Our take on SGQ’s maiden resource. It’s shallow and from surface… more drilling to come

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 29,000,000 SGQ Shares and 12,500,000 SGQ Options at the time of publishing this article. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time.

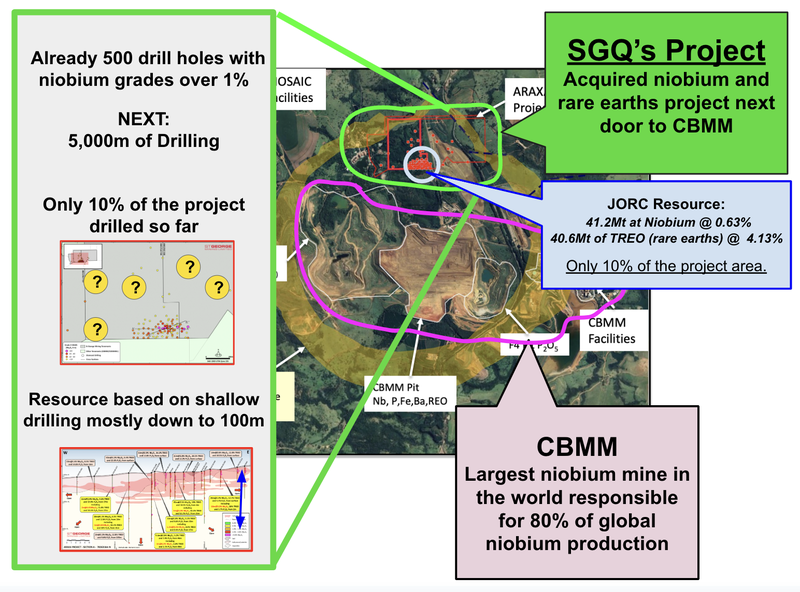

Yesterday we got a first look at a new JORC resource that is amongst the highest grade on the ASX for both niobium and rare earths.

These minerals are set to be in high demand over the coming decades as “critical minerals” - especially in high tech and defense applications - with the various global powers jockeying for control.

Our Investment St George Mining (ASX:SGQ) has delivered its maiden JORC resource for its advanced stage rare earths / niobium asset in Minas Gerais, Brazil.

SGQ is seeking to be next to market in the race to feed global demand.

Yesterday SGQ announced a maiden JORC resource for its project of:

- 41.2Mt at niobium grades of 0.63%, and

- 40.6Mt of rare earths at grades of 4.13% TREO (total rare earths oxide)

And SGQ hasn’t even drilled the project yet...

This first resource estimate is based on historical drilling, which was only on 10% of its ground.

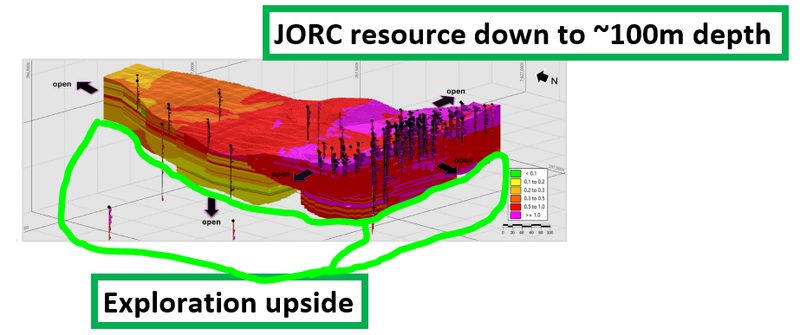

Mineralisation starts from surface.

The resource is open at depth, in all directions and is only based on drilling down to depths of ~100m.

SGQ is due to start drilling any day now to grow the resource...

SGQ is currently capped at ~ $53M.

Without having drilled a hole, SGQ’s rare earths resource is approaching a similar size and is almost double the grade of the ~$406M capped Arafura Rare Earths.

SGQ also has a similar grade to $6.5BN capped giant producer Lynas Rare Earths.

