Our Latest Investment: Patriot Resources (ASX: PAT)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 18,680,000 PAT Shares at the time of publishing this article. The Company has been engaged by PAT to share our commentary on the progress of our Investment in PAT over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our latest Investment is Patriot Resources (ASX:PAT).

Long time readers know we are mega silver bulls.

We think silver is going higher.

And ASX silver stocks will go with it.

Yesterday we shared some data about ASX silver stock prices running during silver price runs:

Before what we expect (hope) will be the next leg up in the silver price and ASX silver stocks, we are adding PAT to our Portfolio.

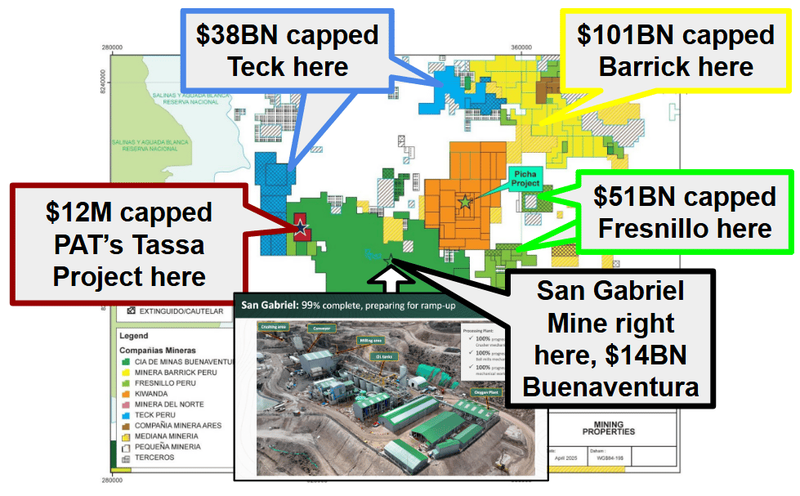

PAT is capped at ~$12M at its last traded price.

PAT’s project has a 31.4M ounce silver equivalent JORC resource estimate based on just 26 drillholes to date - in Peru.

Peru holds approximately 22% of the world's known silver reserves (the largest of any country) (source) and accounts for roughly 11–12% of annual global silver production (the third-largest producer behind Mexico and China).

We think PAT’s 31.4Moz resource could be multiplied with some drilling.

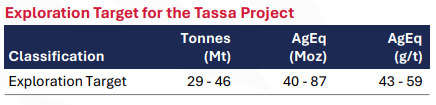

(Beyond the upper end of PAT’s current 40M to 87M ounce silver equivalent exploration target)

Drilling is to come in the next few months.

We like the silver theme, we like the asset AND we are backing the PAT team here.

We have been looking at this project for over 6 months, and the final bit of due diligence we completed 3 weeks ago was a trip to Peru to spend some time with PAT’s Chairman, the new CEO/MD, and the Chief Geologist.

PAT is led by Chairman (and major shareholder) Hugh Warner - Hugh owns ~6.22% of PAT (source).

Hugh knows how to take a tiny micro cap and turn it into a multi hundred million dollar exit for shareholders.

(by that we mean he’s done it recently)

