Small Caps Take a Breather, Setting the Stage for What’s Next

Published 25-OCT-2025 15:50 P.M.

|

12 minute read

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

“It’s a healthy pullback that needed to happen”

Yeah, yeah, shut up...

We all hate hearing that when our glorious paper gains have been clipped.

But unfortunately there is some merit to it in the bigger scheme of things.

(if everything goes up too hard and too quickly, the eventual pull back will be more painful)

Remember our “the small cap market recovery will be like recovering from a hangover or sporting injury” analogy back in late 2024?

The comparison being that the recovery won’t be “instant”.

Instead it will come in progressively longer and stronger waves of bullishness.

With progressively shorter and less intense periods of bearishness in between the bullish waves.

The nearly four full months of bullish conditions in the small end of the market has been a very good signal.

With stock prices generally going up and up... and up some more.

The buoyant conditions in the small end of the market finally took a breather over the last week.

A near 4 month continuous run in small stocks before taking a breather is a very good sign that the market has shaken off a lot of the PTSD that came from the last 3 years of bear market conditions.

(but not all of it just yet, as everyone in the market was suddenly reminded that small stocks can in fact... go down, and the mental flashbacks to 2023 got them mashing the sell button with an open palm)

This time we expect the “risk off” of the last week to be shorter, before the next (and longer) bullish wave.

(This is just our prediction, we could be wrong, but we have positioned our Portfolio for positive conditions through 2026.)

While most stocks did come down a bit, they are finding new floors at higher levels than the start of the year.

Some may have even overshot downwards as any remaining bear market PTSD drives fear based overselling - and they could bounce back strongly.

(This is what we will be watching for over the coming weeks.)

Remember the last bullish wave in small stocks before this one?

It started in November 2024 lasted about 6 to 8 weeks, waning in mid December 2024.

Back then we wrote about how happy we were that the small end of the market managed to string together a positive 6 to 8 weeks.

We also predicted that there could be a “10 to 12 week next wave in early 2025” - looks like we were right on that one...

(aside from us saying it would be in “early” 2025, we are still claiming it though):

(read the full the small cap market recovery will be like recovering from a hangover or sporting injury article here)

What we are watching for now is the speed at which small stocks (and gold and silver) will find their new floor/base price...

And what they will do after that...

We predict (hope) they will start moving up again (in a more orderly fashion this time) to reach their recent highs again and beyond.

(at least in our chosen themes of silver, gold and US critical materials)

Basically we are watching the price discovery after a too rapid rise and then quick correction.

We are firm believers that growing geopolitical uncertainty bodes well for our macro investment themes silver, gold and US critical materials.

Gold and silver prices joined in (and maybe even led?) the pullback in small stocks.

Silver came off around 10% from the highest point it ever reached ~8 days ago, but is still trading at around its all time highs, and still up over 7% for the month.

Looking at the bigger picture, there have been a few pullbacks like this over the last 2 years, and it also puts last week’s pullback into perspective:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Gold is a similar story, after hitting its highest point ever~ 8 days ago, it closed the week down ~7% from that high point, but is still up for the month.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

“Price discovery” is basically markets trying to figure out what the price of something should be.

Sometimes exuberance takes over, prices rise too quickly and a pull back happens.

Prices may then either:

- quickly bounce back,

- or take some time to form a new base by going sideways for a while...

- or proceed to go down even more.

This is what we will be watching for in the coming weeks in our Portfolio stocks, and in silver and gold prices.

The key thing we look at is where prices are retracing to on pullbacks, and where a new “floor” is being set.

For example, IF a share price was up 5x and is setting up a new floor at 3x what it was before it started running.

We take that as a sign there is new capital willing to absorb the selling from profit takers.

Once the selling is absorbed and supply dries out, anyone wanting more shares needs to buy up to a new level where holders are willing to sell and take profits.

(which could be what sets up the second big run in share prices).

And what would get share prices really going?

Real progress on projects or supportive global/macro events in the mainstream news.

We also believe that private US capital hasn’t started flowing into the US critical materials macro theme yet.

(that big green Nvidia ball relative to mining stocks image we always talk about).