As for niobium, SGQ’s project is ~1/4 the size of WA1 Resources which is capped at ~$830M.

We will do a deeper dive comparison of SGQ’s resource to other larger companies and see how it stacks up later in today’s note.

SGQ’s resource is next door to the world’s biggest niobium mine

~80% of the world’s niobium supply is from the mine next door to SGQ, which is owned by one of the biggest private mining companies in the world CBMM.

It's a private company so there’s no easy way to determine its current valuation...

However we do know that way back in 2011, CBMM had a consortium of Asian investors pay ~US$3.75BN for 30% of its project - valuing CBMM at ~US$12.5BN.

That was over 14 years ago...

And the niobium market has come a long way since...

Fast forward to the last ~12-18 months, market interest in niobium companies has changed in a big way (for the better).

WA1 Resources made its discovery in (you guessed it...) WA, and was at one stage capped over $1BN.

WA1 then raised large sums of capital and drilled out its prospect and grew the resource.

Without drilling a single hole itself, SGQ’s resource is just under 1⁄4 of the size of WA1, and there is much more drilling to come.

WA1 is currently capped at ~$830M with an inferred resource of 200Mt at 1% niobium.

SGQ is currently capped at ~$53M with a resource of 41Mt at 0.6% niobium (the majority of the resource is in the Inferred category as well, similar to WA1).

WA1’s resource is in the middle of the desert, a long way from much infrastructure or market. SGQ is next door to the world’s biggest niobium mine, and in the middle of a mining state of 20 million people.

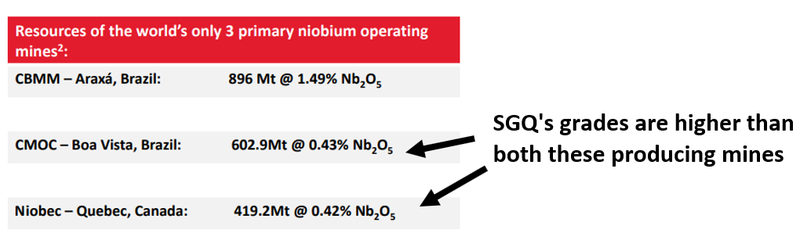

Currently WA1 and CBMM’s niobium assets are both higher grade and a lot larger than SGQ’s, BUT we think SGQ’s grades are stronger relative to the other two major producing mines in the world.

(there are literally only three major niobium mines on the planet)

The Niobec niobium mine in Quebec, which is currently the third biggest producing mine in the world, has a resource with grades at ~0.43% (albeit on a much larger scale than SGQ).

That mine was actually acquired by a private group in 2015 for US$530M (again a time when there was a lot less interest in niobium... we wonder what it might be worth now).

So there is clearly long term sustained interest in large, producing niobium assets around the world.

The next task for SGQ is to drill out its project to see just how big it can become.

Based on company timelines released to the ASX, we think that drilling will start very soon.

SGQ expects all of the drilling to be completed, reported, and the resource upgraded before the end of the year.

But it's not just niobium in SGQ’s resource - there’s also significant rare earths exposure.

Is the market missing the rare earths upside in SGQ’s resource?

Another part of yesterday’s announcement that we think the market may not be fully appreciating is the high grade rare earths component of SGQ’s JORC resource.

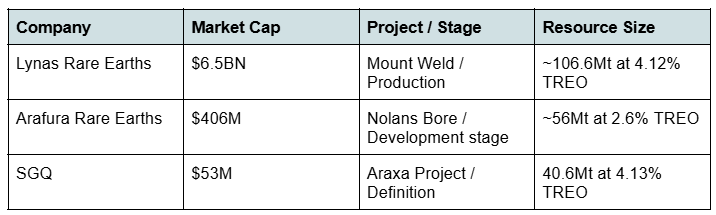

SGQ’s resource is almost half the size of the producing Mount Weld project owned by the $6.5BN capped Lynas Rare Earths.

