lot of assumptions need to be made - costs to mine, operational execution and processing the silver would also need to be considered, which SS1 is in the process of figuring out. That’s before we even consider the time value of money.)

There is still a lot of work for SS1 to be in a position to extract the silver from the ground (including met work and feasibility studies) to realise the value of that silver.

From a technical/charting perspective the momentum is in silver’s favour as well...

Before you read the below or watch any of the videos we discuss, please remember that commodity prices can go both up and down.

Always invest with caution when it comes to small cap ASX stocks. The past performance is not indicative of future performance.

We have shared this video a few times with technical analyst Michael Oliver who said: “If silver goes above $35, watch out because if it goes above $36 it's a triple top breakout”.

(since then silver has broken through both those levels)

(Watch the full webinar here: Silver Slingshot Webinar)

And then Michael said “we are going to get another launch” and when we get it “it will be at a speedier process than what gold is currently doing”.

Remember though - even seasoned investors and analysts do not have crystal balls and cannot predict the future with absolute certainty, there's a lot of factors outside anyone’s control.

Gold is currently trading at all-time highs and is up over 100% over the last 18 months.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

IF silver does anything like that, it could trade above US$50/ounce.

But remember - it might not.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

And here is another technical expert - Mike Maloney - who put out the following video after Monday’s run in the silver price and said a “$10 move is coming quickly”.

Mike thinks the silver price is going to US$48 per ounce.

But remember - he could be completely wrong. Always invest with caution and if in doubt always speak to a professional financial advisor.

What are the risks?

In the short term we think the key risk for SS1 is “Commodity price risk”.

There is commodity price risk, because SS1’s share price tends to move up and down with the silver price.

IF the silver price was to fall, we would expect to see weakness in SS1’s share price.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver and gold prices fall, this could hurt the SS1 share price.

Source: “What could go wrong?” - SS1 Investment Memo 26 March 2025

Other Risks

Investing in SS1 carries other risks which may affect the value of the company. The Company’s primary asset is a pre-production silver and potential antimony project in Nevada, USA, and its prospects are inherently speculative.

As mentioned the value of SS1 is highly sensitive to fluctuations in commodity prices - particularly silver, and maybe antimony. A sustained downturn in these prices could materially impact the project’s economic viability.

There is also exploration and development risk. The Company is currently re-assaying historical drill holes and undertaking new drilling to confirm the presence and extent of antimony, which remains unproven at commercial scale.

Metallurgical test work is ongoing, and the project’s ability to proceed to heap leach production has not yet been demonstrated.

Additionally, there is no guarantee SS1 will receive government funding or support, including from the US Department of Defence, despite strategic interest in antimony.

The Company is as mentioned reliant on capital markets to fund development, and any capital raise may dilute existing shareholders.

Finally, regulatory, environmental, and permitting risks in the US jurisdiction - while generally stable - may delay or adversely affect development.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our SS1 Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our SS1 Investment Memo where you will find:

- What does SS1 do?

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.