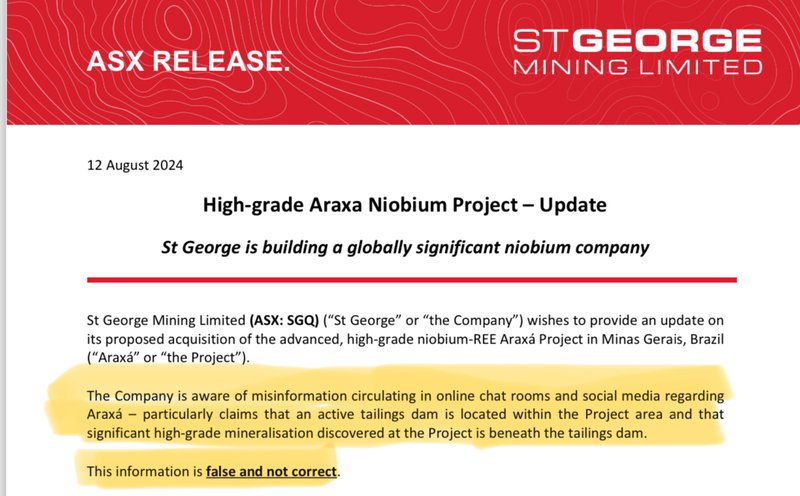

SGQ confirms that anonymous person on internet chatroom is wrong

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 24,900,000 SGQ shares at the time of publishing this article. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time. Some shares are subject to shareholder approval.

Last week we added SGQ to our Portfolio.

We also committed cash into the SGQ capital raise at 2.5c.

We think at a $55M transaction market cap, SGQ’s advanced stage niobium and rare earths project in Brazil will eventually be repriced upwards by the market.

Money appears to be flowing towards niobium projects (WA1 is capped at ~$880M and ENR capped at ~$220M) and rare earths in Brazil (MEI is capped at ~$220M and BRE is capped at ~$581M).

Last week the SGQ share price opened and traded at around 4c post the transaction being announced.

On the second day of trading, the share price suddenly dropped in the afternoon and ended the day at 2.5c.

SGQ put itself into a trading halt to clarify what it said was “mis-information” circulating in the market.

(which we assume is what caused the sudden sell off before the trading halt).

This morning SGQ announced that it is aware of misinformation circulating in online chat rooms and social media regarding the project, and that this information is “false and not correct”.

You can read the full SGQ announcement including a detailed refutal around each incorrect claim SGQ identified on the internet here:

This sort of reminds us of the movie Jay and Silent Bob Strike Back when they fly around the country and track down every anonymous person who talked bad about them on the internet to confront them... even though the exercise seems tiresome and futile.

BUT - when share prices appear to be impacted, we think putting effort into a refutal is the right thing to do.

So nothing has changed from our original initiation note on SGQ...

Except that SGQ last traded at 2.5c instead of 4c.

And global markets have now bounced back from a horror couple of days early last week.

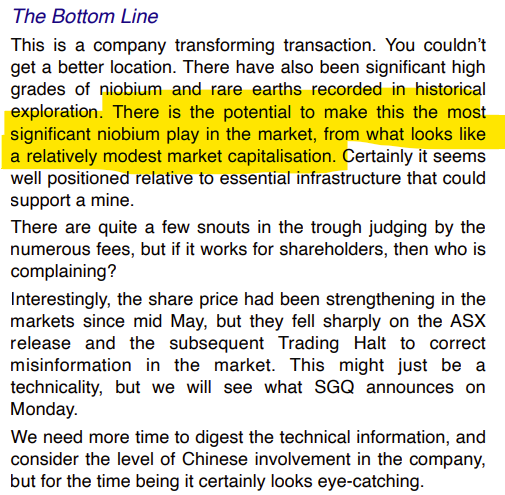

AND on Sunday, well known small cap market commentator and hardcore cynic Warwick Grigor commented on SGQ, saying that:

“there is potential to make this the most significant niobium play in the market, from what looks like a relatively modest market cap”

Grigor is well known for his pessimistic, “pulls no punches”, and often scathing commentary on many ASX listed resource projects and management teams - so we were happy to see that his initial comments on SGQ’s new project were positive.

He did question the high transaction fees (fair enough), and said he will assess the technical merits of the project with more time - we look forward to seeing what he has to say next.

(Read Warwick’s full note here)

So with SGQ having now refuted the false information, that we assume was responsible for Thursday arvo’s share price drop, nothing has changed from our initial position and initiation note.