AND it has very similar grades (which are as high as they get for hard rock rare earth assets).

Lynas’ project has a resource of ~106.6Mt at 4.12% TREO.

SGQ’s project has a resource of ~40.6mt at 4.13% TREO.

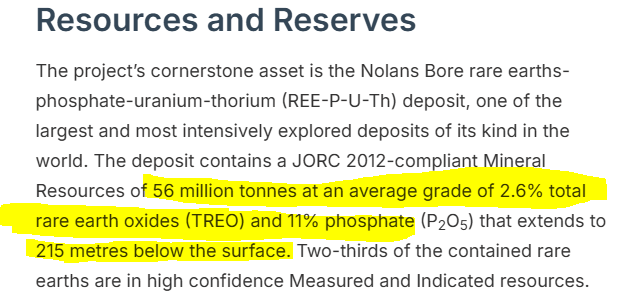

Comparing it to other big ASX success stories, the $406M capped Arafura Rare Earths’ Nolans Bore project has a ~56Mt resource with TREO grades of ~2.6% - much lower than SGQ’s.

Arafura’s resource is also based on drilling down to depths of ~215m... so there is potential for SGQ to even exceed Arafura’s project on a tonnage basis.

(Arafura’s Resource - Source)

Here is how the three rare earths projects stack up:

Remember SGQ is currently capped at ~ $53M...

We think that having rare earths grades that are almost identical to Lynas and bigger then some of the ASX’s big rare earths success stories will work in SGQ’s favour when market sentiment for rare earths projects changes.

And it has a niobium resource too...

After yesterday’s news, the market will now be able to compare SGQ to ASX listed niobium AND rare earth companies with established JORC resources...

The maiden resource estimate is well timed given SGQ is just about to start drilling again.

It provides a baseline for SGQ to grow.

While SGQ’s asset is advanced, exploration is still a big part of SGQ’s story.

As we mentioned above, only ~10% of SGQ’s ground has been explored to date and almost all of SGQ’s resource sits within ~100m from surface.

With deeper drilling to the north, west and east of its resource, we think the JORC resource has potential to grow from its current size and classification.

In today’s note we will breakdown:

- The exploration upside on SGQ’s project

- The ‘location premium’ we think SGQ’s asset deserves (infrastructure rich and starting from surface)

- What we want to see next from SGQ

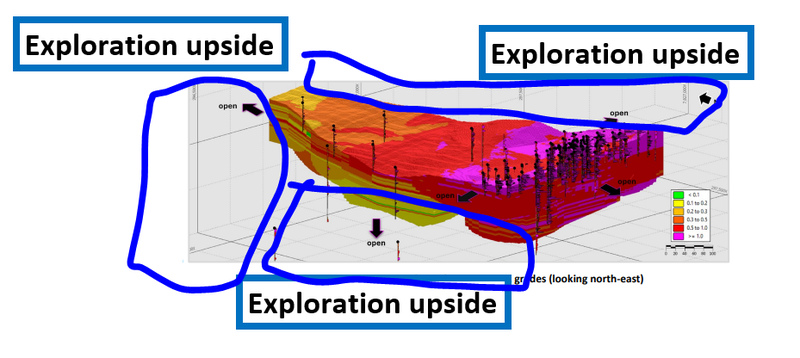

Exploration upside on SGQ’s current JORC resource

A key reason for our Investment in SGQ was because of the additional value built from drilling out the project.

SGQ acquired its project from a phosphate producer listed on the TSX called Itafos (who now holds 10% of SGQ).

For years Itafos has been focussed on producing phosphate from its nearby assets and so hasn’t put any meaningful capital into this niobium project... even though the market was interested in niobium.

SGQ’s project hasn't been drilled for years and has had almost no work done on it during the current positive market sentiment for niobium.

At the moment, almost all of the JORC resource is limited to depths of ~100m.

