Our New Portfolio Addition is ASX:L1M

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 6,360,712 L1M Shares, 3,180,357 L1M options, and 1,400,000 Bengal Mining shares. The Company has been engaged by L1M to share our commentary on the progress of our Investment in L1M over time.

We’re going back to Brazil for lithium.

To roll the dice again on a potential new large lithium discovery right next to one of our all time best Investments.

Our new Investment is an early stage, micro cap explorer:

Lightning Minerals (ASX : L1M)

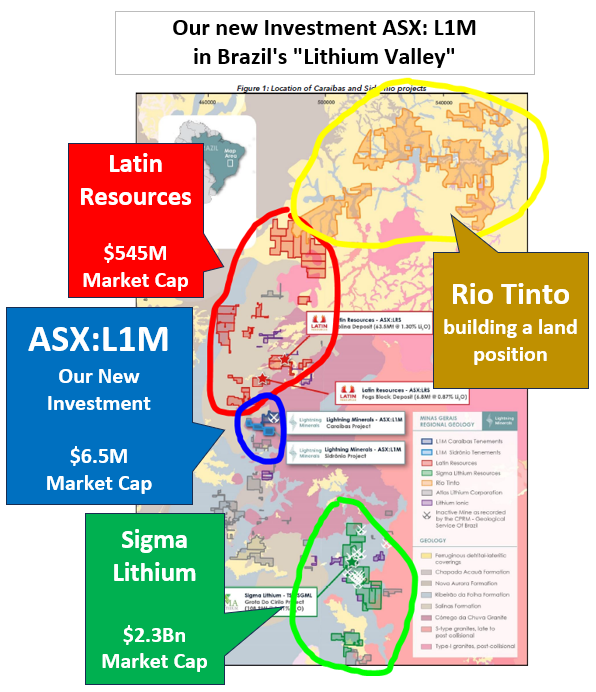

L1M’s new ground in Brazil sits in between the now prominent Latin Resources’ lithium resource and Sigma Lithium’s producing lithium mine.

In Brazil’s “Lithium Valley”. In the same geological trend...

And Rio Tinto has been building a land position there too...

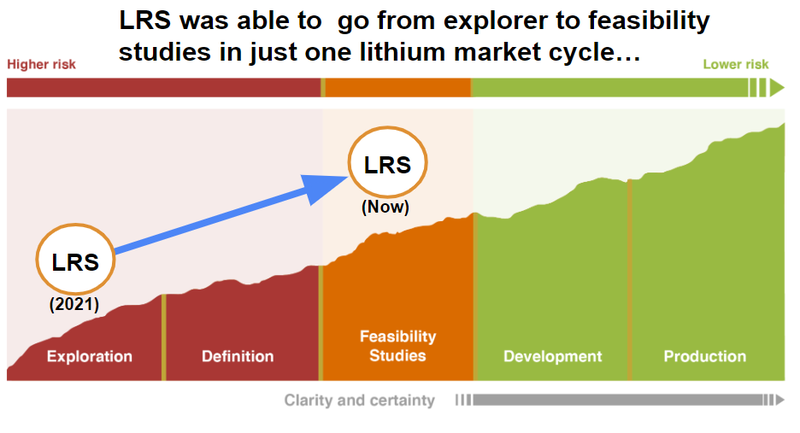

After our success with LRS (it went from 2c to a high of 42c, now at 20c) we looked at (and been approached by) a number of different Brazilian explorers and new “Lithium Valley” hopefuls.

$6.5M capped L1M is a new early stage exploration bet we are putting on to hopefully emulate some of LRS’s success in Brazil’s “Lithium Valley”.

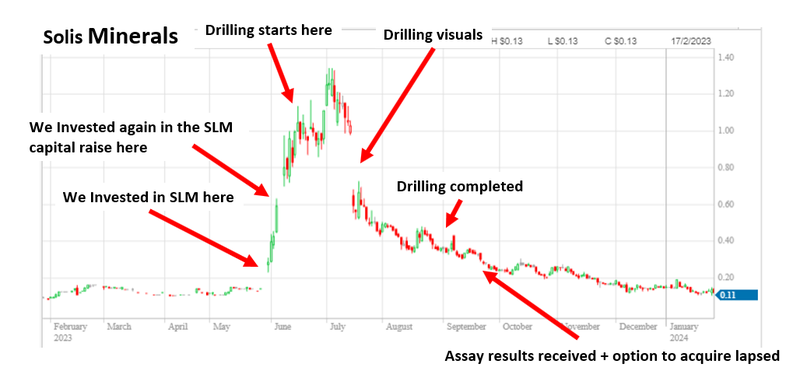

After our success with LRS, we “rolled the exploration dice” again with SLM back in May last year.