A lot of our ASX listed US critical materials stocks are now dual listed on the US OTC exchange, ready to absorb these US capital flows if/when they start happening.

At the company level, US government funding deals for US critical minerals stocks or positive exploration results could drive the next leg up.

It’s much easier to explain it with visuals.

Here are some examples of where we have seen price discovery play out in our Portfolio:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

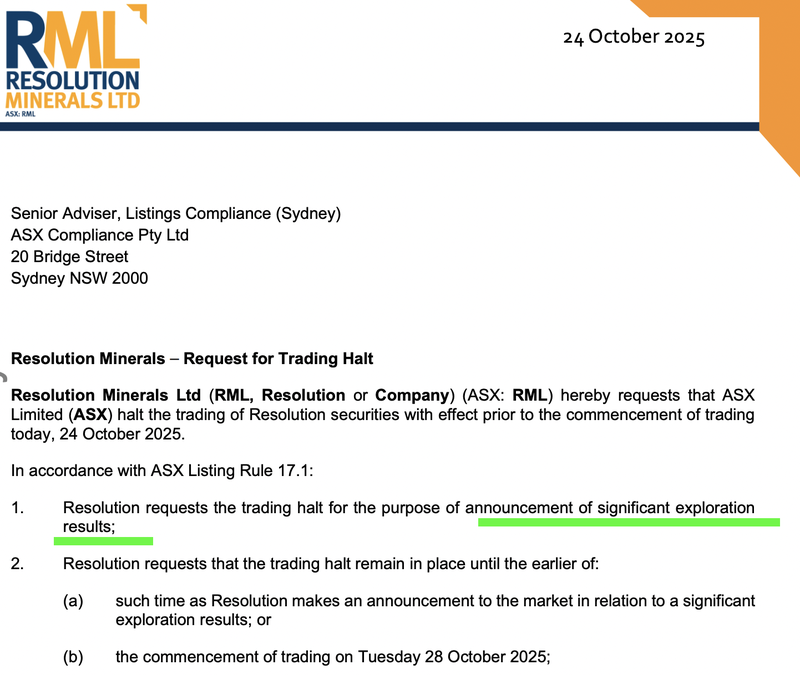

RML went into a trading halt on Friday pending the announcement of “significant exploration results”...

(Source)

Let's see what they come out with next week...

Speaking of drill results...

MTH recently delivered some good drill results (extensions to the west of its existing resource) - which is great news for MTH’s JORC resource estimate upgrade at its Target Area 1.

The news that could really get MTH going would be results from the other Target Areas on which they are drilling for new discoveries.

(11 holes from one Target Area are in the lab right now)

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

On silver...

SS1 has a 480M ounces of silver equivalent resource estimate in Nevada. SS1’s share price generally responds in some way to rises and falls in the silver price.

We think SS1 has been oversold in response to the pullback in the silver price over the last week:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

JBY recently acquired a high grade silver project in Texas, to go with its gold development asset in Nevada, and raised $30M to support progress on both.

JBY’s share price has been nicely churning through the 65c placement stock over recent weeks.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think AL3 has spent a while forming a new base for its next move.

AL3 had a bit of a news vacuum, but came back this week with a $4.5M sale for two 3D printing systems to the biggest shipbuilder in the US - a subsidiary of $18BN Huntington Ingalls.

Even with that big news, AL3 also got caught up in last week's broader small cap stock sell off...

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The common theme is that all share prices need to “decide” which direction to move in next.

How long does it take before we see an outcome? No one knows...

IF the companies can deliver strong news, from a solidly formed base AND while the market is in a good mood - it should take their share prices higher.

A lot of it depends on whether the small end of the market is feeling bullish or bearish.

We are predicting the bearish mood of the last couple of days will be short lived.

Taking the example of the 2020-2022 lithium bull run.

The first burst of enthusiasm was right after COVID hit and immediately got met with selling.

We remember when one of our best ever Investments, Vulcan Energy Resources was at $1.20 (up ~500%) by October 2020 and many were calling an end in the lithium rally (and Vulcan).

People thought the market would slow down into Christmas and many got it wrong.

