Quiet Before the Storm

Published 21-FEB-2026 14:23 P.M.

|

14 minute read

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

Any forward-looking statements are uncertain and not a guaranteed outcome.

Eerily quiet on the small end of the market this week.

(continuing what has been a generally stale and quiet February)

But this is not like previous “pauses” between mini bull runs we have seen over the last few years.

While most stocks have come off a bit, there doesn’t appear to be much “desperate selling no matter what” like we saw during past breathers.

(we wrote about this a lot in 2023 and 2024, where there was a long, drawn out capitulation phase and many shareholders just had to sell at illiquid lows because they needed the money for other stuff - life, bills, mortgages and all that)

Now, even though it's quiet, it seems like most shareholders still want to be there, in anticipation that another run is just around the corner... and have the means to hang around.

The selling during the pauses doesn't seem as strong as it was in the past.

After the run we had in July to October last year... and the mini run in January this year, most shareholders in small stocks are either fresh legs or re-energised long term holders.

AND unlike in previous years, many companies raised a decent chunk of money in the last ~7 months of sporadic bull conditions, and for the first time in a long time have money to do “stuff”...

Meaning by now they are likely pregnant with news - another reason to hold on even when the market takes a pause.

In December 2024 we wrote about how the recovery from the post 2020-21 raging bull market would be a lot like recovering from a hangover or sporting injury”.

(at the time the market was coming off the back of two horror years in 2022 and 2023 and we had just seen 8 weeks of positive conditions, it was a new record at the time)

Our analogy was that the small cap recovery to bullish conditions won’t be “instant”.

Instead it will come in progressively longer and stronger waves of bullishness.

With progressively shorter and less intense periods of bearishness in between the bullish waves.

Here’s the analogy:

Many of us have probably recovered from a major, crippling hangover at some point after the biggest party of our lives.

You don’t just suddenly decide to jump out of bed and go for a run.

You need time to heal...

First build up the confidence to open one eye.

Then eventually... the other.

You then build up the courage to consider reaching for your water bottle.

This basically summarises the first 2 hours.

The small cap market equivalent to late 2022.

Eventually you get up, shakily take your first few steps like a baby deer...

Attempt to eat some food... and then lie back down (2023)

Later... a small walk, possibly even outside.

Progressively bigger and stronger steps to getting back to normal function (2024)

With less and less moping in between.

Which finally leads to being able to get out for a run or do some proper exercise again (2025?)

(exercise being unimaginable at the time your first eye opened)

(read the full the small cap market recovery will be like recovering from a hangover or sporting injury article here)

We think we are now at the stage of more little bullish periods, interspersed by shorter periods of less intense bearishness.

So after the raging party the small end of the market had in 2020-21, and the crippling hangover it woke up with in 2022...

We now think the small end of the market has done a couple of small warm up jogs, and is almost ready to finally shake off the hangover and go for a proper run...

The near 4 month continuous run in small stocks we saw late last year, followed by just 2 months of bearishness before a full bullish month (Jan 2026) is a very good sign that many market participants have shaken off a lot of the PTSD that came from the last 3 years of bear market conditions.

Just compare this to how much we were cheering for the measly 8 weeks of positive conditions we got in late 2024 - the first seen 18 months.

Some pretty broad and generalist observations above...

But what about company fundamentals and management and all that stuff?

That’s important of course, but the small end of the market is driven a lot by the sentiment and mood of the crowd...

which is why we keep a keen eye on the “vibe of the thing”.

So what is the plan then for when the small end of the market runs again?

We think an "all commodities" boom incoming.

The world has suddenly woken up to adversarial countries that dominate supply of a commodity withholding supply to gain leverage.

Meaning that if you need something, money can’t get it for you.

(imagine being on a desert island with $1M and wanting a sandwich - it doesn't matter how much money you have, you just aren’t going to get it unless you figure out how to make one yourself)

To what extent the geopolitical strategic withholding of commodities supply becomes a thing over the coming years - we don’t know.

BUT

The strategic risk of the mere possibility that it can happen has been enough to create a lot of activity and attention on commodities in general.

And it's starting with US critical metals - the metals that the USA needs to power its military, robotics and AI ambitions.

Where China dominates supply and processing.

Most US investors haven't thought about commodities or mining in decades.

Once this penny drops for the general US investor, we think there will be a great migration of capital from big tech into mining and commodities.

The US critical metals theme had a great run late last year, but we think it hasn't even gotten started yet...

We also are still very bullish on precious metals gold and silver.

Our long held view is that in this period of changing world order, questions about the USD as the global reserve currency and spiralling US government debt is the perfect environment for gold and silver prices to keep moving up.

