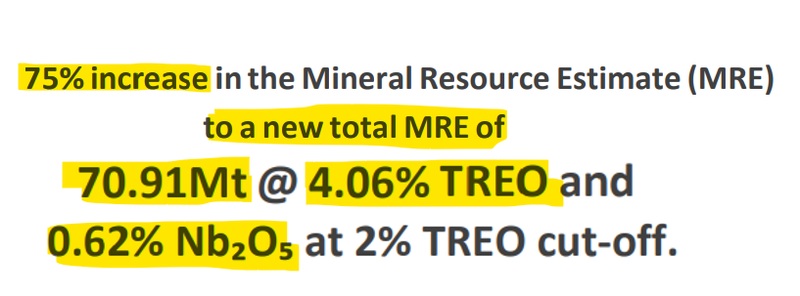

SGQ: New upgraded resource: 75% bigger at 70.91Mt @ 4.06% TREO (and 0.62% niobium) - with drilling ongoing…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 12,403,000 SGQ Shares and 12,500,000 SGQ Options at the time of publishing this article. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

The largest and highest-grade carbonatite-hosted rare earths deposit in South America.

The highest grade undeveloped rare earths asset in the Western world.

And it just got 75% bigger...

Today our Investment St George Mining (ASX:SGQ) significantly increased the size of its rare earths-niobium project in Brazil.

(source)

SGQ isn't stopping here though - the company has four rigs drilling right now on a 24/7 basis (3 diamond and 1 RC) - so something tells us this won't be the last time SGQ upgrades its resource. (source)

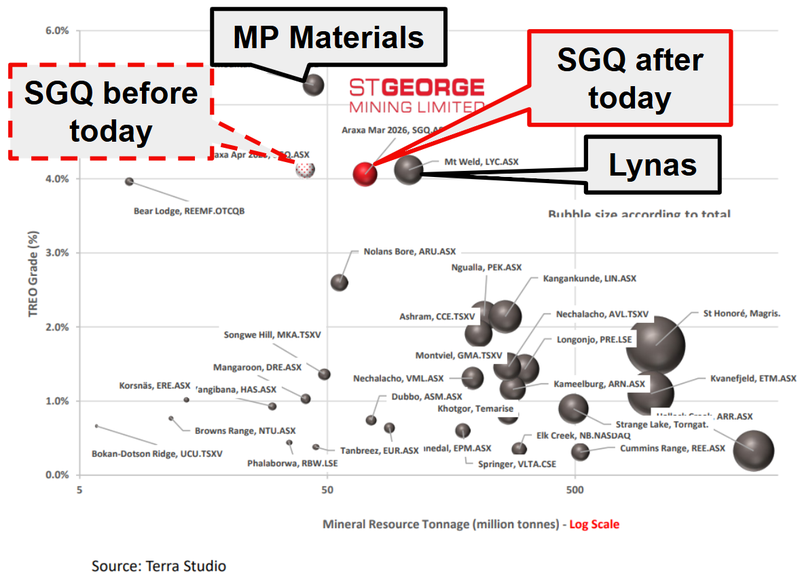

SGQ owns 100% of one of the top three biggest/highest grade hard rock, carbonatite hosted rare earths deposits globally.

The only other two are already in production and owned by:

- ~A$16BN MP Materials - USA’s only rare earth mine that received US$400M from the Department of War and signed a US$500M deal with Apple last year. AND

- ~A$20BN Lynas Rare Earths - a global operator with a mine in WA and a refinery in Malaysia.

Prior to the trading halt, SGQ was capped at ~A$515M (at 13.5c per share)

SGQ’s asset ranks third for grade out of the three projects and second in terms of size - SGQ’s asset is pre development, while the other two are in production.

We are Invested in SGQ to see its valuation grow closer to its multi-billion dollar producer peers over time.

