Silver price about to break out? SS1 delivers high grade extensional hit.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,051,936 SS1 shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time.

Silver has been on another strong run the last few weeks.

On Friday, silver nearly hit US $33 per oz...

Higher than the 10 year record it broke in May this year.

And a new 12 year high.

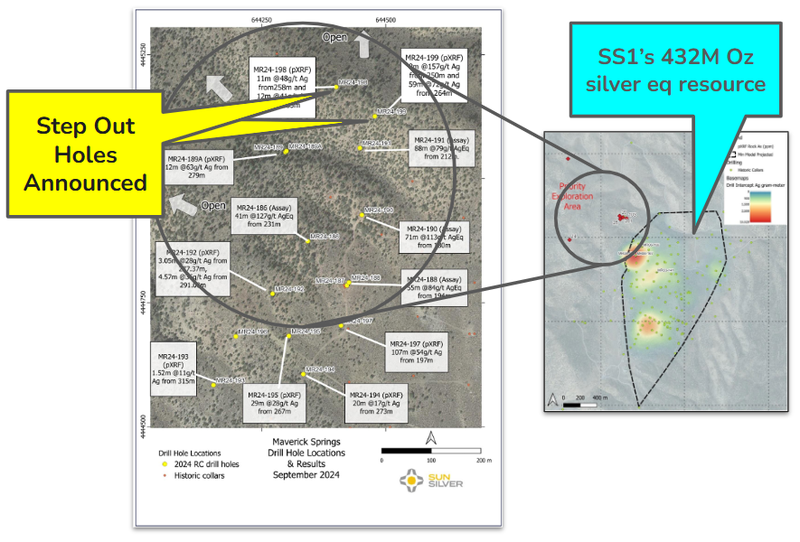

Sun Silver (ASX:SS1) already has the largest primary silver resource on the ASX at 432M ounces of silver equivalent.

While the silver price is moving up, SS1 has been drilling extensional holes to grow its 423M silver oz equivalent resource even further.

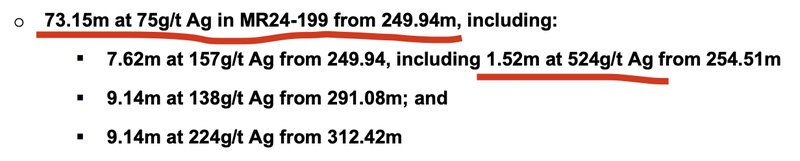

This morning SS1 announced a 73m thick intercept OUTSIDE of its current resource estimate.

Within the 73m intercept SS1 hit a peak grade of ~524g/t silver via pXRF readings.

(The average grade across the intercept was ~75g/t silver)

(Source: SS1 Announcement 8 October 2024)

These cores will be sent for proper assays with the final result expected in the coming weeks.

The big takeaway for us was that the intercept was a full 150m away from previous drilling done on SS1’s project.

So we are seeing some genuine “never been drilled” parts of the project being tested...

And delivering high grade results (pXRF for now, assays pending...)

Last month, SS1 raised $13M, comprising $5M raised at 80c per share and $8M at 62c a share.

In that raise, SS1 brought on a strategic cornerstone investor Nokomis Capital, onto the register - who now has a ~9% stake in SS1.

Nokomis Capital also has positions in gold giant US$41BN capped Agnico Eagle and US$1.4BN capped Mag Silver.

It's always a good vote of confidence when deep pocketed sophisticated funds come into an ASX small cap in a big way.

SS1 is now well funded to execute over the coming months.

Our view is that for SS1 to continue delivering share price re-rates, we need two things to happen over the next few months:

- The silver price keeps tracking upward each week OR goes on a big run.

- AND SS1 keeps delivering high grade EXTENSIONAL hits and eventually an upgraded JORC resource.

Silver at its current levels (~US$32 per ounce) is already great news for SS1 given its giant 423M ounce silver equivalent JORC resource.

But a US$50 per ounce silver price AND 500M ounces of silver equivalent would be a whole lot more interesting.

(Obviously a few things need to go right and a bit of luck for both scenarios to occur)

The silver price keeps threatening to breakout and has now knocked on the door of $33 per ounce.

While silver’s recent rise has been a slow weekly grind upwards, usually there is a trigger moment after a certain level is broken when things start moving a lot quicker.

(it may of course cool off again for a couple of months like it did back in May)

Silver (and gold) have in the past gone on strong price spikes in short periods of time.

Usually during uncertain times of war and/or instability in financial markets.

Silver and gold demand rises significantly when faith is shaken in fiat currency and in times of potential war and instability.

But silver isn’t just “wealth insurance” in uncertain times - industrial demand is also a big part of the silver story.

Silver is used in solar panels, and demand for it is expected to grow exponentially over the next two decades as the world embraces solar power.