Silver delivered the biggest % increase across all commodities in 2025, followed by gold.

Both have now been spending some important time going sideways for the last month.

Huge spikes in commodity prices are great fun.

Mainly for speculators and existing shareholders in equities of that commodity.

But small stocks ultimately go up and stay up when new money comes in... and stays.

For serious (and big) new investors to come in, they need confidence that a commodity isn't just spiking and likely to crash back down again.

They need to see a “new normal” higher price to form and look like it's going to stay at the higher price levels.

So every sideways week we see for gold and silver at these historically higher prices is a good thing:

(source)

(source)

The silver price was actually up over 7.5% last night - but over the last 6 months we have become desensitised to such big moves up or down in the silver price.

(nah... who am I kidding, a 7.5% move up is awesome)

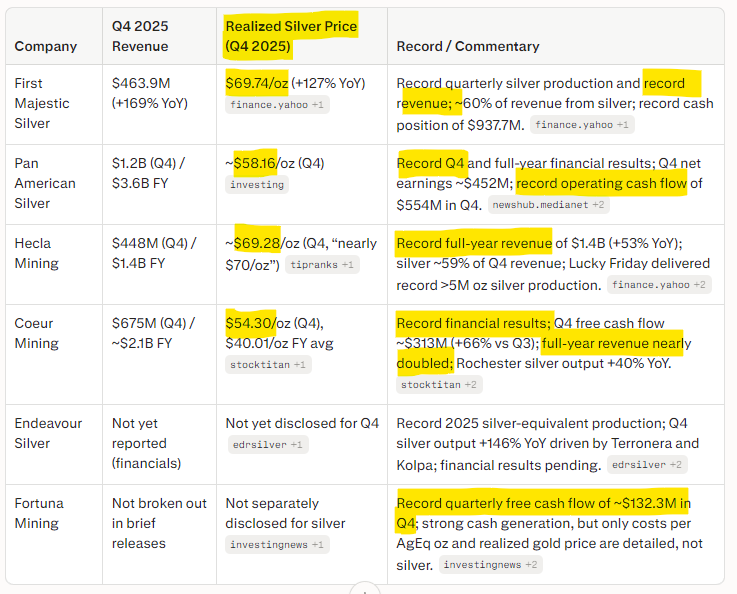

This week was important for silver watchers because it's the first time that the few pure play silver producers out there reported quarterly earnings for the period when the silver price was at record highs.

And as expected with silver spending the entire 3 months at record highs, most silver producers reported record quarterly revenue (thanks AI for doing this work):

(source)

As we have seen with gold M&A, once the producers are cashed up, they start buying the medium companies and development projects.

(the gold price run is a couple years ahead of silver, and we are finally starting to see gold explorers starting to trade at high valuations)

So another few months of silver prices at these historically high levels is important - to get the market to believe, and really start the flow down to the small ASX silver stocks we are invested in.

OR - Another massive leg up in the silver price and it would be game on...

Old mate Michael Oliver (our favourite silver analyst) still reckons we will see US$300 to US$500 silver in the next 6 months... that would be great.

watch his most recent interview here - or just jump straight to his silver price prediction here

(or of course, the silver price could also go down... nobody knows)

Speaking of videos we liked this week...

We have been talking about (and Investing in) the “China withholding Critical metals from the USA” theme for a while now.

This week we watched this interview with Craig Tindale, author of the widely read “Return to Matter” paper in early 2026, which analyses the fragility of the Western economy in the face of China's dominance in physical, tangible industries.

Craig gives one of the best articulated explainers of the US critical metals theme we have heard - well worth a listen

In summary:

- Western Vulnerability – Offshoring mining, refining and manufacturing to China has hollowed out Western industry and created critical dependence for energy, defence and tech inputs.

- Bad Incentives – Central banks and markets worshipped low prices and asset gains, pushing capital into paper assets while starving domestic productive capacity and sovereignty.

- China’s Strategy – China runs state-directed capitalism, treating key commodities and refining as strategic weapons, willing to sacrifice margins to gain control and pricing power.

- Material Chokepoints – Structural shortages in copper, silver and other critical metals collide with EVs, grids, renewables, AI and defence, all funneled through Chinese-controlled refining.

- Mispriced Assets – Tech and AI plays are valued as if materials are infinite, while mining, refining and strategic metals are under-owned and undervalued.

- Shift in the System – Expect a move toward sovereignty-focused state capitalism in the West, directing capital back into strategic resources, refining and munitions, with a major rotation into hard assets.

So why US critical metals?

It ties in to another theme we are excited about for 2026 - the upcoming build of billions of autonomous AI robots driving economic growth... and military might.