Here is how the projects compare to each other after today’s announcement:

(source)

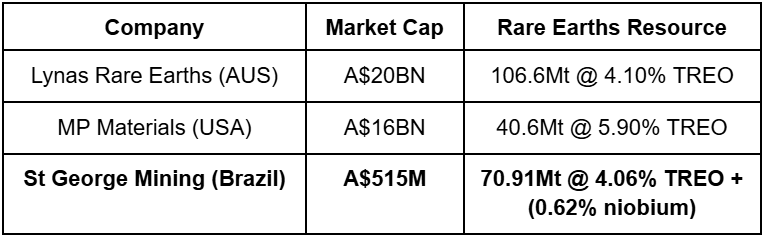

And here are the resources for the three projects side by side:

Note: SGQ’s market cap is based on a 13.5c share price in the table above.

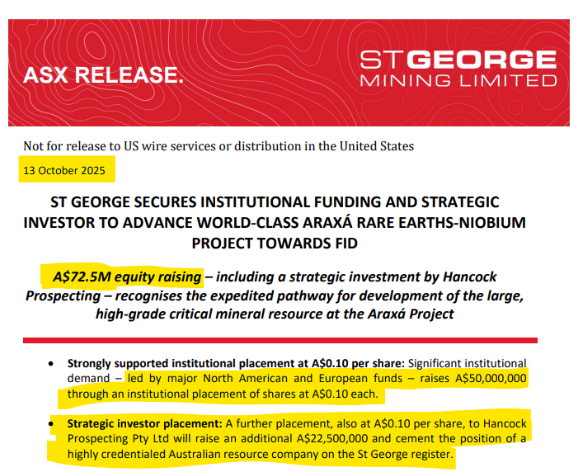

One thing all three companies have in common is a major shareholder - Australia’s richest person, Gina Rinehart.

Gina came into SGQ’s $72.5M placement last year at 10c, taking $22.5M of the offering:

(source)

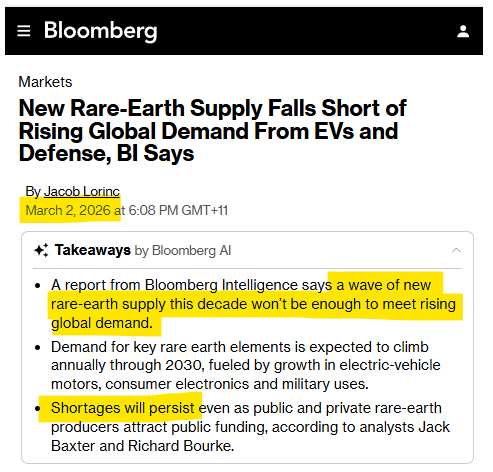

And she was adding to her position across Lynas and MP aggressively in 2025:

It's a good time to release a 75% increase to your rare earths Mineral Resource Estimate.

24 hours ago we saw this article come out about a global shortage of rare earths supply, even if forecast new supply is brought online:

(Source)

We think that as SGQ’s resource gets bigger, it becomes harder to ignore as one of the biggest undeveloped carbonatite rare earths projects globally.

(like the big elephant in the room in the global rare earths industry)

Again, SGQ isn't stopping here though - the company has four rigs drilling right now on a 24/7 basis (3 diamond and 1 RC) - so something tells us this won't be the last time SGQ upgrades its resource. (source)

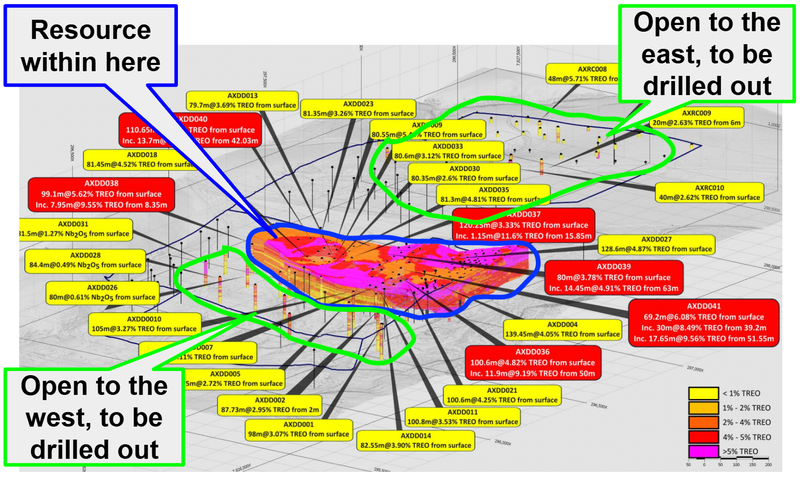

Today’s resource upgrade doesn’t include:

- “44 expansion holes” that have been drilled, but not in the resource yet.