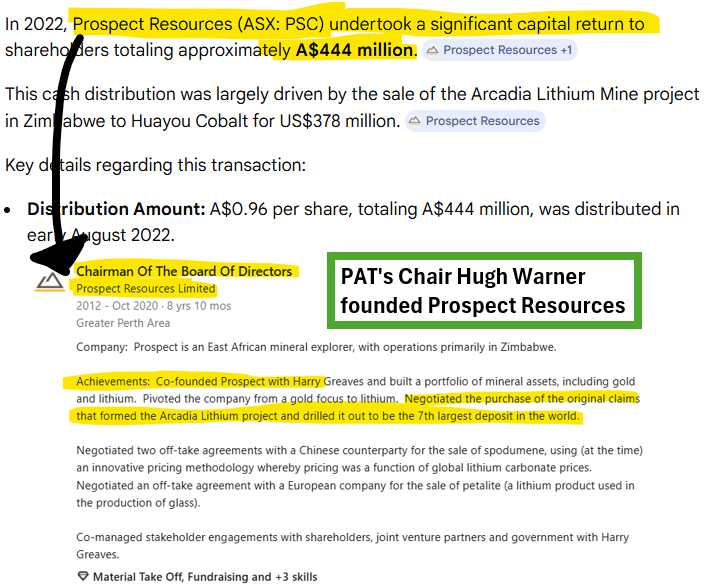

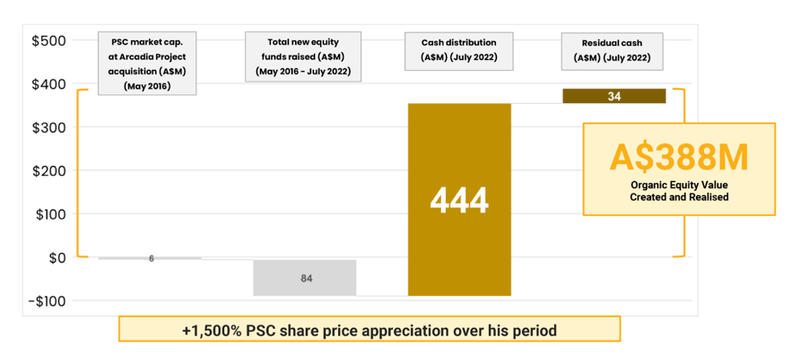

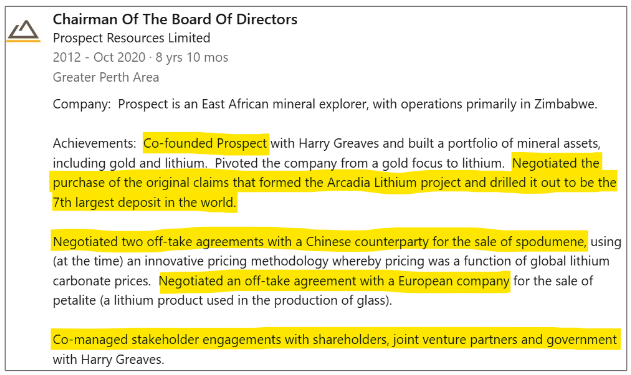

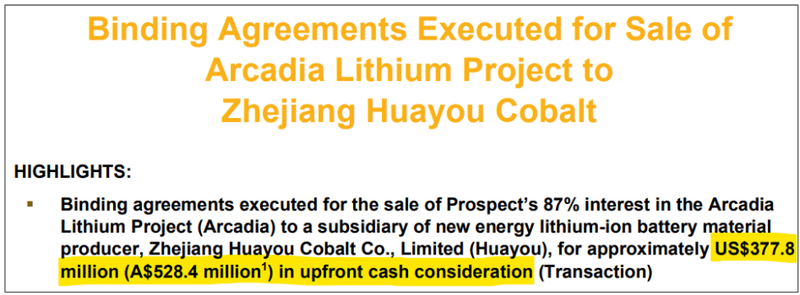

Hugh was co-founder of Prospect Resources which went from a $6M micro cap explorer to acquiring an asset, making a Tier 1 discovery, growing it, and ultimately selling 87% of it for US$378M. (source)

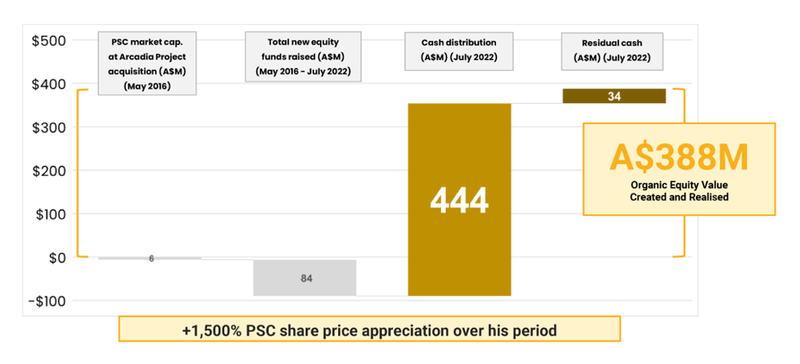

Which allowed Prospect to pay out A$444M in cash to shareholders.

So Prospect went from a tiny $6M market cap to paying out A$444M in cash to shareholders in ~6 years.

(source)

We actually held a small parcel of Prospect shares way back in 2016 but sadly sold them way too early - evidence again that long term Investments can deliver the greatest returns.

We don't intend to make the same mistake with our new Investment in PAT.

Of course a lot of luck in the exploration game is required along the way - a genuine discovery needs to be made, the macro thematic gods must be smiling in your favour, and a lot needs to go right.

One way to try and “do it all again” is to bring back the same team that “did it all before”.

Hugh has also brought the Prospect team into PAT.

Leading the technical side at PAT is Chief Geologist Eugene Gotora, who was directly involved in the aggressive exploration phase at Prospect.

Chris Hilbrands is Director and General Manager at PAT - at Prospect he was also a core part of the team as CFO... so he also has some experience in making giant bank transfers to shareholders?

Caution: Micro cap explorers aren't known for returning cash to shareholders - quite the opposite actually nearly 100% of the time. Well done Hugh and ex-Prospect team. We hope you can deliver something similar for PAT holders like us, but we recognise this is a rare event.

That asset Prospect discovered and developed is still operating and is currently Africa’s biggest operating lithium mine.

At last traded price, PAT has a ~$12M market cap and IF we are right about where the silver price is going we think it's got a capital structure that is leveraged to exploration success in the field.

PAT has no debt and only ~290M shares on issue.

PAT should also have ~$4.9M cash (after the $500k cash we just committed to put in at 5c plus $2.2M cash at 31 Dec + the $2.25M T2 placement settled in January).

So, PAT’s enterprise value is somewhere around ~$7M to $8M.

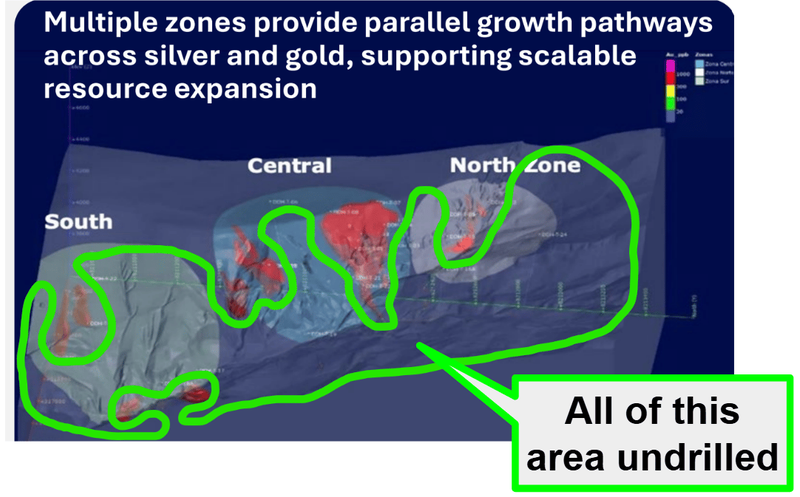

PAT is just getting started on this Peru silver asset - so how big can that 31.4Moz silver equivalent resource get with some drilling?

