SLM is drilling for new copper discovery “imminently”. Peer delivered 700% re-rate a few months ago

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 363,637 SLM Shares and 1,750,000 SLM Options and the Company’s staff own 235,294 SLM Shares and 117,647 at the time of publishing this article. The Company has been engaged by SLM to share our commentary on the progress of our Investment in SLM over time.

The drill permit is (finally) in.

The cash has already been raised.

The drill contractor is ready.

Years of technical work has led up to now.

Time for another ASX micro cap stock to make a new copper discovery?

Our sub $10M micro-capped copper-gold exploration Investment Solis Minerals (ASX:SLM) is about to start drilling with the goal of making a new copper discovery in Peru.

Today it just received some long awaited approvals to begin drilling on one of its key targets.

A 7,500m diamond drilling campaign is due to begin ‘imminently’.

A discovery could significantly re-rate SLM over the coming weeks and months - keep scrolling to see what could happen to the share price...

(no guarantees of a successful discovery of course)

A second drill permit is expected imminently for another key target, and drilling there will kick off as soon as the permit is granted.

So two big shots on goal for a potential company making copper discovery from a micro cap stock over the coming weeks...

SLM raised $4.5M in late February, so has the funding runway to drill both targets.

This also means SLM has a tiny enterprise value right now (especially after yesterday’s market bloodbath where everything got sold down).

SLM’s market cap will be ~$9.8M (at 7c, after the placement shares are issued) with over $5M in cash on hand (at 1 March 2025).

So SLM’s enterprise value going into drilling is circa ~$5M.

Interestingly, SLM’s directors also invested $205k in the February capital raise - we like it when company boards are aligned with shareholders.

Also, a prominent resource fund, Lowell Resources Fund, invested in that same capital raise.

Lowell has a strong track-record in resources investing, and it's not too often that institutional money comes into a micro-cap stock pre-discovery - so they must like what they see.

Historically, there has been very little drilling over these targets which makes them greenfields exploration.

We like high-risk, high-reward drilling... because anything can (and does) happen.

How might the market react to a discovery by SLM?

Well, we don't have to look far back into history to find an example.

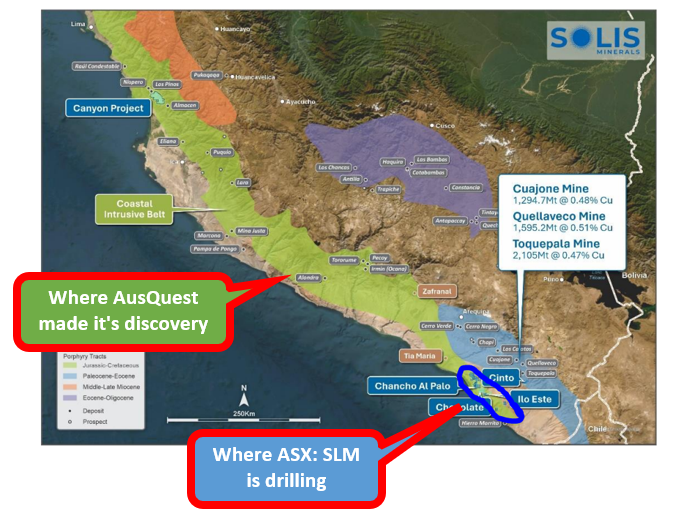

In January this year, ASX-listed AusQuest made a new copper discovery in Peru that delivered a quickfire ~700% share price rise.

AusQuest is now capped at $66M post discovery - about 7x the value of SLM (pre discovery).

SLM’s projects are located along the same coastal belt in Peru as AusQuest.

Since the discovery hole,(despite the broader market volatility) AusQuest’s share price has also held its valuation post discovery:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think this market response shows the warm reception new copper discoveries get from the market from tiny companies, especially when they are in proven copper jurisdictions like Peru.

Incidentally, the region that SLM is exploring in, and where AusQuest made its discovery, hosts several major international copper mining companies in production or with advanced projects, including Southern Copper, Teck, and Anglo American.

Here you can see on the map where both SLM and AusQuest sit in Peru:

SLM has the right team for a discovery

We are backing the SLM team here:

- SLM’s Chairman is Chris Gale - Chris was Managing Director of Latin Resources and led the team that made a lithium discovery in Brazil, which was one of our best ever Investments and at its peak was up 2,332% from our Initial Entry Price. Latin was taken over by lithium producer Pilbara Minerals in a ~ $0.6BN takeover deal.

- SLM’s Managing Director is Mitch Thomas (Latin’s former CFO) - Mitch has a solid background in Peru and in copper having spent 3 years at Rio Tinto’s 4.32BN tonne La Granja Peruvian copper project.

