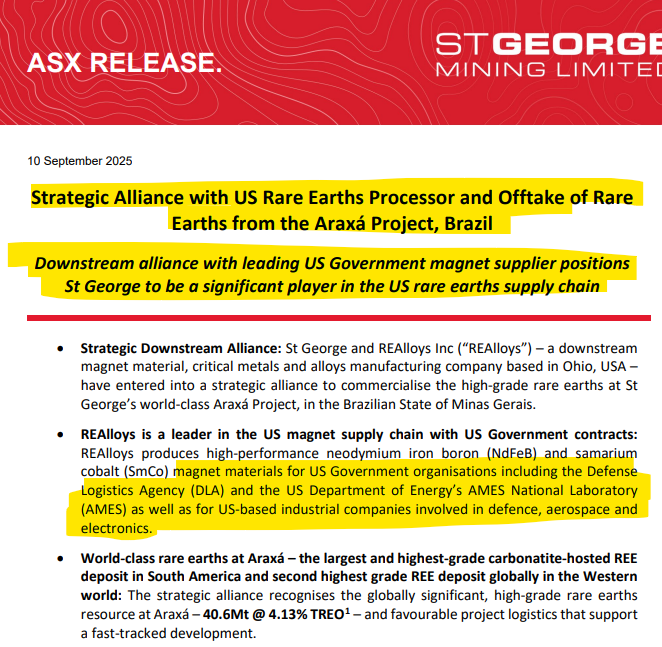

SGQ signs strategic rare earths alliance with US defence industry magnet maker

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 23,470,000 SGQ shares and 12,500,000 SGQ Options at the time of publishing this article. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

It’s happening.

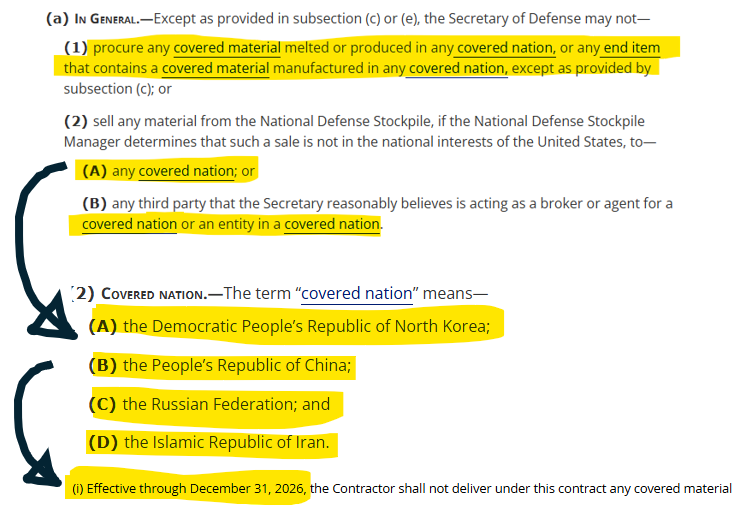

The USA is banning its domestic defence contractors from using Chinese-sourced rare earth magnets and metals in any weapons system.

The US has set a date for when rare earth import bans come into effect - 31 December 2026 (Source) (Source).

From 2027 onwards, anyone buying rare earth products from China risks losing their valuable defence contracts with the US government.

Time to move fast, US magnet makers...

This looming deadline probably helps explain why REAlloys, a “leading US government (rare earth) magnet supplier”, just signed an MoU with our rare earths development stage Investment St George Mining (ASX:SGQ).

SGQ’s new potential downstream partner REAlloys is an integrated magnet materials & magnet producer for high-performance “US Protected Markets” including the:

- US National Defense Stockpile (NDS),

- US Defense Industrial Base (DIB),

- US Nuclear Industrial Base (NIB),

- Robotics, Electric Aviation and Critical Infrastructure Industries and

- for US Partner Countries with Defense Treaties, Alliances & Agreements.

The image on the front of ReAlloys website says it all:

(Source)

Under the terms of the MoU, REAlloys will take SGQ’s rare earth product and test different processing techniques to see if it is suitable for magnet making...

...the precursor to making products that can then be sold into critical US industries like defence, nuclear and robotics.

If all goes well, the strategic alliance could turn into an offtake contract with REAlloys for ~40% of SGQ’s future rare earth production.

Why does a US government magnet supplier want to partner with SGQ?

