Our New Investment: American West Metals (ASX: AW1)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 14,722,222 AW1 Shares and 7,361,111 AW1 Options at the time of publishing this article. The Company has been engaged by AW1 to share our commentary on the progress of our Investment in AW1 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Our new Investment is American West Metals (ASX:AW1).

USA critical metals is a rapidly emerging investment theme as the USA rushes to find and develop domestic supply to diversify away from dominant global supplier China.

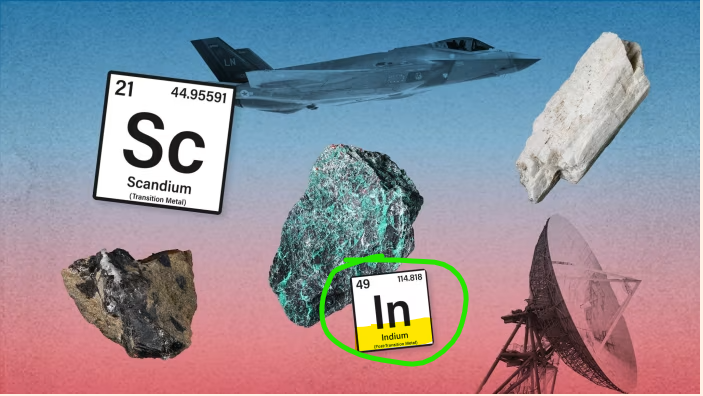

Indium is named by the USA as a critical mineral.

Indium is used in things like infrared detectors, night vision systems, missile guidance systems, Radar systems and F-35 fighter jets...

The USA has zero domestic indium production, relying 100% on imports to meet its demand.

Indium is on the USA critical minerals list. (source)

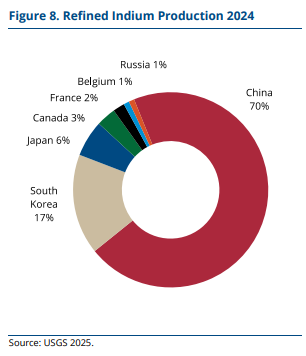

China dominates global indium production and supply (~70%). (source)

China announced indium export controls back in February. (source)