SLM had an amazing run in June 2023, running from ~13c to $1.34.

But unfortunately the drill bit didn’t deliver for SLM and its share price has come back to where it started while it looks for a new project.

Remember that exploration is high risk, just because LRS was successful and the SLM share price performed well pre-drill results, does NOT mean L1M will do the same. Drill results can be disappointing and the share price will respond downwards accordingly.

This can happen in exploration, but as always we are rolling the dice again.

While we hold and wait for SLM to find a new project, we have made an Investment in L1M, another explorer looking to become the “next LRS”.

After looking at a bunch of new projects, (specifically IN the Lithium Valley, this time much closer to LRS and Sigma) L1M’s new projects won.

We like L1M’s capital structure given there are not too many shares on issue - this is good as in the upside case (L1M makes a lithium discovery) the share price can materially re-rate.

And in the downside case (if no lithium is found in Brazil), it still has the capacity to find another asset and do a deal that is not too dilutive to shareholders.

Today, we are launching our L1M Investment Memo. This Memo includes why we invested, what we expect to see in the lead-up to L1M’s drilling, and, importantly, the near-term risks we have identified and accepted prior to making this Investment in L1M.

L1M today announced it has projects in Brazil's Lithium Valley, via a proposed acquisition of Bengal Mining Pty Ltd.

We are also investors in Bengal. It's worth noting that this transaction deal still has to go to a shareholder vote via EGM. When we said it was ‘early stage’, we meant it. We also just participated in the L1M placement at 7c.

Here is an overview of the 11 reasons we Invested in L1M:

- We have had success Investing in Brazilian lithium before - One of our best Investments was Latin Resources, which made a hard rock lithium discovery and was re-rated to a high of ~42c per share—2,332% above our Initial Entry Price. L1M is following the same exploration playbook, 20km away.

- Two of Brazil’s biggest lithium projects are near L1M - L1M’s ground sits between $545M Latin Resources (20km away) and $2.3BN Sigma Lithium (60km away), both of which are the big pioneers of the lithium industry in Brazil.

- Minas Gerais is Brazil’s “Lithium Valley” - The state aims to be the biggest lithium province in Brazil. The “Lithium Valley” concept was launched in the State of Minas Gerais to promote foreign investment in Brazilian lithium projects.

- Rio Tinto moving into Minas Gerais in a big way - Rio Tinto has started pegging ground to the north of LRS and Sigma. Could Rio Tinto be setting up for a play on the region as a whole? Rio is already active in Argentina so South American assets are definitely not out of their remit.

- L1M’s project sits on similar geology to LRS and Sigma - L1M’s ground sits on top of similar geology to where Latin Resources made its discovery (the Salinas Formation). The projects also sit within similar proximity of the granites in the region & has similar aeromagnetic data running through the ground.

- Exploration “roll of the dice” - Our other Investment SLM was trying to find lithium in Brazil, and it ran from ~13c to ~$1.34 per share. Unfortunately it didn’t deliver a discovery (yet, we still hold). We are betting on L1M as another early stage “the next LRS” exploration bet to hold in our Portfolio.

- Bear market pick up - L1M is picking up ground in a lithium bear market, which means the likelihood of finding higher-quality, well-priced projects is higher.

- There is an existing playbook for success in Brazil - Companies like Sigma have gone from <$100M market cap explorer to a peak market cap >$4BN. Latin Resources has gone from <$20M market cap to a peak of ~$1BN. There is a proven valuation re-rate for companies that manage to make hard rock lithium discoveries in the region.

- Tight capital structure - After acquiring the Brazilian assets, L1M will have ~99M shares, which means there aren't many shares on issue. The top 20 hold ~47%, and the board and management hold ~8.7% of the company’s shares on issue.