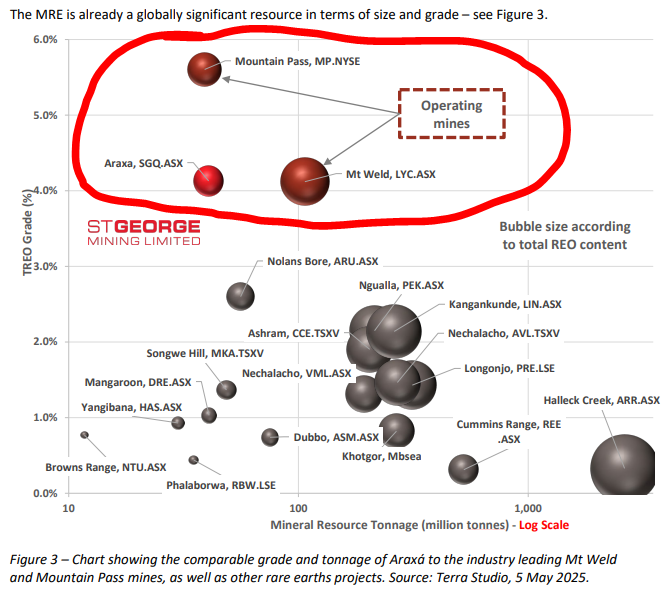

SGQ’s rare earths asset in Brazil is on par with the projects owned by the two biggest Western rare earths producers - the $17BN MP Materials and $14BN Lynas.

In terms of size, SGQ is comparable to ~$17BN MP Materials’ project.

In terms of grade, SGQ is comparable to ~$14BN Lynas’ project.

SGQ has a market cap of $186M so it has some catching up to do in terms of valuation.

(and it's got four drill rigs on site now to improve on the resource - a Mineral Resource update is due next quarter)

Rare earth magnets go into jets, missiles, naval ships, satellites and many more advanced technologies, so the US isn’t messing around with securing what it needs.

As mentioned earlier, the US has effectively set a ~16 month deadline for an entire industry to re-tool and build out a domestic supply chain...

Here are the US government documents that show the ban the US is proposing to kick in on the 31st of December 2026:

We think that as that deadline approaches, any rare earths project that could become a valid supply option could become a lot more valuable.

Which is probably why an Ohio based, US based rare earth magnet producer like REAlloys would be interested in signing a strategic alliance with SGQ.

Under the MoU, REAlloys will take SGQ’s rare earths product, test it and the two companies will look at producing a product that can go into the US rare earth magnet supply chain:

(Source - SGQ’s announcement today)

SGQ’s project is the largest and highest-grade carbonatite-hosted rare earth deposit in South America...

And the second highest grade REE deposit globally in the Western world:

(source)

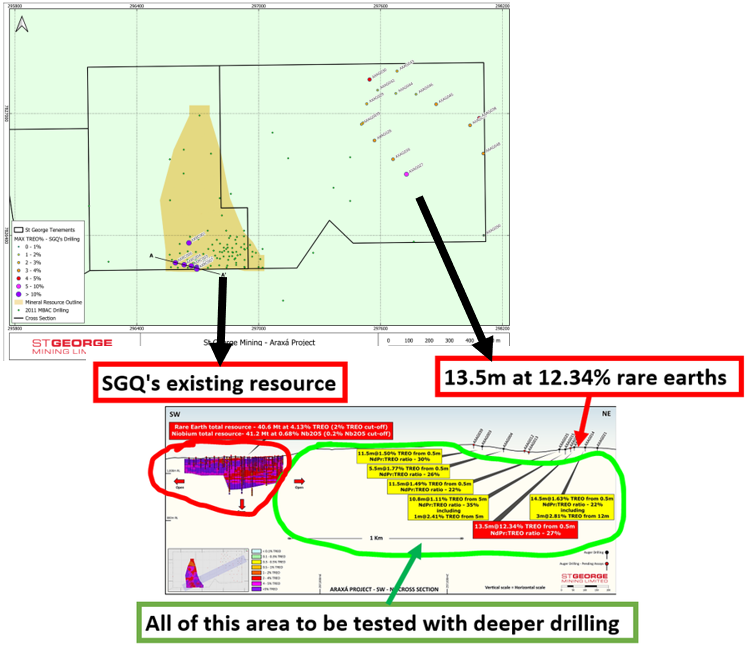

Within the next 3-6 months, we think SGQ’s project could get even bigger from a size perspective.

SGQ is drilling right now with 3 diamond rigs and one RC rig, having added an extra drill rig after its $5M capital raise in July.

(Interesting side note - that July placement was done at a 13.1% premium to the 30 day VWAP at the time, and happened after SGQ received “significant unsolicited interest from European based strategic investors”).

Earlier shallow auger drilling already hit rare earths way outside of the current resource footprint (with one hole ending in mineralisation).

Now SGQ is drilling deeper RC/diamond holes - so we should start to see the real material results come out over the coming weeks.

