SLM: First hole, visual mineralisation from surface - more holes to come and assays in a few weeks

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 363,637 SLM Shares and 1,750,000 SLM Options and the Company’s staff own 235,294 SLM Shares and 117,647 SLM Options at the time of publishing this article. The Company has been engaged by SLM to share our commentary on the progress of our Investment in SLM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

A very nice first hole...

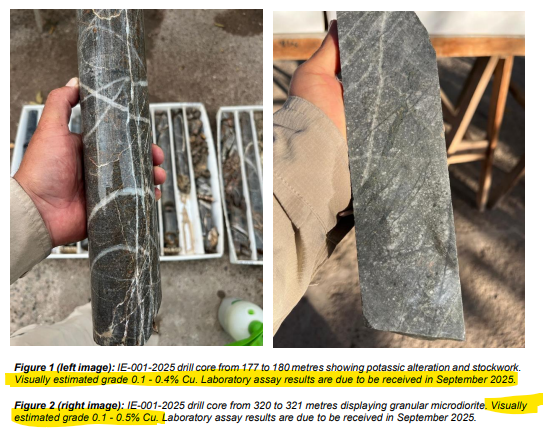

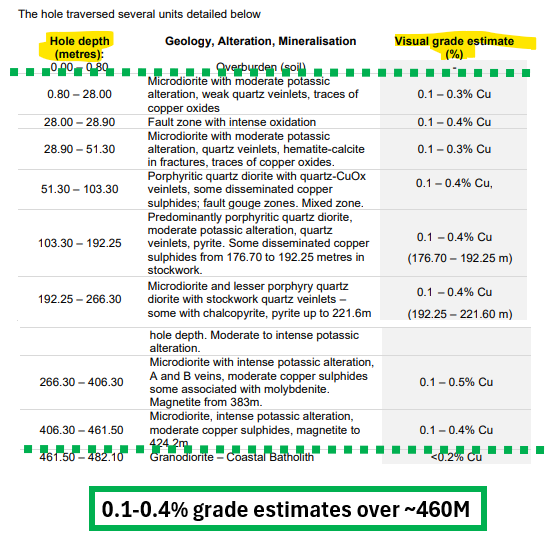

Solis Minerals (ASX:SLM)’s onsite geologists have eyeballed the latest drill cores to come out and seen “extensive” porphyry copper from surface at grades they estimate to be between 0.1% to 0.4% copper...

SLM has the right type of rocks - “copper in a porphyry setting”.

And visual mineralisation extending ~460m from surface...

And visual estimates of grades range from 0.1-0.4% copper.

If all of that translates to strong lab assay grades of copper and gold it could be a quite the first hit from the target we were most looking forward to see SLM drill this year.

IF the coming lab test results confirm the visual estimates announced today... this could also come in better than the discovery intercepts that triggered a ~700% rally in ASX listed AusQuest’s share price (on similar targets, also in Peru).

(noting that visuals are not an accurate estimate, the lab assays will give us the best understanding of grades - they are due in a few weeks time. Also the past performance of AQD is not an indicator of the future performance of SLM)

SLM clearly like what they are seeing too with these Ilo Este assays being “prioritised ahead of Chanco al Palo assays” that had already been drilled earlier this month.

And SLM still has ~4,500m of drilling to come on this project... today’s hole was for ~482m out of a total 5,000m planned.

Solid start so far... now we wait for the assay results to be announced.

Assay results from today’s announcement are due in the coming weeks which is when we will get a proper understanding of mineralisation grades.

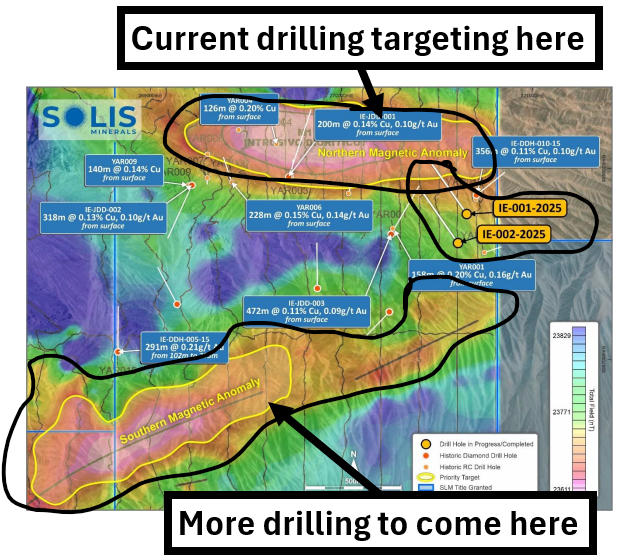

SLM is now moving over to drill a second hole into the same structure ~200m to the south-west of the first hole.

