PUR: Lithium up 400% in 6 months - PUR’s lithium project is back. Gold up 45% in 6 months - PUR drilling for gold soon too.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 5,675,105 PUR Shares and 610,356 PUR Options at the time of publishing this article. The Company has been engaged by PUR to share our commentary on the progress of our Investment in PUR over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

We recently glanced up from our near constant staring at the gold and silver price to notice that...

The lithium price is up 65% over the last 5 weeks and up nearly 400% over the past six months.

During the last lithium boom in 2020-2021, some of our ASX companies progressed genuine lithium projects.

Then during the subsequent 3 year “lithium winter”, moved to gold, silver or other critical minerals.

BUT...

Some held onto (and further progressed) their advanced stage lithium projects...

Just in case the lithium price made a roaring comeback...

Which it now has.

One of those companies is Pursuit Minerals (ASX:PUR).

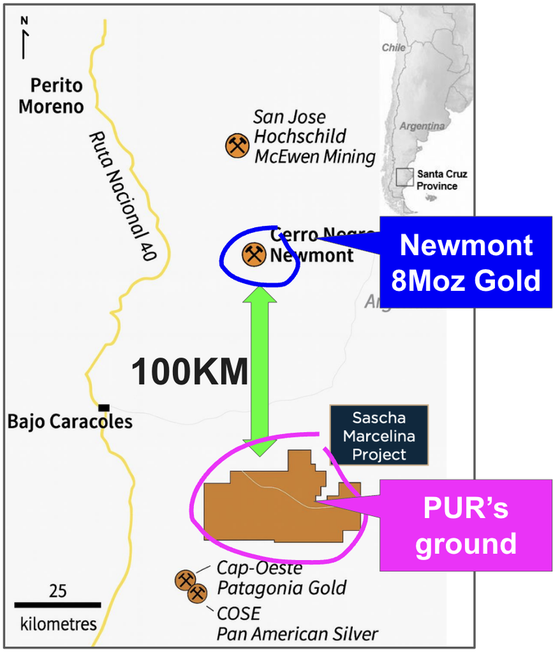

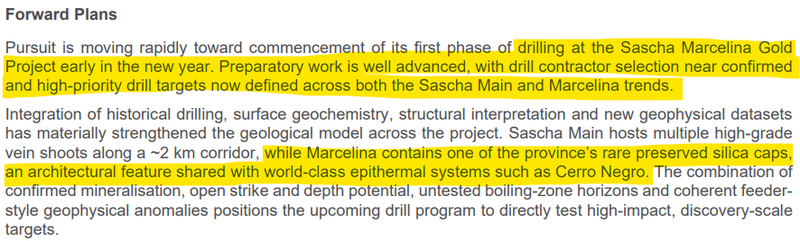

PUR is set to drill its gold-silver project in Argentina early this year - where the target is a discovery similar to 8M ounce Cerro Negro currently being mined by the world’s largest gold company, the $207BN capped Newmont.

(we are very bullish gold this year)

PUR has what it calls a “silica cap” similar to the one that was drilled to discover Cerro Negro - PUR’s early stage project has similar structure, mineralisation, geophysics, and geochemistry.

We just need to see PUR drill it... (which PUR is planning for early this year)

In parallel, while the market wasn't paying attention, PUR has been quietly working on a Pre-Feasibility Study (PFS) on its 100% owned, development stage lithium carbonate project in the Lithium Triangle of Argentina.

(A PFS is an economic study that gives estimates on how much a mine/plant will cost to build and how much money it could make)

PUR has already defined enough lithium in resources for a 25+ year mining operation.

(based on its stage 1 production target of 5,000tpa)

PUR just unveiled the Pre Feasibility Study (PFS) for its lithium project this morning, which it can use to work with development stage financiers and offtakers to progress its efforts to get into production.

(Source - PUR announcement)

PUR’s PFS Stage 1 economics delivered an NPV ~US$364M, a CAPEX ~US$135M and operating costs of ~US$6,500/t.

(costs in the lowest quartile of the global cost curve).

One of the best parts of the study for us was that PUR used a pretty conservative lithium price - almost ~80-90% below the peaks we saw in 2021-2022...

IF PUR were to plug in prices just 30% higher (still well below the all time highs for lithium) - the NPV of the project goes up to US$601M. (Source)

All of that from just Stage 1 of the development plan.

At full production, PUR’s project generates approximately US$138M per annum in revenue and ~US$55M per annum in free cash flow.

