SGQ next door to multi-billion dollar niobium producer - here’s what to expect next

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 29,000,000 SGQ Shares and 12,500,000 SGQ Options at the time of publishing this article. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time.

It took a little longer than we thought it would... but the deal is now done.

St George Mining (ASX:SGQ) now owns an advanced stage Brazilian niobium and REE asset.

Settlement was completed at 2c per share - this was the share price that SGQ just raised $20M, including an $8M cornerstone investment from Xinhai Group - a global mining services provider.

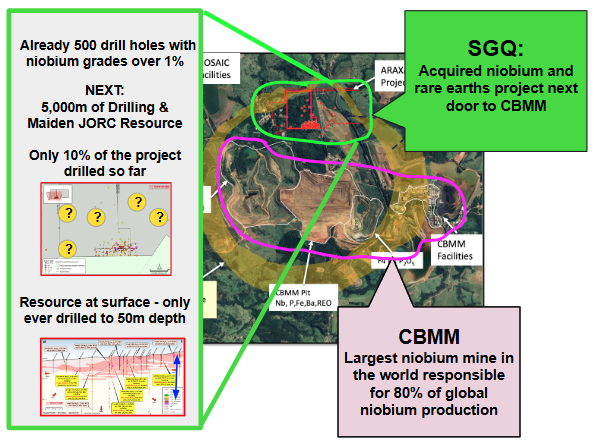

SGQ’s advanced stage niobium and rare earths asset is right next door to the world’s biggest niobium mine owned by CBMM.

CBMM is one of the biggest private mining companies in Brazil, earning billions in revenues each year from this one mine alone.

CBMM is responsible for 80% of the world’s niobium supply.

(Way back in 2011, Asian consortiums collectively paid US$3.75BN for 30% equity in CBMM, valuing the private company at US$12.5BN... we wonder what it is worth now in 2025...)

SGQ is the only company on the ASX with an advanced stage niobium project close to existing infrastructure...

This is going to help it move toward production sooner.

Being in the state of Minas Gerais also helps (we’ve seen first hand how quickly Latin Resources was able to progress in the state when it came to permitting and licenses).

SGQ is starting a 5,000m drill program next month, targeting a maiden JORC resource.

This maiden JORC resource will allow the market to compare it to other ASX companies with established JORC resources.

We are also watching out for metwork and production of offtake samples to show potential offtake partners.

News on permitting progress will be welcome, plus sealing any firm offtakes or strategic partnerships.

Plus the usual development stage studies to be released over the rest of 2025.

Now that the $20M cap raise has been completed and the deal has settled, today we will cover:

- Reasons for our Investment in SGQ

- What progress SGQ has made in recent months prior to finalising the project acquisition (hint: there was a lot)

- What we are looking out for next.

Niobium assets are attractive on the ASX right now - WA1 Resources is now capped at ~$900M and Encounter Resources is capped at ~$120M.

At the 2c cap raise price, SGQ is capped at ~$53M.

REMINDER: 9 Key reasons why we are Invested in SGQ:

Before we go too far, its worth covering the initial reasons for our Investment into SGQ.

We first Invested in SGQ back in August last year on the back of the Brazil niobium/REE asset.

Below you can read our reasons for our Investment at the time.

(Source: SGQ Investment Memo 6 August 2024)

1. Niobium is a critical mineral. Governments want it, SGQ has it.

80% of the global niobium supply is controlled by one company CBMM. Niobium sits as the second highest risk metal on the critical materials list for both the EU and the US for supply concentration.

2. SGQ is capped at $55M post acquisition, much smaller than listed peers.

Post acquisition SGQ will be capped at A$55M (at 2.5c/share). Peers that have made niobium discoveries include WA1 Resources ($842M) and Encounter Resources ($249M). SGQ can also be compared to peers that have defined Rare Earth Element projects including Brazilian Rare Earths ($550M) and Meteoric Resources ($210M).

[UPDATE: At the cap raise price (2c) SGQ is capped at ~$53M. WA1 Resources is now capped at ~$900M and Encounter Resources is capped at ~$120M]

3. Existing discovery with 500 intercepts above 1% niobium.

Compared to other companies that are in the exploration stage, SGQ already has a niobium discovery. This provides a strong foundation for SGQ to quickly progress towards a JORC resource through more drilling of its own.