And these robots are going to need a LOT of critical materials to build... where China currently dominates supply.

(China is also in the lead on manufacturing said robots... and USA is rushing to catch up)

We think the race to “win” autonomous AI robots is also going to drive a lot of attention and capital into certain small resource stocks.

This week the following video was doing the rounds on social media, showing some pretty fancy moves by Chinese built robots:

(source)

(Happy Chinese New Year by the way everyone)

As if this wasn’t already terrifying enough... some peanut on the internet decided to catch the wave of interest in this video by generating a fake AI video of similar robots holding guns and doing military exercises:

(source FAKE VIDEO - but you can watch it here)

While this video is fake af, it does paint a potentially dystopian future and the vision driving the upcoming robot arms race...

So to tie it all together, China appears to be surging ahead in robotics, a debt laden USA is rushing to catch up (print more money to solve?), the robot and AI race winner will reap economic benefits and military dominance.

A rapid build of physical robot technology is incoming... hard commodities suddenly become highly strategic, supply is withheld by those who have it leading to an all commodities boom.

...and in the period of “world dominance uncertainty” during this race to win robotics and AI, gold and silver will keep rising.

To finish up, here is an update on recent merger and acquisition activity in gold and silver - a positive sign of things to come.

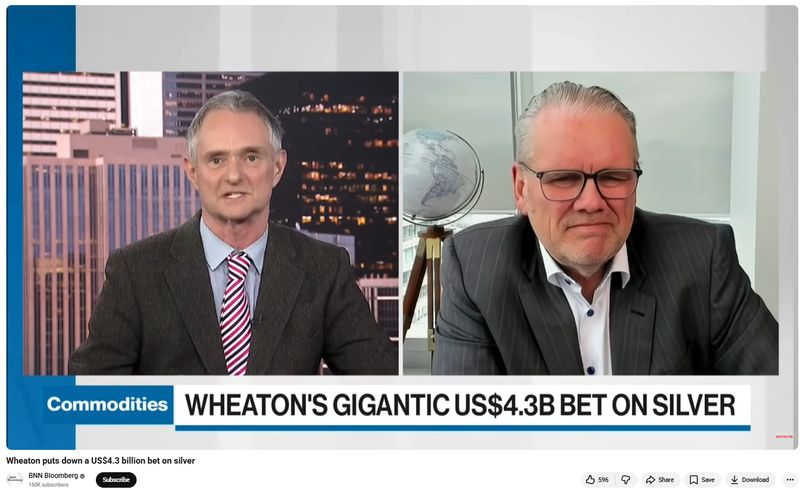

$95BN Wheaton put on a US$4.3BN silver bet

So far, in this silver cycle, we hadn’t really seen anything happen apart from the silver price rally.

Especially in the big end of town - which usually sets the precedent for the rest of the market.

This week may have been a turning point for the silver space.

$95BN Wheaton Precious Metals did a US$4.3BN silver streaming deal with BHP - for one of the big copper assets the two jointly own.

(source)

Wheaton paid US$4.3BN upfront in exchange for the right to purchase silver from the big copper asset at 20% of the spot price going forward (for the rest of the project's life).

Basically a big leveraged silver long - putting up the capital now, betting on silver prices going up (or staying high) from current levels.

If Silver rallies, then Wheaton would have done a superb deal, if silver prices fall, then that deal doesn’t really make much sense.

The CEO of Wheaton explains the deal really well here - interesting that he says “one of the challenges is looking for opportunities in the silver space”.

(we’ve got a couple for you, mate)

He also says “silver is the most critical mineral”, “in this age of mobility and AI” at ~7:20 into the interview.

(source)

For us it was the first time a corporate - in the mining space who would understand the supply/demand dynamics for silver well - shows its cards on its silver strategy...

( a sign of things to come?)

We haven’t really seen any M&A happen in the silver space yet, despite the massive rally in the silver price.

Maybe this week's deal forces a few of the corporate development guys in the big silver miners to start dusting off their spreadsheets...

Our view is that as soon as silver prices start to stabilise and consolidate gains at new highs - the equities will really start to run.

So maybe, consolidation in and around US$70 and US$90 for a few months will actually be bullish for silver stocks over the coming months.