And will be drilling a number of other holes as part of the ~5,000m diamond program across two geophysical anomalies (to the north where drilling is happening now, and to the south which is largely undrilled):

(SLM has two other copper exploration projects in Peru that will be drilled later this year and in early 2026, but more on those later).

Today’s announcement is from the first hole on SLM’s Ilo Este target - where SLM is looking to make a big copper-gold porphyry discovery.

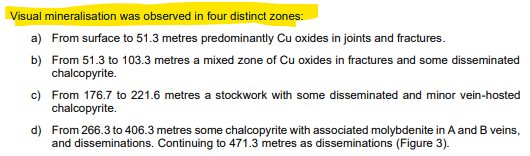

And based on visual estimates, SLM is already seeing visual mineralisation across four distinct zones from its first drillhole:

And those zones stretch over ~460m...

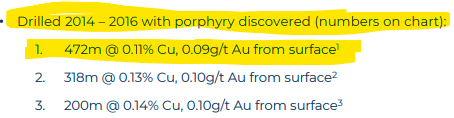

We already know that SLM’s project has been drilled in the past and delivered assay results like ~472m at 0.11% copper with 0.09g/t gold grades, from near-surface...

(Source)

Today’s visual estimates make us think that SLM could produce similar (if not better) results.

Firstly, because the visual estimates of grade are looking a lot better in this hole (estimated between 0.1-0.5% copper.

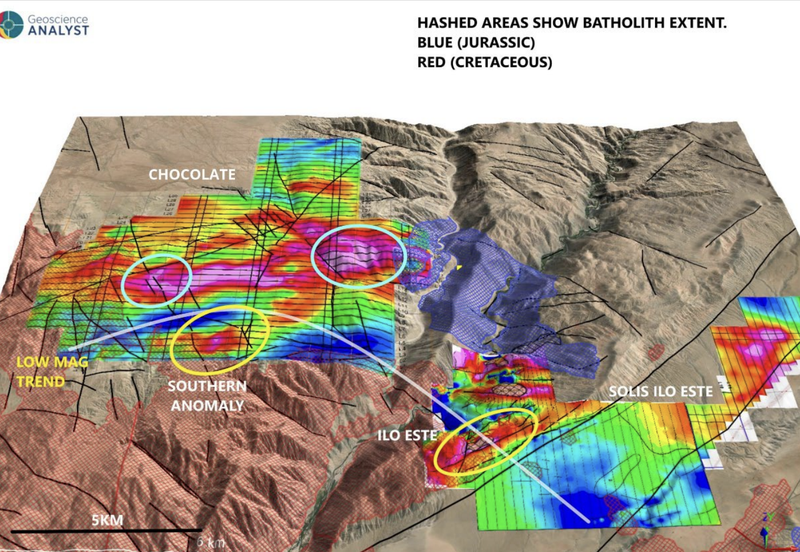

And secondly because SLM is now drilling with the benefit of IP geophysical data which was done by SLM in 2022.

(IP surveys send down electrical currents and look for rocks that are conductive... if it finds the right type of rocks it produces those bright coloured “chargeability” anomalies in the image below).