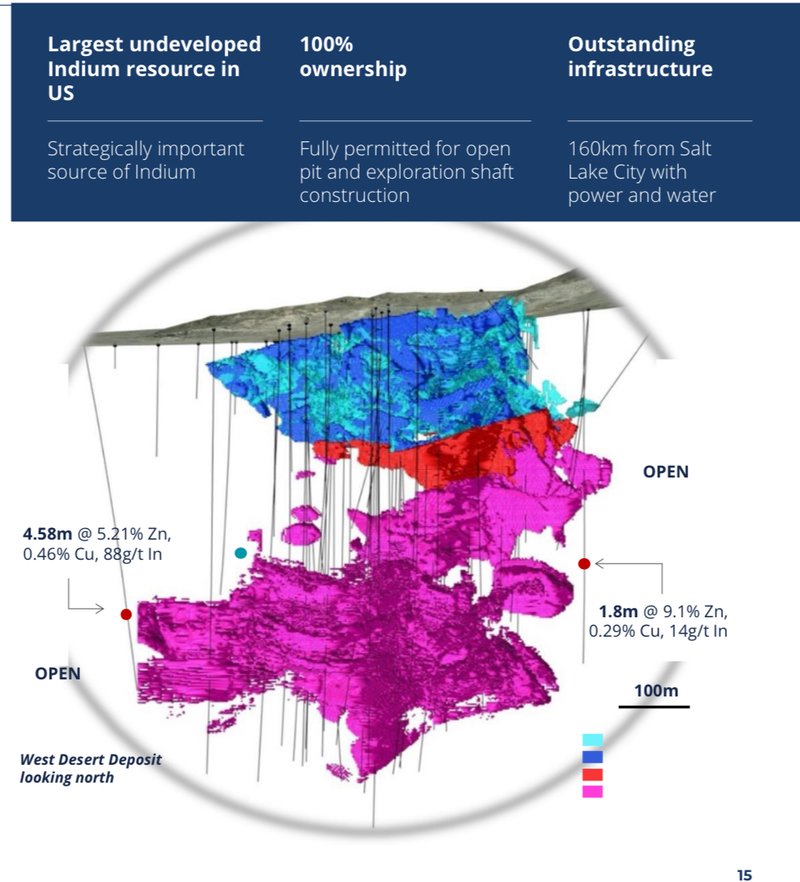

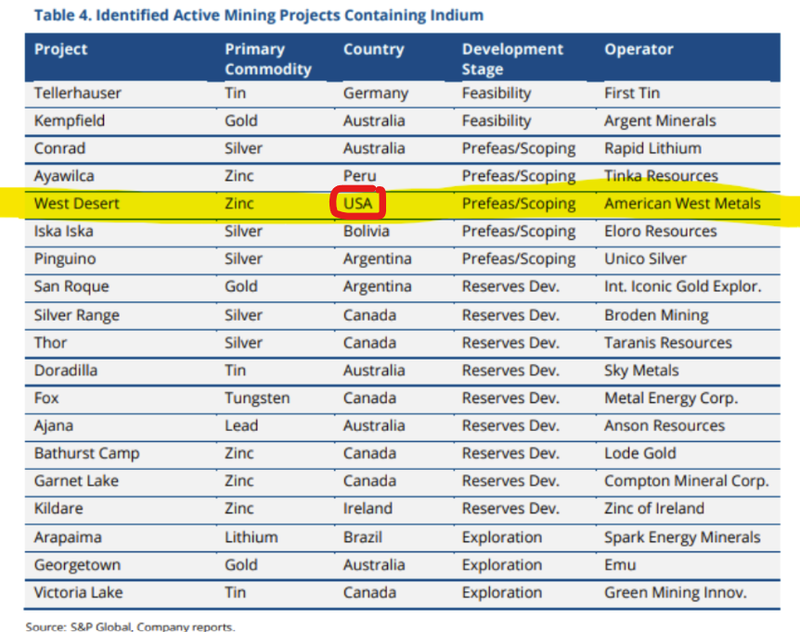

AW1 owns 100% of one of the biggest indium resources in the world...

And it’s in Utah, USA.

Which means It's the single BIGGEST indium resource in the US...

Four days ago, the Pentagon (US Department of War) announced indium as one of the 12 critical minerals they are looking to buy as part of its planned US$1BN critical minerals buying spree.

(Source)

This news is what got us looking for ASX companies in US critical metals OTHER THAN rare earths and antimony.

With big, advanced projects in the USA, that the market hasn’t discovered yet.

Like AW1’s “biggest indium resource in the USA”.

We listed in to a webinar with AW1’s MD Dave O'Neil where he said “We have been approached by the Department Of War, Department of Energy and local government to move this forward” (source)

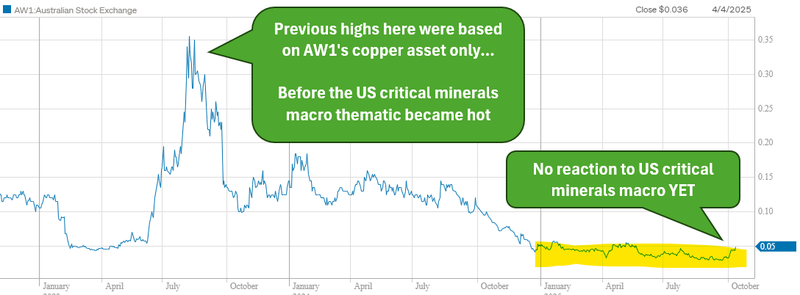

But AW1 seems to have, ahem... “flown under the radar” of the market...

(get it? Indium is a key input into radar systems)

AW1’s share price has barely moved from its recent 52 week lows.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Unlike most other critical minerals stocks on the ASX that have been on a tear.

(especially the rare earths and antimony stocks which are currently getting all the market attention).

After the capital raise today at 4.5c, AW1 will have a market cap of ~$45M, with ~$16M cash in the bank. (source)

That gives AW1 an enterprise value of ~$29M - for the biggest indium resource in the USA.