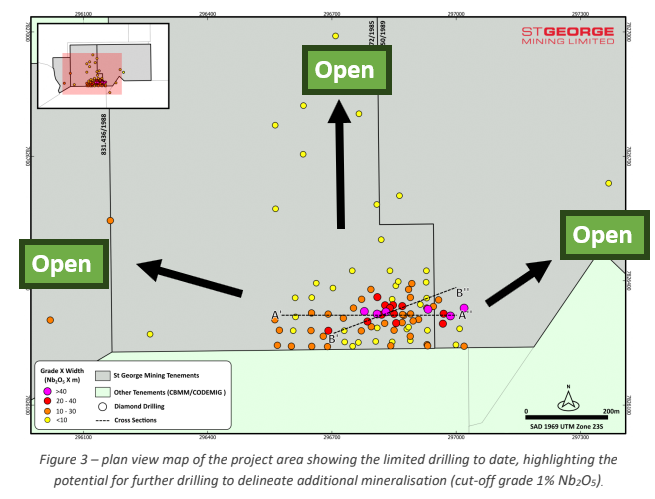

AND the drilling has been on only ~10% of the project area:

For SGQ’s upcoming drill program we want to see SGQ do two things:

- Extend the JORC resource below 100m.

- Extend the JORC resource ot the east/west and north of the current resource

Here is a very basic 3D view of where we want to see SGQ drill (excuse us, we are not artists):

SGQ expects all of the drilling to be completed, reported, and the resource upgraded before the end of the year.

Any upgrade to the JORC resource will be good news especially given the potential economics of a project even smaller than yesterday’s resource.

Back in 2012, SGQ’s project had a Preliminary Economic Assessment (PEA) done on it using the previous foreign resource.

That study was done using a foreign resource of ~27Mt resource with niobium grades between 0.64%-1.02% and rare earths with grades between 3.99%-5.01%.

(That PEA showed the project as having a Net Present Value (NPV) of US$967M)

SGQ’s JORC resource is now almost TWICE that size.

Remember SGQ is capped at $53M...

Any upgrades to the JORC from here could be good for when SGQ takes the project into feasibility studies again.

Could SGQ’s JORC resource command a “location premium”?

Earlier in today’s note, we did a very ‘back of the napkin’ comparison between SGQ’s niobium resource and WA1 Resources.

The markets usually like to compare companies going after similar commodities on resource/valuation ratios.

But we think valuing resources on size and grade alone isn't enough.

It’s also important to try and understand where those resources are, what type of geology they sit inside and most importantly how hard it would be to get those resources developed.

That’s where we think SGQ’s project is best positioned.

A big reason for our Investment in SGQ is because of how close the project is to existing infrastructure.

REASON 5: Project sits next door to the largest niobium producer in the world

SGQ is next door to CBMM, which supplies 80% of the global niobium market. SGQ’s project sits on the same geology as CBMM.

Source: “Why did we Invest in SGQ?” - SGQ Investment Memo 6 August 2024

Having access to all that infrastructure and workforce on its doorstep means it is much faster and cheaper to bring a mine into production.

It's been interesting to observe SGQ’s hiring of a number of former CBMM executives over recent months, with a significant amount of experience with the mine next door.

We think that the project's location (next door to an existing niobium mine) and access to all the infrastructure/human capital should mean SGQ’s project should trade with a “location premium”.

Location premiums are a large part of what drives mergers and acquisitions in the mining space.

Thinking back to the lithium market of 2023, lithium prices were trading near their lows, but all the lithium stocks in Western Australia were trading near all-time highs.

We think the only logical reason for that disparity was the “location premium” - Gina Rinehart, MinRes, SQM and Albemarle were all trying to takeover WA hard rock assets, so the market was inflated relative to the rest of the world.

The same is happening in the gold sector right now...

WA assets at or close to production are being bid up by the majors, whereas assets in other jurisdictions are being neglected.