SGQ is expecting the drilling to lead to a resource upgrade before the end of the year.

We think that in a few months time, SGQ’s project could have a resource that is hard to ignore from a size and grade perspective.

Which might start to make it a potential M&A target from anyone looking for a big high grade non Western supply source.

(no guarantees of course)

Western rare earth majors are flush with cash - is the next natural move to do some M&A?

So far the single biggest critical mineral the US government has put capital behind has been rare earths.

Across US and Australia we have seen:

- The US$400M direct investment from the Pentagon into MP Materials.

- The US$500M offtake deal between Apple and MP Materials.

- The US$1BN loan commitment from JP Morgan & Goldman Sachs for MP Materials.

- A$1.65BN in loans from the Australian government to Iluka Resources.

- The $750M capital raise from Investors into Lynas Rare Earths.

Now all of a sudden these companies' projects are funded and/or the corporations have a treasury to put to work (maybe by doing deals...)

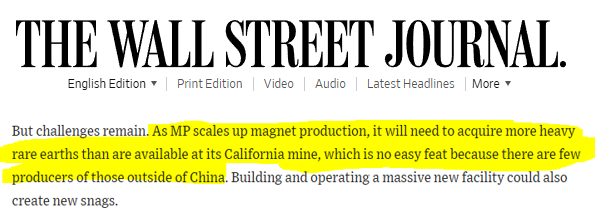

The biggest benefactor so far has been MP Materials.

Most of MP Materials new cash is earmarked for “10xing its magnet facility” - they are literally calling it “the 10x Facility” - aside from sounding cool, and delivering much needed US onshore processing capacity, it will also create a big hungry plant which is (as the Wall Street Journal reported) going to need feedstock which MP’s current mine just isn't able to provide:

(Source)

Where will the feedstock for a 10x facility come from?

Then there is the ASX listed Lynas Resources - who just raised $750M and said it was considering doing deals downstream with the cash raised...

(Source)

The article then featured another Aussie rare earths developer who had a downstream plant but no mine “to provide feedstock”:

(Source)

This is another sign that these big players can go downstream fairly easily, but have issues filling those facilities with upstream supply.

In May, the Lynas CEO flagged an interest in early stage development assets in Brazil, and “plans to work with early-stage developers to help bring their mines online”...

(Source)

SGQ could certainly use some help from a multi-billion dollar partner like that.

The question then becomes, what can MP and Lynas do to secure feedstock?

They could do what Iluka Resources did, and do a deal with the developers that have assets with defined resources.

Iluka did a rare earth concentrate supply deal with African rare earths developer Lindian Resources.

The deal essentially sees Lindian supply Iluka’s refinery in Australia with rare earth concentrate feedstock for ~15 years.

Lindian's share price went up ~200% after that news:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Of course no one knows exactly what Lynas and MP will do but we are hoping at least one of them has at the very least “watchlisted” SGQ and is paying attention.

It would definitely make sense for the two to be watching SGQ because SGQ’s project is hosted in the same type of geology as the two projects they mine (hard rock carbonatite-hosted rare earth deposit).

They know this type of rare earth deposit well and would be able to form a view on what can

be done with SGQ’s project pretty quickly (unlike other types like ISR or clay hosted deposits).

We noticed last week a Canadian listed Brazilian rare earths stock got US government funding for its project.

(Source)

Which tells us that Brazil as a jurisdiction is somewhere the Americans are clearly OK to make investments in.

IF the US government is willing to directly give projects in Brazil cash, then surely the national champion MP Materials looking at assets in the country would be OK?

We think that once SGQ has finished its current round of drilling and has put out a resource upgrade, SGQ’s project could start to get a lot more interest from within the rare earths industry.

Ultimately, we are hoping the drilling and resource upgrade contribute to SGQ achieving our Big Bet which is as follows:

Our Big Bet for SGQ

“SGQ defines a niobium/rare earths deposit large enough to take into development or attract corporate interest via a takeover at a market cap of >$500M”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our SGQ Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for SGQ?

Drilling results 🔄

In the short term the main thing we want to see are drill results.

Ideally we see big extensions at depth and to the north/east/west of SGQ’s current JORC resource estimate.