- Low market cap leveraged for a re-rate on a discovery - Post acquisition at 7c per share, L1M has a market cap of ~$6.5M leaving plenty of room to re-rate off the back of a discovery, especially given the peer valuations in the region like Sigma and Latin Resources.

- Good deal terms tied to success on the project - Bulk of the consideration being paid for the assets are tied to milestone payments related to defining a JORC resource, NOT the usual “lithium bearing drill intercepts” we see on project acquisitions.

Yes, this is an early stage exploration bet, and at $6.5M the company’s market cap is tiny.

However, L1M is on the same geological trend as LRS and Sigma, and the publicly available aeromag data shows L1M has ground in the right place.

And there’s already lithium in rock chips at the new acquisition.

This is all a nice start, but it's still very early stage. To progress things, there’s an aggressive exploration strategy in place.

In the background, lithium prices have moved up gently after a big slump and look to be holding a new level.

We think L1M's acquisition is well-timed and well priced, which is just part of the reason we have Invested.

Our previous experiences Investing in Brazil tell us two things:

FIRST - the best time to pick up lithium projects is in a down market - this is where the biggest re-rates can come from.

Second - Brazil’s “Lithium Valley” is an excellent area of the world to Invest in for exploration.

L1M fits the bill for us.

Latin Resources, helmed by Chris Gale, picked up its Brazilian lithium project when lithium sentiment was at a low point in 2019.

Great timing.

But Latin’s success prompted a land rush on this part of Minas Gerais in Brazil since they announced a lithium discovery.

Vendors of assets could suddenly charge far more for their projects.

(and they did - or tried to)

But then the tide went out again - the lithium price got smashed in 2023, shedding circa 80% in price.

Our new Investment, L1M, has taken advantage of the lithium market's weakness to strike what could prove to be a shrewd bargain.

It announced an acquisition just 20km south of Latin’s project - and 60km north of Sigma Lithium’s mine. Right between both of them.

Time (and drill results) will ultimately reveal if it was a bargain or not...

We’re confident that lithium prices will come back eventually - we think there’s just too much demand to come.

And if or more likely, WHEN that does happen, we hope L1M has made a discovery and pulled off a Latin-Style run.

Of course - the past performance of Latin should not be taken as an indicator of the future performance of L1M.

“1. Buy assets in a down cycle, 2. Make a large discovery in an up cycle and 3. Raise before prices cool.”

That appears to be the model for success from our experience.

To achieve all three of the above steps is not easy, and requires a fair bit of luck.

Success in exploration is rare, and this is a high risk Investment for us but we’ve seen what outsized returns like those generated by Latin can do for our overall Portfolio.

Noting that like everyone, we do get things wrong sometimes - even our last foray into Brazilian lithium, SLM - has not entirely worked out over the long term as we thought it would.

Our Big Bet for L1M is based on the ultimate upside scenario, and is the same as for most early stage exploration companies we Invest in:

Our L1M Big Bet:

“L1M returns 1,000%+ by making a discovery significant enough to move into development studies, or attract a takeover offer.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our L1M Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

We think it's a straightforward, attractive exploration Investment in what is quickly becoming a major global lithium hub in Brazil.

L1M has acquired a private company called Bengal Mining that holds option agreements over two lithium projects today in what’s called the Eastern Brazilian Pegmatite Province (transaction is still subject to shareholder approval).

This is the same area that includes “Lithium Valley” that Latin Resources’ operates in, as Sigma and others launched the region on the NASDAQ back in April 2023:

(Source)

It’s a highly prospective region.

BUT, now with a significantly lower lithium price, L1M has been able to secure what we see as a well priced project pick up at the right time.

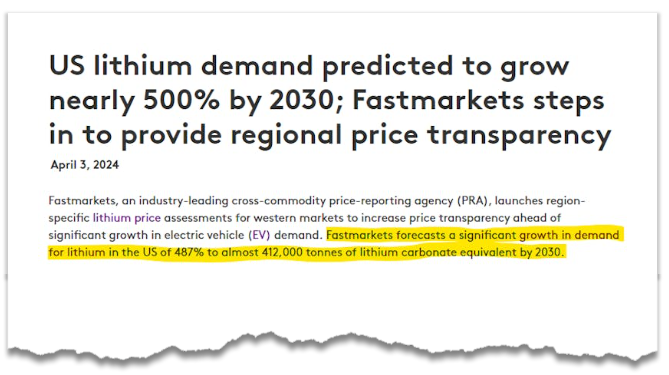

Lithium market fundamentals are a big topic of discussion - we see this as a demand driven story.