It’s a simple case of the bigger players going toward jurisdictions/specific regions where they have a clear line of sight to an operating mine.

For SGQ, the clear line of sight is CBMM’s mine next door.

We think the same sort of “location premium” could be placed on SGQ’s project IF SGQ can advance it to the point where another party could come in and fund it into production.

What we want to see next from SGQ

In the short term we want to see SGQ kick off its drilling.

We think this could begin any day now given last month the company flagged “drilling to begin this month”... and we have just ticked over to April.

Beyond that, over the next 12-18 months, a lot of the catalysts for SGQ could come at hard-to-forecast times:

- Progress on strategic investors/offtake partners - hopefully SGQ can follow up the $8M cornerstone investment it managed to get from Xinhai Group - a global mining services provider - as part of its last raise.

- Finalise the remaining vendor payments - US$6M is due in ~9 months and then another US$5M in ~18 months.

- Start working on development studies - SGQ has mentioned some of these workstreams are already underway.

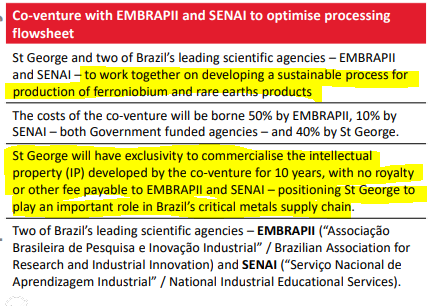

- Updates on downstream processing processing venture - SGQ is also working on a downstream processing process for niobium/rare earths products. This could be additional upside if SGQ manages to make any material progress on this front.

(Source)

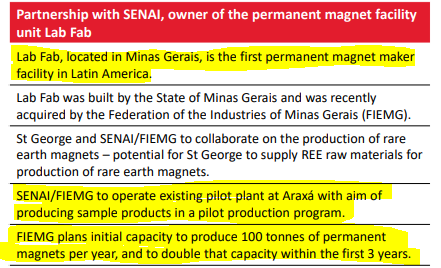

- Pilot plant trials - SGQ has an agreement in place with Latin America’s only permanent magnet maker.

(Source)

- Permitting - SGQ is working with the same consultants that worked on Sigma Lithium and Latin Resources projects (two large lithium players in the same region of Brazil, Minas Gerias). Permitting targeted for full completion by Q4, 2026.

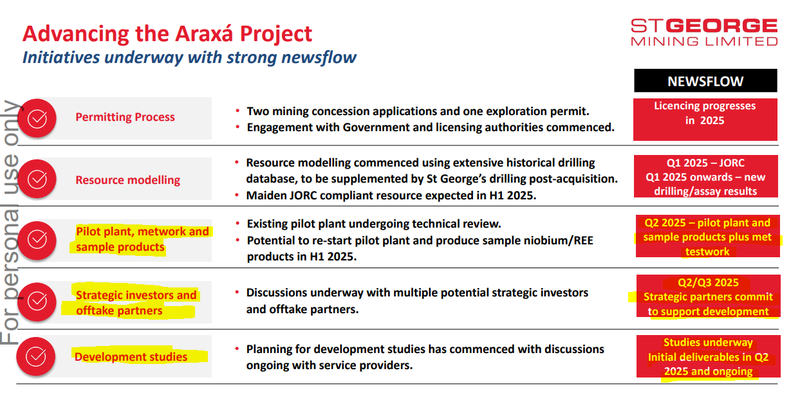

Here is the slide in SGQ’s most recent corporate presentation which lays out what to expect in 2025:

(Source)

Ultimately, as SGQ progresses’ its project, we are hoping it achieves our Big Bet which is as follows:

Our SGQ Big Bet:

“SGQ defines a niobium/rare earths deposit large enough to take into development or attract corporate interest via a takeover at a market cap of >$500M”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SGQ Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

How does SGQ’s new JORC resource impact our SGQ Investment Memo?

Yesterday’s maiden JORC resource estimate from SGQ marks significant progress across Objective #3 from our SGQ Investment Memo.