Beyond the drilling 🔄

Over the next 12-18 months, a lot of the catalysts for SGQ could come at hard-to-forecast times:

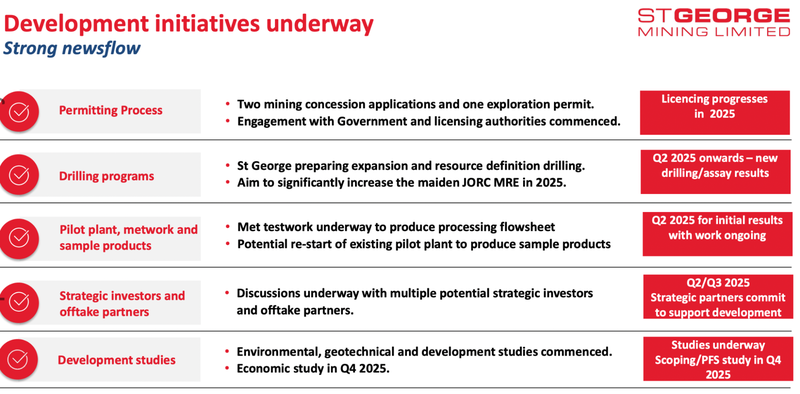

- Updates on downstream processing strategy (TODAY’S NEWS) - After today’s news we want to see the results from the testing done on SGQ’s rare earth feedstock. IF REAlloys can make SGQ’s product work it could lead to an offtake for 40% of SGQ’s future production.

- Start working on development studies - SGQ has already commenced environmental, geotechnical and development studies with a view of getting to economic studies in Q4 2025.

- Pilot plant trials - SGQ has an agreement in place with Latin America’s only permanent magnet maker. SGQ is participating in the “MAGBRAS Initiative” - a program that has major automakers like Stellantis working toward building Brazil’s first permanent magnet-making facility.

- Metwork and sample production - SGQ should have results from this fairly soon. The main catalyst we are looking forward to is the re-starting of SGQ’s pilot plant so that product samples can be produced for potential strategics/offtake partners.

- Permitting - SGQ is targeting completion for all project related permitting by Q4 2026.

- Finalise the remaining vendor payments - US$6M is due before the end of the year and US$5M due next year. Hopefully, SGQ can follow up on the $8M cornerstone investment it managed to get from Xinhai Group earlier this year with some other funding solution to cover off on these vendor payments. SGQ also raised $5M at a premium to its share price in July. It looks like the market is liking the project right now given SGQ’s $186M market cap - which means securing the funds for these vendor payments should not be too big a hurdle over the coming months.

(Source)

What are the risks?

In the short term, the key risk for SGQ is “exploration risk”.

With drilling underway we are conscious there is no guarantee that drilling will successfully grow SGQ’s resource estimate.

Exploration risk

A big part of our Investment is in seeing SGQ extend mineralisation at its project at depth and along strike. There is no guarantee that drilling will return anything of significant commercial value for SGQ (either through weak grades or thin intercepts).

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

Beyond the drill program and SGQ’s resource upgrades, the main corporate risk is that SGQ will need to make the deferred payments due for the acquisition of its project.

SGQ has already paid the first US$10M of the acquisition costs.

SGQ will still need to make a US$6M cash payment by the 26th of November and then another US$5M cash by August 2026 to the project vendors to complete the acquisition.

IF SGQ struggles raising these funds, it would likely have a negative impact on SGQ’s share price.

Deferred payments risk

To pay for the acquisition SGQ will need to make three separate payments totaling US$21M. The first US$10M installment is due on closing of the deal with the remainder due over the next 18 months.

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

For the full set of risks we have identified and accepted in making our Investment in SGQ, see our SGQ Investment Memo.

Other risks?

There are several other significant risks worth keeping in mind.

First, there's supply chain concentration risk, with the global niobium market dominated by just three producers (CBMM controlling 80%), SGQ faces the challenge of breaking into an extremely concentrated market where existing players have significant market power and established customer relationships.

The rare earths market is also concentrated, but to a lesser extent than the niobium market.

There's also environmental and regulatory risk.

Brazil has a troubled history with tailings dam disasters, leading to stricter regulations and lengthy permitting processes.

SGQ’s project requires approvals from multiple government authorities with no certainty these will be granted on acceptable terms.

While SGQ’s project sits on well understood geology, there is no guarantee that SGQ can put together a flowsheet that is capable of processing its deposit.

Processing and scaling up production is something that even experienced operators have struggled with in the rare earths-niobium space.

Other risks include commodity price volatility.

Niobium prices can fluctuate up to 35% between quarters due to the opaque pricing mechanisms in this specialised market, potentially impacting project economics.

Rare earths markets are also small and volatile which can impact project economics.

As always, these risks are part of early-stage mining investments, particularly in critical minerals projects in emerging markets.

Our SGQ Investment Memo

You can read our SGQ Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our SGQ Investment Memo covers:

- What does SGQ do?

- The macro theme for SGQ

- Our SGQ Big Bet

- What we want to see SGQ achieve

- Why we are Invested in SGQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.