4. Money flowing into companies developing niobium projects.

Because of the importance of niobium, and its concentrated supply chain, large swathes of capital is pouring into other companies that are developing niobium projects. WA1 and Encounter Resources are two of the most successful stories on the ASX, both discovering niobium in WA.

5. Project sits next door to the largest niobium producer in the world.

SGQ is next door to CBMM, which supplies 80% of the global niobium market. SGQ’s project sits on the same geology as CBMM.

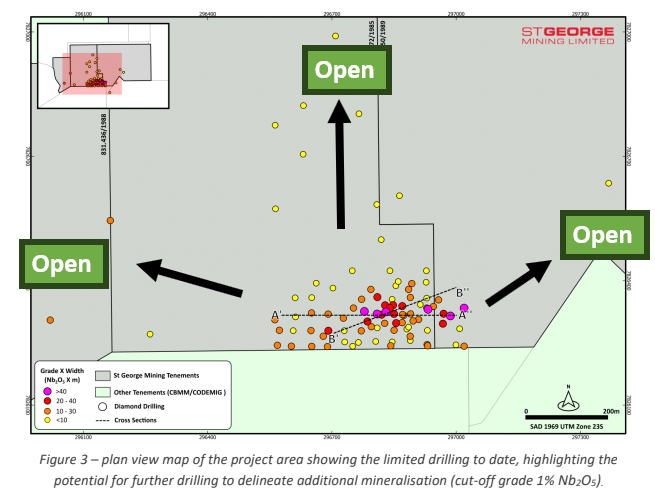

6. Only 10% of the project has been drilled (exploration upside).

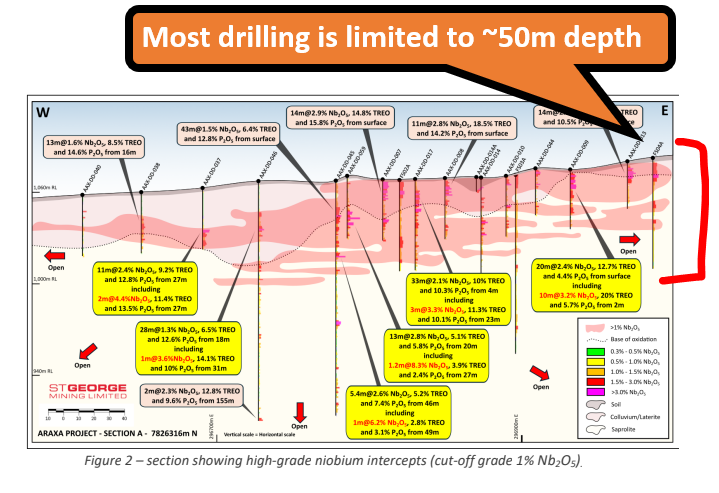

To date, only 10% of SGQ’s project has been drilled with most of the drilling only down to ~50m depths. The high-grade mineralisation commences at surface and is open in all directions, leaving open the possibility for this discovery to grow even bigger.

7. Rare earths, with high grade TREO.

SGQ’s project also contains ultra high grade rare earths with TREO grades >10% in 10-60m intercepts. SGQ’s project sits on the same type of geology (carbonatites) as Lynas’ giant Mount Weld rare earths mine.

8. Project located in the same state in Brazil as Latin Resources.

The project is located in the Minas Gerais state of Brazil, a state that we have visited and home to one of our best ever Investments, Latin Resources. Latin Resources grew from $0.03 to over $0.40 off the back of a giant lithium discovery. The region is very mining friendly with good access to infrastructure and power.

9. Project acquired from a forced seller.

The vendor of the asset (Itafos) is a TSX listed phosphate producer and is currently going through a de-leveraging process trying to reduce debt. SGQ is picking up an asset that Itafos likely sees as non-core because of the business’ phosphate focus and a lack of bandwidth to bring another mine into production.

SGQ’s progress since the deal was announced in August last year.

