Our New Investment: Investigator Resources (ASX: IVR)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 13,714,286 IVR Shares at the time of publishing this article. The Company has been engaged by IVR to share our commentary on the progress of our Investment in IVR over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

We think silver is going to go on a generational price run.

And by generational run we mean a big run to new all time highs.

It looks like it has already started with the silver price hitting a new record high this week, and getting closer to hitting its all time high.

(but we are always mindful that commodity prices can go down as well as up)

Taking lessons learned from the last ASX small cap bull market in 2020 (in lithium), we have been on the hunt for a real silver stock, with a real project, close to building a mine...

With a MD who has successfully built mines before...

BEFORE the silver price run really kicks off and takes real silver stocks with it.

Followed by the sudden deluge of new “early stage silver explorers with amazing rock chips next door to a mine” come to the ASX.

(Remember when that happened in the lithium bull market? It was the companies that were already lithium companies BEFORE the lithium run started that performed the best)

Our newest silver Investment is Investigator Resources (ASX:IVR).

IVR is an advanced stage, silver development stock.

We have Invested in IVR to see it produce its ‘first silver bar’.

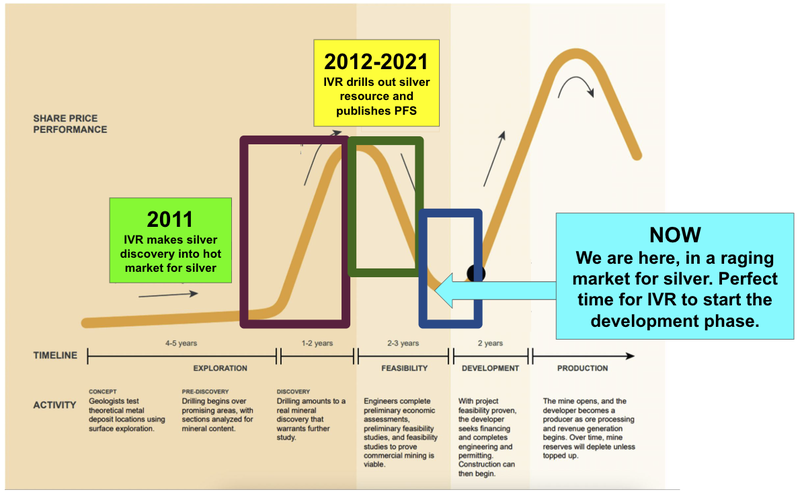

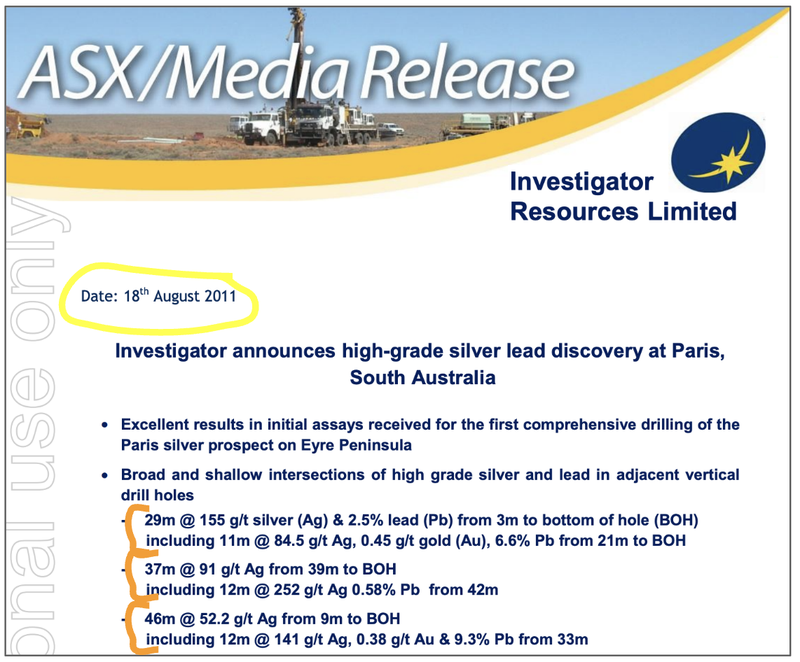

IVR first made its silver discovery way back in the last silver bull market of 2011.