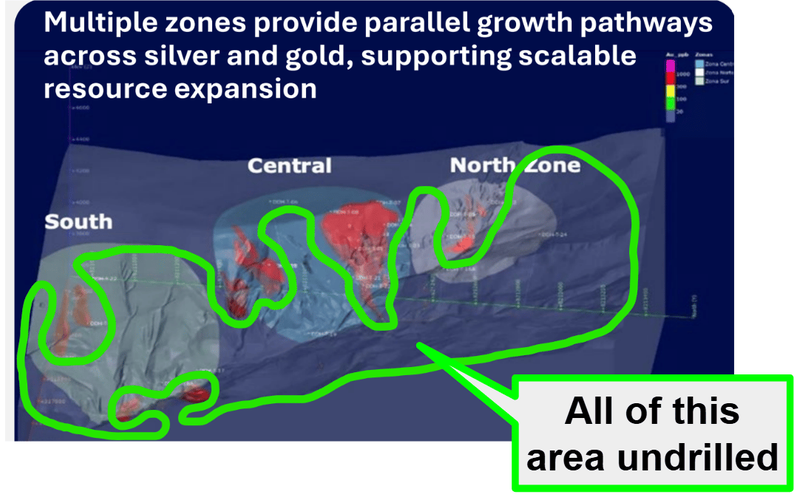

So far the asset has only had 26 holes completed across a ~2.8km corridor.

And from just those 26 holes, there is already a JORC resource estimate and a big exploration target.

The rest of the project is completely undrilled:

(source)

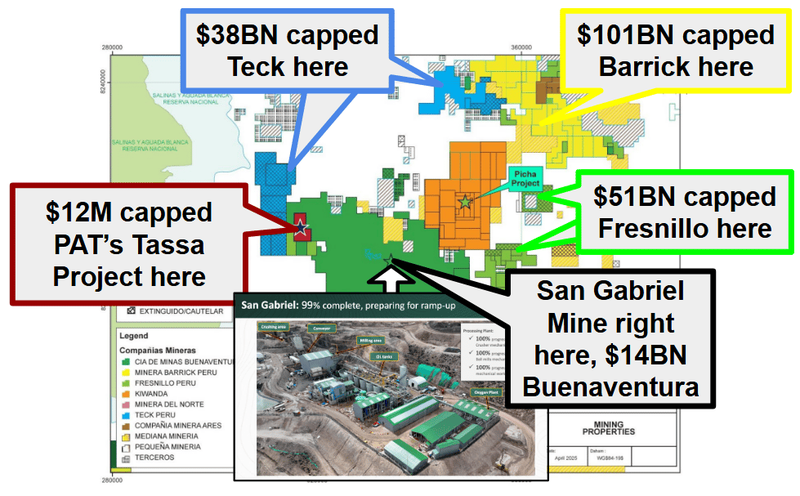

$38BN mining major Teck previously worked on this asset (between 2020 and 2024) and completed a 3D geological model of the project.

(sounds expensive...)

PAT now has Teck’s data and says it has “defined a larger mineralised envelope beyond the current resource”... (source)

After doing years of work on this silver asset, Teck’s leadership changed the company's focus to its major copper and zinc projects.

So Teck didn't even get to drill a single hole after all those years of pre-drill preparation work.

This is what we get to see PAT do soon.

But if the asset was good enough for mining major Teck to work on for a few years - we think it could be a company maker (with exploration success) for a fast moving, singularly focused, $12M capped PAT.

$38BN Teck wouldn't waste their time (years) on something they didn't think had Tier 1 potential.

We think that with some drilling and playing around with that 3D geological model that Teck spent years building - PAT could multiply its existing silver resource.

(not to mention the gold/copper upside on the project - more on this in a second).

Remember there's only ever been 26 holes put into the project...

We think PAT’s got hold of the asset at the right time too.

The silver price is up first and foremost - so there is capital willing to back exploration projects now.