We first announced our Investment in SGQ back in August 2024.

Since then the company had to re-cut the terms of the $20M the capital raise to pay for its acquisition, (initially done at 2.5 per share) now done at 2 cents per share.

In the six months since, and while the settlement process was ongoing, SGQ still got a fair bit of work done in the background:

- [Oct 2024] Signed a strategic MoU offtake with SKI HongKong, leading global trader of steel materials.

- [Oct 2024] Signed an MoU with the State of Minas Gerais to fast-track approvals for its project.

- [Nov 2024] Appointed the former Brazilian Minister of Mines as an advisor for the project.

- [Dec 2024] Signed a collaboration agreement with a top research institution in Brazil to investigate downstream applications of niobium and REE.

- [Jan 2024] Signed a niobium offtake agreement with a top 20 global steelmaker, Liaoning Fangda Group, for ~20% of SGQ’s niobium product.

- [Feb 2024] Appointed a former Head of Mineral Processing at CBMM to its management team.

- [Feb 2024] Appointed a former Engineering Manager at CBMM as a processing specialist for the project.

- [Now] Completed a $20M cap raise of which an $8M cornerstone investment came from Xinhai Group (global processing engineering company)

All of this is in six months... BEFORE the project acquisition was even finalised.

Today SGQ has finally completed the acquisition of the project.

And now the really interesting work can begin...

Now we get to see SGQ drill out its project...

SGQ is a later stage asset with a proven discovery.

There are over 500 drill holes with niobium grades above 1% and some of those have grades as high as 8%.

There are also 10-60m intercepts where rare earth grades are >10%.

SGQ’s mineralisation is from the surface and is open in all directions, with the majority of drilling limited to just ~50m in depths.

Over the coming months SQG will conduct a 5,000m drill program to grow the size of its resource.

A maiden JORC-compliant MRE is targeted for March 2025 on the existing drilling.

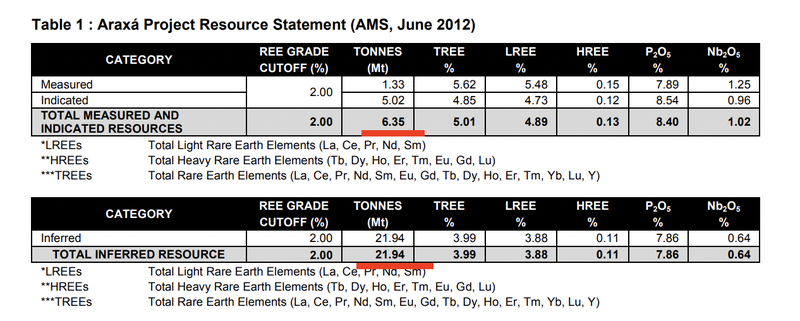

In a 2012 Preliminary Economic Assessment (PEA) the project was modelled using a ~27Mt resource with rare earths grades ranging from 3.99% to 5.01% and niobium grades from 0.64% to 1.02%.

(Source)

That PEA showed the project as having a Net Present Value (NPV) of US$967M.

However, SGQ will now look to update this feasibility study with the updated resource, costs and commodity prices.

(keep in mind the PEA was from 2012... a lot has changed since then)

Our view is that SGQ’s niobium/REE deposit is the most likely to come to market IF market forces dictate that another niobium supplier needs to come to market.

The current sector ‘pre production’ favourites WA1 Resources and Encounter Resources’ discoveries are in the West Arunta in WA - a remote part of WA which would need billions of dollars in infrastructure development before a project can come to market.

SGQ’s project on the other hand is literally next door to the world’s biggest niobium mine and all of the associated infrastructure that mine is tapping into like sealed roads, grid power, water, telecommunications, and accommodation.

SGQ even has an existing pilot plant on site that is undergoing a technical review.

Having access to all that infrastructure and workforce on its doorstep means it is much faster and cheaper to bring a mine into production.