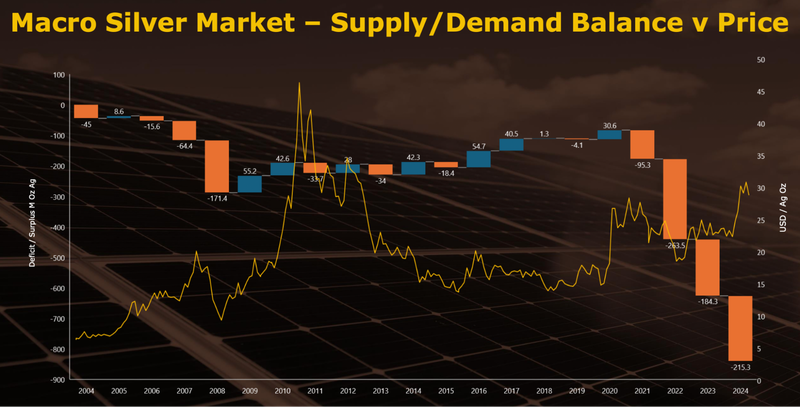

Silver mining is already in a deficit because of demand from industrial users and precious metals buyers.

Responding to deficits isn't easy either. ~72% of silver is mined as a “by-product” of mining other metals (like zinc, lead and copper).

So if the silver price goes up, it does NOT mean that zinc, lead and copper mines will increase their production to satisfy the demand, as silver is not their main business - this exacerbates the shortage in supply (more on this below).

SS1 is a “primary” silver resource, meaning that its main product will be silver, hence it is highly sensitive to the silver price.

(which is good when the silver price looks to be going on a run)

With the silver price on Friday looking like it was about to break into a run, over the weekend we did some reading about the silver market in particular and we came across this concept of the “Silver & Gold Mega Bubble”.

What is the Silver & Gold Mega Bubble?

“I own gold because I am afraid, not hopeful, that it is going to go to $7,000 or $8,000”.

This quote by Rick Rule perfectly encapsulates the sentiment behind the gold and the silver mega bubble.

At today's gold/silver ratio, if gold hit US$8,000 per ounce, silver would trade at ~US$100 per ounce.

When faith in fiat currency is shaken, particularly the US dollar, everyday people pile into alternatives like gold and silver (and more recently bitcoin).

It's hard to imagine in Australia where the exchange rate with other currencies is pretty stable and strong.

But think of a country like Argentina or Lebanon which lost 78% and ~90% of their values against the USD in 2023.

Compared to silver... it was even worse.

Here is how the silver price appreciated against the Argentine Peso over the last 5 years.

Had a local decided to take all their pesos and buy silver in 2021 they would be exponentially better off than holding the domestic currency.

(an excellent strategy in hindsight of course - and this is not financial advice)

Here in the West, we don't really consider a world where our currencies are depreciating at that kind of rate.

But IF the confidence in USD, Euro or AUD is lost as it has happened in other parts of the world, rapid silver price appreciation can happen here too.

Most of the time, these depreciation events happen when a government racks up more debt than it can afford, eventually leading to money being printed to repay that debt.

Usually, the money printing starts when the debt has reached a point of no return, which means the country has to print significant amounts of cash to repay those debts.

Printing money leads to the currency losing its value, which then leads to a loss of confidence - a negative feedback loop that can spiral into what we saw in Argentina.

Our view is that the big move - the one where prices can reach levels that seem ridiculous to think about right now - happens when confidence is lost in the reserve currency (the USD).

(We track the silver price against the US dollar)