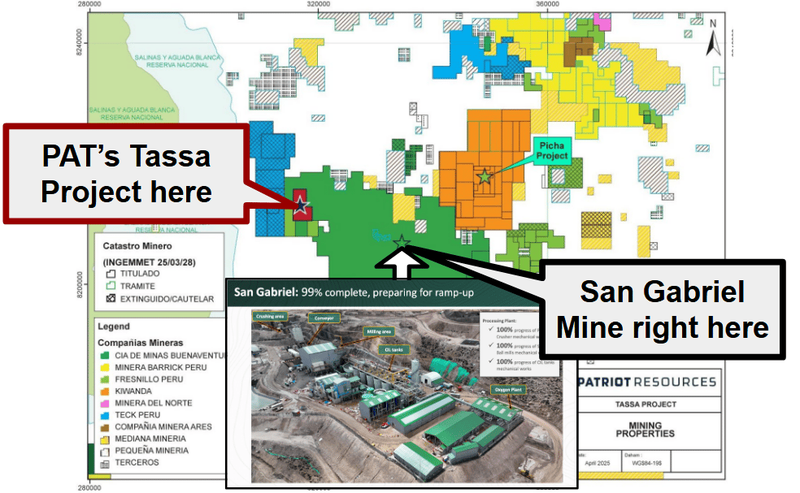

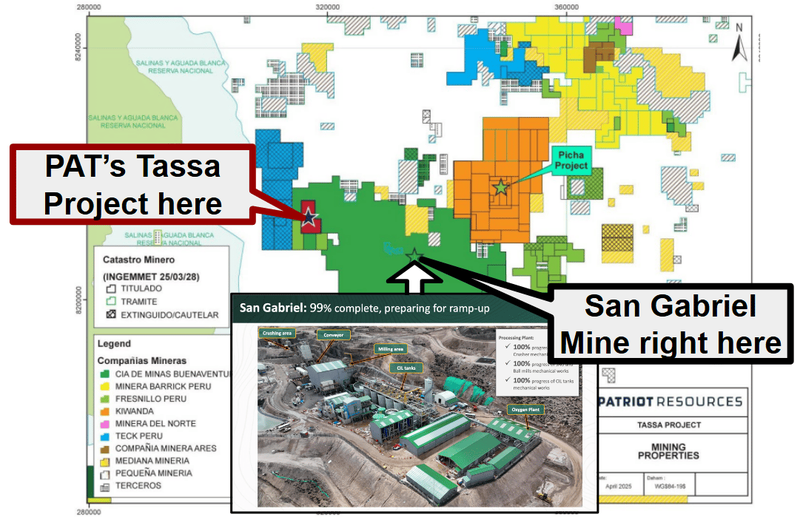

And second, the San Gabriel gold mine owned by $14BN Buenaventura poured its first gold bar just before Christmas - 18km away from PAT’s project.

(Source)

(~18km away is extremely close by gold mining / trucking standards).

(Source)

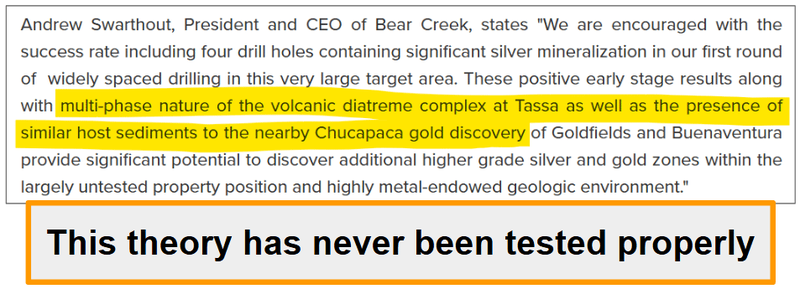

PAT’s project is also ~16km away from the ~6M ounce gold, ~46M ounce silver Chucapaca deposit owned by Goldfields/Buenaventura.

And similarly to that mega deposit - PAT’s project has deeper gold targets (that have only ever had three holes put into them).

All three of those old holes hit gold (albeit at low grades) - 81.9m at 0.41 g/t gold and ~234m at 0.25g/t gold.

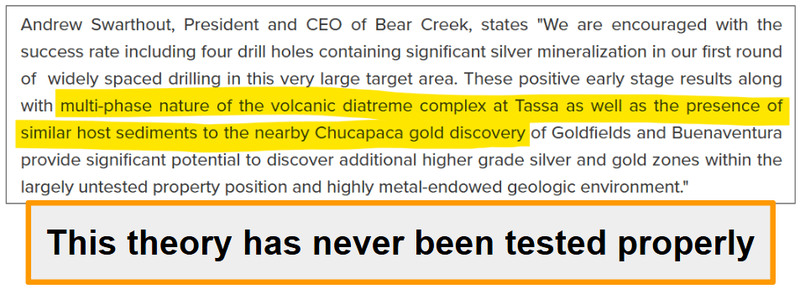

The CEO of the previous company that owned PAT’s project said this in 2010:

"multi-phase nature of the volcanic diatreme complex at Tassa as well as the presence of similar host sediments to the nearby Chucapaca gold discovery”.

(source)

It will be interesting to see what PAT can find with some deeper drilling...

PAT will now be the first owner who can piggyback off any corporate/market interest that comes into the area (from those watching the gold mine next door).

We think Peru as a jurisdiction more broadly is also a good place to be for any mining company - let alone a silver explorer.

Peru is the third largest producer of silver globally AND the likes of $101BN Barrick, $51BN Fresnillo and as mentioned earlier, $38BN Teck Resources are operating in this part of the country.

(source)

Ultimately, we think PAT got hold of an asset that has been largely ignored by explorers (probably because of a low silver price) for over a decade.

And now, PAT has it with silver trading above US$75 per ounce and a mine having just come online nearby...

Now we wait to see what PAT can find with some drilling.

A quick side note - PAT’s also got a lithium asset in Canada and a copper asset in Zambia.

Both are fairly early stage BUT that lithium asset - with lithium prices running - could be of interest right now.

(If anyone knows a good lithium asset it has to be Hugh and his team - as mentioned earlier, they acquired and developed the current largest operating lithium mine in Africa).

The copper asset in Zambia has all the hallmarks of a potential discovery too.

So we think one of those two assets could also be sold or farmed out for non-dilutive funding to progress PAT’s Peru silver asset.

(or maybe a lucky drill hole or two and it becomes the main game... who knows in the game of micro cap exploration)

Anyway - we are mainly here for the silver in Peru.

And our thesis that if the silver price runs, so will ASX silver stocks.

ESPECIALLY those that deliver some exploration success into a silver run.