Check out our initiation note here

SGQ’s new project is right next door to this niobium mine that supplies 80% of the global niobium market.

The project already has an existing niobium discovery, and post acquisition SGQ will be capped at $55M.

(based on 2.5c transaction share price)

Below are some key excerpts from our initiation note published 6th August 2024

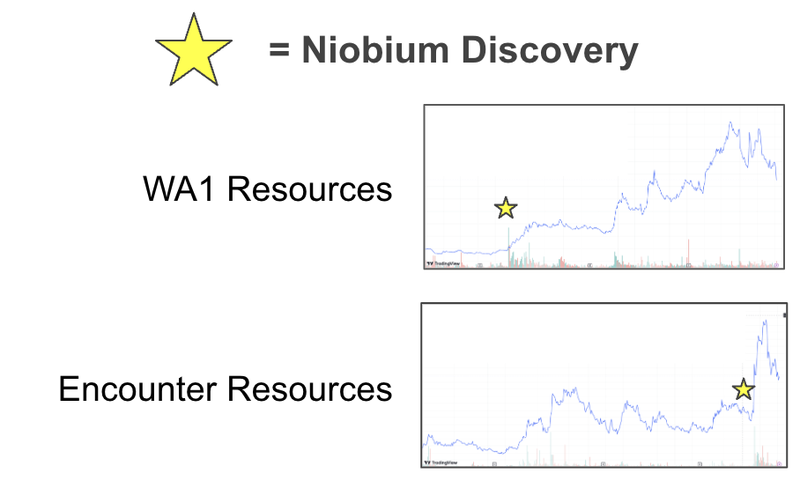

On the ASX, we have recently witnessed large inflows of capital towards quality new niobium discoveries in Western Australia:

- WA1 Resources grew from a $9M microcap explorer to over $1BN in the space of two years, on the back of a new niobium discovery in WA.

- Encounter Resources went up 300% off the back of announcing a niobium discovery in WA, it is now capped at ~$248M.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

SGQ’s project already has a proven discovery, and it is right next door to the world’s biggest niobium mine.

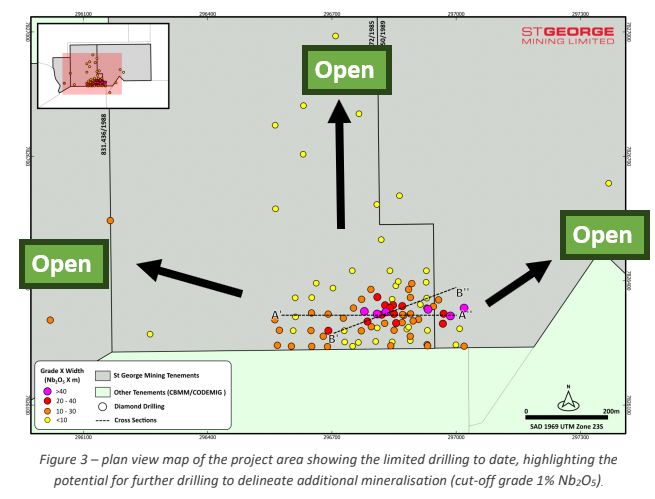

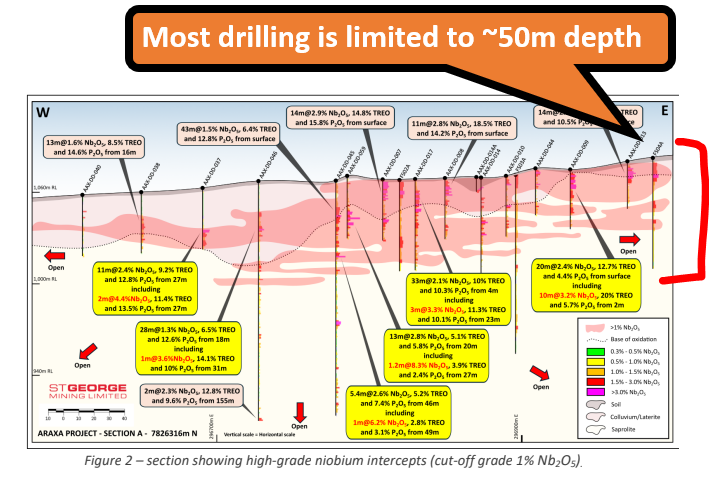

To date, there have been over 500 drill holes on SGQ’s project that have hit significant intercepts of over 1% niobium oxide, with some hits as high as 8%.

