Our Latest Investment: OD6 Metals (ASX: OD6)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 10,650,000 OD6 Shares at the time of publishing this article. The Company has been engaged by OD6 to share our commentary on the progress of our Investment in OD6 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our latest Investment is OD6 Metals (ASX:OD6).

The $13.5M capped OD6 just acquired an option on an asset in the USA with historic production for the US critical mineral of...

Fluorspar.

(fluor-what now? Hang in there for one second...)

Fluorspar might just be the critical mineral you have never heard of - until today.

Fluorspar is used in the production of missile systems, military electronics and jet fuel, and it has been on the US Critical Minerals List since 2018.

Fluorspar also plays an essential role in AI semiconductor chips, batteries, nuclear power, aerospace and defense.

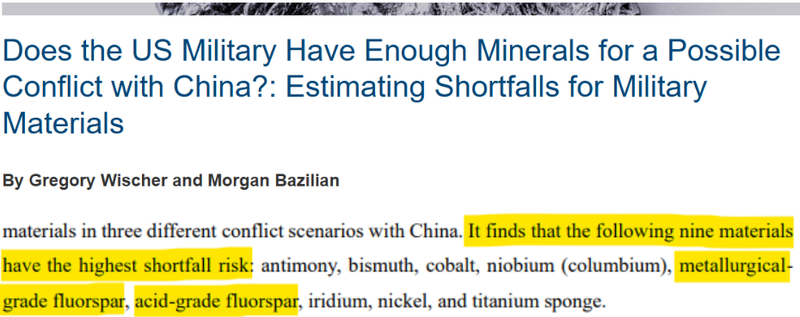

Fluorspar has been identified as one of the nine materials with the highest shortfall risk for the US military in a major conflict scenario. (source)

... and China controls 60% of global supply.

Just six weeks ago the Department of War awarded a US$168.9M supply contract to a company with a development-stage fluorspar project in the USA. (source)

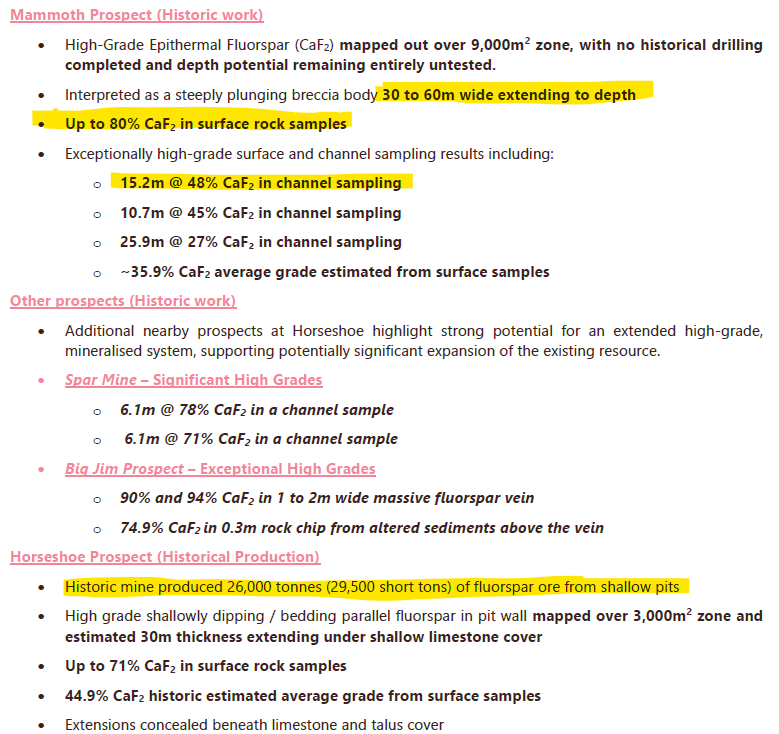

OD6’s new project already produced fluorspar from a small-scale mining operation in the 1950s - producing ~26,000 tonnes of material at an estimated grade of 44.9% fluorite. (source)

This project DOES have a historic resource - but it can’t be announced because it was estimated in 1956 and has not been verified under current JORC guidelines. (source)

Despite the history of production and a mysterious historic resource (non-JORC compliant), the project has NEVER been drilled before...

Which OD6 plans to do ASAP.

OD6’s project sits in the US state of Nevada, where we have had success Investing before:

- Viking Mines (VKA) - up 360% at peak and currently up 280%,

- Sun Silver (SS1) - up 1,478% at peak, currently up 1,039%,

- Black Bear Minerals (BKB) - up 304% at peak, currently up 228%, and;

- Locksley Resources (LKY) (on Nevada border) up 626% at peak, currently up 74%.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

IF 2025 was a small glimpse of what’s to come for the broader US critical minerals macro thematic...