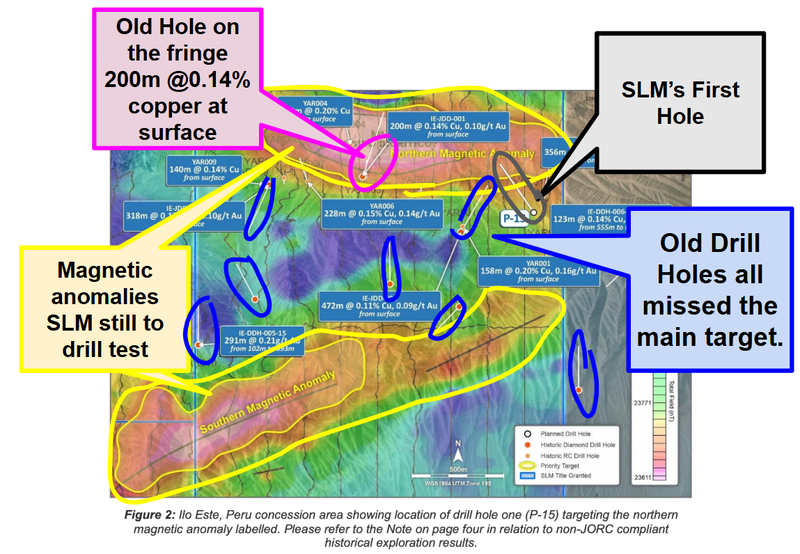

The previous drilling on this asset was done “blind” without any of that geophysical data - which meant most of the old drillholes completely missed where the geophysics would have suggested are the best drilling locations.

Here is where those old drillholes were placed relative to the higher chargeability (brighter colours) which are usually marker for where to drill:

So far so good from SLM’s first hole (visually) - now we just need assays to deliver monster 400m hits with grades ranging in that 0.1-0.4% range so that the market can start comparing SLM’s results to other companies that have re-rated on similar results...

AusQuest rallied 700%+ off results similar to historic holes on SLM’s current project

We think there is a chance SLM could deliver assay results on par (if not better) than another ASX listed company that rallied by ~700% earlier this year - ASX listed AusQuest.

(at the same time it's no guarantee, minerals exploration is risky, and the past performance of AusQuest is not an indicator of the future performance of SLM.)

Earlier this year AusQuest made a major copper discovery in Peru.

AusQuest is now capped at $50M post discovery - about 3.3 times SLM’s current market cap of ~$15M.

Earlier in the year it traded at a market cap above $100M.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

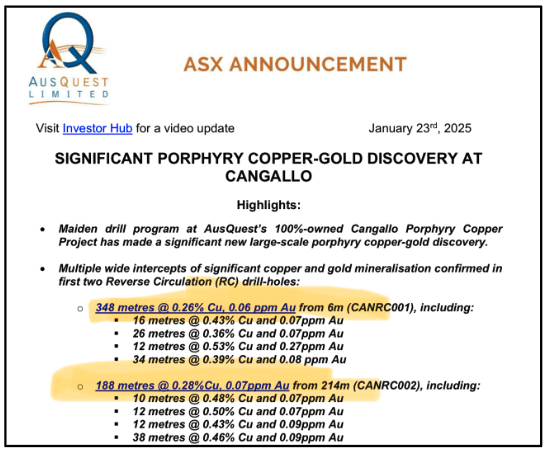

Here is the discovery announcement that triggered the AusQuest re-rate:

The two discovery holes that AusQuest announced were: 348m at 0.26% copper and 188m at 0.28% copper.

There have been pretty similar old holes on SLM’s project including 158 metres at 0.20% copper and 0.16 g/t gold from surface.

and of course SLM’s big one which hit 472m at 0.11% copper with 0.09g/t gold grades, from near-surface...

And now we have visual mineralisation across ~460m in SLM’s first hole from this project.

IF we see assay results returned with grades and widths comparable to those historic holes then we think the market could start to compare AusQuest and SLM...

And notice the valuation difference... i.e. we think SLM might re-rate upwards to levels approaching AusQuest.

Once again - this also might not happen - success is no guarantee, this is high risk exploration in a small cap company.

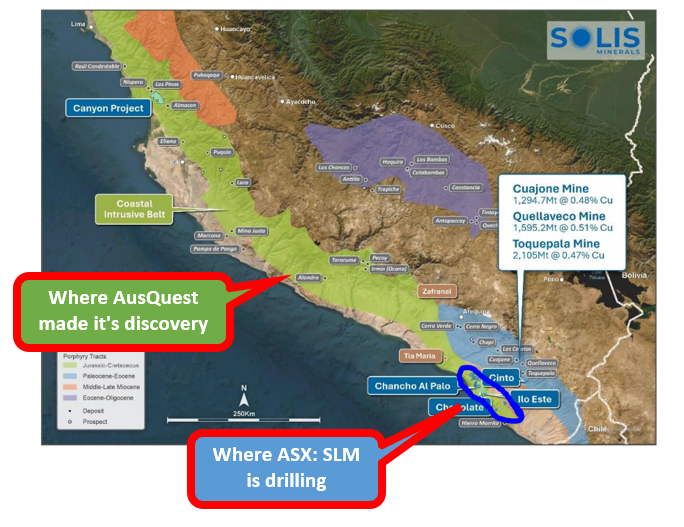

There could be a reasonable comparison because both AusQuest and SLM are looking for similar deposits in the same “coastal belt” in Peru:

Ultimately, we are hoping that with drilling at Ilo Este SLM can deliver our Big Bet which is as follows:

Our SLM Big Bet:

“SLM discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our SLM Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

ASX:SLM

Why we are Invested in SLM

We initially published the below reasons for our Investment in our SLM Investment Memo from the 9th of July 2024.