Since then its been working up this now advanced silver project (14 years!) - diligently plugging away before silver has once again “become cool” in 2025 and started getting market attention.

IVR owns 100% of one of Australia’s highest grade pure play silver projects, located in South Australia.

It has a 57M ounce silver JORC resource estimate with an average grade of 73g/t.

Now that silver is coming back, the company is gearing up to develop its project into a mine and ramp up exploration to grow its silver resource (today’s capital raise gives them the cash runway for this).

IVR recently bought on a new Managing Director, Lachlan Wallace, former CEO and MD of Hillgrove Resources where he led the design, permitting, financing and restart of the Kanamantoo copper mine, also in South Australia...

We are backing him to do it again with IVR.

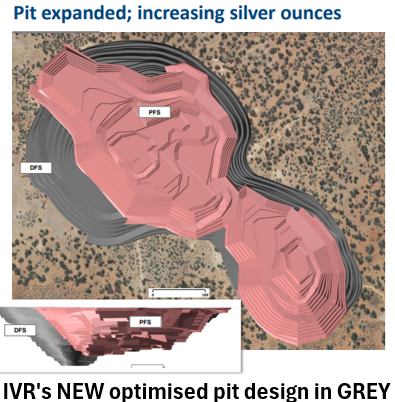

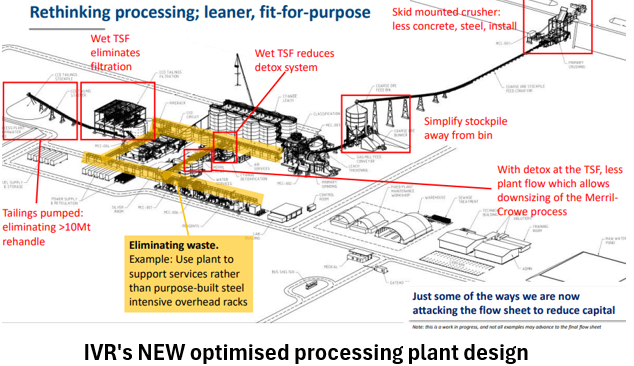

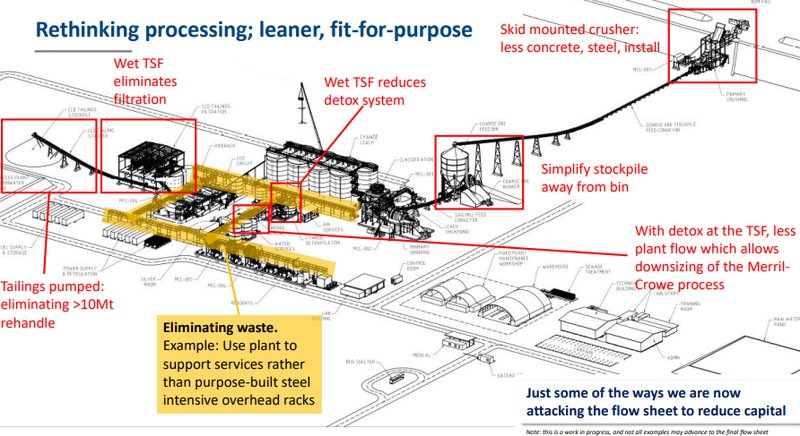

Lachlan is a mining engineer by background - so he will know exactly what needs optimising in the images below (IVR’s pit and processing plant design):

Ultimately, we want to see him use the coming silver bull market and renewed interest in silver to bring IVR into first production.

We Invested in IVR as we think it might run as the silver bull market shifts up a gear.

Many silver stocks have already started running... but IVR hasn’t really gotten going... yet.

(of course this is small cap resources investing - nothing is a guarantee, IVR might not go up as we think it will)

IVR just raised $10M at a premium to the 10 day VWAP from institutions including long term major holder Jupiter Asset Management (more on them below)... and us.