We think the next 2-5 year period could be the window of opportunity for small cap ASX resources companies to take their expertise into the US and find company making assets.

2025 was the year that the starter gun was fired for antimony and rare earths assets in the USA.

2026 looks like it's started with tungsten...

What critical mineral is next?

No one knows for sure, but we are going long on niche critical minerals that fit a certain criteria:

1. It has to be on the US critical minerals list

✅ OD6 has picked a fluorspar asset. Fluorspar is on the US critical minerals list. Fluorspar has also been identified as one of the nine materials with the highest shortfall risk for the US military in a major conflict scenario.

2. Where the US is near or at 100% import reliance

✅ The US has zero domestic fluorspar production and China controls ~60% of global production.

3. Where the mineral is being used in advanced technologies (and preferably defence, AI, robotics or advanced energy).

✅ Fluorspar is required for missile systems, military electronics and jet fuel.

4. Where the US government has sent out signals to the market that it NEEDS supply.

✅ About six weeks ago, the Department of War awarded a US$168.9M supply contract to a company with a similar, development-stage asset in Utah, USA. So we have very recent evidence of the US government putting its money down to secure a supply of fluorspar. (source)

That’s why today, we Invested in OD6.

OD6 just acquired an option on a fluorspar asset in Nevada, USA and completed an $3.4M raise at 5c/share.

Again, OD6’s new project produced fluorspar from a small scale mining operation in the 1950s - producing ~26,000 tonnes of material at an estimated grade of 44.9% fluorite. (source)

The project has never been drilled before - the previous mining was limited to near surface material from the side of a hill.

(This kinda reminds us of the previously “small scale mined” tungsten assets VKA acquired in Nevada. VKA is up 280% in ~90 days - past performance of VKA is not an indicator of future performance of OD6)

(source)

As far as we know, OD6 is the only company on the ASX with a fluorspar asset in the USA.

We like a first-mover in ASX small cap land.

OD6 Metals

ASX:OD6

OK but what is fluorspar? Does the US REALLY need it?

Fluorspar (AKA Fluorite) is the world's primary source of fluorine.

Without it, you can't make the chemicals needed for semiconductors, lithium-ion batteries or uranium processing.

There is also no commercially scalable lithium-ion chemistry without fluorine, and no fluorine without fluorspar.

And in defence - it's used to produce missile systems, military electronics and jet fuel.

Fluorspar has been identified as one of the nine materials with the highest shortfall risk for the US military in a major conflict scenario:

(source - from the full paper)

Right now, the US has almost zero domestic fluorspar production and China controls ~60% of global production. (source)

Fluorspar was one of the O.G. critical minerals - making it into the US critical minerals list way back in 2018 - it has maintained its status on that list ever since.

And fluorspar was one of the few minerals that was added to the tariff exemption list by the Trump administration in April 2025.

(source)

(meaning that supply was too important to the US to mess with by imposing import tariffs)

It’s also on the critical minerals lists of the EU, Australia and Japan.

Fluorspar is also one of the materials included in the US$12BN strategic stockpiles initiative (Project Vault).

A few weeks ago the US Department of War awarded a fluorspar supply contract (initially US$168.9M - with a US$250M contract ceiling - to a development stage fluorspar company in Utah, USA.

(source)

Fluorspar has also done well on the ASX before

Another reason for our Investment in OD6 is because there is already one ASX success story for a fluorspar company with assets in Western Australia, the $970M capped Tivan (ASX: TVN).

Tivan’s project is in a joint venture with Japanese conglomerate $69BN Sumitomo.

That fluorspar supply is headed to Asia...

... which means there is no real way to get US fluorspar exposure on the ASX - outside of OD6.

Another reason we like OD6 is because the grades from its project are multiples higher than Tivan’s.

Tivan’s resource is 43.2mt at 8.3% Fluorspar. (source)

Whilst OD6 does not have a defined resource estimate yet, OD6 is sampling grades up to 94% in rock chips and 48% fluorspar across 10+ metre channel samples (source)

(source)

Remember OD6’s project produced fluorspar from a small scale mining operation in the 1950s - it produced ~26,000 tonnes of material at an estimated grade of 44.9% Fluorite. (source)

That’s production at grades that are ~7.5x Tivan’s resource.

Tivan is capped at $974M.

OD6 - with an asset in the US - is capped at $13.5M.

Now, Tivan is a lot more advanced relative to OD6 with a defined resource estimate and a major partner involved backing its project. Market cap differences reflect these vastly different stages of development.