(Note - these financials are based on a number of assumptions which may not prove to be correct. Project economics are highly sensitive to lithium pricing and variations in price may have a material impact on cash flows, project value, development timing, and financing outcomes.)

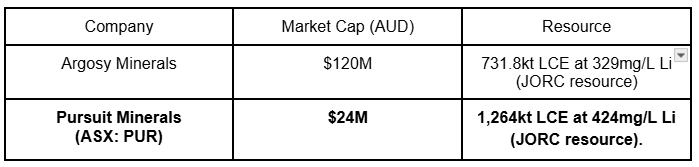

PUR’s project has a 1.264Mt lithium carbonate equivalent resource estimate, averaging grades of ~424 mg/L Li.

Today, PUR defined a maiden probable ore reserve (the highest classification any resource can get) of ~125kt lithium carbonate equivalent (grading even higher at ~670 mg/L Li).

So PUR is progressing both:

- A gold exploration asset which could deliver a company making discovery, AND;

- an advanced stage lithium project with strong economics.

PUR is capped at ~$24M post the just completed raise, after just raising $7M at 9.5c (no options).

(We put some cash into this capital raise, and so did a number of new institutional investors, including the Lowell Natural Resources Fund)

It could finally be the right time for PUR.

Other companies also with advanced stage lithium projects in Argentina have been running lately:

- Galan Lithium is up ~235% since November (9.5M tonnes of LCE @ ~841 mg/L Li, development stage, $530M market cap)

- Argosy Minerals up ~464% since July (0.7M tonnes of LCE @ 329 mg/L Li, production stage, $154M market cap)

PUR’s project has a resource of ~1.2M tonnes of LCE @ ~424mg/L Li at the PFS stage, also in Argentina.

Could we see a similar run from the $24M capped PUR now it has delivered its PFS and has just raised $7M to progress its projects?

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think PUR could have the right combination of assets, with a solid capital structure, which means it is now leveraged to any success at either of its two projects...

Potential gold discovery in a rising gold market?

(yes, we know gold was down on Friday, but you only have to zoom out a year or two to see how little that fall on Friday means for the gold market)

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Lithium development in a rising lithium market?

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

And both projects are in Argentina, where management has years of experience and relationships.

After today’s capital raise, PUR’s enterprise value sits around ~$17M.

With the market up and about, we will think PUR has two catalysts that could re-rate its market cap over the next few months:

- Gold-silver drilling in Argentina - planned for early this year, going after a discovery that is similar to an 8M ounce deposit owned by $207BN Newmont.

(Source)

- Lithium in Argentina - now that the market all of a sudden is interested in lithium stocks again, PUR’s lithium project might start to attract increased market interest into the company.

(source)

ASX:PUR

Why we like PUR’s lithium asset

PUR’s lithium asset sits in South America’s lithium triangle - home to ~56% of the world’s lithium reserves.

It's where some of the biggest lithium projects in the world are being developed by mining supermajors like Rio Tinto.

PUR owns 100% of its project as well as a 250tpa pilot plant that is capable of producing battery grade lithium carbonates.

Here is a picture of that plant:

PUR’s project now has an 1.264Mt LCE resource estimate, averaging grades of ~424 mg/L Li.

(including a probable ore reserve (the highest classification any resource can get) of ~125kt LCE (grading even higher at ~670 mg/L Li).

That’s an ore reserve big enough to produce lithium for ~25 years.

We think PUR’s market cap (at $24M), relative to its current JORC resource, is being mispriced by the market.

Especially when it's compared to other ASX listed companies - the most obvious being Argosy Minerals.

Argosy is currently capped at $120M, and trades with a market cap 5x bigger than PUR - despite having a smaller, lower grade resource.

We do acknowledge Argosy is much further advanced relative to PUR - but we think that can be solved by executing the Stage 1 development plan in PUR’s PFS from today.

Here is how PUR’s lithium asset stacks up side by side with Argosy:

We think PUR already looks good comparing its market cap to its JORC resource.