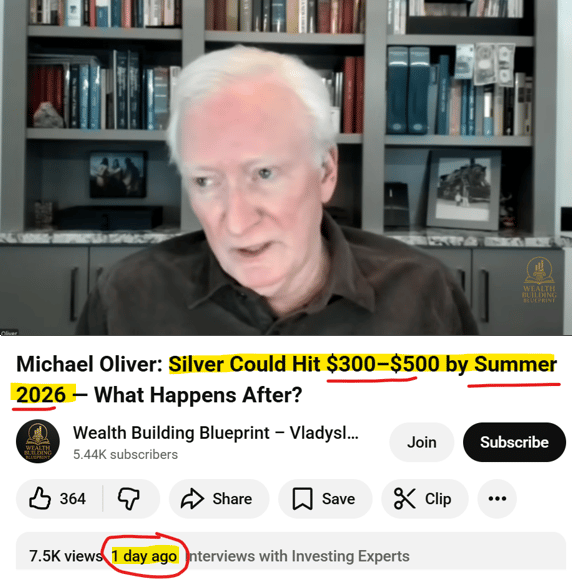

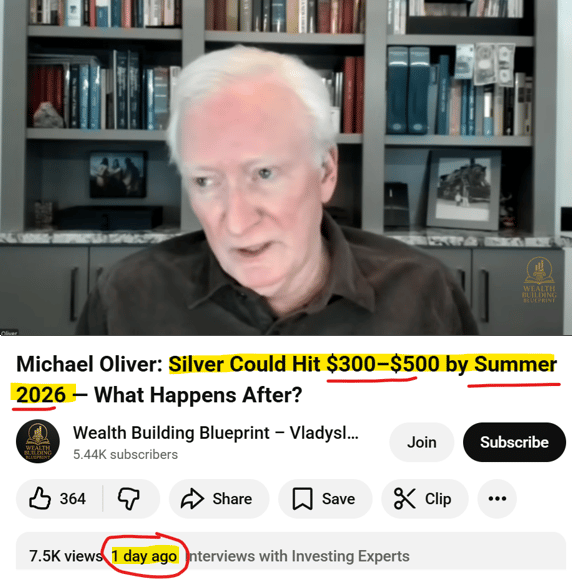

And just in time - our favourite momentum and technical analyst, Michael Oliver, just dropped a new video yesterday.

In it, he is calling a US$300 to US$500 silver price “by summer 2026”.

(we assume he means North American summer which is in a couple of months from now)

(while he has a got a lot of things right on silver over the last 18 months, remember analysts often get things wrong)

So we have added PAT to our Portfolio today, now we wait for the next silver price run and PAT’s first set of drill results.

Hopefully both happen at the same time.

Later in today’s note we will share our updated PAT Investment Memo which will cover:

- What PAT does

- The macro theme for PAT

- Our PAT Big Bet

- What we want to see PAT achieve

- Why we are Invested in PAT

- The key risks to our Investment Thesis,

- Our Investment Plan

But first, here are the 10 reasons we Invested in PAT, which will provide a bit more detail on what we covered in the introduction.

The 10 Reasons We Invested in PAT

1. We think silver is getting ready to run to new all time highs

Silver was the best performing commodity of 2025.

From its March 2025 lows of US$29/oz, it went to a peak of US$121/oz just ten months later in January 2026:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

But like most price run ups, silver needs to consolidate at a new higher level for a while - which it has been doing for the last two months.

And after some consolidation... we think it’s going higher than its January all time highs (we could be wrong though, of course).

2. PAT has an existing 31.4M ounce silver equivalent resource that we think can grow

PAT’s project has a JORC 31.4M ounce silver equivalent resource.

PAT’s resource is open in all directions across a ~2.8km structural corridor.

The project also has a 40-87M ounce silver equivalent exploration target. With some drilling we think PAT can get closer to that upper end (and potentially extend way beyond that number).

(Source)

Only 26 drill holes have been completed across a 2.8km structural corridor and there are IP geophysical anomalies down to ~100-400m depth that remain largely undrilled.

(and some targets to the north down to ~500m depths - completely untested)

(source)

3. We are backing the team from Prospect Resources here

PAT’s got the same team behind it as Prospect Resources.

PAT’s chairman, Hugh Warner, was one of the co-founders of Prospect Resources, where he oversaw the Arcadia lithium project in Zimbabwe, picking up the asset, making the discovery, then growing that into what is now the largest operating lithium mine in Africa.

(Hugh holds ~6.3% of PAT shares at last count and is one of PAT’s single biggest shareholders).

Prospect Resources ended up selling that lithium asset for US$378M in 2022 and returned ~A$444M to shareholders off the back of the sale - an incredible outcome for what started as a $6M capped explorer in 2016.

We Invested in PAT now in the early stages of its exploration as we are backing Hugh to repeat the same formula as he executed at Prospect Resources.

He has brought some of the Prospect team along with him into PAT too.

(source)

4. ~$12M market cap and a tight capital structure.

PAT trades at an enterprise value of ~$7M ($12M market cap, ~$4.9M cash and no debt).

(That cash balance is based on our $500K we just committed to at 5c, plus $2.2M cash at 31 Dec + the $2.25M T2 placement, settled in January)

PAT also has a fairly tight capital structure with only ~290M shares on issue and high ownership amongst the management team.

5. The current resource underpins PAT’s valuation

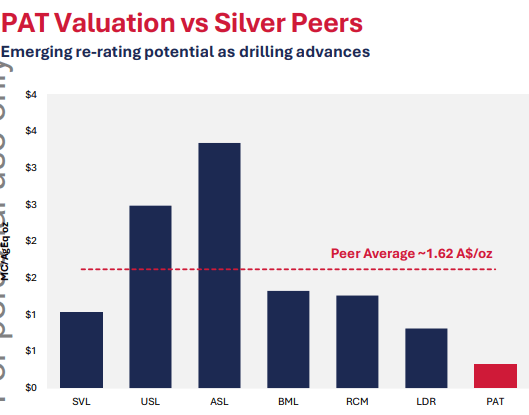

PAT trades at an enterprise value of ~$7M.