The mineralisation is from surface, widespread, and open in all directions.

Looking next door, the carbonatite that hosts CBMM’s niobium mine is confirmed to depths of 800m, but SGQ’s project has not seen drilling any deeper than 50m.

So while this is not a pure exploration story, there is exploration upside, especially given less than 10% of SGQ’s project area has been drilled (and that drilling was close-spaced).

Unlike ~$842M WA1 Resources and $248M Encounter Resources which have their valuable niobium sitting far away in the West Australian desert - the $55M capped SGQ’s Brazilian niobium project is near a skilled workforce and important infrastructure like sealed roads, grid power, water, telecommunications, and accommodation.

(this is because of the niobium mine next door to SGQ, plus a number of other mines within a few kilometers)

Having access to all that infrastructure and workforce on your doorstep means it is much faster and cheaper to bring a mine into production.

We Invested in SGQ to advance the existing niobium discovery and progress through the development stages toward building a mine.

As SGQ progresses through each stage, we hope to see the market steadily re-rate the stock.

It is early days, and success is no guarantee, but we think SGQ is acquiring a niobium asset which has a clear pathway to becoming an operating mine - and there are only three in the world right now.

SGQ’s project also contains rare earths in the same deposit.

Just like the high grade niobium found from surface, SGQ’s project has also recorded thick intercepts of high grade rare earths elements (REE) from surface.

As well as niobium, later stage rare earth projects (specifically those located in Brazil) have also been attracting capital in the markets:

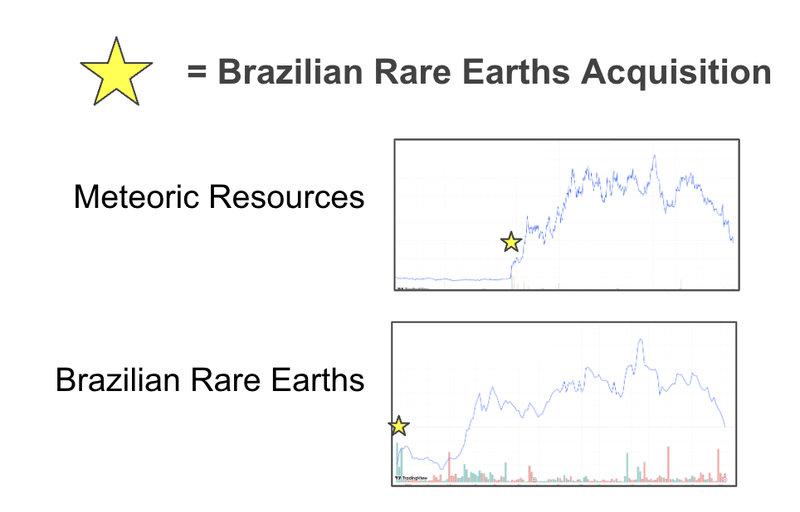

- Brazilian Rare Earths - IPO'd in December last year at $1.47/share raising $50M. The company hit a high point of $3.70 and now trades at a market cap of ~$550M.

- Meteoric Resources - Traded at $0.012 before acquiring the Brazilian REE project. The company hit a high point of $0.30 and now trades at a ~$210M market cap.

Both of these companies have significantly shown sustainable re-rates off the back of acquiring and developing REE projects in Brazil:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Remember - post acquisition SGQ will be capped at $55M - significantly less than Meteoric and Brazilian Rare Earths.

We think the ASX will rerate SGQ’s new later stage niobium and rare earths asset inline with the values placed on other ASX listed niobium and rare earth players like WA1 Resources, Encounter Resources, Meteoric Resources and Brazilian Rare Earths.

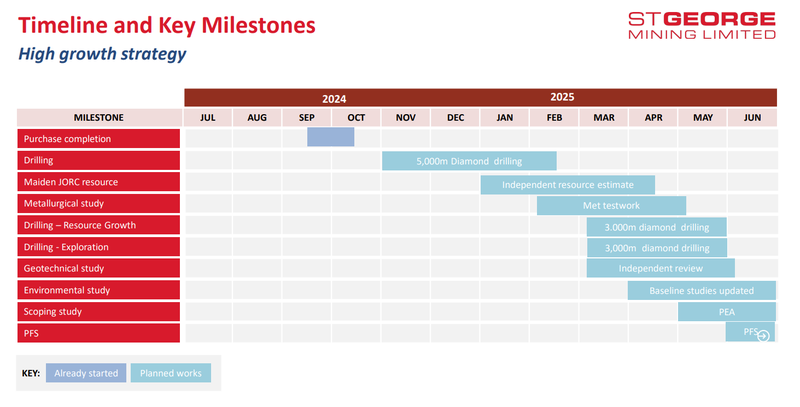

Over the coming 12-18 months we want to see SGQ:

- Complete the transaction and vendor payments

- Run an extensive amount of drilling

- Deliver a JORC compliant resource

- Run met test work

- Complete a Pre Feasibility Study

SGQ to become the most advanced Brazilian Niobium/REE exposure?