- SLM’s technical director is Mike Parker - Mike was the senior country manager for (the now $15BN) First Quantum, where he was responsible for two major copper discoveries (Lonshi and Frontier Mines). Then, between 2011 and 2017 he was First Quantum’s country manager in Peru.

As is often the case with exploration, it is a bet on a geological thesis and the team behind the company doing the drilling.

We think SLM’s team has the right mix of expertise to get the most out of SLM’s projects.

If there is a discovery to be made, then we back this team to deliver it...

SLM is now:

- Well funded with >$5M cash on hand as at 1 March 2025. ✅

- Has four highly promising projects to drill, with 7,500m set to start imminently. ✅

- Is in the same region, and has the same type of targets as another discovery made by an ASX listed junior that re-rated ~700%. ✅

- And has the backing of a small cap resources fund with a track record of successful investments. ✅

Here’s more on what to expect from SLM as it sets itself up for a big 2025 chasing a new copper discovery in Peru...

SLM will be diamond drilling 7,500m on its first target

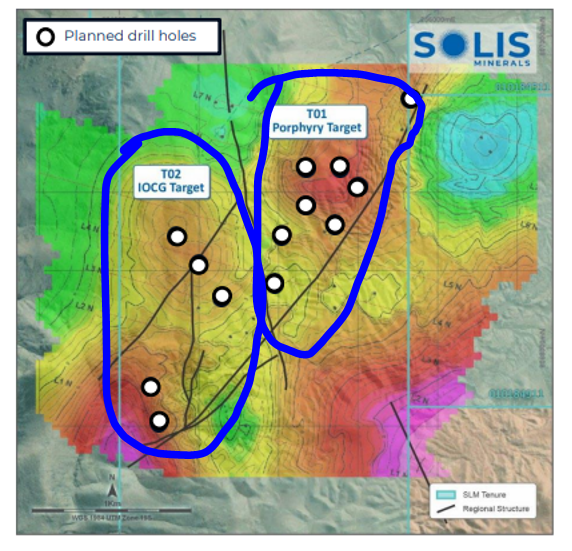

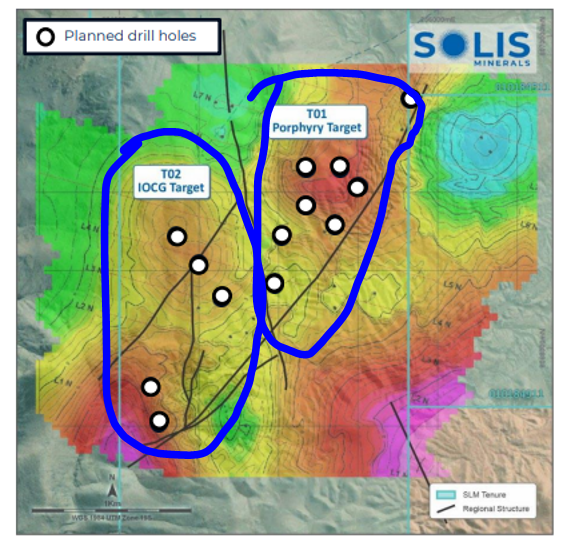

Today’s news is for drill permits on one of SLM’s projects (Chancho Al Palo) where it will be testing both IOCG (Iron oxide copper gold) style mineralisation and porphyry potential.

Permits for a second project (Ilo Este) are scheduled to land in the following weeks.

Here are the two targets SLM will be drilling at Chancho Al Palo:

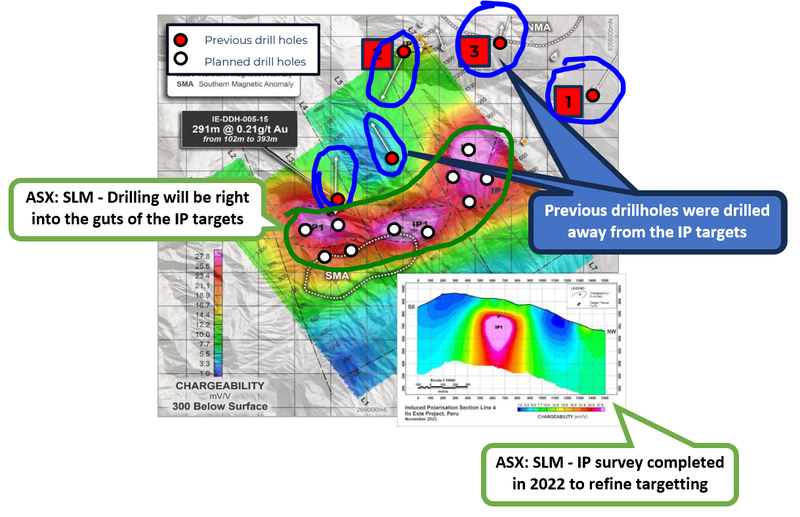

At Ilo Este SLM will be following up newly shot IP surveys (geophysics completed by SLM in 2022):