- Results from the next 50 holes that have been planned.

- The known discoveries SGQ has recently made ~230m to the west and ~1km to the east. (source) (source)

Here is how SGQ’s resource looks now - and how we think it can grow over time:

(source)

We think the resource upgrade today (and any future upgrades that come) will just increase SGQ’s relevance on the global stage.

IF the US government (or corporates) decide to go out and look for a single project that can secure a MATERIAL amount of raw rare earths material, SGQ’s project could be right up there as one of the most obvious choices.

Especially now with the US Department Of War saying securing critical minerals like rare earth elements is “fundamental to national security and the economy”:

(source)

We are already in an environment where the US government has been comfortable backing projects in Brazil.

The US has been pretty public about Brazil as a destination rich in rare earths - and where the US is looking to secure its supply chains from:

(no surprise given Brazil has the world’s largest reserves outside of China) (source)

(source)

(source)

Meanwhile there is clear corporate interest in Brazil too - Australian producer Lynas are on the record as being interested in Brazilian assets:

(source)

Why rare earths, why now?

The last bull run in rare earths was led by expected future demand from wind turbines and electric vehicles - an overarching “electrification” thematic.

We think a big reason that rare earths are now front and centre of political/public debate is because the stakes are now a lot higher.

Whichever country wins the race in AI, AI robotics and military robotics will likely be the next global superpower.

And without rare earths, nation states can't build AI military infrastructure like robot armies.

(which gives everyone reasons to spend trillions, not billions?)

So if the country to win the AI and AI robot race is likely to become the new global superpower, (both from robot driven productivity gains and robot driven military dominance), it means that securing rare earths supply domestically OR from allies has become urgent and of strategic importance.

Warfare capability has become highly dependent on drones (attack and surveillance), especially on the front lines which we’ve seen from the Ukraine/Russia conflict and from Iran over the weekend.

~12 months ago, the USA came to the realisation that the supply of critical minerals (especially rare earths) required to build things such as these are almost entirely controlled by China.

This realisation also came with the frightening reality that China could at any time withhold supply (exactly like it started doing last year).

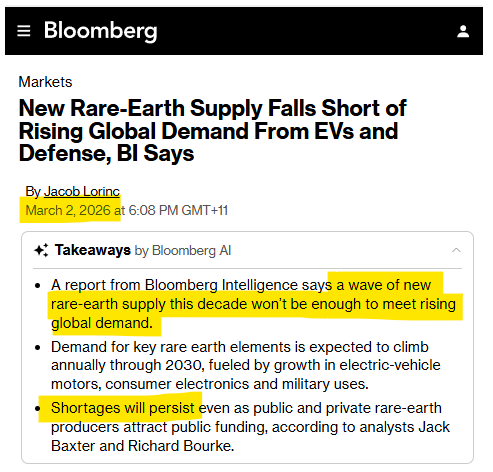

And as we highlighted above, in breaking news overnight - Bloomberg Intelligence is now reporting that there won't be enough rare earths to meet all that demand (despite the recent wave of capital coming into the sector).

(source)

The US is now repeatedly throwing large amounts of capital at the sector and just a few weeks ago, launched a US$12BN critical minerals stockpile initiative, titled “Project Vault”. (source)

Remember the US Department Of War is calling the securing of critical minerals including rare earths “fundamental to national security and the economy”.