Objective #3: Maiden JORC resource estimate & met testwork

Milestones

🔄Metwork updates

✅Maiden JORC resource estimate

Source: 6 August 2024 SGQ Investment Memo

Releasing a JORC resource is an important part of the development pathway for SGQ as it allows potential financiers and/or offtake partners to get a sense of the scope of the project.

Resources can act as important barometers for these parties as they compare their investment options and work to secure supply.

Meanwhile, SGQ’s JORC resource is also coming at a key time for critical minerals projects around the world which is relevant to two key reasons we Invested in SGQ:

Niobium is a critical mineral. Governments want it, SGQ has it.

80% of the global niobium supply is controlled by one company CBMM. Niobium sits as the second highest risk metal on the critical materials list for both the EU and the US for supply concentration.

Rare earths, with high grade TREO.

SGQ’s project also contains ultra high grade rare earths with TREO grades >10% in 10-60m intercepts. SGQ’s project sits on the same type of geology (carbonatites) as Lynas’ giant Mount Weld rare earths mine.

Source: 6 August 2024 SGQ Investment Memo

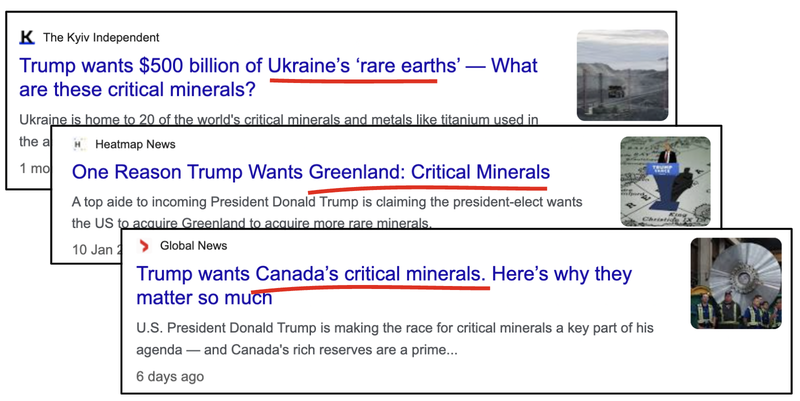

Taking a step back and looking at the global dynamics at play -

Concessions for “critical minerals” are seen as a key bargaining chip in the ongoing negotiations for peace in Ukraine...

Greenland is “on the table”, with the new US administration making overtures in order to access potentially huge deposits on the large island...

Trump has even talked about “taking over” Canada to access its raw materials...

And just in the last 24 hours, news broke that the US is looking to work on rare earths projects with... Russia?

(Source)

Whatever happens, we think the macro sentiment around the critical minerals on SGQ’s project will continue to be in strong demand in the current geopolitical environment.

What are the risks?

In the short term, the key risk for SGQ is “exploration risk”.

Exploration risk

A big part of our Investment is in seeing SGQ extend mineralisation at its project at depth and along strike.

There is no guarantee that drilling will return anything of significant commercial value for SGQ (either through weak grades or thin intercepts).

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

Beyond the drill program and SGQ’s resource upgrades, the main corporate risk is that SGQ will need to make the deferred payments due for the acquisition of its project.

SGQ has already paid the first US$10M of the acquisition costs.

Inside the next 9 months, the next US$6M is due, and in 18 months, the final US$5M.

IF SGQ struggles raising these funds it would likely have a negative impact on SGQ’s share price.

Deferred payments risk

To pay for the acquisition SGQ will need to make three separate payments totaling US$21M. The first US$10M installment is due on closing of the deal with the remainder due over the next 18 months.

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

Our SGQ Investment Memo

You can read our SGQ Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our SGQ Investment Memo covers:

- What does SGQ do?

- The macro theme for SGQ

- Our SGQ Big Bet

- What we want to see SGQ achieve

- Why we are Invested in SGQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.