With a 31.4M ounce silver equivalent resource, PAT’s effectively trading at an EV/silver equivalent ounce of resource at $0.22 per ounce.

For context - Andean Silver (ASX: ASL), a more advanced development stage silver-gold play in Chile, trades at ~A$2.20/oz (based on yesterday’s close price).

Here is how PAT ranks against other peers:

(source - PAT presentation from March 2026)

6. PAT’s silver asset was previously owned by $38BN Teck Resources

Teck - one of the world's largest diversified miners - had the asset for 4 years, validated the geology and secured drill permits.

Then, before a single hole was drilled Teck walked away in 2024 as the company repositioned as a pure-play copper company.

We think that if the project was interesting enough for one of the world’s biggest miners - Teck - to spend time and cash on the asset then we think it could be a potential company maker for a small cap like PAT.

7. PAT’s project is next door to the 1.8M ounce San Gabriel gold mine, owned by $14BN capped Buenaventura

PAT’s direct neighbour, Compañía de Minas Buenaventura (NYSE: BVM), has 1.8 million ounces of Proven and Probable gold reserves at 3.71 g.t gold and 3.1 million ounces of silver.

The San Gabriel gold mine poured its first gold bar on December 23rd, 2025.

PAT’s project gets to benefit from all the infrastructure developed by Buenaventura (and the interest that would have come into this part of Peru).

(Source)

8. Peru is a fertile hunting ground for silver

Peru is the third largest producer of silver in the world accounting for ~13% of global silver production.

It’s also home to some of the biggest silver mines in the world.

The area PAT operates in is active with some of the world’s biggest mining companies like $38BN Teck Resources, $101BN Barrick and $51BN Fresnillo.

(source)

9. Exploration upside in addition to silver (gold and copper)

We think there is also gold (and copper) exploration upside on PAT’s project.

As mentioned earlier, PAT’s project is ~18km away from the San Gabriel gold mine - which entered production in late 2025.

It's also ~16km away from the ~6M ounce gold, ~46M ounce silver Chucapaca deposit owned by Goldfields/Buenaventura.

PAT’s project has similar deep gold targets to the Chucapaca deposit, which to date, have only been tested by three holes that all hit gold (albeit at low grades) - 81.9m at 0.41 g/t gold and ~234m at 0.25g/t gold.

The CEO of the previous owners of the project had said in 2010 that the "multi-phase nature of the volcanic diatreme complex at Tassa as well as the presence of similar host sediments to the nearby Chucapaca gold discovery”.

So it will be interesting to see what PAT finds with some deeper drilling.

(source)

10. Two non-core projects could be sold to free up cash for the silver project

PAT also has two non-core assets that we think could provide non-dilutive funding for the company (IF sold):

- A lithium asset in Canada - PAT’s project sits along strike from ~$160M Frontier Lithium’s deposits - one of North America’s largest and highest grade lithium deposits, expected to come into production in the coming years.

As mentioned earlier, PAT’s team knows lithium well (from the Prospect exit), so we are backing them to get the most out of this asset for PAT.

- Copper in Zambia - PAT’s project sits ~4km from Sinomine Resources Group's Kitumba copper processing plant (which is scheduled to come online in late 2026).

This asset is fairly early stage (trenching/sampling) BUT if a few drillholes are put in and they come in, it could become an interesting M&A target for the owners of that nearby plant.

Ultimately, we are hoping that a combination of the above reasons contribute to PAT achieving our Big Bet which is as follows:

Our PAT Big Bet:

"PAT re-rates to a $150M plus market cap by proving up the size and scale of its Peruvian silver asset"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PAT Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

More on the Hugh Warner and Prospect Resources story - $6M micro cap explorer to US$378M cash pay day

One of the biggest reasons for our Investment in PAT is due to its leadership by chair Hugh Warner.

Hugh was a founding Director and Chairman of Prospect Resources.

Under Hugh’s leadership, starting out as a $6M micro cap company, Prospect acquired, explored and developed the Arcadia lithium project in Zimbabwe.

(That mine is now Africa’s biggest operating lithium deposit).

Shortly after Hugh’s tenure, in April 2022, Prospect’s 87% interest in the project was officially sold for US$378M CASH. (source)

(source)

(source)

Eventually, Prospect distributed ~$444M AUD in cash back to its shareholders. (source)

An excellent outcome for what started out as a $6M micro cap explorer in May 2016.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We Invested in PAT now in the early stages of its exploration as we are backing Hugh to repeat the same formula as he executed at Prospect Resources.

Zimbabwe is normally a region that is considered relatively difficult to do business in - but Hugh discovered a Tier 1 asset and got a deal done.

Of course in mining exploration luck plays a role in making a discovery - so success is not a guarantee.

The past performance of Prospect is not an indicator of the future performance of PAT.

ASX silver stocks run if the silver price runs

(in case you missed it)

Long time readers know we are mega silver bulls.

When the silver price runs, it will generally take ASX silver stocks up with it.

(like we saw a few months back)

We like silver and think the price is currently consolidating after a face melting run in late 2025.

Silver was the best performing commodity of 2025.