(the cash figure is based on what AW1 raised today and what was in the bank at 30 June 2025 - we will get an updated figure at the end of this month when the new quarterly is out)

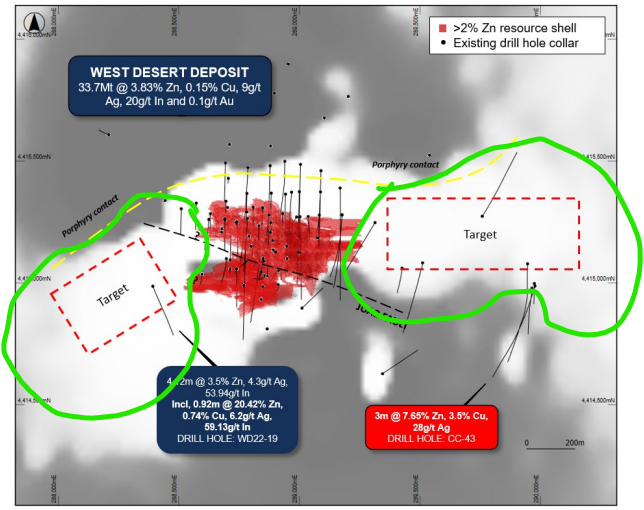

AW1’s indium resource can get even bigger with only 35% of the drilling sampled for indium to date:

(Source)

AW1’s project is actually a "polymetallic deposit”, meaning it contains several valuable metals.

AW1’s resource contains ~1.3Mt of zinc, 49Kt copper, 10Moz silver, 23.8Moz indium and 119Koz gold (indicated and inferred, estimate). (source)

It has zinc, copper, silver (nice!), some gold and...

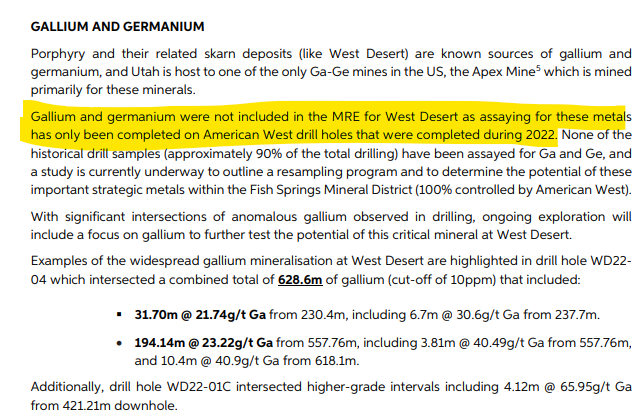

Potentially gallium and germanium too. (source)

Gallium and germanium are used to create high-performance semiconductors essential for AI because of their thermal and electrical properties compared to traditional silicon.

Again, the USA has zero domestic gallium and germanium production.

Again, China controls ~98% of global gallium supply and ~59% of germanium supply. (Source)

And again, China put gallium and germanium export controls back in December last year. (source)

(a big problem for the USA in the global AI race)

AW1 first started seeing gallium/germanium in drill results from its 2022 drilling program.

Only 10% of the drilling done on the project has ever been assayed for gallium or germanium...

(Source)

So we still could see upside on this aspect of the project over the coming months.

There is no guarantee anything comes from the gallium/germanium potential, and we are conscious of there being no JORC resource for either at the moment.

With the current rush of attention and capital from the USA to build and secure domestic sources of critical metals for military and AI dominance...

We have identified that the indium and (potential) germanium & gallium in AW1’s deposit in Utah could be of strategic interest to the USA.

Plus AW1 has a separate, development stage copper asset in Canada that we think underpins its current valuation... (more on this later)

But the indium is what we are here for because it gives AW1 that “biggest in the US” title.

And we have observed the USA’s strategy to invest in the “biggest” deposits of a particular critical metal, in a “creating domestic national champions” style strategy.

US critical minerals macro is heating up again...

We are adding AW1 to our Portfolio just before what we think is a big wave of US capital that starts pouring into the biggest and best US critical minerals projects.

Which looks like it isn't very far away now.

Earlier in the week JP Morgan came out and said it would put US$1.5 trillion to work in industries deemed “critical to US national interest”.

(Source)

We think the JP Morgan news might be the starting gun for a wave of capital flowing into the sector.

(Actually the US government investing in US rare earth miner MP Materials was probably the starting gun, JP Morgan entering the scene is adding to the momentum)

The US government has already been active in the sector taking equity stakes in the US rare earth/lithium national champions AND has explicitly said that Australian critical minerals companies are fair game for direct equity stakes...

