Our New Portfolio Addition: West Coast Silver (ASX:WCE)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,863,000 WCE Shares at the time of publishing this article. The Company has been engaged by WCE to share our commentary on the progress of our Investment in WCE over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

We think silver is going to go on a generational run.

Silver has already done it twice in the last ~50 years - once in the late 1970s and again in 2011.

(we could be wrong of course, but just in case we are right, we are adding a new silver stock to our Portfolio today)

Big generational macro themes don't come around very often.

The lithium boom in 2020-22 - unlikely we see anything like that ever again in that sector.

Internet boom of the 2000s, unlikely we see that either.

During both booms, even the smallest companies reached market caps in the hundreds of millions (some in the billions).

We think the same is about to play out in silver in the near term.

Over the last few days the silver price has been pushing towards new 14 years highs.

Here is what the silver price looks like across ~25 years:

(source - silver spot price)

We think silver is going to continue its run to new highs.

Which is why today, we are adding West Coast Silver (ASX:WCE) to our Portfolio.

WCE’s project was one of the highest grade silver mines to ever produce in Australia - the Elizabeth Hill Mine.

It was also where the biggest native silver nugget in Australia was found - the 145kg Karratha Queen (we saw it in real life at the Perth Mint earlier this year):

(Source: our photo from the Perth Mint of the largest Australian native silver nugget in existence - this came from WCE’s current ground)

When WCE’s Elizabeth Hill mine was operating over 20 years ago, it produced 1.2M ounces of silver from just 16,830 tonnes of ore.

That means average grades during production were ~2,194g/t silver...

The mine was exceptionally high grade, but 20 years ago the silver price was US$5 per ounce, which made operations less economical.

(silver is US $38.3 today)

Then mining abruptly ceased in a single day due to a fall out between JV partners at the time, leaving a potentially untapped resource (source)

(Source)

We are Invested in WCE to see it:

- Drill out and make near-mine discoveries next to the Elizabeth Hill mine.

- Drill, discover and define Elizabeth Hill look-a-likes across its ~20 regional targets.

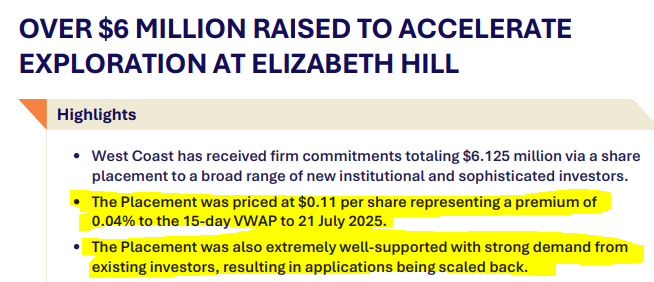

WCE just raised $6M at 11c, adding to its $1.4M cash balance at 30 June 2025. At last close WCE was capped at ~$45M.

Hopefully any new discovery is a high enough grade that WCE can use relatively cheap and easy processing methods - like on their old mine which was so high grade, the silver would separate using just gravity...

Based on the project's history, we think WCE is one of those small cap stocks that really has the potential to deliver ultra high grade drill results - which the markets reward in times of high silver prices.

Of course the company will still need to drill out the project and make new discoveries, which may not happen. Investing in small cap explorers is risky.

The type of mineralisation WCE is going after isn't about size/scale where lower grades are perfectly fine.

WCE is looking for high grade “ore shoots” which can be multiples the grade of any of the big silver mines that operate around the world.

(and then quickly and cheaply mined, processed and sold while silver prices are high - on site or toll treated at one of two nearby processing plants)

Since acquiring the project in March, WCE has already drilled 12 diamond drillholes to confirm and extend the high grade sections at Elizabeth Hill.

(10 assays are still pending from that drill program - which means we will be getting some near term newsflow)

So far, WCE has already hit a 21m intercept with silver grades of ~1,047g/t silver from its first hole. (source)

(which included a 1m intercept grading 15,071g/t silver).

So far WCE’s share price has responded well to that result.

WCE now has 10 more assays pending inside the next 4-8 weeks and will have more drilling start up right after.