Below, we have included some updates for things that have changed since then:

- Latin Resources success - We have had success Investing in Latin Resources which made a hard rock lithium discovery in Brazil and re-rated to a peak market cap of ~$1BN. Latin is now being called “Sigma 2.0” due to it following the nearby $1.8BN Brazilian lithium producer Sigma Lithium. In a similar way, we hope to see SLM become a “Latin 2.0”.

Update: Latin Resources was acquired by the $6.9BN lithium producer Pilbara Minerals in a deal that valued Latin at circa $560M. - Same team as Latin Resources (Latin 2.0?) - SLM is backed by the same team that delivered Latin Resources discovery last year. Latin’s Managing Director Chris Gale is SLM’s non-executive Chairman. Chris Gale has taken Latin from a ~$5M market cap multi-asset early stage explorer (similar to where SLM is now) to a peak market cap of almost $1BN off its lithium discovery in Brazil. Latin is now fully focused on bringing its Brazilian lithium discovery into production.

Update: SLM has since brought on board Mitch Thomas as its CEO. Mitch was Latin Resources' CFO and was with Chris through to the A$560M deal being done with Pilbara Minerals. - Latin Resources is SLM’s biggest shareholder - Latin Resources holds ~15.3% of the company (as of 3 May 2024) which should mean they are incentivised to see SLM succeed. We hope that SLM can leverage its Latin Resources connection to deliver success in acquiring valuable projects in South America..

- Latin Resources has a big investor following - SLM should benefit from the crowd of investors that follow (and have made money from) Latin Resources (Latin Resources has ~12,900 shareholders).

- Copper price near all-time highs - Copper is trading at US$4.60/lb and could push higher as the electrification and decarbonisation macro themes get stronger.

Update: The copper price briefly hit all time highs a few months ago at ~US$6 per lb. Now it's trading around ~US$4.55 per lb again. - Lithium bear market could throw up opportunities - SLM has publicly stated it is looking at making new lithium acquisitions. With the current bear market in lithium stocks, SLM could find interesting exploration ground at a reasonable valuation.

- Tiny enterprise value (EV) means leverage to a discovery - At the time of this memo SLM has an EV of ~$2M, which we think means that the company is highly leveraged to a re-rate in the event of successful drilling results.

Update: SLM’s current market cap is ~$15M which is higher than when we first published our SLM Investment Memo back in July 2024. SLM is now more advanced, drilling now, which means it's close to a potential discovery.

A big part of our SLM Investment is the Latin Resources connections - here’s why

Four of the 7 reasons we are backing SLM have to do with the Latin Resources team behind the company.

Latin Resources was one of our best ever Investments.

Latin was capped at just $15M when it discovered a giant lithium deposit in Brazil and was eventually taken over by Pilbara Minerals in a deal worth over $500M.

At its peak, Latin was up ~2,332% from our Initial Entry Price.

(past performance of Latin is not an indication of future performance of SLM)

You can hear the full story from SLM’s Non-exec Chair Chris Gale and CEO Mitch Thomas in the podcast here:

(Source)

What’s next for SLM?

🔄 Assay results from first project (Chancho al Palo)

We want to see the final assay results from the drilling done at Chanco al Palo

🔄 Drilling Second Project: Ilo Este

After today’s visuals, we want to see assay results from Ilo Este. These are now expected to arrive before assays from Chanco al Palo.

After that, we will be watching to see if we get more visuals in the next batch of holes.

SLM is running a ~5,000m drill program over this project.

🔲 Permitting on two other projects.

We mentioned earlier that SLM is drilling four different projects this year.

We did a deep dive on all four projects in our last note here: An update on SLM’s 4 shots on goal

Across the two remaining undrilled projects, we are waiting to see SLM get drilling permits granted.