From its March 2025 lows of US$29/oz to a peak of US$121/oz just ten months later in January 2026:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

But like most price run ups, silver needs to consolidate at a new higher level for a while - which it has been doing for the last two months.

After some consolidation... we think it’s going higher than its January all time highs (we could be wrong though, of course).

Now what about ASX silver stocks?

We saw what happened to most ASX silver stocks during the silver price run from March 2025 to January 2026.

(look, if you didn't see - they all went up a lot)

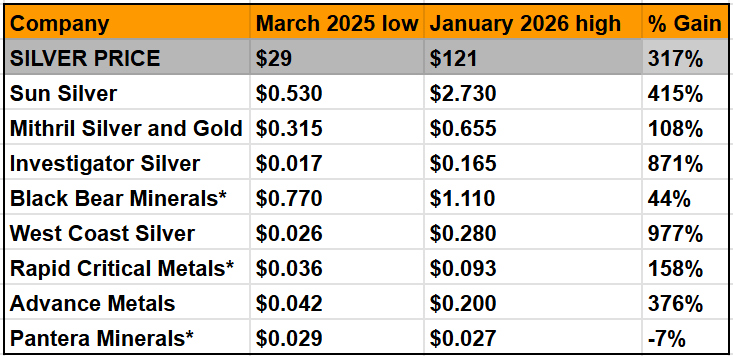

Here’s a few examples of our what our silver stocks did during the Mar 2025 to Jan 2026 silver run:

Note: these are company share prices at March 2025 lows to January 2026 highs and NOT our Investment performance.

* indicates the company acquired a silver project post March 2025 so the starting price shown is at close on the day prior to the acquisition announcement.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

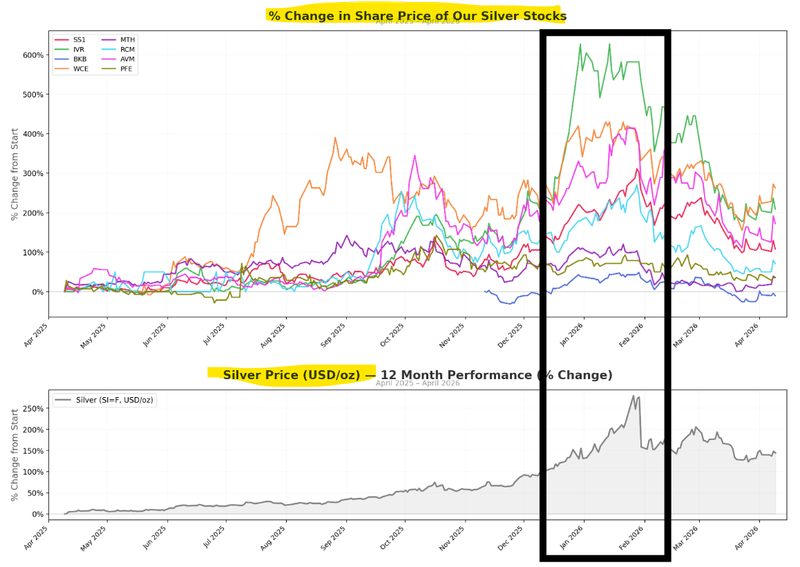

You can see it here too overlaid on a chart, this time highlighting the December 2025 to Jan 2026 window when silver spiked up:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Point is, there looks to be a strong correlation between the silver price going up and silver stocks going for a run.

So if we think silver is going to run hard again...

And now that silver is well into building a new base for what we think will be the next leg up...

AND silver stocks have been taking a breather too...

We think it's a good time to add another silver stock - PAT - to our Portfolio.

We are still very bullish on silver - we think it will run again.

Our favourite momentum and technical analyst, Michael Oliver, just dropped a new video.

In it, he is calling a US$300 to US$500 silver price “by summer 2026”.

(we assume he means North American summer which is in a couple of months from now)

He reckons silver’s consolidation phase will last a few more weeks.

He's the guy who correctly called the triple top silver breakout at $36/oz back in early 2025.

He also said there's going to be a correction on the journey to those targets - which we saw at the start of February - he got that one right too.

There is nothing more dangerous than an analyst on a heater who has got a few things right in a row... of course he can also get things wrong - it's just one prediction that may not eventuate.

But if silver DOES do something silly like go to US$300 or US$500 - well it's game on for a second (hopefully much stronger) rally in silver stocks like PAT.

(based on what we saw with other ASX silver stocks during the 10 month silver run from $29 to the $121 peak)

Even if we only get a fraction of what Oliver is predicting and silver runs to US$150 per ounce we think silver stocks could do really well from here.

Check out that latest video of Oliver again - watch it here

(his predictions are way higher than we are personally hoping for — but it's a fun “confirmation bias” listen if you're long on silver like we are)

We think the silver price needs to consolidate the recent gains - go sideways for a bit, prove the re-rate is real - for the broader market to start believing and the big boys to start buying.

Once that happens, institutional capital can adjust their models to a higher floor price for silver, and generalists can feel comfortable knowing the price rally wasn't a temporary flash in the pan.

If you're a glass-half-full person, this is the consolidation before the next leg higher.

If you're a glass-half-empty person, silver just fell 47% from its all-time high and you're still underwater from January. It could stay sideways for a long time OR even go another leg lower.

We're in the glass-half-full camp. Obviously.

But once again - all commodity prices are extremely hard to predict, and there’s no guarantee that any future silver price will eventuate.

Ultimately we remain bullish on silver - and that’s one of the reasons we have added PAT to our Portfolio today.