Now they have enough money to progress their Definitive Feasibility Study (the DFS is an economic study to support financing to build the mine, IVR expects to complete this next half).

AND at the same time aggressively explore to increase their silver resource (IVR’s existing resource could be part of a wider district scale silver corridor).

(the market loves exploration results when a commodity is running hard)

In the capital raise announcement this morning, IVR’s MD said:

“Every element of the strategy – permitting, DFS, exploration, and building the register – is directed toward one clear outcome:

Bringing forward first silver pour”

(source - Today’s IVR announcement)

Also, here is a video of the IVR CEO talking about the cap raise and plans for the $10M raised:

IVR’s major shareholder is Jupiter Asset Management, who hold 14% of IVR and invested again in the just completed $10M institutional capital raise.

Jupiter is a huge resource fund out of the UK with over £47.1 billion in assets under management (yep... BILLION)

We liked seeing Jupiter’s name on the IVR share register.

We’ve had success on Jupiter-backed silver stocks before:

- Mithril Silver and Gold - up 515% from our Initial Entry Price. Jupiter invested shortly after we Invested.

- Rapid Critical Metals - up 111% from our Initial Entry Price. Jupiter invested in the same round as us (like IVR).

So as we mentioned above, a DFS is in the works for IVR, and is due to be finalised and published next half.

The last study done on IVR’s asset was back in 2021 when the silver price was in the US$20’s.

That showed IVR’s project had an after-tax Net Present Value (NPV) of A$153M based on a 7-year mine life and A$131M of CAPEX.

That previous study was done using a silver price of US$27.35 per ounce.

And it showed that with an all in sustaining cost on silver of A$17.45/oz... (meaning the cost per ounce to produce the silver)

We are now in different times.

The silver price is currently trading at ~A$72/oz.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

(that old study also excludes all of the lead that the mine would produce and none of the exploration upside we think IVR has.)

We think that IVR’s updated DFS could come just as silver rips to new all time highs, and with all of the cost savings found during the ‘silver winter’, the feasibility study results could surprise to the upside.

Just enough to get a potential financier to back bringing the project into production...

(no guarantees of course - like any small cap ASX stock - a lot can go wrong with our investment thesis...)

Every time a commodity price rises, it sends the market a signal to get projects built and into production.

The last time the silver price was this high, IVR made its first silver discovery on this asset.

It spent well over 10 years in the silver bear market drilling it out, and now it is returning to the next stage of the Lassonde Curve at the perfect time with silver pushing all time highs:

We think that in this current silver up cycle, a few projects will come into production and a few big discoveries will get made.

We are Invested in IVR to hopefully see it become one of those projects that enters production during this silver bull cycle...

Later in today’s note we will share our updated IVR Investment Memo which will cover:

- What IVR does

- The macro theme for IVR

- Our IVR Big Bet

- What we want to see IVR achieve

- Why we are Invested in IVR

- The key risks to our Investment Thesis,

- Our Investment Plan

But before that, here is a summary of the 8 reasons why we increased our Investment in IVR.

8 reasons why we Invested in IVR

1. IVR has one of the highest-grade silver projects in Australia

IVR’s project has an estimated 57M ounces of silver at an average grade of 73g/t.

That makes it one of the highest grade primary silver deposits in Australia.

2. IVR project is at the advanced DFS stage

It is hard enough to go and make a mineral discovery, it is even harder to get a mine into production.

For the DFS stage companies that are in the market during a hot commodity cycle, securing project financing can become a whole lot easier.

We like that IVR is at this DFS stage and it can potentially be one of those companies that ‘survives the cycle’ and becomes a mine during this current silver bull run.

We also think that with a running silver price, IVR’s DFS could surprise the market to the upside in terms of project economics.

3. We are investing alongside Jupiter Asset Management

Jupiter Asset Management owned 14% of IVR (before today’s capital raise - that they also went into) and we are following them into the story.

Jupiter is a huge resources fund out of the UK with over £47.1 billion in assets under management.

We have had success investing alongside Jupiter with another silver story Mithril Silver & Gold, which is up 515% from our Initial Entry Price.