One of the key reasons we liked the SGQ acquisition is because of the parallels it has to the Meteoric acquisition from back in 2022...

For those that are unfamiliar with the Meteoric story:

Back in 2022, Meteoric acquired an advanced rare earths asset in Brazil for what the market at the time thought was expensive (~US$20M cash headline number).

For the perennial cynics, it was a high price to pay for an asset in a hot macro thematic...

From the company (Meteoric’s) perspective it was actually a very different approach to what every other ASX junior was doing at the time...

Every other junior explorer at the time was trying to pay as little as possible for early-stage, ‘roll of the dice’ exploration assets.

While the juniors spent capital trying to make a REE discovery, Meteoric was busy defining a monster deposit.

The asset was picked up in October 2022 and in less ~12 months time Meteoric was the number one Brazilian rare earths exposure on the ASX.

In less than 12 months Meteorics share price was up by over 33 times - at its peak Meteoric’s market cap was ~$610M.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think SGQ is doing the same, defining an existing discovery, but for niobium as well as REE.

And where SGQ differs from Meteoric is that Meteoric has an ionic clay deposit - SGQ’s deposit is in carbonatites - like WA1 Resources.

SGQ is acquiring what we think is the most advanced Brazilian niobium exposure on the ASX.

AND importantly it is right next door to niobium heavyweight CBMM - they control ~80% of the world’s niobium supply.

The 9 Reasons why we Invested in SGQ

- Niobium is a critical mineral. Governments want it, SGQ has it.

80% of the global niobium supply is controlled by one company CBMM. Niobium sits as the second highest risk metal on the critical materials list for both the EU and the US for supply concentration.

- SGQ is capped at $55M post acquisition, much smaller than listed peers.

Post acquisition SGQ will be capped at A$55M (at 2.5c/share). Peers that have made niobium discoveries include WA1 Resources ($842M) and Encounter Resources ($249M). SGQ can also be compared to peers that have defined Rare Earth Element projects including Brazilian Rare Earths ($550M) and Meteoric Resources ($210M).

- Existing discovery with 500 intercepts above 1% niobium.

Compared to other companies that are in the exploration stage, SGQ already has a niobium discovery. This provides a strong foundation for SGQ to quickly progress towards a JORC resource through more drilling of its own.

- Money flowing into companies developing niobium projects.

Because of the importance of niobium, and its concentrated supply chain, large swathes of capital is pouring into other companies that are developing niobium projects. WA1 and Encounter Resources are two of the most successful stories on the ASX, both discovering niobium in WA.

- Project sits next door to the largest niobium producer in the world.

SGQ is next door to CBMM, which supplies 80% of the global niobium market. SGQ’s project sits on the same geology as CBMM.

- Only 10% of the project has been drilled (exploration upside).

To date, only 10% of SGQ’s project has been drilled with most of the drilling only down to ~50m depths. The high-grade mineralisation commences at surface and is open in all directions, leaving open the possibility for this discovery to grow even bigger.

- Rare earths, with high grade TREO.

SGQ’s project also contains ultra high grade rare earths with TREO grades >10% in 10-60m intercepts. SGQ’s project sits on the same type of geology (carbonatites) as Lynas’ giant Mount Weld rare earths mine.

- Project located in the same state in Brazil as Latin Resources.

The project is located in the Minas Gerais state of Brazil, a state that we have visited and home to one of our best ever Investments, Latin Resources. Latin Resources grew from $0.03 to over $0.40 off the back of a giant lithium discovery. The region is very mining friendly with good access to infrastructure and power.

- Project acquired from a forced seller.

The vendor of the asset (Itafos) is a TSX listed phosphate producer and is currently going through a de-leveraging process trying to reduce debt. SGQ is picking up an asset that Itafos likely sees as non-core because of the business’ phosphate focus and a lack of bandwidth to bring another mine into production.