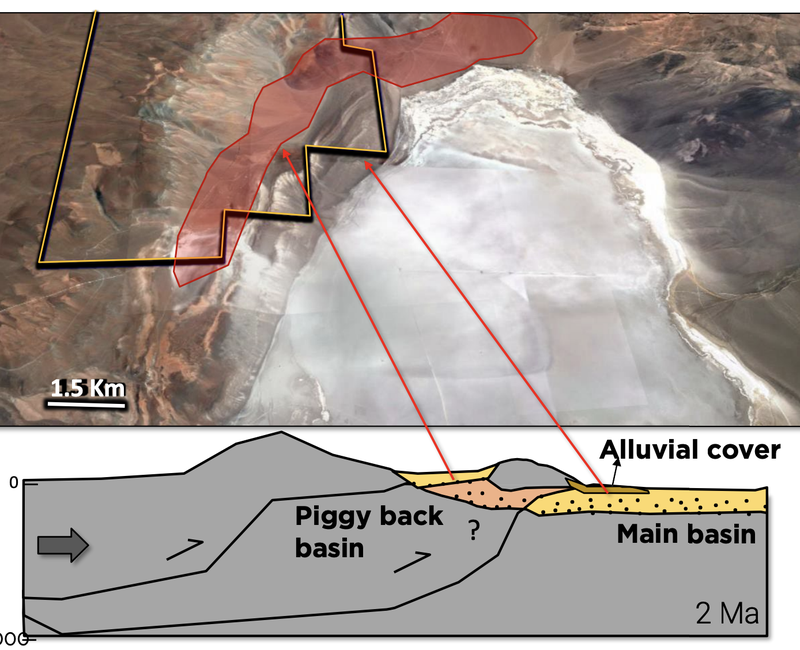

And we think PUR’s lithium resource could get bigger with some more drilling.

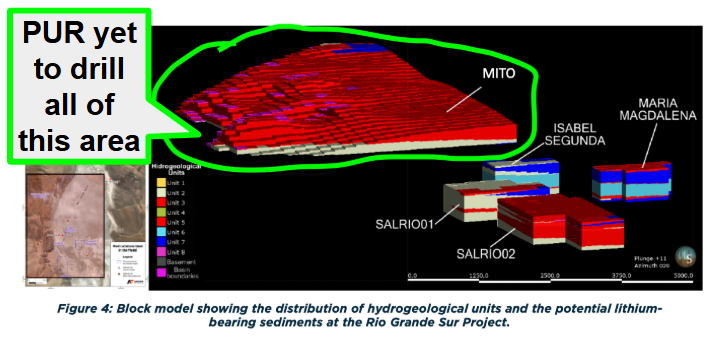

PUR is yet to drill its biggest tenement, which sits on the margins of the salar (salt flat).

A big part of the exploration upside for PUR is based on a theory that whatever lithium brines sit inside the salt lake, extends out onto its margins...

Like the image below shows:

That big piece of PUR’s ground (Mito) is the much larger untouched part of PUR’s project where there is potential to exponentially increase PUR’s resources.

This ground is where we think PUR’s blue sky exploration upside is:

(source)

PUR expects to drill that part of its project with the funds raised today.

PUR ran geophysical studies on this area that showed at depth this theory may be correct.

(source)

We are hoping to see a repeat of PUR’s regional peer NOA Lithium’s results which came from similar ground.

NOA hit grades as high as ~925mg/L Li - IF PUR was to hit grades like this across decent thickness, it could be a game changer for PUR’s project.

Those are some of the highest grades from any salars in South America...

Our view is that with some exploration on that bigger block to the north, PUR could multiply its resource estimate.

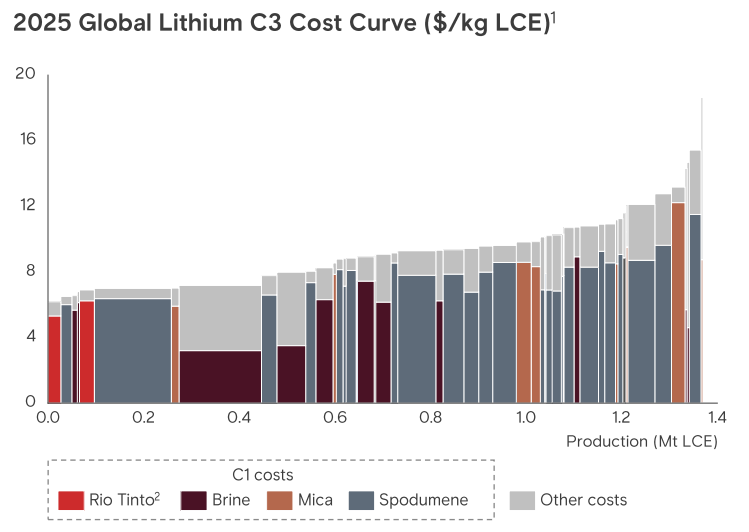

Another reason we like the lithium asset is because, brine projects typically have the lowest marginal costs of production in the lithium space:

(source)

Our view is that when the lithium market stabilises and prices are less volatile, the lowest cost assets will be the ones that survive.