Also, Jupiter came into one of our recent silver picks Rapid Critical Metals which is up 111% since our Initial Entry Price.

(past performance is not an indicator of future performance)

Jupiter have been major holders in IVR for years now and have followed their money into IVR’s capital raises - including the most recent one.

4. We think silver could go on a ‘once in a generation’ run to new highs

Silver is now at 14 year highs, and we think it's about to go on a “once in a generation” run to new all time highs... taking all silver stocks with it.

(no guarantees, past performance is not a reliable indicator of future performance)

5. Very few silver stocks on ASX

There are very few silver stocks on the ASX.

Even less ‘pure play’ silver stocks.

If silver runs, there could be a lot of capital chasing silver exposure in only a handful of names.

This scarcity could mean valuations run from where they are now.

6. Exploration upside (three projects that haven’t been systematically drilled)

IVR just did a deal on the ground next door to its 57M ounce JORC resource estimate.

IVR now has a 15km corridor of exploration targets where it can look to make repeat discoveries (similar to its existing deposit).

Drilling so far has shown district scale potential.

7. IVR’s project being designed to work even in the event of a lower silver price

IVR updated its project's resource in 2023 and started working on its Definitive Feasibility Study (DFS) later that year.

The study started when silver prices were trading in the mid US$20 per ounce.

That means IVR has been designing the project to work in a low silver price environment.

The silver price is now more than double where it was when IVR started its DFS.

8. IVR’s new MD has brought an asset online in South Australia before

Lachlan was previously Managing Director of ASX-listed Hillgrove Resources where he led the design, permitting, financing and restart of the Kanamantoo copper mine...

That project is also in South Australia ~60km south east of Adelaide.

So he knows his way around permitting in South Australia.

We are backing Lachlan to do it all again with IVR’s project, also in South Australia.

Ultimately, we want to see IVR achieve our Big Bet which is as follows:

Our IVR Big Bet:

“IVR takes advantage of the high silver price environment and puts its project into production. At that point, we would expect IVR to be capped at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our IVR Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Here’s some more details on why we Invested in IVR.

We are backing IVR’s new MD who has built projects in South Australia before

IVR recently brought onboard Lachlan Wallace as the company’s new Managing Director.

Lachlan was previously Managing Director of ASX-listed Hillgrove Resources where he led the design, permitting, financing and restart of the Kanamantoo copper mine...

That project is also in South Australia ~60km south east of Adelaide.

Oh and did we mention he was a mining engineer - the exact credentials we would want overseeing a complete reset of a project’s feasibility study.

We especially like the focus he has on “viewing IVR’s project from a financiers lens” which is a big part of the work going into the Definitive Feasibility Study.

Basically, IVR is looking to restructure the way its project gets developed in a way that is most friendly for project financiers... focusing on limiting downside risk.

We are backing Lachlan to do it all again with IVR.