So far, the US government has taken direct equity positions in:

- MP Materials (one of the two biggest western producers of rare earths and the only one with a mine in the USA).

- Lithium America’s (which owns the biggest lithium project in the USA)

A clear theme is emerging in the actions of the US government...

It wants to take direct equity stakes in the biggest projects in the chosen critical mineral they are trying to encourage domestic production in...

And we are already seeing evidence of private US investors following the government's cues with on market buying.

Which is why we are Invested in American West Metals (ASX:AW1) - which owns the single biggest indium project inside US borders.

P.S. We are also backing AW1’s non-executive director John Prineas.

We Invested in St George Mining where John is the Managing Director - and St George has been one of our best performers this year... up 560% from our Initial Entry Price.

We also liked that Tribeca investment partners are getting involved here with a $2M position in AW1...

Some of our Investments where Tribeca has come in have performed well this year - LKY which is up 574% from our Initial Entry Price and RCM which is up 91%.

(Note that past performance may not be indicative of future performance and that no guarantee of performance)

9 reasons why we Invested in AW1

- AW1 has the biggest indium (critical mineral) resource in the USA - AW1 owns 100% of the West Desert Deposit in Utah - one of the biggest indium resources in the world and the single BIGGEST indium resource in the US...

- Indium is listed as one of the 12 strategic defence critical minerals in the US - the Pentagon explicitly mentioned indium as one of the minerals it is looking to buy up as part of its stockpiling strategy. The only option to bring into production domestic supply would be AW1’s project.

- China dominates global supply and has placed export restrictions on indium - ~70% of the world’s refined indium comes out of China and earlier in the year indium was one of the five critical minerals that China put export restrictions on.

- The US has no domestic production and is 100% reliant on imports for indium - at the moment there is no domestic production of indium in the US. 100% of US demand is satisfied with imports...

- AW1’s deposit could get bigger, only 35% of deposits’ drill cores assayed for indium so far - AW1’s project is a polymetallic deposit meaning it also has zinc, copper, silver and gold which were the focus of previous drilling. At the moment only 35% of the project’s old drillcore has been tested for indium, so the deposit could get bigger with more assay results.

- AW1’s deposit might also have Gallium/Germanium potential - Gallium and germanium are other critical metals used in semiconductors. AW1 intercepts from its 2022 drill program found gallium and germanium. At the moment, only 10% of the drilling data on the project has been assayed for gallium or germanium.

- Capital is flowing into US critical metals macro thematic - The US government through its different agencies is allocating billions of dollars to the critical minerals sector. More recently JP Morgan also announced it would put to work US$1.5 trillion in industries that are “critical to the U.S national interest”.

- AW1 can follow the “US market listing playbook” - there is a playbook for ASX stocks to attract more attention and capital to projects that are based in the US. AW1 isn’t yet listed in the US and we think that if its project gets any traction it could go for a US listing that opens up the project to North American investors.

- We are backing John Prineas here - we Invested in John’s other company St George Mining (ASX: SGQ) and it has been one of our best performers this year, up 560% from our Initial Entry Price. John has managed to capture US critical minerals macro momentum with SGQ’s rare earths asset. We are hoping AW1 is able to repeat SGQ’s success.

- AW1 hasn’t yet run like most other US critical Minerals stocks - most juniors who pick up exploration ground in the US are trading at market caps in the $20-30M range. We think that AW1 should trade at a premium to these companies given its indium asset is at a relatively advanced stage and the biggest in the USA.

- We think AW1’s copper asset more than underpins it’s current valuation - The company’s copper asset in Canada has had a Preliminary Economic Assessment done on it showing an after tax Net Present Value (NPV) for the project of US$149M. AW1 already has binding commitments for offtake and development financing for this project too.

Our AW1 Big Bet:

“AW1 receives capital from either the US government, a strategic partner or the capital markets to progress its Indium project in the USA, re-rating AW1 to a valuation that is multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our AW1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Later in today’s note we will share our updated AW1 Investment Memo which will cover:

- What AW1 does

- The macro theme for AW1

- Our AW1 Big Bet

- What we want to see AW1 achieve

- Why we are Invested in AW1

- The key risks to our Investment Thesis,

- Our Investment Plan

But before that, here is a summary of the 10 reasons why we Invested in AW1.