We picked up this recent report about US lithium demand:

(Source)

And new lithium supply has traditionally moved slowly into the market - LRS has been a great anomaly - advancing its project ultra quickly:

Below is a link to esteemed Canaccord Genuity analyst Reg Spencer talking about how he likes Latin Resources’ prospects.

We listened to the whole thing, and it was interesting to see Latin Resources singled out as one of Reg’s top picks for the next cycle...

(Source)

We’re Invested in L1M to hopefully see it ride LRS’ slipstream in a lithium market that returns to form.

So that we can follow the company’s progress over time and track our Investment, today we will be launching our L1M Investment Memo where we share:

- What L1M does

- The macro theme

- Our L1M Big Bet

- What we want to see L1M achieve

- Why we are Invested in L1M

- The key risks to our Investment Thesis

- Our Investment Plan

L1M Investment Memo

What does L1M do?

Lightning Minerals (ASX:L1M) is a hard rock lithium explorer with projects in Brazil (and also Western Australia, which are quite interesting too).

What is the macro theme?

Lithium is a critical material used in Electric Vehicle (EV) battery cathodes.

We believe battery metals are the most compelling investment theme of this decade with lithium supply deficits anticipated through to the end of 2030.

L1M will be looking to replicate the success of other Brazilian lithium companies like Sigma Lithium and Latin Resources.

Our L1M Big Bet:

“L1M returns 1,000%+ by making a discovery significant enough to move into development studies, or attract a takeover offer.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our L1M Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

11 Key reasons why we Invested in L1M:

- We have had success Investing in Brazilian lithium before - One of our best Investments was Latin Resources, which made a hard rock lithium discovery and was re-rated to a high of ~42c per share—2,332% above our Initial Entry Price. L1M is following the same exploration playbook, 20km away.

- Two of Brazil’s biggest lithium projects are near L1M - L1M’s ground sits between $545M Latin Resources (20km away) and $2.3BN Sigma Lithium (60km away), both of which are the big pioneers of the lithium industry in Brazil.

- Minas Gerais is Brazil’s “Lithium Valley” - The state aims to be the biggest lithium province in Brazil. The “Lithium Valley” concept was launched in the State of Minas Gerais to promote foreign investment in Brazilian lithium projects.

- Rio Tinto moving into Minas Gerais in a big way - Rio Tinto has started pegging ground to the north of LRS and Sigma. Could Rio Tinto be setting up for a play on the region as a whole? Rio is already active in Argentina so South American assets are definitely not out of their remit.

- L1M’s project sits on similar geology to LRS and Sigma - L1M’s ground sits on top of similar geology to where Latin Resources made its discovery (the Salinas Formation). The projects also sit within similar proximity of the granites in the region & has similar aeromagnetic data running through the ground.

- Exploration “roll of the dice” - Our other Investment SLM was trying to find lithium in Brazil, and it ran from ~13c to ~$1.34 per share. Unfortunately it didn’t deliver a discovery (yet, we still hold). We are betting on L1M as another early stage “the next LRS” exploration bet to hold in our Portfolio.

- Bear market pick up - L1M is picking up ground in a lithium bear market, which means the likelihood of finding higher-quality, well-priced projects is higher.

- There is an existing playbook for success in Brazil - Companies like Sigma have gone from <$100M market cap explorer to a peak market cap >$4BN. Latin Resources has gone from <$20M market cap to a peak of ~$1BN. There is a proven valuation re-rate for companies that manage to make hard rock lithium discoveries in the region.

- Tight capital structure - After acquiring the Brazilian assets, L1M will have ~99M shares, which means there aren't many shares on issue. The top 20 hold ~47%, and the board and management hold ~8.7% of the company’s shares on issue.

- Low market cap leveraged for a re-rate on a discovery - Post acquisition at 7c per share, L1M has a market cap of ~$6.5M leaving plenty of room to re-rate off the back of a discovery, especially given the peer valuations in the region like Sigma and Latin Resources.