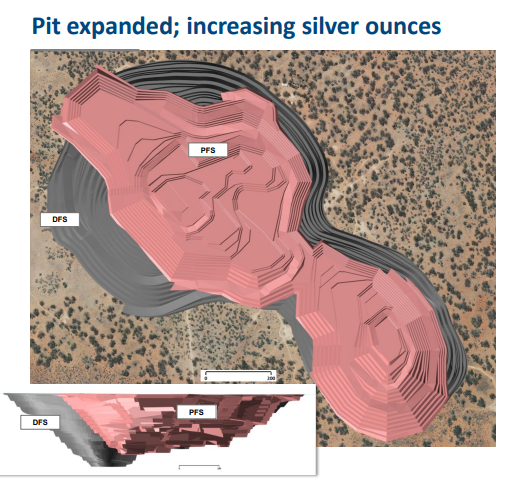

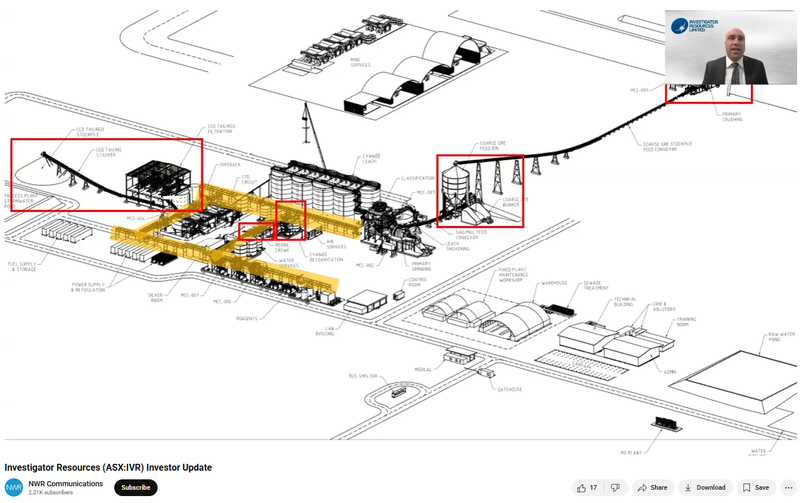

Two main changes are:

1. A restructure of the processing plant - things like changes to the crusher and a change in the processing circuit from dry stacked tailings to wet tailings.

AND

2. A move to expand the pit to bring more silver ounces into the mine plan.

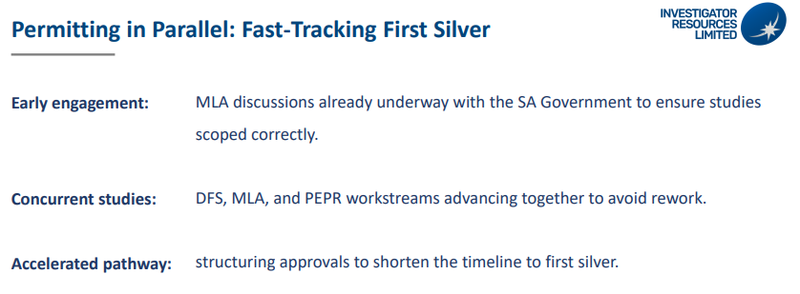

At the same time, IVR has already started the permitting process - mining license discussions are underway as well as other permitting workstreams:

Check out Lachlan talk through his plan to get IVR’s project development ready here:

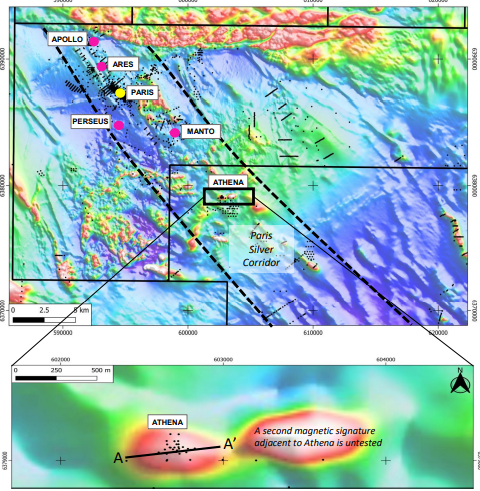

IVR has exploration upside that the market hasn’t noticed... yet

Right now IVR is sitting on one of Australia’s highest grade undeveloped silver projects.

It has a 57M ounce silver JORC resource estimate, and any more high grade silver that it can add to this resource should improve the project economics.