We think that SGQ finds itself in that fortunate position (that not many listed companies get) where:

- The macro thematic is hot - due to geopolitical tensions and supply chain dependency, there is an urgency to create a domesticated supply chain, especially away from China

- The company has cash - $53M at 31 December 2025, so there is no immediate need to raise (source)

- The rigs are turning - 4 drill rigs (3 diamond and 1 RC) are ongoing 24/7 drilling extensional holes to upgrade the resource even further. (source)

- There is REAL strategic appeal of an asset like SGQ’s - because it offers supply security in a relatively stable Tier 1 jurisdiction at a time of increasing and inflamed geopolitics, AND

- There is REAL corporate/government interest in Tier 1 rare earths assets like SGQ’s - we are seeing large government investment in processing infrastructure and these companies are seeking supply.

We first Invested in SGQ back in August 2024, since then a lot has changed for SGQ - here are some links to the key takeaways we have had over the last 10 months:

- SGQ also has niobium - another mineral on global critical minerals lists

- Could SGQ’s JORC resource command a “location premium”?

- SGQ receives state government support for Brazilian rare earths project

- SGQ appoints US advisor for rare earths project

- SGQ Advances Toward Rare Earth Magnets with MagBras

- SGQ signs strategic rare earths alliance with US defence industry magnet maker

- SGQ acquires land for processing infrastructure at its rare earths/niobium project

- Western rare earth majors are flush with cash - is the next natural move to do some M&A?

What’s next for SGQ?

Drilling results 🔄

SGQ is currently drilling its project 24/7 with three diamond core rigs and one RC rig.

On top of the upgraded MRE today, SGQ is drilling aggressively with 44 holes recently completed NOT included in this upgrade plus 50 more holes planned in the coming 2 months. The drill results from these could feed another significant resource upgrade.

Prior to today, SGQ said that drilling will continue indefinitely into 2026. (source)

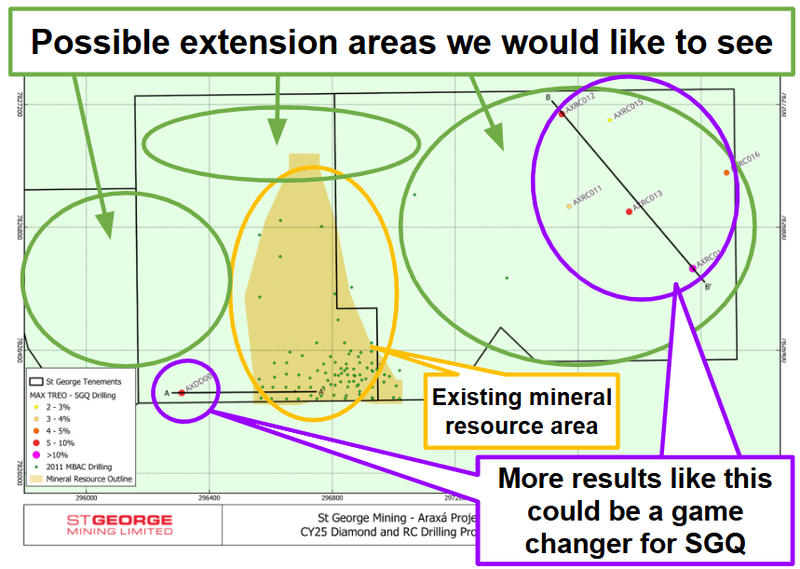

In the short term the main thing we want to see are drill results confirming big extensions at depth and to the north/east/west of SGQ’s current JORC resource estimate:

(Source)

Beyond the drilling 🔄

Over the next 12 months, a lot of the catalysts for SGQ could come at hard-to-forecast times:

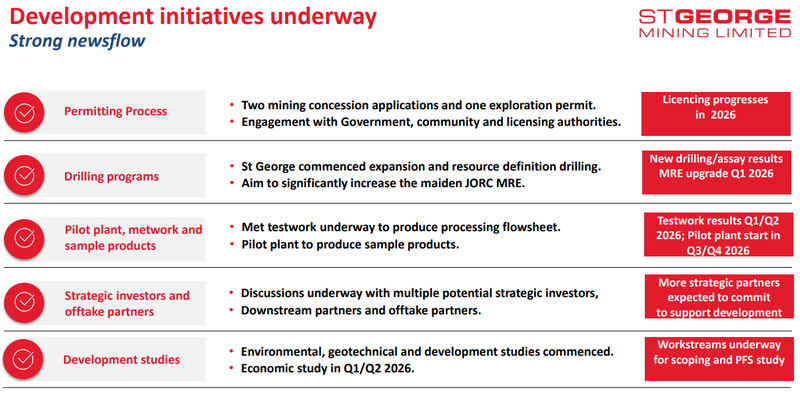

- Updates on downstream processing strategy - We want to see SGQ define its downstream rare earths strategy. We are especially looking forward to an update in relation to the US. SGQ recently extended its agreement with US magnet producer REalloys, who SGQ is aiming to supply feedstock to (source). SGQ has confirmed there are talks with more downstream partners and offtake partners, plus multiple strategic investors.

- Work on development studies - SGQ has already commenced environmental, geotechnical and development studies, which were mentioned as continuing here and in the most recent quarterly, that negotiations with the government were underway to expedite these (source). The economic study is due in H1.

Recently, SGQ confirmed a scoping study for a niobium mine and feasibility studies for rare earths were underway. (source)

- Pilot plant trials - SGQ has signed an agreement with CEFET to jointly collaborate on a new Pilot Plant trial that will build on the prior 9 month trial from 2012-13 which successfully produced rare earth product at over 99% purity and recoveries of 86% TREO. The pilot plant is expected to begin in H2

SGQ is also participating in the “MAGBRAS Initiative” - a program that has major automakers like Stellantis working toward building Brazil’s first permanent magnet-making facility.

- Metwork and sample production - SGQ should have results from this in the pipeline with the creation of the St George Technical Centre. The main catalyst we are looking forward to is the restarting of SGQ’s pilot plant with development of this underway with the agreement signed with CEFET to host and jointly collaborate. This will allow for product samples to be produced for potential strategics/offtake partners. Met testwork results are expected in H1.

- Permitting - SGQ is targeting completion for permitting to progress throughout 2026 with 2 mining concession applications and 1 exploration permit.

(source)

What are the risks?

In the short term, the key risk for SGQ is “exploration risk”.

With drilling underway we are conscious there is no guarantee that drilling will successfully grow SGQ’s resource estimate.

Exploration risk

A big part of our Investment is in seeing SGQ extend mineralisation at its project at depth and along strike. There is no guarantee that drilling will return anything of significant commercial value for SGQ (either through weak grades or thin intercepts).

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

Other Risks

Like any pre-development mining company, SGQ carries significant risk, here we aim to identify a few more risks.

For rare earth element projects, defining a large resource is only the first hurdle; the real challenge is metallurgy. Extracting rare earths and niobium from hard rock carbonatites involves complex, highly technical chemical processing to separate the individual elements.

While SGQ has historical pilot plant data and plans for new trials with CEFET, scaling these complex chemical processes from a small pilot plant to a commercial-scale facility is notoriously difficult, prone to delays, and highly capital-intensive.

Although SGQ is currently well-funded with $53M in the bank for exploration, building a commercial rare earths mine and downstream processing facility will ultimately require hundreds of millions of dollars in capital expenditure (CAPEX).

To reach production, the company will eventually need to secure massive debt facilities, major strategic partnerships, government grants, or conduct highly dilutive equity raises to fund construction.

SGQ is targeting the completion of its permitting in Brazil by Q4 2026. Large-scale mining and processing projects globally frequently face regulatory, environmental, and bureaucratic delays, which could push back the development timeline and increase the company's cash burn rate.

The company's valuation is also heavily leveraged to the current "critical minerals" macro thematic and Western efforts to break China's monopoly on rare earths supply.

If global geopolitical tensions ease, alternative technologies reduce the need for specific rare earths, or if China decides to flood the market to suppress prices, the strategic premium currently attached to SGQ’s asset could diminish rapidly.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our SGQ Investment Memo

You can read our SGQ Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our SGQ Investment Memo covers:

- What does SGQ do?

- The macro theme for SGQ

- Our SGQ Big Bet

- What we want to see SGQ achieve

- Why we are Invested in SGQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.