Now with the deal done and the $20M cash in the bank available to make the first vendor payment plus upcoming newsflow we want to see SGQ deliver the following over the next 12-18 months:

- 5,000m of drilling

- Deliver a maiden JORC resource estimate

- Progress permitting

- Update the market on the existing pilot plant and its potential to produce sample niobium / REE products

- Progress on strategic investors/offtake partners

- Finalise the remaining vendor payments AND

- Start working on development studies

What stood out to us the most over the past few months

As mentioned earlier, SGQ has got a fair bit of work done while the deal with the project vendors was settling.

SGQ managed to bring onto its team some ex-CBMM (the producer next door) niobium experts and sign a few offtake/development partnership deals, including a cornerstone $8M strategic investment.

Here are our takes on all of the news:

Cornerstone Investment & Development Agreement: Global Engineering Company (Xinhai Group)

A few weeks ago, SGQ signed a MoU with Xinhai Group, a global process engineering company based in China.

Under the MoU SGQ and Xinhai would establish a “mutually acceptable funding solution for the EPC contract including exclusive distribution and marketing rights for 80% of niobium offtake sold by St George into the Chinese market”.

The MoU also included a direct investment into SGQ at the most recent cap raise at 2c per share.

Our take:

We like that Xinhai Group came in for a cornerstone stake of $8M in the equity raise to support the acquisition.

After the placement shares are issued, they would be ~15% owners in SGQ and have a real incentive to see SGQ succeed.

We also like the deal because Xinhai is genuinely big.

The Engineering Procurement and Contracting (EPC) company has constructed more than 2,000 mines in more than 100 countries.

So when it comes time to tender out for an EPCM contractor, Xinhai should be a good partner to have in SGQ’s corner.

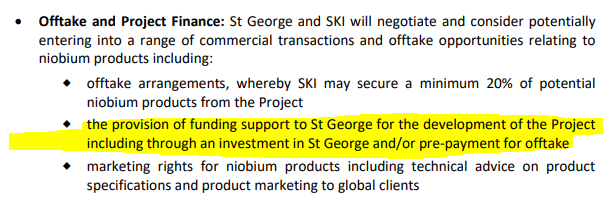

MoU Offtake 1: Global trader of steel materials (SKI Hong Kong)

In October last year SGQ signed a non-binding MoU with SKI HongKong Limited, a leading global trader of steel materials including niobium.

The key terms of the MoU were:

- Offtake deal where SKI may secure minimum 20% of niobium products from its project

- SKI to provide funding support for project development, potentially through investment in SGQ or pre-payment for offtake

- SKI to advise on product specifications and marketing of niobium to global clients

Our take:

We like these types of offtake agreements because it means SGQ can reduce its distribution and marketing risk when it comes time to develop its project.

We also liked the potential for a pre-payment solution that was mentioned in the deal - this could be big for SGQ when it comes time to try and lock in project financing.

(Source)

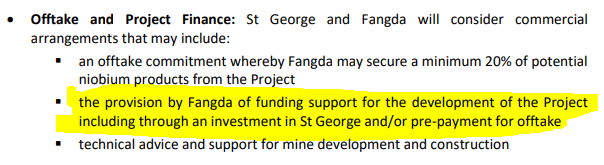

MoU Offtake 2: Top 20 global steel maker (Liaoning Fangda Group)

Fangda is a global Top 20 steelmaker, with plans to eventually crack the Top 5.

The MoU includes potential offtake for ~20% of SGQ’s niobium products and potential funding support for project development.

The offtake agreement has the following:

- Fangda to be granted exclusive rights to 20% of SGQ’s niobium product

- 5 year offtake term

- Pricing based on market-linked reference price

- A potential pre-payment loan facility

Our take:

We think it’s a smart move by SGQ to build out a framework for a long term partnership with a major steelmaker at this early stage.

We also like that SGQ has again opted for a pre-payment solution with Fangda, which will help come project financing time.

(Source)

SGQ’s team now made up of ex-CBMM niobium experts and the ex- Brazilian Minister For Mines:

Over the last few months SGQ has announced three key appointments.

Appointment 1: Former Minister of Mines and Energy

Last year SGQ announced a new advisor to its board, Adolfo Sachida, Brazil’s former Minister of Mines and Energy.

This is the exact type of appointment that we want to see from our development stage companies.