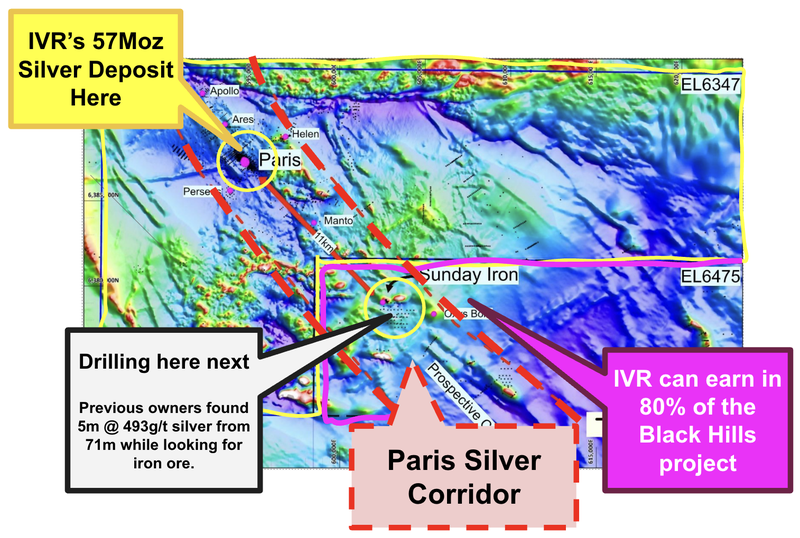

Earlier this year IVR signed an agreement to earn-in up to 80% of the Black Hills project which sits directly adjacent to IVR’s ground (and potentially an extension of the silver mineralisation):

The Black Hills project was drilled in 2013 hitting 5m @ 493g/t silver from 71m (while looking for iron ore).

To the north of the Paris deposit at the Apollo prospect IVR has hits as high as 8m @ 1,262g/t Ag from 149m.

The “Paris Silver Corridor” will present the company with many exploration opportunities as it advances the Paris project through to production.

We know there is high grade silver there...

IVR just needs to find more of it.

IVR plans to drill at one of the prospects in Black Hills, where it has the opportunity to earn-in up to 80% of the project.

IVR will be following up on the 5m @ 493g/t silver from 71m and the several other silver occurrences that remained untested in the region.

(IVR also plans to drill another of its assets 80km away, but we are mostly focussed on the drilling closest to the existing deposit).

We think the upcoming drill programs could bring attention to the IVR story while the permitting process and feasibility studies are progressing in the background.

The reason a discovery could be material for IVR is because any new ore (especially if its high grade) could be plugged into the front end of a development plan and increase the economics of a development scenario.

It could also extend the life of the mine beyond the current 7 years...

Both things are what potential financiers want to see - first because higher grade early in the mine life means a quicker payback on development CAPEX, and second because a longer mine life de-risks the project in the long run.

Can IVR get its project into production during this silver cycle?

That’s what we think can happen, and what we are Invested for

Every time there is a big run in commodity price, it evokes a supply side response.

Silver is often generated as a byproduct of other base metals mining, which means that mine supply generally doesn’t come on quickly for silver.

Higher silver prices for longer mean that producing projects can print serious cash during an up market.

The issue for silver is that there has been an exploration drought for over a decade, with the price under US$20/oz for most of the last 10 years, there was no incentive for anyone to go and find more silver.

For the companies that “stuck it out” in the down market, they are in a MUCH better position to take advantage of the up-cycle as their project is more advanced and closer to production.

(Like IVR)

IVR first made its silver discovery in 2011, during the previous bull run for silver:

(Source)

The company was able to ride the silver momentum over the next few years to drill out the project and get to a maiden resource.

With the support of cornerstone institutional investor Jupiter Asset Management, the company spent the next 10 years (that’s right 10 years) drilling out the project.

Now that the silver market has recovered back to 2011 levels (and hopefully higher), IVR is in an excellent position to get this mine into production.

In 2021 IVR completed its PFS, with an all in sustaining cost on silver of A$17.45/oz...

The silver price is currently trading at ~A$71.25/oz. (~US$47 per ounce)

Everything about this project has been to build a silver mine at cheapest all-in sustaining costs as possible.

IVR even made the decision to delay its DFS by around six months to make even more adjustments to lower the project's CAPEX.

(the IVR share price didn’t like it at the time and has taken a while to recover, which in our opinion provided a good entry point into IVR now that silver has started running)

We are backing the new Managing Director Lachlan Wallace to develop this into production.

While there will likely be a lot of silver exploration plays popping up on the ASX, there aren’t that many silver companies that are “development ready”.

Which is why we Invested in IVR.

We think silver is about to “do a gold” - and silver equities the same

Anyone invested in gold stocks will remember how small cap gold equities were trading despite the big run in the gold price.

Gold went from US$1,200 to US$2,000/oz and hit all time highs (at the time) but the small/mid cap gold stocks did nothing.