Here is a quick update on those two remaining projects:

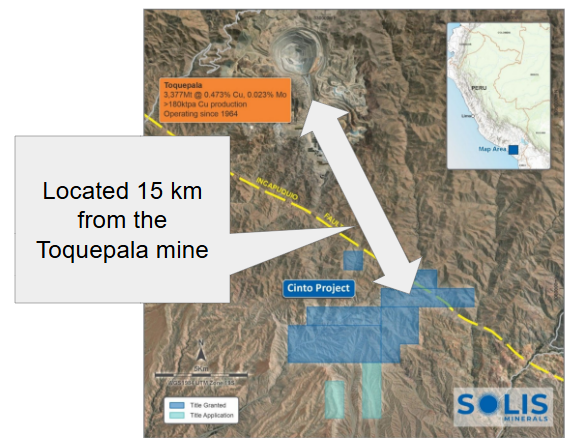

Project 3: Cinto Project

Stage: Drill targets identified, permits pending.

When is it drilling: Q4 this year

Why it is interesting:

SLM’s drill targets here are ~15km away from the Toquepala mine which has a 3.3BN tonne copper resource and is producing over 180,000tpa copper:

Project 4: Chocolate (previously Guaneros)

Stage: Target generation

When does SLM expect to drill: Q4 2025 - Q1 2026

Why it is interesting:

The Chocolate project sits between SLM’s two other main projects Chancho al Palo and Ilo Este. A drone magnetic survey conducted by SLM showed that the area was potentially prospective for gold and copper - similar to what was found at Ilo Este.

What are risks?

Now that drilling has commenced the biggest risk for SLM is “Exploration Risk”

There is no guarantee that SLM will make an economic discovery with its drill program.

There is also no guarantee that the visuals announced today will return final assay results that are considered economic enough to declare any new discoveries.

If nothing economically viable is found, the company’s share price could be re-rated lower.

Exploration risk

SLM’s projects are all considered early stage prospects. This means SLM is yet to make a discovery on the projects. Inherently there is a risk that drilling programs return results with no mineralisation and the projects are not considered valuable.

Source: “What could go wrong” - SLM Investment Memo 9 July 2024

SLM held ~$3.3M of cash at May 31 2025.

7,500m of drilling in Peru will cost money and as SLM has no means to generate its own revenue, it may need to secure finance again from the market at some point in the future.

The share price could be lower when this raise is done, diluting any new investors that come in at a higher price.

Funding risk

SLM is a very early stage exploration company with zero revenue and is reliant on regular capital raises (or attracting a farm in partner) so it can undertake high-risk / high reward exploration programs. There is a risk that market conditions deteriorate and investors shun high-risk explorers like SLM, and SLM is unable to raise capital without significant dilution of existing shareholders.

Source: “What could go wrong” - SLM Investment Memo 9 July 2024

Another risk for SLM is permitting/delay risk.

If SLM is delayed in securing final drilling permits it could delay the drilling program and cost the company valuable time and money while it has the drill rig secured.

We list more risks to our SLM Investment in our SLM Investment Memo here.

Other risks

Like any stock, investing in SLM carries other risks which may affect the value of the company, some which are unable to be identified (this is the nature of risks).

The company's projects are all early-stage exploration assets with no established mineral resources or reserves. There is no guarantee that SLM will make an economic copper-gold discovery or that any discovery will prove commercially viable for mining operations.

SLM is highly sensitive to fluctuations in copper and gold commodity prices. Any sustained downturn in these prices could materially impact the project economics and the company's ability to attract investment or secure funding.

The company operates in Peru, exposing investors to significant country risk including potential changes in mining regulations, taxation policies, environmental requirements, and political instability.

Social license risks are also a factor here.

Permitting and regulatory approvals present ongoing execution risks. Any delays or rejections could materially impact timelines and investor confidence. Environmental and social permitting processes in Peru can be complex and time-consuming.

Finally, technical and operational risks are inherent in exploration activities, including the possibility of drilling programs failing to intersect mineralisation, adverse geological conditions, equipment failures, or delays in obtaining reliable assay results from laboratories.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our SLM Investment Memo

In our SLM Investment Memo, you can find the following:

- What does SLM do?

- The macro theme for SLM

- Our SLM Big Bet

- What we want to see SLM achieve

- Why we are Invested in SLM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.