We think the big re-rate for WCE could come from new discoveries being made near-mine (at Elizabeth Hill) or regionally across its undrilled targets.

While (hopefully) the silver price goes on a run...

No guarantees of course, this is speculative small cap investing in the commodities space - anything can happen.

Silver has had a great week this week, pushing towards $39 again and looking to retest new 14 year highs.

Here’s the historical silver price chart, where you can see silver price looking like it wants to retest new 14 year highs, especially in the last few days:

(source - silver spot price)

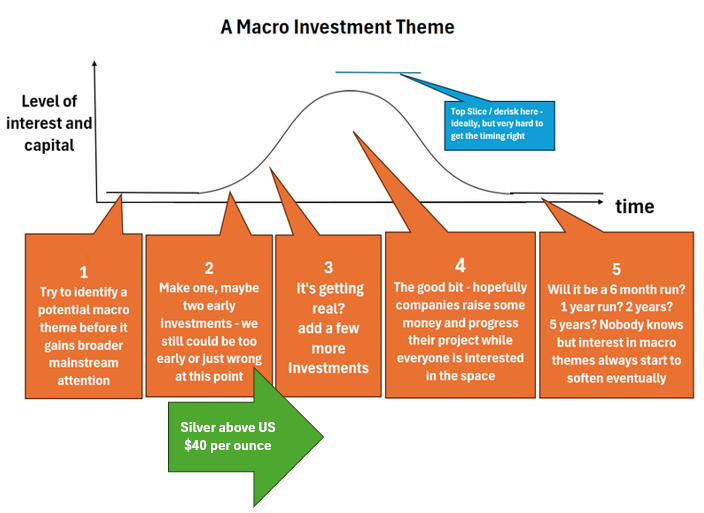

In our view, if silver finally goes above US$40 per ounce in the next few weeks, it will be the trigger to move the “silver macro theme” from stage 2 to 3 on our “macro theme interest” model - see below.

So it's time for us to add a third Investment in the silver theme (WCE) as it’s “starting to get real...”

We already added two silver stocks to our Portfolio over the last 18 months, while in our “stage 2” of the silver macro theme:

- Sun Silver (ASX: SS1) - currently up ~295% from our Initial Entry Price and was up ~582% at its peak.

- Mithril Silver and Gold (ASX: MTH) - currently up ~312% from our Initial Entry Price and was up ~715% at its peak.

Past performance of SS1 and MTH is no guarantee of future performance for WCE.

And with the silver price ticking towards $40 and into our “it’s getting real now” stage 3 for the thematic, we think a lot of attention and capital is going to start flowing into silver stocks.

Today we are releasing our WCE Investment Memo, which runs through:

- What does WCE do?

- The macro theme for WCE

- Our WCE Big Bet

- What we want to see WCE achieve

- Why we are Invested in WCE

- The key risks to our Investment Thesis

- Our Investment Plan

Before we get to our Investment Memo, here is a quick overview of the key reasons we Invested in WCE.

9 key reasons why we are Invested in WCE:

- We are bullish silver - We believe silver is heading to new all-time highs. A breakout could push prices well above US$50/oz, much higher than historic averages. Two of our top four positions in our Portfolio are silver companies right now.

- WCE’s project was one of Australia’s highest-grade silver mines - WCE’s project had historic production of ~1.2M ounces of silver at average grades of ~2,194g/t silver. A typical high grade project has grades around ~100g/t silver...

- WCE’s project sits on a granted Mining Lease - this gives WCE optionality with respect to getting its project back into production. IF the silver price gets high enough, WCE can get its project into production quicker than other greenfields assets.

- Historic production had cheap, simple processing - Historic mining used simple gravity processing because the ore contained visible silver nuggets easily separated from the surrounding rock. No need for chemicals or any other complex (expensive) processing routes.