For a good 6 months it was pretty rough out there... until all of a sudden it wasnt...

Eventually gold stocks finally started ripping - some of the more advanced ones ripped really hard off very little newsflow.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

What that tells us is that the market sits and waits to see if a move in an underlying commodity price is “real” before really putting capital to work in the smaller end.

We think the same will happen in silver.

Right now, we are going through the initial run up phase where the silver price is spiking.

There are a few green shoots, some buying in the companies who were trading at depressed prices for years.

But we think the big capital inflows and big runs in silver names happens when the market starts to believe the move in the silver price is real and longer lasting.

Here is how we see it look for silver right now relative to that gold image from earlier:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

One precious metals expert we follow, Florian Grummes (CEO of a technical consultancy) thinks the silver price is going to a “minimum of US$100 per ounce”.

(Florian was a keynote speaker at the recent Beaver Creek Precious Metals conference in the US which we attended - check out the full presentation here).

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

IF silver hits US$100 per ounce, then the market will start to extrapolate US$50 or US$60 as the new normal for valuing silver assets.

(Exactly the way the gold investors are now plugging in US$3,000/oz into their valuation models, instead of US$2,000/oz 12 months ago).

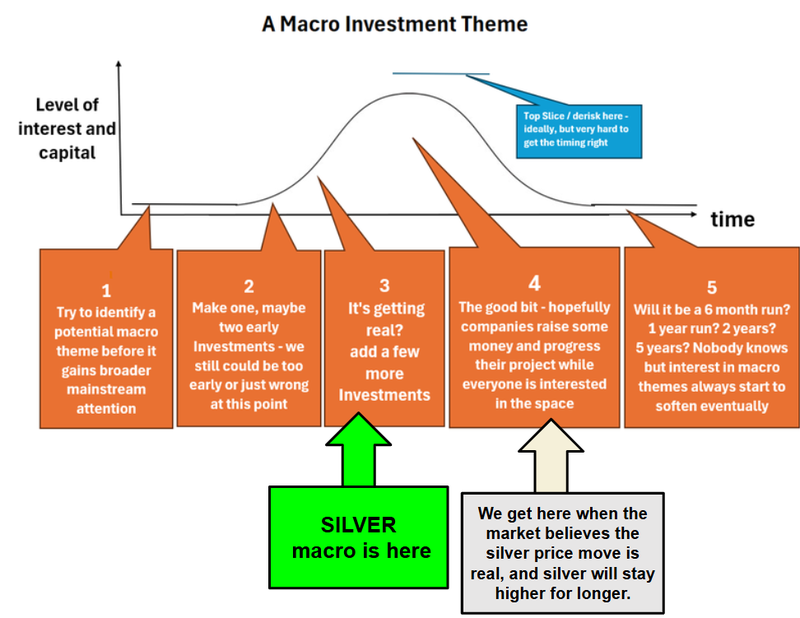

This is why we think “silver” as a macro thematic is now firmly in Stage 3 of our “macro theme interest” model - see below.

That is why we have added a few silver stocks (especially more established silver stocks) in rapid succession to our Portfolio lately.

(we hope we are right and silver goes crazy... but we could be wrong, nobody can predict commodity prices)

IF silver “does a gold” and the market starts to believe the silver price is going higher and will stay higher in the long term, we will enter stage 4 where we think silver names could start re-rating higher:

We have written at length about why we think the silver price could rally, we even published an e-book on it here: What we’ve learned about gold and silver and the incoming mega-bubble

Investment Memo 1: Investigator Resources (ASX:IVR)

Memo Opened: 3 October 2025

Shares Held: 13,714,286

What does IVR do?

Investigator Resources (ASX:IVR) owns 100% of the Paris silver project in South Australia.

The project has a 57M ounce silver JORC resource estimate, is at the Definitive Feasibility Study (DFS) stage and is one of Australia’s highest grade silver deposits.

What is the macro theme behind IVR?

Silver is both an industrial and a precious metal.