(we don’t know anything though - silver can go up, down or sideways)

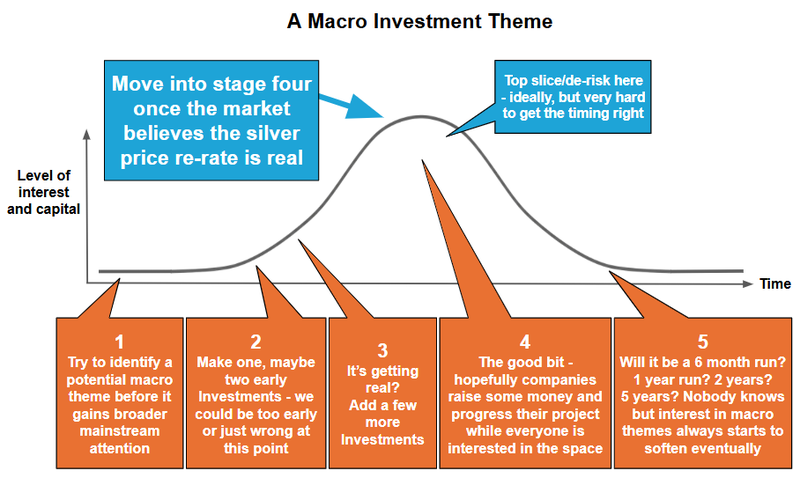

Here is where we think the silver macro thematic is right now:

We hold the following silver stocks in our Portfolio - SS1, IVR, BKB, MTH, RCM, WCE, AVM, PFE

Gold M&A to trigger a bull market in juniors?

We saw another deal get announced this week with Genesis putting an offer in for Magnetic Resources.

(source)

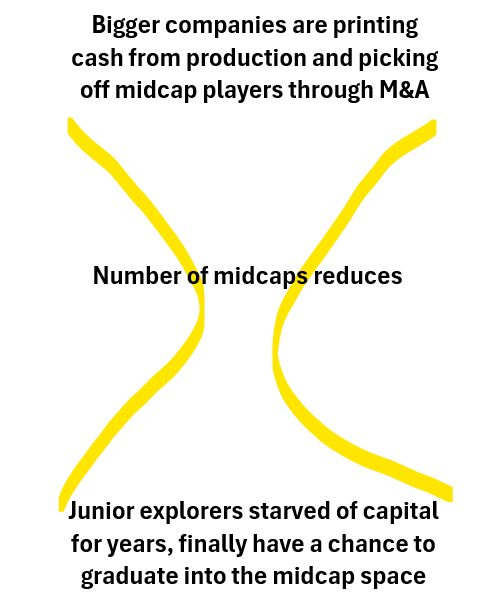

Genesis is the perfect example of a corporate structure taking advantage of the value disconnect in the midcap space relative to the gold price.

Genesis has become the $8BN behemoth it is today by stitching a bunch of companies/assets together that would otherwise sit in mid cap ASX listed gold co’s.

We think Genesis’ corporate activity is part of a broader theme playing out in the small/midcap gold space...

... where the number of small/midcaps ($100M to $1BN) is getting smaller and smaller.

Especially those with projects that have resources with size/scale.

Basically something like this is playing out (we will explain how in a second):

Over the last ~18 months we have seen deals galore in the gold space.

In the big end of town:

- Northern Star taking out De Grey Mining.

- Gold Fields and Gold Road Merging

- Ramelius Resources taking over Spartan Resources.

In the midcap end:

- Westgold buying Karora Resources

- Greatland Gold buying Newmont’s Telfer/Havieron assets.

- Robex Resources merger with Predictive Discovery (currently being completed)

- Genesis with three deals since 2023 - buying Focus Minerals gold asset in WA, taking over Dacian Gold and then this week announcing a deal for Magnetic Resources.

And then in the smaller end:

- Astral Resources taking over Maximus Resources (MXR)

- Capricorn Metals taking over Albion Resources’ Monger asset.

- Torque Metals and Aston Minerals merging.

- Patronus Resources

If a midcap had a project with legs, a major came in and took them out.

If a small cap had a project with legs - it was usually trading at a pretty big discount to the rest of the market and the midcaps looking to become large caps (like a Genesis) came in and started consolidating them.

Our view is that “hollowing out” of the small/midcap space has left a big gap in the market for the junior explorers.

The market is clearly sending a signal to the junior explorers and the companies sub <$100M to raise cash, start drilling and develop assets to a size/scale that makes them interesting M&A targets.

As a result, we think it's time to start taking positions in explorers pre-discovery AND the companies with relatively smaller resources that could (with the right amount of capital and drilling) become assets “of scale” that attract corporate interest.

The gold sector looks like it is already here.

(The smaller silver sector looks to be just waking up...)

We hold the following gold stocks in our Portfolio - TTM, KAU, BKB, RML, MTH, AVM, BMG, BPM, PUR, TG1, LSR, L1M

But again, as mentioned last week, we are looking to add a few new gold stocks to our Portfolio.

See you next week, and have a great weekend

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.