(like owning the oil fields in Saudi Arabia when oil prices are depressed).

As for when prices are low - our view is that the high grade brines in parts of the world that are amenable to evaporation will still find a way of being profitable.

And Rio Tinto seems to agree with that strategy, putting most of its lithium focus and capital into Argentina.

You can hear more about Rio Tinto’s Argentina lithium investments in an episode of the Money of Mine podcast - check it out here.

Why we like PUR’s gold-silver asset

We think PUR’s gold-silver asset is one where the company can make a genuinely material discovery.

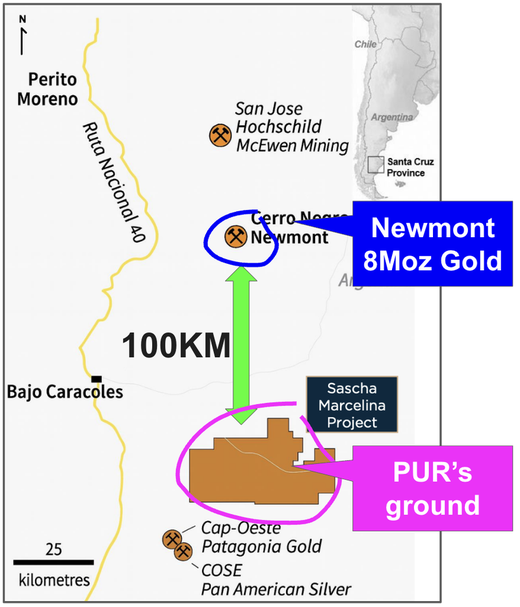

PUR’s project sits in the Santa Cruz Province of Argentina, one of the world’s premier precious metals provinces.

This province is host to ~30 million ounces of gold equivalent discoveries.

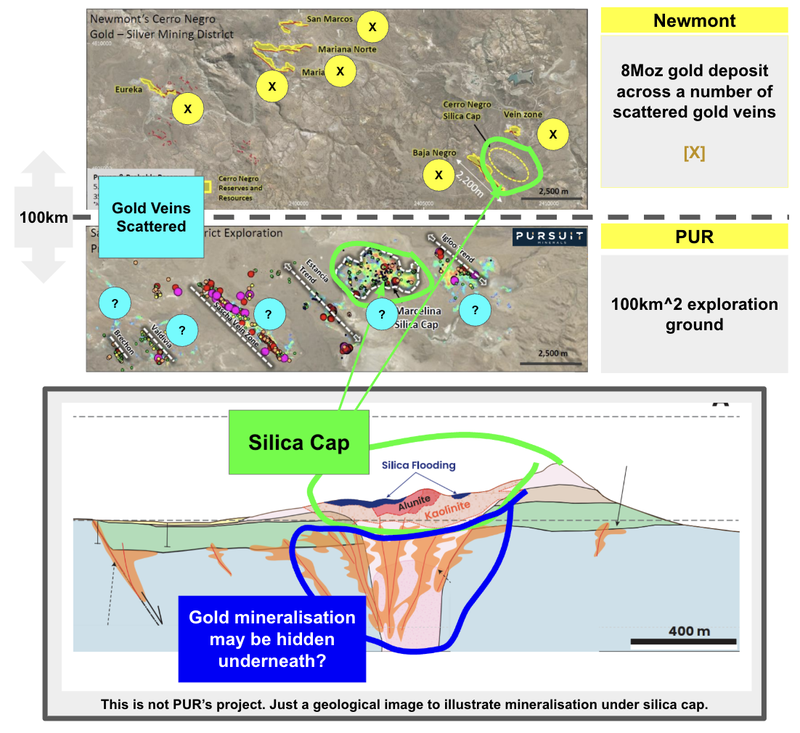

PUR’s exploration theory is based around a lookalike drill target to where the 8M ounce Cerro Negro deposit was discovered.

(source)

PUR wants to drill below a “silica cap” where it thinks a Cerro Negro lookalike could be sitting.

All the ingredients are there: structure, mineralisation, geophysics, and geochemistry...

Now we just need to see PUR drill and see if the theory is correct.

With the gold-silver asset we are backing PUR’s Chairman Tom Eadie.

Tom is the Chairman of another ASX listed gold company Southern Cross Gold.

Southern Cross, for a long time, was misunderstood by the market because of the type of deposit the company had...