Silver also has a prominent industrial use case in the manufacture of photovoltaic cells for solar panels - and as such can be considered important to the energy transition.

Silver is currently trading at 14 year highs at the time of this memo.

Our IVR Big Bet

“IVR takes advantage of the high silver price environment and puts its project into production. At that point, we would expect IVR to be capped at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our IVR Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 8 Reasons We Invested in IVR

- IVR has one of the highest-grade silver projects in Australia

- IVR project is at the advanced DFS stage

- We are investing alongside Jupiter Asset Management

- We think silver could go on a ‘once in a generation’ run to new highs

- Very few silver stocks on ASX

- Exploration upside (three projects that haven’t been systematically drilled)

- IVR’s project being designed to work even in the event of a lower silver

- IVR’s new MD has brought an asset online in South Australia before

What do we want to see IVR do next?

Objective 1: Definitive Feasibility Study on Paris silver project

We want to see IVR complete and release its Definitive Feasibility Study (DFS). We are hoping to see a big improvement on the A$153M Net Present Value (NPV) that was delivered in IVR’s last study in 2021.

Milestones:

🔲 Pit design

🔲 Flowsheet revision

🔲 Throughput optimisation

🔲 DFS completed

Objective 2: Drilling on regional targets

We want to see IVR drill out the 15km corridor of targets that sit around its 57M ounce JORC resource estimate. The ultimate success from these drill programs would be a discovery similar to IVR’s existing resource.

Milestones:

🔲 Geophys/Geochemistry work

🔲 Identify drill targets

🔲 Drilling starts

🔲 Drilling results

Objective 3: Permitting of the Paris silver project

We want to see IVR go through all of the permitting workstreams on its project. We especially want to see the project get a mining license and go through all of the environmental permitting process’.

Milestones:

🔲 Environmental permits

🔲 Project infrastructure permits

🔲 Mining license granted

Objective 4 (Bonus): Drilling on IVR’s other assets

We also want to see IVR drill out its other projects in South Australia.

IVR plans to drill one of those projects later this year.

These sit outside of the key reasons we are Invested, but if IVR makes a meaningful discovery on these it could become material to the company’s valuation.

What are the risks?

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver prices fall, this could hurt the IVR share price.

Permitting Risk

IVR will be seeking a mining permit for its silver project. If this permit is delayed or rejected it may be a drag on the IVR share price.

Development risk

IVR’s project is relatively well advanced which carries its own risks.

IVR will need to raise funding and go through the development process for its project.

IF there are any delays to forecast development timelines, the market could sell down IVR.

Funding risk/dilution risk

As a pre-revenue small cap company, IVR is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, IVR could struggle to access capital on favourable terms.

These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking IVR’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Other risks

Like any stock market investment, investing in IVR carries a range of risks that may affect the company’s value. Some risks are identifiable, while others are unpredictable.

IVR’s main asset is the Paris silver project in South Australia. It is at the Definitive Feasibility Study (DFS) stage but is not yet a producing mine. There is a risk the project never reaches production.

IVR is highly exposed to silver prices. A sustained fall in silver could materially impact project economics and investor sentiment.

The company is pre-revenue and reliant on raising capital to fund development. Any equity raise may dilute existing shareholders, and debt funding may not be available on favourable terms.

Permitting and approvals pose another risk. Mining licenses and environmental permits can take longer than expected or face objections that delay project timelines.

Development risk is also material. Building a mine involves technical, financial, and operational challenges. Cost overruns or delays could hurt the share price.

IVR’s share price has already moved with silver’s recent strength. Current levels may partially reflect anticipated upside, increasing the risk of pullbacks if silver softens or milestones slip.

Finally, market and macro risks apply. A downturn in equity markets or sentiment towards junior explorers could weigh on IVR regardless of company progress.

Investors should carefully consider these risks and seek professional advice before making an investment decision.

What is our Investment Strategy?

Our plan is to hold the majority of our position in IVR for 3 to 5 years, which should be enough time to see IVR get into production... and the silver price to go on the run we hope it will.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates in line with our minimum hold conditions.

We intend to maintain a position in IVR for 3 to 5 years.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.