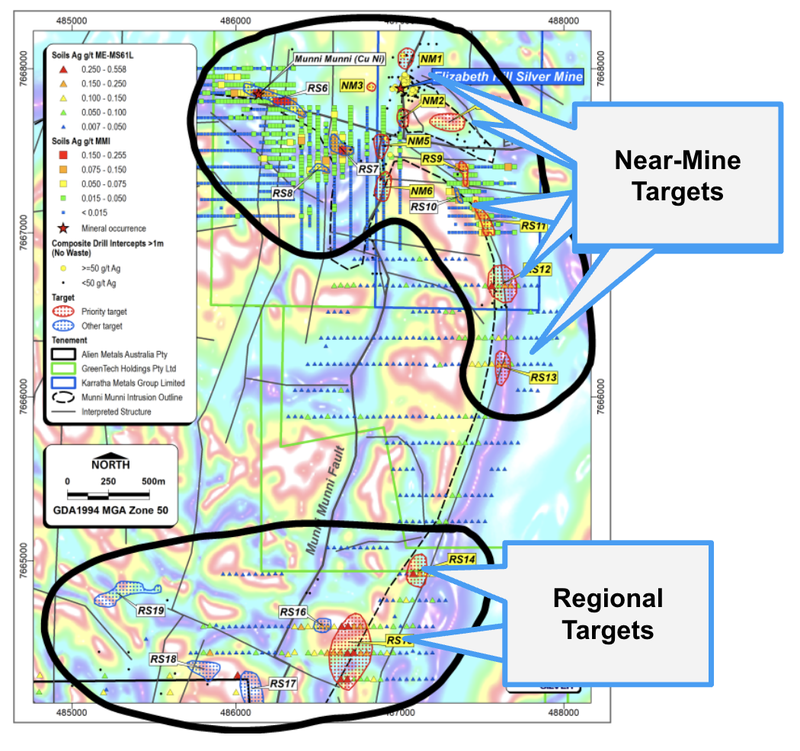

- Near mine exploration upside - WCE’s project hasn’t been systematically drilled for over 25 years. We think there is potential to make new discoveries near the old Elizabeth Hill Mine - with lookalike targets along strike.

- Already hit very high grade silver in the first few drillholes - WCE has already hit a 21m intercept with silver grades of ~1,047g/t silver (including a 1m intercept grading 15,071g/t silver). Post-results, WCE’s share price has gone from ~4c to a touch a high of 17.5c. (Remember past performance is not indicative of future performance.)

- WCE has 10 assays pending right now - WCE still has 10 assays pending from its first drill program, any strong results (similar to what came in from the first hole) into a rising silver price could be good for WCE in the short term.

- 20 regional targets ranked, exploration starting soon - There is very limited modern exploration over WCE’s regional targets. WCE just identified ~12 high priority and 8 earlier stage regional targets. These are the targets where we are hoping to see a repeat of the high grades at Elizabeth Hill. Air-core/channel sampling to start on these very soon.

- Record 145kg native silver nugget came from WCE’s mine - this is more a bonus reason really, it doesn’t drive the Investment decision but it certainly got our attention onto the project when we saw it in real life at the Perth Mint.

(Source: our photo from the Perth Mint of the largest Australian native silver nugget in existence - from WCE’s project)

WCE is funded following a recent $6M capital raise at 11c, and is set up to deliver some drill campaigns and potential new discoveries - and we are betting this can happen into a major run in the silver price.

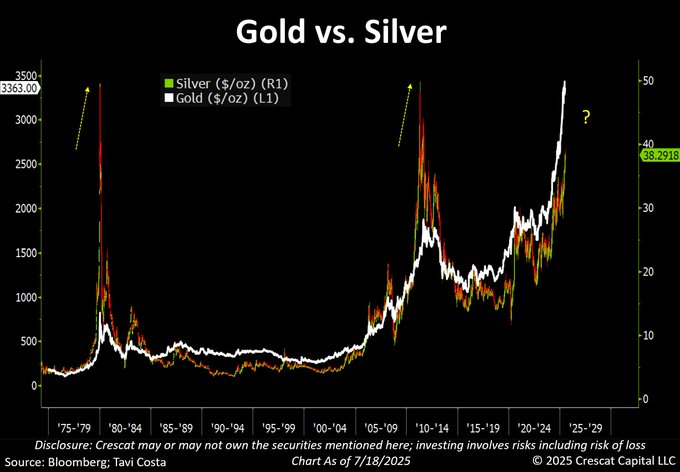

Why we think silver is about to go on a generational price run

(remember this is just our opinion, we could be wrong)

- Technical Breakout - Silver broke multi-year resistance in 2024–2025, triggering bullish technical patterns and signaling the potential for a major upward move.