However, Southern Cross has gone from $3.80 to $8/share and a $1.8BN market cap under Tom Eadie’s stewardship.

The market has now come to appreciate the value of projects with high grade, thin gold veins.

(the past performance is not an indicator of future performance)

Both Southern Cross and Cerro Negro are high grade gold assets across multiple thin veins...

... similar to what PUR is looking for on this new asset - and naturally, PUR will be applying the same geological model and exploration strategy that unlocked those finds.

Previous drilling on PUR’s project only went down to 170m.

PUR’s theory is that if it drills down to 150-400m it could make a giant gold discovery that was previously missed because of the shallower silica cap that sits on top of the gold mineralisation.

This is exactly how the 8 million ounce, Newmont owned, Cerro Negro was discovered...

PUR plans to drill test the veins marked with a (?) on the map below and soil sample, channel sample and follow up previous hits:

PUR plans to drill the project early this year.

This is high-risk, high-reward exploration from PUR.

They might not find anything valuable.

Or one good drill hit could unlock the entire project and be a company maker.

Why Argentina?

Let’s go macroeconomic and political for a moment.

A few months ago the US Trump administration backstopped Argentina with a US$20 billion currency swap.

Since Javier Milei became president in 2023, Argentina has gone from a disaster to a destination from an investment perspective.

Here is the US Treasury Secretary Scott Bessent on the US-Argentina alliance:

(Source)

Australia’s largest miner BHP is taking notice of the changes in Argentina.

(and maybe even more now that China just banned BHP iron ore imports)

(Source)

PUR is aiming to make a discovery on its gold project which shares key geological markers and similarities to that Cerro Negro mine - and is located roughly 100km to the south of Cerro Negro.

Two years ago (just before the turn of the gold price), Newmont invested a further $540M into this gold mine.

(Newmont will be pretty happy about that given the gold price has nearly doubled since)

(Source)

Overall, we think Argentina is doing all the right things to promote and encourage the domestic mining industry which we hope creates tailwinds for PUR’s.

ASX:PUR

What’s next for PUR?

🔲 Drilling at PUR’s gold-silver project

Next we want to see PUR drill its gold-silver project.

PUR’s latest update said that drilling would start “early in the new year” which means it should happen within the next few months.

We would expect PUR to update the market more once timelines firm up.

(source)

🔲 Lithium asset

PUR has confirmed today that with the uptick in lithium prices gaining momentum, it is going to be putting some attention back on this project, especially after the PFS released today.

Next, we want to see some drilling on its largest tenement (Mito), which has never been drilled and where nearby NOA hit grades as high as ~925mg/L Li.

What are the risks?

In the short term the key risks for PUR will be “Delay risk”.

Delay risk

PUR plans to drill two parts of its project all before the end of the year. There is a risk there is some slippage in these timelines and IF PUR were to have big enough delays it could lead to the market losing interest in the stock.

Significant delays could be negative for PUR’s share price as it would burn down the company’s cash balance and bring the company to a position where it needs to raise more capital and dilute existing shareholders.

Source: “What could go wrong” - PUR Investment Memo 01 October 2025.

Other risks

Like any small cap exploration and development company, PUR carries significant risk, here we aim to identify a few more risks.

PUR’s gold-silver asset is still pre-discovery.

There is no guarantee that the deep drilling (150-400m) below the silica cap will intercept the high grade veins predicted by their geological model. If the drilling fails to find anything of economic value, the market could re-rate the stock lower.

PUR’s valuation is heavily leveraged to the recent surge in lithium prices. The newly released PFS economics (NPV ~US$364M) are sensitive to these prices holding up.

As a junior company with a ~$24M market cap, PUR faces a significant funding hurdle to build its lithium project, which has a Stage 1 CAPEX of ~US$135M. The company will likely need to secure debt, a joint venture partner, or raise substantial equity, which could result in significant dilution for existing shareholders.

Operating in Argentina introduces specific country risks. While the current political climate under President Milei has become more favourable for foreign investment, the country has a history of economic volatility, high inflation, and regulatory changes that could impact project timelines and profitability.

Finally, any delays in permitting, construction, or failure to achieve the target recovery rates and purity levels could delay cash flows and weigh on the share price.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our PUR Investment Memo

You can read our PUR Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our PUR Investment Memo covers:

- What does PUR do?

- The macro theme for PUR

- Our PUR Big Bet

- What we want to see PUR achieve

- Why we are Invested in PUR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.