- Good deal terms tied to success on the project - Bulk of the consideration being paid for the assets are tied to milestone payments related to defining a JORC resource, NOT the usual “lithium bearing drill intercepts” we see on project acquisitions.

What do we expect L1M to deliver?

Objective #1: Find high priority drill targets

- We want to see L1M conduct geochemical and geophysical surveys and determine the best drilling spots at its Brazilian lithium project.

Milestones

🔲 Geological mapping

🔲 Rock chip sampling

🔲 Soil sampling

🔲 Define high-priority drill targets

Objective #2: Drill high priority targets

- We want to see L1M drill its best targets.

Milestones

🔲 Drilling permits

🔲 Drilling starts

🔲 Drilling completed

🔲 Assay results

Objective #3: Exercise option to acquire Brazilian lithium project

- After de-risking the project, we want to see L1M exercise its option and acquire the project

Milestones

🔲 Exercise the option to acquire the project

Objective #4: Drilling at WA lithium project

- We want to see L1M do some more sampling work before drilling one of the priority targets at its WA lithium asset (Dundas)

Milestones

🔲 Geochemical/Geophysical surveys

🔲 Drilling starts

🔲 Drilling completed

🔲 Assay results

What could go wrong?

Exploration risk

L1M’s project is an early stage exploration asset. There is always a risk that L1M finds no targets worthy of drilling or that, even after drilling, the company fails to find any economic lithium mineralisation. As a result, exploration risk is one of the primary risks for L1M.

Deal completion risk

L1M’s Brazilian assets are yet to be acquired and will still need to have the “option to acquire” exercised. L1M will also need to get shareholder approvals for the transaction which is never guaranteed to proceed. There is always a risk that the deal isn’t completed and L1M ends up with no asset ownership. In that scenario, L1M’s share price would likely be impacted negatively, and it will likely seek other assets to complement its existing ones, which could take time.

Financing risk

L1M does not generate revenues and relies on raising capital to fund its exploration programs. If the market is unwilling to fund the company, it risks being unable to drill its project or offering large discounts to its share price when raising capital.

Commodity price risk

The lithium price is very volatile, given that the market is still in its infancy. There is a risk the lithium price fails to recover, and the valuations for greenfields explorers or new discoveries aren't as high as they would have been in a stronger price environment. Low lithium prices will impact L1M’s share price in the long run.

Market risk

Investors may shy away from high-risk investment opportunities like junior explorers if the broader market sells off. During market downturns, investors will look to pull capital away from high-risk investments. L1M is a junior explorer and may be impacted by these market-wide sell-offs.

Investment Plan

Exploration is high risk and share prices often can swing up and down before, during and after the drilling event.

Our plan is to hold the majority of the position into the drill results (in case L1M can deliver a “Latin Resources style” result), if the drill results are excellent or the price runs in the lead up to drilling we may Top Slice 20% of the position in line with our trading policies which you can read here.

If the drill results do not deliver, we are happy with the cap structure and back the management team to further test the West Australian assets or acquire a new project.

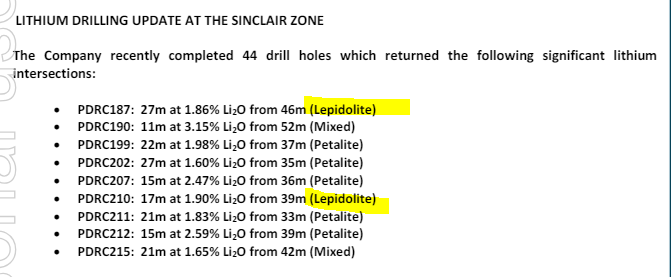

A few words on lepidolite

L1M is early stage exploration, and the company’s $6.5M market cap reflects this.