Technical analysis is basically analysing a price chart to predict if a price will go up or down.

Whether you believe in it or not, there are enough people and traders out there who DO believe it that it can become a self fulfilling prophecy as they all act on what their charts tell them.

And currently the silver chart is threatening a “triple top breakout” which some technical analysts are saying could be the trigger for silver to do an explosive move higher (like gold did). - Persistent Supply Deficits - The silver market has been in a deficit for multiple years now (over 100 million ounces/year).

Most of the world’s silver production is as a by-product to another metal which means a supply response to increasing demand can be a lot slower than for other metals.

(that why we like companies with silver as their primary metal, not a by-product of mining other metals) - Surging Industrial Demand - Silver is the world’s most conductive metal and we think demand for silver will rise as technology advances.

Silver is currently being used in electronics, solar panels, EVs, and green energy sectors are driving demand sharply higher. - Historic Gold-Silver price ratio out of whack - The gold-to-silver price ratio remains historically high (around 80:1). To close that historic gap either silver prices will need to go higher OR gold prices will need to come down.

- Inflation Adjusted Upside - Historical peaks in silver, when inflation-adjusted, point to much higher levels ($100–$160/oz), suggesting current prices could be just the beginning of a larger, generational move.

- Major Institution predictions - Major institutions and analysts predict US$38 to US$50/oz for 2025–2026, with aggressive projections of US$75 to US$100/oz possible by 2030 if supply/demand imbalances deepen.

So, if the price of silver continues to run like we think it will (we could be wrong or too early in our prediction), then any high grade silver hits could build enough momentum for WCE to turn back on the old Elizabeth Hill mine.

Ultimately, we hope some or all of these reasons combined contribute to WCE achieving our Big Bet which is as follows:

Our WCE Big Bet:

“WCE re-rates to a market cap of $300M by bringing the Elizabeth Hill mine back online OR making a new discovery that is as big (if not bigger) than Elizabeth Hill into a strong macro silver theme.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our WCE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

WCE owns 70% of the Elizabeth Hill silver project in WA.

When it was in production, WCE’s historical mine was one of the highest grade silver producers in Australia.

Then the silver price fell to ~US$5 per ounce and mining abruptly ceased in a single day due to a fall out between the project’s JV partners at the time, leaving a considerable untapped resource. (source)

Again, when WCE’s project was operating, it produced 1.2M ounces of silver from just 16,830 tonnes of ore.

That means average grades during production were ~2,194g/t silver...

For some context - most operations these days are happy if grades are north of 50g/t...

Historic mining was done with very easy processing too.

The project had ore with visible silver nuggets, so it could be separated from the surrounding rock with simple gravity processing flowsheets.

No need for chemicals or any other more expensive processing routes... (which means things were likely to be low cost too).

(1.2M ounces of silver today is ~US$46M (~A$70M) produced using simple and cheap processing methods)

Since then, the project has barely seen any drilling on it - apart from a few holes in and around the old workings.

A big part of the reason we are Invested in WCE is because we think that the company could make new discoveries similar to what was mined at Elizabeth Hill in the past - both next to its existing mine infrastructure AND regionally:

Ideally WCE makes a discovery into a serious silver price run (which we THINK will happen BUT we can’t control or predict).

Earlier this week WCE ranked a total of ~20 near mine targets - 12 being high priority and another 8 that are slightly earlier stage. (Source)

Follow up work on the highest priority targets is next:

And here is the larger regional opportunity:

WCE has already hit a 21m intercept with silver grades of ~1,047g/t silver with its first round of drilling.

This also included a 1m intercept grading 15,071g/t silver.