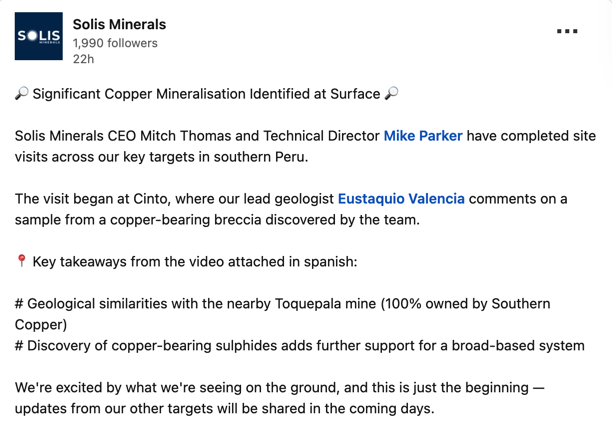

At another of its projects “Cinto” - SLM recently uncovered the below huge vibrantly coloured piece of brecchia that hosts copper mineralisation - click the link below to watch the video on Linkedin.

The plan is for this asset to be drilling in the second half of 2024.

(Source)

SLM’s four “shots on goal” for 2025.

SLM has four different projects it plans to drill this year with the goal of making a copper-gold discovery.

Here is our rapid fire take on each of those projects:

Project #1: Chancho Al Palo - Drilling to begin imminently

SLM anticipates drilling to start “immininently” and will be drilling five holes over a 2,500m drill program (with scope for expansion after initial drilling).

Assay results from the drilling are expected within two to four months.

Why is this project interesting?

Here SLM has two different targets - one is an IOCG target, the other a porphyry target.

Both targets were ranked highest after SLM ran geophysical surveys (IP survey) on the project.

Both targets also sit inside Peru’s “Coastal Belt” - which is where ASX listed AusQuest made its discovery and re-rated by ~700%.

The coastal belt targets are lower altitude and a lot easier to access than up in a mountainous region, so any major discovery here could be valuable from an economic perspective.

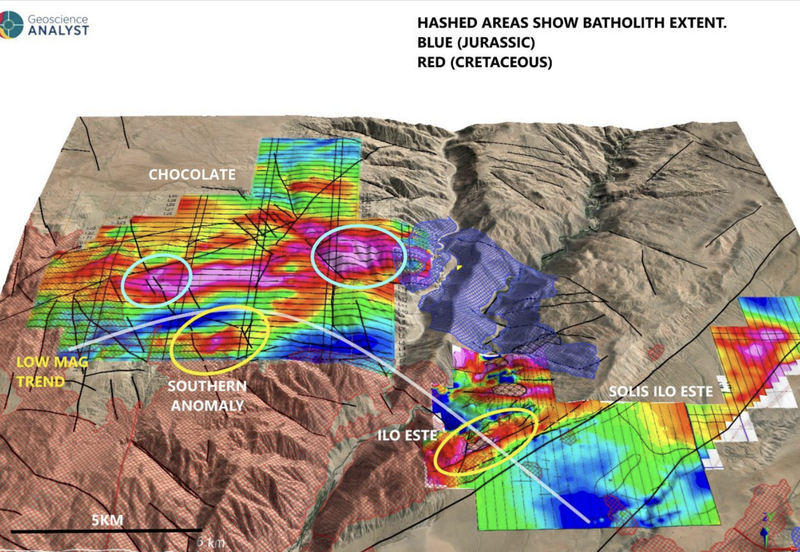

Project #2: Ilo Este - Permits expected in coming weeks, then drilling to immediately begin

Ilo Este is the next project SLM expects to drill.

This project sits ~17km away from the project SLM is drilling first.

As soon as drilling on Chancho Al Palo is done, we expect to see the rig move over to Ilo Este for a 5,000m drill program.

Why it is interesting:

The target here is a big porphyry discovery.

This project had previously been drilled, returning intercepts of ~472m at 0.11% copper with 0.09g/t gold grades.

BUT the drillholes just missed the main targets...

SLM ran an IP survey (geophysics) in 2022 which showed just how close that old drilling got.

We are particularly looking forward to the drilling on this project because of the results from all the old drilling (albeit at lowish grades).