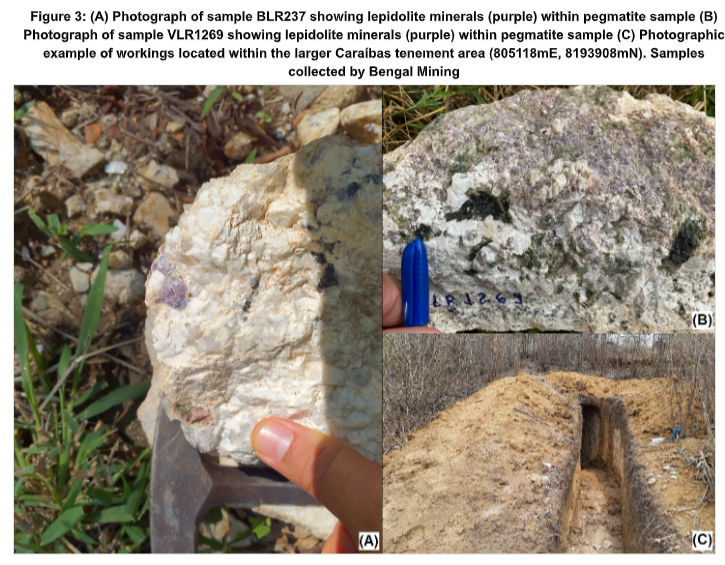

But we do have the early sniffs we are looking for - for starters, here is one of the rock samples with lithium in it:

We think that’s a good hint that it's a fertile area - and yes, we know lepidolite is not the most desirable lithium rock chip to have.

Spodumene is preferred.

🎓Learn: The different types of lithium projects explained

BUT - there once was a little company called Galaxy Resources with lepidolite on its project.

Galaxy Resources was trading at ~75c and had a market cap of ~$320M in 2019 during a low ebb for lithium, and is now one half of Alkem which eventually merged with Livent in December of last year in a ~$10BN merger.

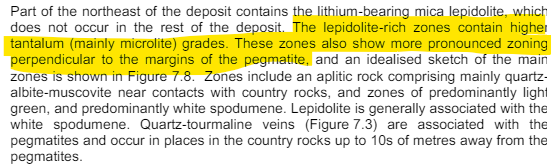

Short explanation - lepidolite and spodumene aren’t mutually exclusive - giant lithium resources can have both.

Here’s an excerpt of Galaxy Resources NI43-101 Technical Report from what is now the large lithium producing Mt Cattlin project:

(Source)

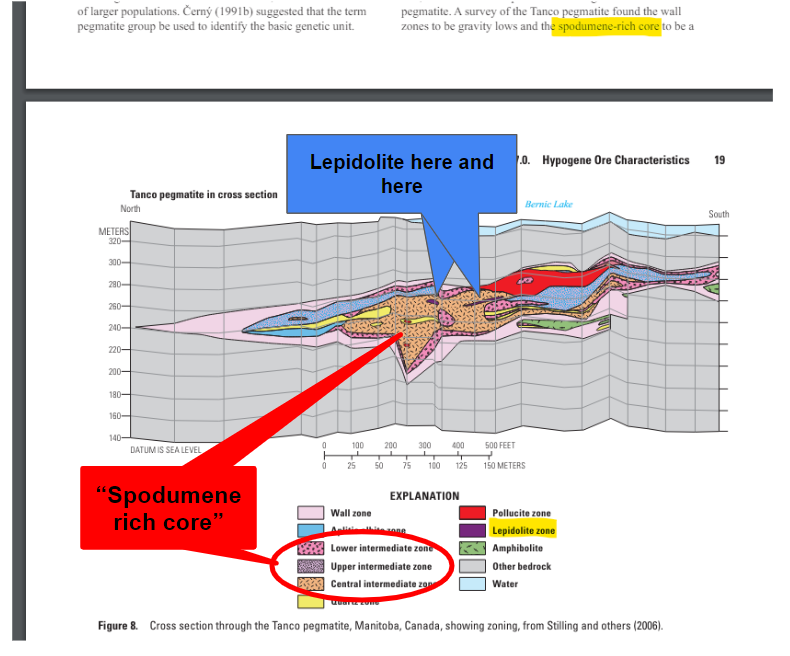

And here’s a map of the Tanco mine in Canada, which is owned by the large $6BN capped Chinese multinational mining company Sinomine (which happens to own a stake in another of our lithium Portfolio Companies, Tyranna Resources):

(Source)

That Tanco mine has a lithium grade of 7.3Mt at 2.76% lithium:

(Source)