AW1 owns 100% of the West Desert Deposit in Utah.

The project is one of the biggest indium resources in the world.

AND the single BIGGEST indium resource in the US...

(Source)

The project is fully permitted for an open-pit mine...

(Source)

And the project's indium resource is based on assays from only ~35% of the existing drill cores on the project.

Only ~10% of the prospective project area has been drilled to date... so it could be a lot bigger than the current resource suggest too:

(Source)

AW1’s project has a 23.8M ounce indium resource.

Which is more than 675 tonnes of indium metal, and ~3x the supply that the Pentagon is looking to secure JUST for its strategic stockpile buying spree.

The project also has ~118k ounces of gold, ~9.8M ounces of silver and is finding gallium (and Germanium) in its assay results.

Gallium and germanium are also critical metals we have no exposure to at the moment, so we are interested in seeing what happens there.

AW1 picked up gallium and germanium in drilling during 2022.

At the moment, only 10% of the drilling data on the project has been assayed for gallium or germanium.

At a very high level, we are in AW1 because we think there is a non-zero chance that the company’s project attracts some sort of strategic funding package that gets its project developed.

Especially given the lack of US domestic indium supply...

So what is indium and why does the Pentagon want it?

Indium is listed as a critical mineral in the USA’s critical minerals list from 2022. (Source)

At the moment China controls ~70% of all global production...

(Source)

China actually explicitly included indium in the list of ~5 critical minerals that it would restrict exports on back in February.

(Source)

The US has no domestic indium production and is 100% dependent on imports...

Indium’s primary use case is in things like touchscreens and TV’s but indium is becoming more and more important in next-generation semiconductors used in data center infrastructure.

The reason the Pentagon would be interested (and why it caught our attention) is because indium is also critical for the US military...

Indium is used in things like Infrared detectors, night vision systems, Missile guidance systems, Radar systems and F-35 fighter jets...

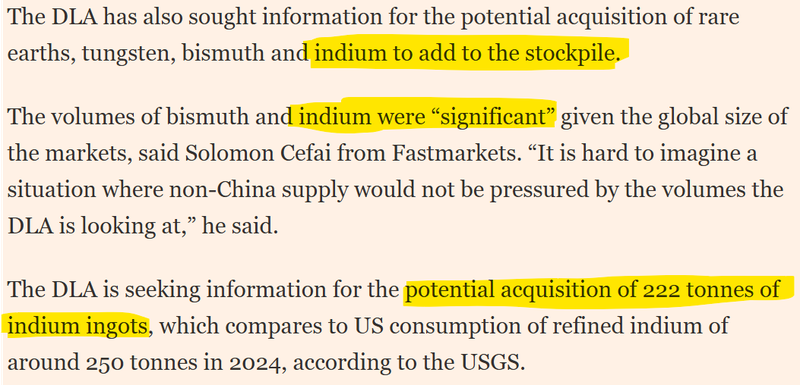

The Pentagon actually explicitly mentioned indium among 12 strategic defense critical minerals essential for national security AND said it would look to acquire indium as part of its US$1BN critical minerals buying spree.

Here is a quote from the Pentagon saying it is “seeking to acquire 222 tonnes of indium ingots”.

(Source)

Just look at that image used in the Financial Times article above:

(Source)

The way we see our Investment in AW1 is that IF China (or any other supplier) puts further restrictions on indium exports then we could see urgency increase even more to bring online US domestic supply...

And IF the US stays true to their form of backing the big projects in the country then AW1 could see some love from a government agency...

Imagine the Pentagon taking a direct equity stake in AW1...

We also like AW1’s advanced copper asset

We think the company’s 80% owned Copper project underpins the company’s current valuation.

Which effectively allows us to get a free kick on the indium asset.

If the indium asset isn’t able to capture the capital flowing into US critical metals, we are pretty comfortable owning AW1 for its copper.

AW1’s copper project has 20.6Mt at 1.1% copper and 3.3g/t silver JORC resource.