“Surely this lithium price sentiment can’t last longer than a few months”

By mid January 2021, Vulcan hit $9... and then by September 2021 was at ~$16 per share.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

From start to finish the last lithium bull run lasted almost 2 years.

The US critical minerals macro thematic only just started getting any real traction in about June this year...

So it’s only been ~4 months.

And we certainly didn’t see this level of urgency and capital flying around from the US government for lithium, like we are seeing now for the current cohort of minerals deemed “critical” and of strategic importance by the USA.

We think there is still so much that can play out with this whole thematic...

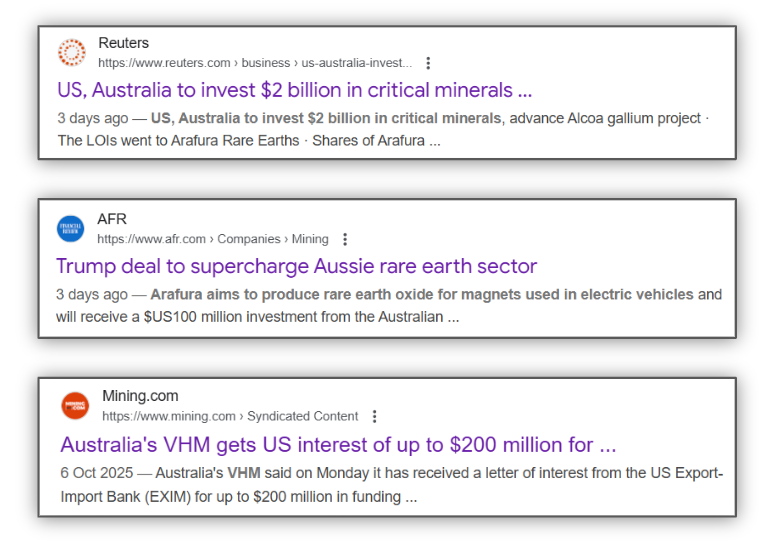

Some big news in the US critical minerals macro theme this week

The biggest news without a doubt was the US$8.5BN critical minerals and rare earths “Mining and Processing” deal signed between the US and Australia which would see:

- $1 billion in financing mobilised for new projects in mining and processing (within 6 months).

- Streamlining approvals to accelerate project delivery

- Investing in recycling technologies to manage e-waste and black mass scrap

- Establishing a Rapid Response group to secure priority mineral supply chains

(Source - read the full agreement)

(yes, the irony is not lost on us that the small end of the market, including small US critical minerals stocks, started its correction around at the same time that this deal was announced)

Then almost immediately off the back of that deal, the US government announced:

- US$200M investment in Alcoa’s Wagerup alumina refinery to build a gallium processing plant in Western Australia.

- Up to US$300M financing from the Export Important Bank (EXIM) in an LOI and up to US$100M investment from Export Finance Australia into Northern Territory rare earths developer Arafura Resources.

- Up to US$200M financing from EXIM in a LOI and up to $75M investment from Export Finance Australia into Victorian rare earth and mineral sands developer VHM

- Up to US$122M financing from EXIM in a LOI into magnesium plant developer LMG

- Up to US$67M financing from EXIM in a LOI into New South Wales scandium developer SRL

We also saw a ~$730M offer get announced for Larvotto Resources - from the USA’s only antimony smelter operator US Antimony Corp.

We are finally starting to see US capital get committed to ASX listed companies...

“Committed” being the keyword here...

The US government (and corporates) still need to go through months of approvals and documentation before any cash actually lands in the ASX listed company accounts.

Once the cash transfers happen, the wealth effect will surely come into full effect for ASX listed companies (more cash, more progress on assets should mean higher valuations).

And then it becomes a case of what the companies do with their bigger valuations.

An example of this is the Larvotto/US Antimony Corp dealings.

US Antimony Corp received a US$245M deal from the Pentagon which took its market cap up to a high of over US$3BN briefly.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

US Antimony Corp then had to justify that valuation (and source feedstock to supply into that Pentagon deal), so it went and tried to takeover a company which could help solve both problems.

We think there will be many, many more of these type deals where there is a rush to do M&A in assets that have exposure to the US critical minerals macro thematic.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.