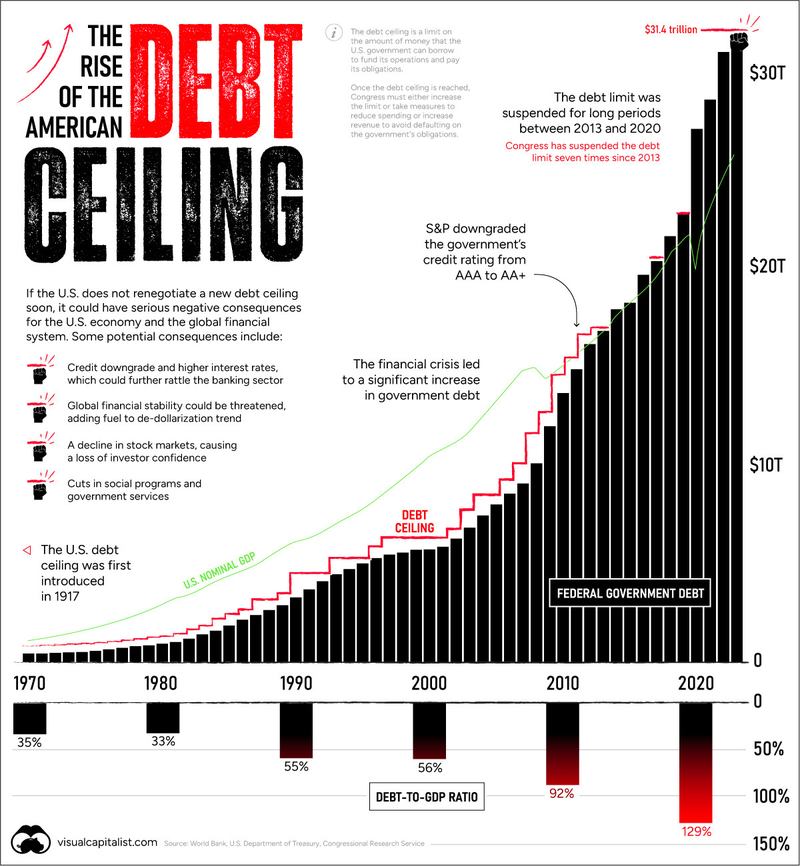

The US has $35 trillion in public debt and spends ~50% of all personal income taxes on just servicing the interest of that debt.

(Source)

Our view is that as global debt levels increase, the price of safe havens like gold and silver as “insurance” for a money printing doom loop scenario as we mentioned above.

US govt debt has been increasing sharply over the last 10 years - you can read more on the above image here.

None of this considers the expected industrial demand for silver, which we mentioned above, and have written about in detail in previous notes.

IF the silver price starts running, and enough people start second guessing the stability of the US dollar, we expect to see a wave of capital flow into the market looking for silver exposure.

And naturally, that cash will want to go into the company that has the most leverage to a running share price.

What happens to small cap mining companies when the silver price is running?

When the silver price is running due to excess demand, it will take some time before supply can catch up.

According to Metals Focus, mine production of silver is yet to catch up to higher silver prices because silver is generally a byproduct.

Only 28% of the silver supply is driven from primary mines.

(most of it is a secondary “by product” from lead, zinc or copper mines)

This means that the mined silver supply is generally slow to respond to an increase in demand as it is not the primary focus of that mine.

I.e a copper mine can’t increase silver production by making changes to its mine plan.

(Source)

If the silver price runs hard enough, silver projects like SS1’s start to become the go to exposure for investors to get leveraged silver exposure.

SS1 currently has the largest silver resource on the ASX and recently took over that mantle from Silver Mines Ltd.

Silver Mines ran into some permitting trouble recently which has delayed the advancement of its silver project in NSW.

During the last silver run in 2020, Silver Mines was considered a de facto silver ETF, where there was a premium placed on the share price due to being the largest silver company.

We think that SS1 has taken the mantle now and will be the de facto silver ETF for those looking for silver exposure on the ASX.

This is what we look for when Investing in development stage companies - big resources that increase in valuation in line with the price of the underlying commodity.

We have also seen moves from legendary investor Eric Sprott entering the silver equities market:

(Source)

For us, this is strong validation that now could be the time for the silver equity market to turn.

What SS1 has achieved since IPO and what’s next

Since SS1’s IPO in May, here’s what has happened:

- SS1 is currently the largest primary silver resource on the ASX... at a time where the silver price has reached a decade high and looks to break out.

- SS1 found antimony on its project... weeks before China banned antimony and sent the US government scrambling to secure domestic supply.

- SS1’s peer Silver Mines announced permitting issues... which drove capital and attention towards SS1 as the new de facto “silver stock” on the ASX.

- Finally, SS1 managed to raise capital from an institutional investor at a PREMIUM to its market price at the time.

With the recent capital raise, SS1 added $13M cash to its balance sheet.

This means it has plenty of cash to test the antimony potential of its project, buy “time” for the silver price to run & deliver silver resource upgrades.

In the short-term, we are looking forward to three main catalysts:

- More drill results from its exploration program (Visual/XRF/Assays).

- Re-assay of old drilling data for antimony so that eventually, the antimony can be included in SS1’s JORC resource.

- Any external grant funding from the Department of Energy (DOE) regarding SS1’s silver paste program or Department of Defence regarding antimony program.

...and of course the silver price breaking out past its 12 year highs and going on a strong run, which nobody can predict or control.

So far, a lot of the stars have aligned for SS1, we are hoping that the catalysts above help the company achieve our Big Bet which is as follows:

Our SS1 Big Bet

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SS1 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

What are the risks?

In the short term, the two key risks for our Investment in SS1 are “Commodity price risk” & “Exploration risk”.

First of all, commodity risk because SS1’s share price will ebb and flow with the movements in the silver price.

If the silver price re-rates lower, it could impact SS1’s share price.

Second is exploration risk because SS1 may be pricing in some exploration success at its current valuation.

So far, the results have been positive, but there is no guarantee that the company continues to deliver these results.

These are just two risks we think are relevant to SS1 in the short term, check out our SS1 Investment Memo to see other risks we have previously mentioned.

SS1 Investment Memo

For a full rundown of our investment thesis, read our SS1 Investment Memo, where we share:

- What SS1 does

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.