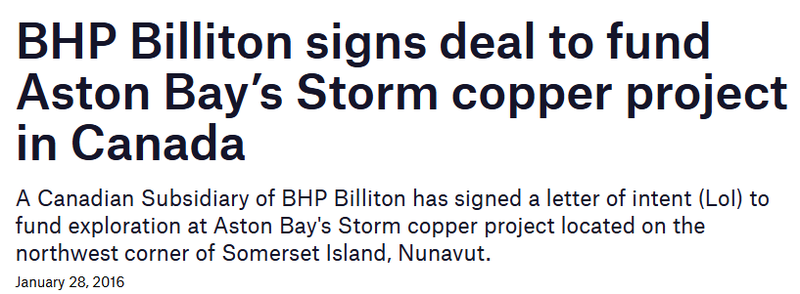

Back in 2016 the same assets under different ownership had BHP come in via an earn-in deal that would have seen BHP spend US$50M on the asset.

(Source)

The deal fell through in 2018.

Then in 2021 AW1 signed an earn-in deal to acquire 80% of the asset by spending a minimum of CAD$10 million on exploration expenditure

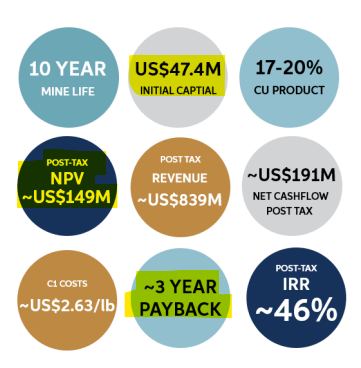

AW1 completed a Preliminary Economic Assessment (PEA) on the project earlier this year which showed the project had a post-tax Net Present Value (NPV) of US$149M based on CAPEX of just US$47.4M. (source)

That study was done using a copper price of US$4.60/lb and US$25 per ounce for silver.

The copper price is now closer to US$5/lb and silver is at US$50/lb....

(Source)

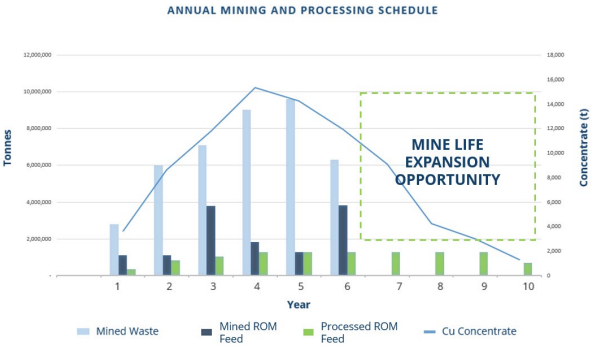

Project based on ~6 year mine life and 10 years of processing.

So exploration upside here matters too to fill in the mining gaps in years 7 and beyond:

(Source)

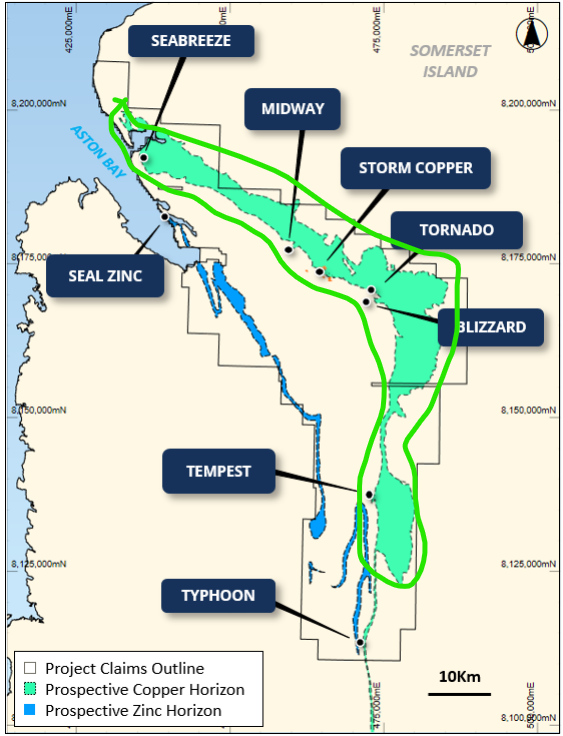

AW1’s project is largely undrilled at the moment and drilling is ongoing right now with across the multiple regional targets on the project:

(Source)

AW1 currently has a Pre Feasibility Study (PFS) and permitting in the works on the existing Storm project right now.