Investment Memo 1: Patriot Resources (ASX:PAT)

Memo Opened: 10-04-2026

Shares Held: 18,680,000

What does PAT do?

Patriot Resources (ASX:PAT) owns a silver project in southern Peru with a 31.4 million ounce silver equivalent JORC resource.

PAT also has two non-core assets (copper in Zambia, lithium in Canada) that we think the company could deal out to fund its silver project.

What is the macro theme behind PAT?

Silver is both an industrial and a precious metal.

Silver also has a prominent industrial use case in the manufacture of photovoltaic cells for solar panels - and as such can be considered important to the energy transition.

Silver just recently made all time highs and we think it is now finding a base to consolidate in before another run higher.

(of course we could be wrong - no one knows what's going to happen with commodity prices)

PAT’s projects are in Peru which is the 3rd biggest producer of silver in the world.

Our PAT Big Bet

"PAT re-rates to a $150M plus market cap by proving up the size and scale of its Peruvian silver asset"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PAT Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 10 Reasons We Invested in PAT

- We think silver is getting ready to run to new all time highs

- PAT has an existing 31.4M ounce silver equivalent resource that we think can grow

- We are backing the team from Prospect Resources here

- ~$12M market cap and a tight capital structure.

- The current resource underpins PAT’s valuation

- PAT’s silver asset was previously owned by $38BN Teck Resources

- PAT’s project is next door to the 1.8M ounce San Gabriel gold mine, owned by $14BN capped

- Peru is a fertile hunting ground for silver

- Exploration upside in addition to silver (gold and copper)

- Two non-core projects could be sold to free up cash for the silver project

What do we want to see PAT do next?

Objective #1: Drill and update the current silver resource

We want to see PAT drill its silver project in Peru and confirm the existing 31.4M ounce silver equivalent JORC resource.

With the first program, we want to see the previous results confirmed with infill drilling.

Milestones:

🔲 Phase 1 drill program (mostly infill drilling)

🔲 Assay results from phase 1 drilling

🔲 Updated JORC resource.

Objective #2: Drill and grow the current resource

Once PAT has run some infill drilling campaigns, we will be looking for PAT to do some exploratory drilling by stepping out and testing extensional/deeper targets.

That’s where we are hoping PAT grows its current 31M oz silver equivalent resource to the upper end of its 87M ounce silver equivalent exploration target.

By growing the resource PAT will be able to be better compared to its other silver peers on the ASX.

Milestones:

🔲 Phase 2 drill program (mostly infill drilling)

🔲 Assay results from phase 1 drilling

🔲 Updated JORC resource (target: 50M+ silver equivalent ounces)

Objective #3 (Bonus): Sell non-core assets

We think PAT could also unlock capital for its silver asset in Peru by spinning out its projects in Zambia and Canada. Any deal here would be a bonus.

(PAT has a copper asset in Zambia and a lithium asset in Canada).

What are the risks?

Exploration risk

The company’s silver project has a resource based on ~26 historical drill cores and is 100% in the inferred category.

There is no guarantee that PAT's upcoming drill programs will confirm the presence of additional mineralisation, upgrade the resource classification, or deliver the kind of results needed to justify a development pathway.

Early-stage exploration is inherently risky and many projects fail to deliver economic mineralisation.

Commodity price risk

PAT, as a silver exploration company is exposed to movements in the silver price.

Silver prices are currently near all-time highs - should silver prices fall, this could hurt the PAT share price significantly.

A silver price correction from current levels is a real and meaningful risk.

Funding risk / dilution risk

PAT is a pre-revenue explorer and so it is always reliant on access to fresh capital to fund drilling and exploration.

Further capital raises will be needed, and these may take place at a discount to the prevailing share price, diluting existing shareholders.

PAT’s silver project also has deferred cash payments attached for up to US$3M over 30 months, so PAT may need to raise to fund these payments also.

There is no guarantee PAT can access capital on favourable terms.

Geopolitical risk

Peru has experienced significant political instability in recent years, with three presidents since 2023.

The country has also had problems with illegal mining operations and social conflicts stalling new project developments.

PAT’s silver project is in the pre-permit phase for drilling operations right now and there is no guarantee that community relations or regulatory approvals will proceed smoothly.

There is also a risk that PAT gets "stuck" in early-stage exploration without progressing to scoping studies, feasibility, or attracting a development partner due to the geopolitical/political risks in country.

Delays could mean newsflow dries up and PAT’s share price drifts lower.

Market risk

Broader market sentiment could deteriorate, particularly for small-cap explorers.

If the ASX small-cap market enters a period of weakness, PAT could struggle to attract the capital and attention needed to advance its silver project, regardless of the quality of the underlying asset.

Other risks

Like any small-cap exploration company, PAT carries significant risk, here we aim to identify a few more risks.

While PAT has an existing 31.4M ounce silver equivalent JORC resource, it is entirely in the 'Inferred' category and based on just 26 drill holes.

There is a high statistical probability that infill and step-out drilling fails to replicate the grades or continuity needed to upgrade the resource classification to 'Indicated' or 'Measured', which are required for robust economic studies.

Operating across vastly different jurisdictions, Peru for silver, Canada for lithium, and Zambia for copper also stretches management bandwidth. Advancing multiple exploration fronts simultaneously requires immense capital and logistical effort.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our Investment Strategy?

Our plan is to hold the majority of our position in PAT for a minimum of 18 months, which we hope is enough time to see PAT drill out its project, hopefully make more discoveries and the silver price to go on the run we hope it will.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates in line with our minimum hold conditions.

We intend to maintain a position in PAT for 2 to 5 years.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.