That result was strong enough to take WCE’s share price from ~4c pre-drilling to a high of ~17.5c per share post-drill results:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

It also led to WCE’s most recent 11c capital raise which was actually done at a 4% premium to the companies 15-day VWAP...

(Source)

Most of the capital raise settled on the 31st of July which means WCE should have ~$7.4M in cash ($1.4M at 30 June 2025 + $6M from the cap raise) AND the placement stock has had a week or so to churn out on market.

(The small amount of tranche 2 shares still to be issued are going to directors and related parties and are subject to shareholder approval)

WCE now has 10 more assays pending inside the next 4-8 weeks and will have more drilling start up right after.

We think the big re-rate for WCE could come from new discoveries being made near-mine (at Elizabeth Hill) or regionally across its undrilled targets.

And hopefully (if they happen) they are announced when the silver price is running...

(Source)

More on why we like silver right now

Right now two of the top five positions in our Portfolio are silver stocks - SS1 and MTH.

And we think now is the time to add more exposure to silver.

Just before a big breakout in silver prices hopefully eventuates, and a broad-based rally across the very few silver names on the ASX.

(This works for us and our personal investment strategy and risk profile, it may not work for yours)

Last weekend we talked about how macro thematics morph into super thematics in 5 stages.

Read the weekender note here: Catching the Next Wave: LKY, Critical Minerals & Our Portfolio Strategy

Right now we think silver is firmly in stage 2 approaching stage 3 - which is where we want to add some more exposure.

Just before the big move into stage 4 where everything starts getting frothy.

Silver is flirting with US$40 and we think a clean break of that level will kick the macro thematic into stage 3 where companies are being re-rated higher.

Remember this is all our opinion, the future is very hard to predict - we could be wrong in our investment thesis.

Before you read the below, please remember that commodity prices can go both up and down.

Always invest with caution when it comes to small cap ASX stocks. The past performance is not indicative of future performance.

Technical Analysts (people who analyse charts for a living) are calling for the silver price to “do a gold” now after breaking out of a triple top.

(Source)

One macro analyst that we follow - Otavi Costa - thinks silver has “one of the largest cup-and-handle formations” he has seen in his career:

(A cup and handle is a setup that technical analysts believe is a precursor to a big move higher).

(Source)

We also recently watched the following video with Eric Sprott (the godfather of silver in markets).

In the video he talks about how there could be a “commercial short squeeze” in silver markets because:

- Silver is used in the military - Sprott says “all of those missiles being fired off”, “they use a lot of silver”.

- Silver deliveries on the COMEX are at all time highs - Sprott talks about how actual physical deliveries are happening now, which wasn't a thing on the COMEX in the past.

- Silver's suppression era is ending - Sprott talks about how banks have been short paper silver for decades and are finally starting to unwind these positions as demand for physical delivery increases.

(Watch Sprott's most recent take on the silver market here: full video here)

Sprott makes the case for silver from a fundamental perspective...

Can silver “do a gold”?

We have shared this video a few times with technical analyst Michael Oliver who said: “If silver goes above $35, watch out because if it goes above $36 it's a triple top breakout”.

(since then silver has broken through both those levels)

And then Michael said “we are going to get another launch” and when we get it “it will be at a speedier process than what gold is currently doing”.

Remember of course that this is only his opinion and he could be wrong.

Gold is currently trading at all-time highs and is up over 100% over the last 18 months.

IF silver does anything like that, it could trade above US$50/ounce.

Technical analysis is basically analysing a price chart to predict if a price will go up or down.

Again, whether you believe in it or not, there are enough people and traders out there who DO believe it that it can become a self fulfilling prophecy as they all act on what their charts tell them.

And currently the silver chart is threatening a “triple top breakout” which some technical analysts are saying could be the trigger for silver to do an explosive move higher (like gold did).

And finally, here is our WCE Investment Memo:

Investment Memo: West Coast Silver (ASX:WCE)

Memo Opened: Friday, 8th August

Shares Held: 4,863,000

Initial Entry Price: 7.7c

What does WCE do?

WCE holds 70% of the Elizabeth Hill silver project in WA.