So that we can follow the company’s progress over time and track our Investment, today we are also publishing our SGQ Investment Memo, where we share:

- What SGQ does

- The macro theme for SGQ

- Our SGQ Big Bet

- What we want to see SGQ achieve

- Why we are Invested in SGQ

- The key risks to our Investment Thesis

- Our Investment Plan

SGQ Investment Memo 1

Shares Held: 24,900,000

Memo Opened: Tuesday, 6th August 2024

What does SGQ do?

St George Mining (ASX:SGQ) is a Brazilian niobium & rare earths developer in the state of Minas Gerais.

What is the macro theme?

80% of the global supply for niobium is controlled by one company and one mine in Brazil.

This commodity is considered the second highest commodity for both the US and the EU in terms of supply chain risk.

Although the market for niobium is still relatively niche, it may grow as metal of the future in things like ultrafast charging batteries.

Rare earths are also considered critical minerals with production and processing capacity concentrated in China.

Our SGQ Big Bet:

“SGQ defines a niobium/rare earths deposit large enough to take into development or attract corporate interest via a takeover at a market cap of >$500M”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGQ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

Why did we Invest in SGQ?

- Niobium is a critical mineral. Governments want it, SGQ has it

- SGQ is capped at $55M post acquisition, much smaller than listed peers

- Existing discovery with 500 intercepts above 1% niobium

- Money flowing into companies developing niobium projects

- Project sits next door to the largest niobium producer in the world

- Only 10% of the project has been drilled (exploration upside)

- Rare earths, with high grade TREO

- Project located in the same state in Brazil as Latin Resources

- Project acquired from a forced seller

What do we expect SGQ to deliver?

Objective #1: Acquisition completion

We want to see SGQ satisfy the conditions for the acquisition and complete the deal.

Milestones

🔲 Shareholder approvals

🔲 Upfront cash payment completed

🔲 Deferred consideration #1 Paid

🔲 Deferred consideration #2 Paid

Objective #2: Drilling to increase size of discovery

We want to see SGQ drill out its existing discovery at depth and in all directions to increase the footprint of the deposit.

Milestones

🔲 Drilling permits granted

🔲 Land access agreements

🔲 Drilling commenced

🔲 Drilling results

Objective #3: Maiden JORC resource estimate & met testwork

We want to see SGQ define a maiden JORC resource for its project. As part of the resource estimate we also want to see SGQ run some metallurgical testwork and confirm its project sits on similar geology to CBMM’s project next door AND that it can be processed using similar processing techniques.

Milestones

🔲 Metwork updates

🔲 Maiden JORC resource estimate

Objective #4: Enter feasibility studies

We want to see SGQ take its project into economic studies either via a scoping study, Preliminary Economic Assessment (PEA) or a Pre Feasibility Study (PFS).

Milestones

🔲 Scoping study/preliminary economic assessment commenced

🔲 Scoping study/preliminary economic assessment completed

What could go wrong?

Exploration risk

A big part of our Investment is in seeing SGQ extend mineralisation at its project at depth and along strike.

There is no guarantee that drilling will return anything of significant commercial value for SGQ (either through weak grades or thin intercepts).

There is also some risk associated with metwork for later stage projects like SGQ’s - SGQ will be focusing on understanding the metwork over the coming months in parallel to drilling.

Commodity price risk

The niobium market is very small, which means that there can be big swings in commodity prices based on supply out of CBMM (who controls 80% of the market).

There are also a number of substitute commodities to niobium such as tantalum and vanadium.

If the price of niobium accelerates, then buyers may look for substitutes, pushing the price of the commodity down.

Deal Risk

The acquisition by SGQ is still subject to a certain number of conditions being met.

SGQ will need to get shareholder approvals for the deal - and there is a chance the vendor will need to get approvals for the transaction also.

SGQ expects the conditions of the deal to be satisfied by late September/early October 2024 but there is always a risk that these do not happen. If the deal falls through then our Investment Thesis wouldnt be applicable anymore.

Deferred payments risk

To pay for the acquisition SGQ will need to make three separate payments totaling US$21M. The first US$10M installment is due on closing of the deal with the remainder due over the next 18 months.

IF SGQ is unable to raise funds to pay for the deferred milestone payments then it risks losing the asset. It is possible that SGQ fails to make these payments in which case we would expect the company’s share price to be re-rated significantly lower.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking SGQ’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Development/delay risk

Should any or all of the above risks materialise, SGQ could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on SGQ.

Investment Plan

We are Invested in SGQ to see it progress its project into development.

Our plan is to hold the majority of our position in SGQ for 3 to 5 years which we hope is enough time to see SGQ to move towards development (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may also look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.