So we should get an updated look at project economics fairly soon.

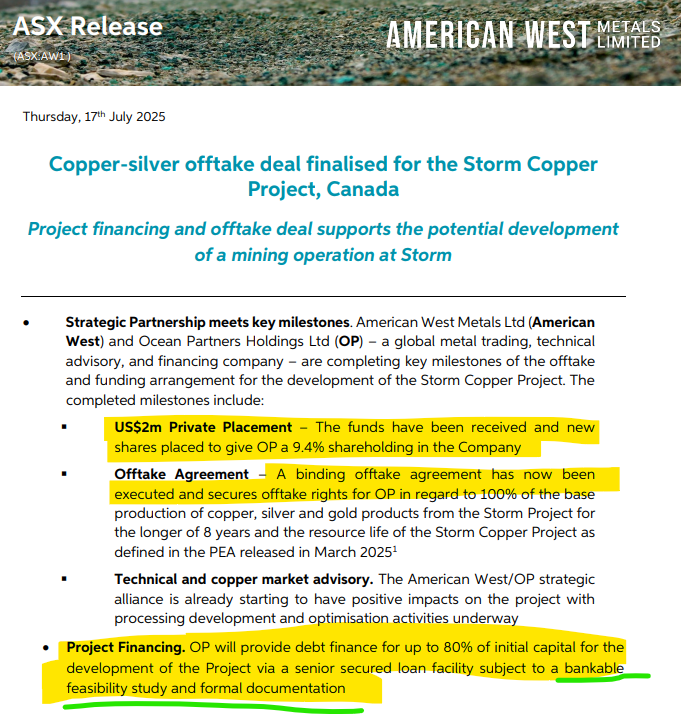

Another reason we like the copper project is because it has attracted two project financing deals.

AW1 did a deal with Ocean Partners for the project via a 9.4% equity stake in the company and a binding offtake agreement which could see ~80% of the project financed...

(Source)

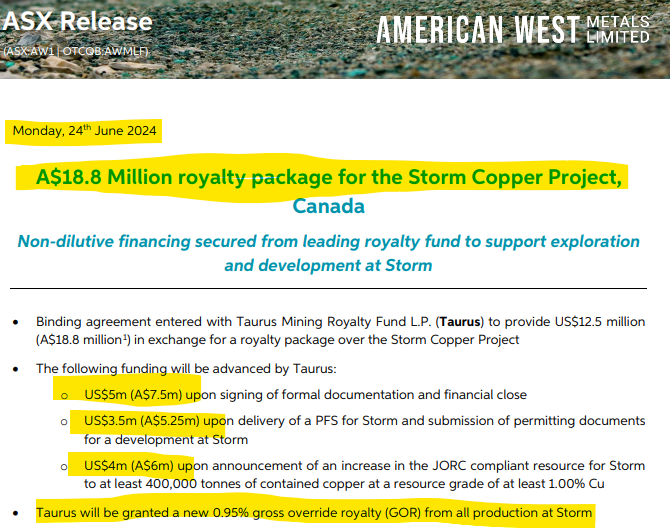

Back in June 2024, AW1 also did a royalty deal for A$18.8M in non-dilutive financing for the project.

(Source)

Despite how advanced the project is it still trades at a discount to its peers - even one peer that is in the exploration stage in the same region as AW1 - without even factoring in the US indium asset:

(Source)

Investment Memo 1: American West Metals (ASX:AW1)

Memo Opened: 16-10-2025

Shares Held: 14,722,222

Options Held: 7,361,111

What does AW1 do?

American West Metals (ASX:AW1) owns a portfolio of critical minerals projects including:

- Indium in Utah, USA - AW1 owns 100% of the biggest indium deposit in the USA.

- Copper in Canada - AW1 owns 80% of an advanced copper project in northern Canada.

What is the macro theme behind AW1?

Critical minerals and US-based projects are attracting attention and capital.

Trump is now looking to adopt pandemic-era level urgency to boost critical minerals production in the US.

With Trump signing Executive Orders to encourage US domestic critical metals production, fast track permitting and providing funding for mining projects private interest and capital has followed into the sector.