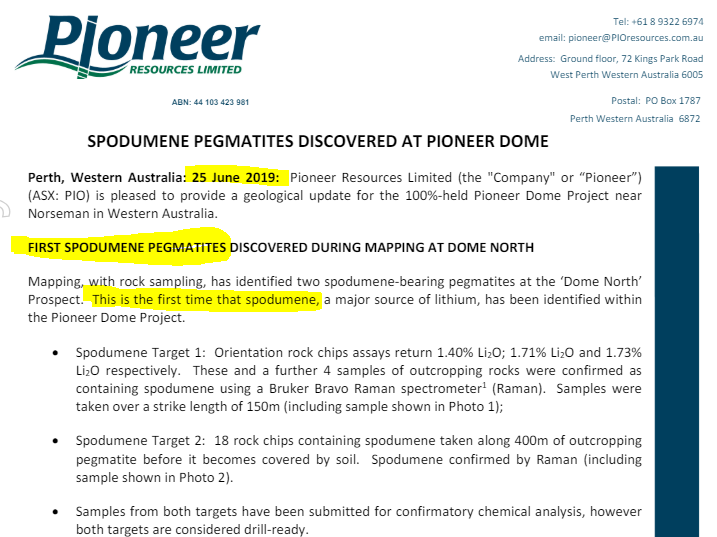

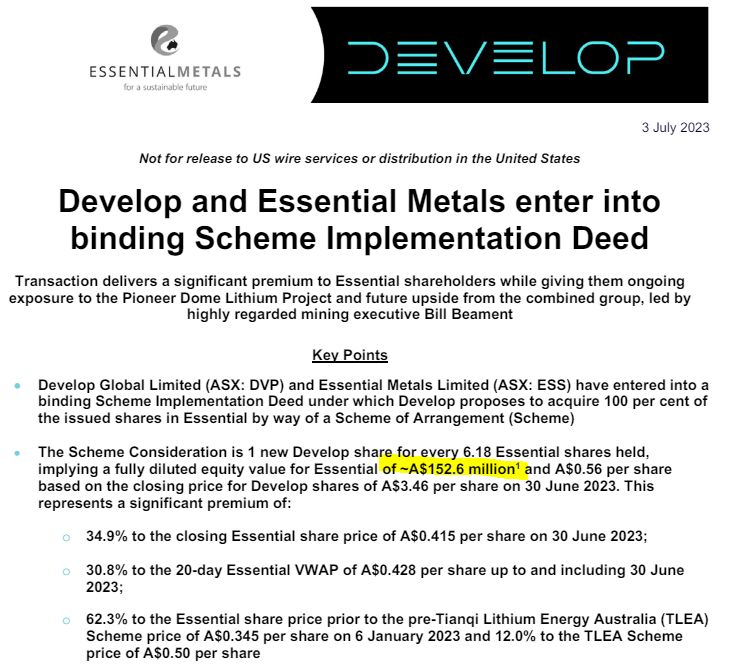

Another example is the Pioneer Dome project, which Develop Global took over from Essential Metals for $152.6M in 2023.

For most of the 2017-18 lithium bull market Essential’s project was largely seen as a lepidolite deposit - the market had labelled the project that way and was valuing the company appropriately.

The market had sort of written off the spodumene potential of the project.

Then, on June 25, 2019, Essential (at the time called Pioneer Resources) discovered spodumene-bearing pegmatites on the project for the first time...

Up until that point, Essential was trading with a market cap of <$30M for a lot of the time.

It spent the next few years drilling out the asset, putting together a maiden JORC resource estimate through to the eventual takeover by Develop Global for a valuation of ~$152.6M.

Without being geologists, we think this means that that L1M there’s a chance there could be on the outskirts of a spodumene bearing pegmatites, like we’ve seen in Canada with the Tanco mine and with Essential Metals in WA.

Taking into account L1M’s highly successful regional neighbours LRS with 70.3Mt @ 1.27% and Sigma 94.3 Mt @ 1.40%.

And pegmatites have been sighted by geos on this project - which again is in a region of Brazil that holds 100% of the country’s lithium reserves.

Pegmatites are the host rock that often contains spodumene bearing lithium - so that’s also a good sign.

So that we can follow the company’s progress over time and track our Investment, today we will be launching our L1M Investment Memo where we share:

- What L1M does

- The macro theme

- Our L1M Big Bet

- What we want to see L1M achieve

- Why we are Invested in L1M

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.