But so far we have some precedents set for:

- A pre-resource asset in the US gets a US$169M supply contract signed, and

- A company with a big resource brings in a multi billion dollar partner.

Validation for us that an asset with both (a resource AND inside US borders) could end up being a company maker for an ASX small cap.

We need to reiterate here though that thematic conviction doesn't guarantee individual stock success. OD6 is an early-stage explorer and the fluorspar market is small and opaque. Our macro thesis on US critical minerals may not translate into value for every company in the space, and we could be wrong about both the timing and the opportunity.

In the rest of today’s note, we will run through:

- Why we Invested,

- Our “Big Bet”,

- Outline our Investment Memo, and

- What we want to see OD6 execute on over the coming 12 months.

But first, here are the key reasons why we Invested in OD6:

11 reasons why we Invested in OD6

1. Low market cap with room to re-rate higher.

OD6 will have a market cap of ~$13.5M and an enterprise value closer to ~$8M (at 5c per share) following the completion of the capital raise announced today.

We think the company’s current valuation is at a level where it can re-rate to multiples of where it is now - especially IF the “US critical minerals playbook” is executed well and the market continues to reward the sector - and of course some successful drill results confirming the size and scale of the deposit.

No guarantees of course - this is small cap early stage resources investing - things can and do go wrong.

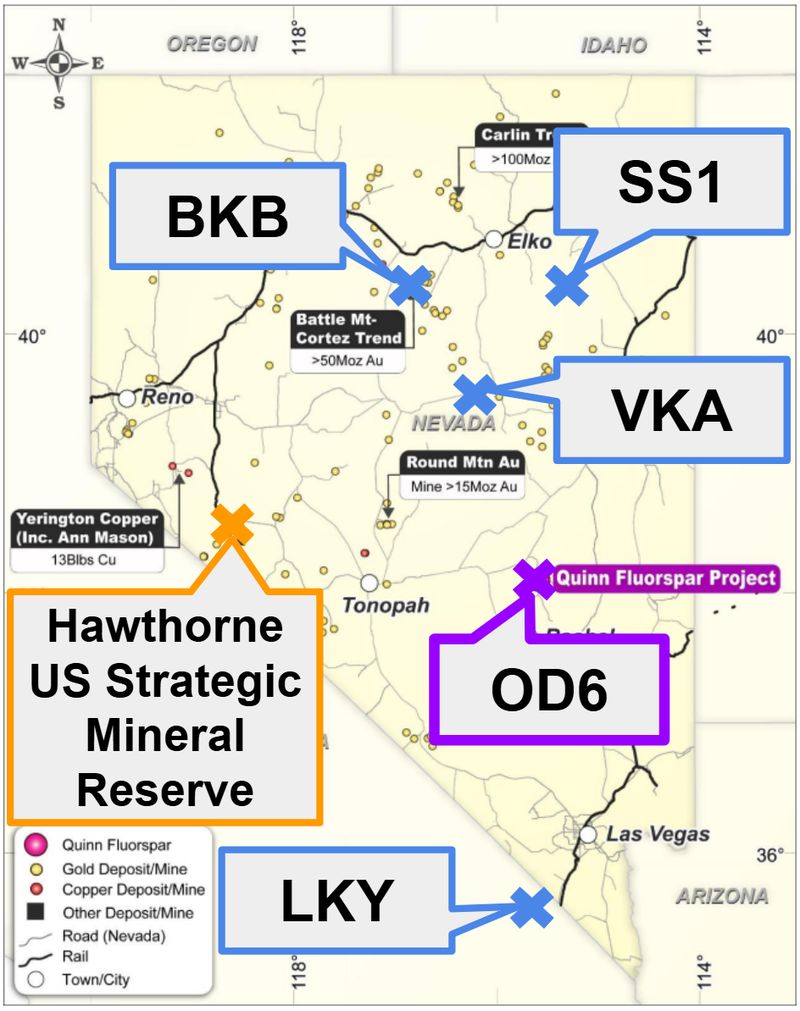

2. OD6’s Fluorspar asset is in Nevada, USA. We have had past success in Nevada.

We like Nevada as a mining jurisdiction within the USA because it's home to some of the biggest, lowest cost mines in the country, and we have had some good success in Nevada before (SS1, BKB, VKA).

The past performance of these stocks is not an indicator of future performance of OD6.

3. OD6’s projects have produced fluorspar in the past but have never been drilled.

The project OD6 is acquiring has produced 26,000t from a small scale open pit before. The project has never been drilled before either. The mining was limited to carving out a hillside... we wonder what systematic exploration drilling could yield?