AW1 has exposure to:

- Indium - a US listed critical mineral essential for semiconductors, touchscreens, and advanced defence technologies.

- Gallium/germanium - both are also on the US critical minerals list and are essential for semiconductors and the military industrial supply chain.

- Copper - a cornerstone metal for electrification, renewable energy infrastructure, and the EV supply chain.

Our AW1 Big Bet

“AW1 receives capital from either the US government, a strategic partner or the capital markets to progress its Indium project in the USA, re-rating AW1 to a valuation that is multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our AW1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 9 Reasons We Invested in AW1

What do we want to see AW1 do next?

Objective 1: Drilling at the US indium project

We want to see AW1 drill its indium project to really test the projects exploration upside (including other metals like gallium). Ultimately, we think some exploration will revive market interest in the project.

Milestones:

🔲 Drilling starts

🔲 Drilling results

🔲 Assay results for gallium/germanium

Objective 2: US government or strategic funding for the US indium asset

We want to see AW1 lock in either government or strategic funding for its US indium asset.

Milestones:

🔲 US government fast-tracking permitting

🔲 Non-dilutive US critical minerals funding opportunity applications

🔲 Strategic funding partnership

Objective 3: Pre-feasibility study and permitting for the Canadian copper project

We want to see AW1 deliver a pre-feasibility study and key permits related to developing the project.

Milestones:

🔲 Pre Feasibility Study

🔲 Environmental Studies

🔲 Mining/development permits

Objective 4: Exploration drilling at the Canadian copper project

We want to see AW1 drill out its regional targets and hopefully add to the projects existing JORC resource.

Milestones:

🔲 Geophysics/Geochemistry work

🔄 Drilling starts

🔄 Drilling results

🔲 JORC resource upgrade

What are the risks?

Niche commodity price risk

We completely acknowledge that this AW1 has exposure to a very niche commodity (indium) were the market isn’t as big as more mature commodities like gold or oil. This means prices for the commodity can go up or down a lot. If the price was to fall then it would negatively impact AW1’s share price

Development/processing risk

AW1’s indium resource sits inside a polymetalic deposit. These deposits can sometimes be difficult to process and recover valuable minerals from. There is no guarantee that AW1 will be able to recover any of the critical minerals in the deposit economically. We will need to see the company complete metallurgical testing before this risk is addressed.

Permitting Risk

AW1 will need to get permitting in order for its Canadian copper project. If this permit is delayed or rejected it may be a drag on the AW1 share price.

Funding risk/dilution risk

As a pre-revenue small cap company, AW1 is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, AW1 could struggle to access capital on favourable terms.

These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking AW1’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Critical Minerals Macro risk

A big part of our Investment is related to critical minerals macro sentiment strengthening and resulting in a funding deal for AW1’s US indium project. IF macro sentiment was to turn, then the chances of that asset being funded/brought online would reduce significantly. This could mean a re-rate lower in AW1’s share price.

Other risks

Like any small cap exploration company, investing in AW1 involves a range of risks, some known, some unknown (this is the nature of investing in early-stage companies).

Here we aim to identify a few more risks.

AW1’s indium project, while large and strategically located in the US, is still at the pre-development stage. There is a risk the project does not progress to production or that feasibility studies show weaker-than-expected economics.

The indium market itself is small, opaque, and subject to significant price swings. Limited transparency around pricing and supply chains could impact project valuation and investor sentiment.

Although AW1’s US project is fully permitted for an open-pit mine, the company will still need to secure ancillary approvals for development and production. Any delays or regulatory changes could push timelines back.

There is also the risk that AW1 is unable to attract US government or strategic funding despite being well-positioned in the critical minerals thematic.

On the copper side, AW1’s Canadian project may face operational or permitting challenges due to its remote location and environmental regulations.

AW1 remains reliant on capital markets to fund project development. Future equity raisings could dilute existing shareholders, while debt funding may not be available on favourable terms.

Finally, broader macro conditions, such as a downturn in commodity prices or waning investor appetite for critical minerals could impact AW1’s ability to raise funds or achieve its development goals.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our Investment Strategy?

We are Invested in AW1 to see it progress its project into development.

Our plan is to hold the majority of our position in AW1 for 3 to 5 years which we hope is enough time to see AW1 to move towards development (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may also look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.