Elizabeth Hill was one of Australia’s highest grade silver mines when in production.

We are Investing in WCE to see it make repeat high grade discoveries.

What is the macro theme behind WCE?

Silver serves as both an industrial and a precious metal.

As a precious metal, silver is often used as a hedge against inflation, a relevant factor given the persistently high inflation at the time of writing.

On the industrial side, silver plays a key role in the production of photovoltaic cells used in solar panels, making it an important material in the global energy transition.

Our WCE Big Bet:

“WCE re-rates to a market cap of $300M by bringing the Elizabeth Hill mine back online OR making a new discovery that is as big (if not bigger) than Elizabeth Hill into a strong macro silver theme.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our WCE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 9 Reasons We Invested in WCE

- We are bullish silver

- WCE’s project was one of Australia’s highest-grade silver mines

- WCE’s project sits on a granted Mining Lease

- Historic production had cheap, simple processing

- Near mine exploration upside

- Already hit very high grade silver in the first few drillholes

- WCE has 10 assays pending right now

- 20 regional targets ranked, exploration starting soon

- Record 145kg native silver nugget came from WCE’s mine

What do we want to see WCE do next?

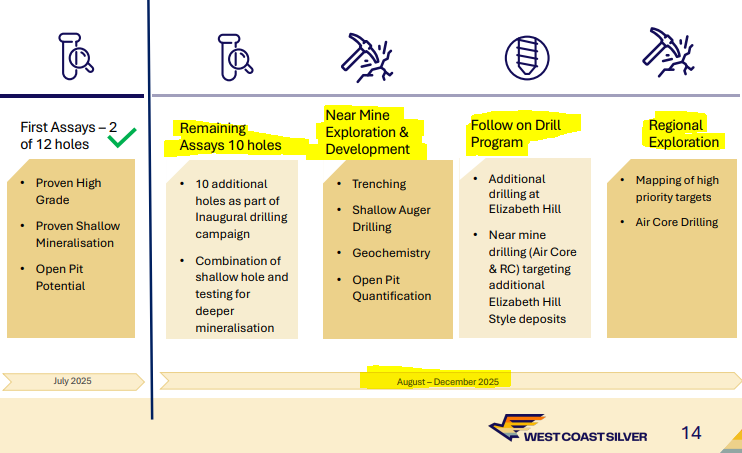

Objective 1: Assays from 12-hole drill program

WCE just completed its first 12 hole drill program on the project - assays from the next 10 holes are currently pending.

Milestones:

🔄 Assay results from remaining 10 holes

Objective 2: Target generation - near Elizabeth Hill mine

We want to see WCE do some geochemical sampling and shallow aircore drilling to rank new targets next to the Elizabeth Hill mine.

Milestones:

🔲 Soil Sampling

🔲 Trenching results

🔲 Identify drill targets

🔲 Permit for further drilling

Objective 3: Target generation - regional targets

WCE’s project area covers ~180km^2. We want to see WCE run geochemical sampling and geophysics across the broader land package and rank new drill targets.

Milestones:

🔲 Geochemical sampling (soils, trenching)

🔲 Geophysical surveys

🔲 Identify drill targets

Objective 4: Second drill program starts

We want to see WCE kick off its second round of drilling and have results out to market before the end of the year.

Milestones:

🔲 Drilling permits granted

🔲 Drilling starts

🔲 Assay results

What are the risks?

Exploration risk

There is no guarantee that WCE’s upcoming drill programs are successful. WCE may fail to find economic deposits of silver.

Funding risk/dilution risk

As a pre revenue explorer WCE is dependent on capital markets to fund ongoing drilling and development.

Although it recently raised $6M, future exploration may require additional fundraising.

That could come at discounted prices and further dilute existing shareholders.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver prices fall, this could hurt the WCE share price.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking WCE’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

What is our Investment Strategy?

Our plan is to hold the majority of our position in WCE for a minimum of 12 months as part of our Catalyst Hunter exploration portfolio, which we hope is enough time to see WCE drill out its project, make a discovery and the silver price to go on the run we hope it will.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates in line with our minimum hold conditions.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.