Sachsida is a highly credentialed business leader, whose roles include:

- Minister of Mines and Energy

- Chief Secretary of Economic Affairs of the Ministry for the Economy

- Secretary of Economic Policy of the Ministry for the Economy

Appointments like this one are critical for development stage companies working in a particular jurisdiction.

He will be able support SGQ’s activities in the region by facilitating interactions with key stakeholders in government.

Appointment 2 & 3: Former key employees at CBMM

Last month SGQ added Ricardo Maximo Nardi, a former CBMM mineral processing head, to its Araxa Project team in Brazil.

Nardi brings over 30 years of niobium processing experience to the role and was employed at the Araxá operations of CBMM from 1982 to 2021.

Remember that the largest and highest grade producer of niobium - CBMM’s mine - also happens to be next door to SGQ’s project.

In addition to Nardi, SGQ also hired former CBMM engineer Mr Carlos Alberto de Araujo.

He was with CBMM for 15+ years and was also one of the industrial specialists who managed the design, construction and commissioning of CBMM’s niobium processing plant.

Between Ricardo and Carlos, SGQ now has over 45 years of experience working at the world’s biggest niobium mine next door...

Now with the deal complete and all of the progress SGQ has made to date. We are looking forward to seeing SGQ work toward our Big Bet which is as follows:

Our SGQ Big Bet:

“SGQ defines a niobium/rare earths deposit large enough to take into development or attract corporate interest via a takeover at a market cap of >$500M”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGQ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

What’s next for SGQ?

In the short term we want to see SGQ start drilling and put out a maiden JORC resource estimate.

5,000m Drilling program

With the acquisition complete SGQ will commence its 5,000m drill program next month.

Maiden JORC Resource

SGQ is scheduled to publish a maiden JORC-compliant resource next month.

We mentioned earlier that a 2012 Preliminary Economic Assessment (PEA) for SGQ’s project used a ~27Mt resource with rare earths grades ranging from 3.99% to 5.01% and niobium grades from 0.64% to 1.02%.

This isn't currently JORC compliant but we think that if SGQ can declare anything remotely close to this, it will more than justify SGQ’s current market cap.

For context - WA1 Resources has a market cap of ~$900M and a JORC inferred resource of ~200mt at 1% niobium.

(That values WA1 at ~$4.5M per tonne of JORC resource)

Beyond these two catalysts, we are also looking forward to the project being progressed from a permitting perspective & from a funding/offtake perspective:

(Source)

What are the risks?

Exploration risk

A big part of our Investment is in seeing SGQ extend mineralisation at its project at depth and along strike.

It will now be starting a 5,000m drill campaign.

There is no guarantee that drilling will return anything of significant commercial value for SGQ (either through weak grades or thin intercepts).

There is also some risk associated with metwork for later stage projects like SGQ’s - SGQ will be focusing on understanding the metwork over the coming months in parallel to drilling.

Commodity price risk

The niobium market is very small, which means that there can be big swings in commodity prices based on supply out of CBMM (which controls 80% of the market).

There are also a number of substitute commodities to niobium such as tantalum and vanadium.

If the price of niobium accelerates, then buyers may look for substitutes, pushing the price of the commodity down.

Deferred payments risk

To pay for the acquisition SGQ will need to make three separate payments totaling US$21M.

The first US$10M has already been paid. The remainder needs to be paid over the next 18 months.

SGQ is now on the clock.

In 9 months, the next US$6M is due, and in 18 months, the final US$5M.

This cash could come from a strategic cornerstone investor or via an institutional capital raise.

This funding injection will dilute existing shareholders, to what extent will depend on how the company is making progress and how the broader market is responding to its assets.

In an extreme scenario, IF SGQ is unable to raise funds to pay for the deferred milestone payments, then it risks losing the asset.

It is possible that SGQ fails to make these payments, in which case we would expect the company’s share price to be re-rated significantly lower.

Our SGQ Investment Memo

You can read our SGQ Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our SGQ Investment Memo covers:

- What does SGQ do?

- The macro theme for SGQ

- Our SGQ Big Bet

- What we want to see SGQ achieve

- Why we are Invested in SGQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.