SLM will be the first to drill the big geophysical (IP) targets properly which we are looking forward to seeing the results from:

Project #3: Cinto Project - Drilling in H2 of 2025

Stage: Permitting / Target Generation

Why it is interesting:

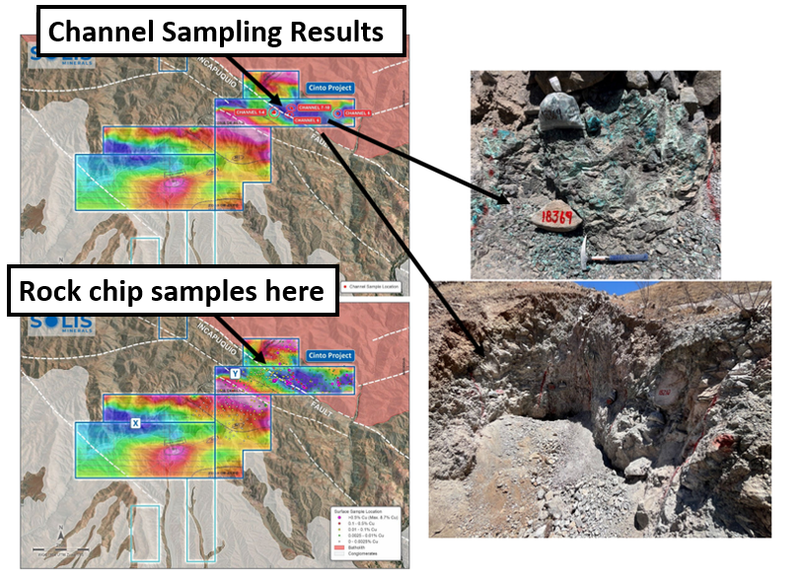

It is just 10km away from the Toquepala mine that produces 180,000 tonnes of copper each year. Importantly, channel and rock chip sampling results seem to line up in the North Eastern part of SLM’s project...

What is next: IP survey this quarter & drill permitting

When does SLM expect to drill: H2 of 2025

Project #4: Chocolate - drilling planned for Q4 of 2025

Why it is interesting:

The Chocolate project sits between SLM’s two other main projects Chancho Al Palo and Ilo Este which explains the timing preference.

IF SLM has success at those prospects, then drilling Chocolate would probably become more of a priority for the company.

When does SLM expect to drill: Q4 2025

What’s Next for SLM?

Drilling.

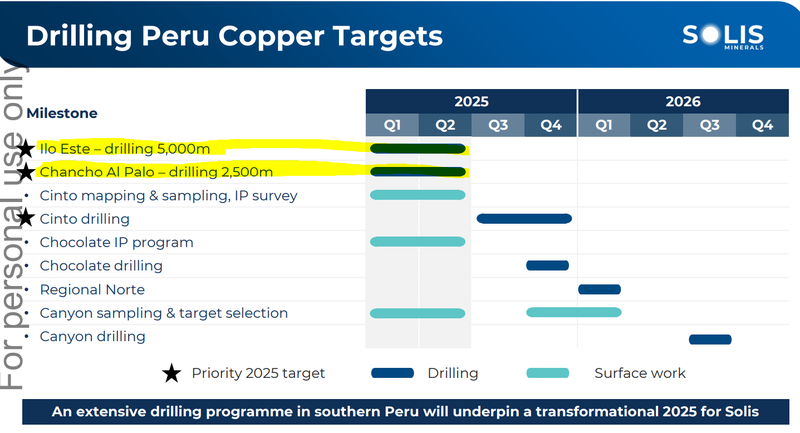

In February, SLM released a timeline for drilling at each project:

🔄 Drilling

After today’s announcement the main news we will be looking out for over the coming months will be drilling on Ilo Este and Chancho Al Palo.

SLM expects drilling to take 2-4 months (including assay turnaround times).

So we could see some results come in before the end of Q3.

🔄 Permitting

We now have a drill permit for Chancho al Palo.

We are still waiting for permitting on SLM’s other three main targets for the year.

Here’s what's still to come:

- Drill permits for Ilo Este - anticipated to be a few weeks away

- Drill permits for Cinto

- Drill permits for Chocolate

🔄 Additional exploration work to firm up drill targets

SLM plans to conduct further induced polarization (IP) surveys at Cinto to refine drill targets, with a first-pass drill program anticipated for 2025.

What are the risks?

With drilling about to start, the main risk for SLM in the short term is “exploration risk”.

There is no guarantee that SLM will make a discovery with its drill program.

SLM has committed to 7,500m of drilling and if nothing economically viable is found, the company’s share price could be re-rated lower.

Exploration risk

SLM’s projects are all considered early stage prospects. This means SLM is yet to make a discovery on the projects. Inherently there is a risk that drilling programs return results with no mineralisation and the projects are not considered valuable.

Source: “What could go wrong” - SLM Investment Memo 9 July 2024

We list more risks to our SLM Investment in our SLM Investment Memo here.

Our SLM Investment Memo

In our SLM Investment Memo, you can find the following:

- What does SLM do?

- The macro theme for SLM

- Our SLM Big Bet

- What we want to see SLM achieve

- Why we are Invested in SLM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.