This project DOES have a historic resource - but can’t be announced because it is from 1956 and has not been verified under current JORC guidelines. (source)

4. OD6 is a ASX listed first mover into US fluorspar assets

As far as we know, right now, there are no other ASX listed companies with pure-play fluorspar assets in the US.

We have observed that the first movers in an emerging investment thematic often do the best.

5. Fluorspar is listed as one of the 12 strategic defence critical minerals in the US

The Pentagon explicitly mentioned fluorspar as one of the minerals it is looking to buy as part of its US$12BN critical minerals stockpile. (source)

Fluorspar has been identified as one of the nine materials with the highest shortfall risk for the US military in a major conflict scenario.

6. The US Department of War awarded a US$169-250M supply contract to another US based fluorspar asset in January 2026 (source)

It’s clear the Department of War wants to secure its domestic fluorspar supply given the contract award of a few weeks ago.

We are backing OD6 to define a fluorspar resource of its own, fast-track it toward development and hopefully one day, receive similar funding deal/purchase contracts.

7. China controls 60% of Fluorspar supply

The US has zero domestic fluorspar production which we think makes projects like OD6 (inside US borders) valuable.

8. There is a listed fluorspar success story on the ASX capped at $974M

We think that having a success story in the market is important. ASX listed Tivan has a fluorspar asset in WA and is capped at $974M.

Tivan’s project looks to be targeting supply into Asia. We are backing OD6 to achieve success by targeting supply into North America (mainly the US).

9. Capital is flowing into US critical minerals macro thematic

We think OD6’s US fluorspar asset could attract increased capital flows both on the ASX and from North American investors/governments/institutions.

10. OD6 can follow the “US critical minerals playbook”

There is a playbook for ASX stocks to attract more attention and capital to projects that are based in the US (source). OD6 isn’t yet listed in the US. We think that if its project gets any market traction it could go for a US listing that opens up the company to North American investors.

11. Free kick on “one of Australia’s largest and highest grade clay hosted rare earths deposits” (source)

OD6 also owns one of the largest and highest-grade clay-hosted rare earth deposits in Australia which in its own right could become a company maker.

We are mainly Invested in OD6 for the US fluorspar project but the WA rare earths come with it as a sort of “free option”.

Ultimately, we hope the above reasons contribute to OD6 achieving our Big Bet which is as follows:

Our OD6 Big Bet:

"OD6 re-rates to a +$200M market cap by defining a significant fluorspar resource in Nevada, attracting US government funding or a strategic offtake/supply deal, and/or attracting a takeover bid at multiples of our Initial Entry Price."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our OD6 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

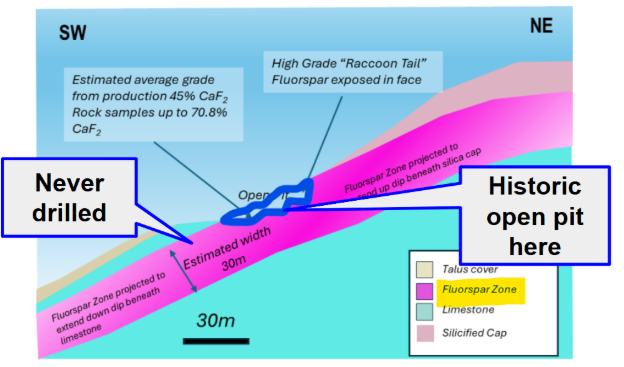

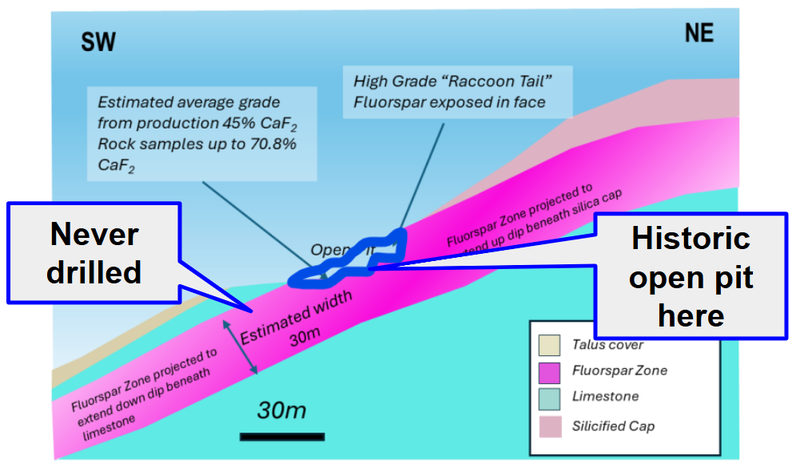

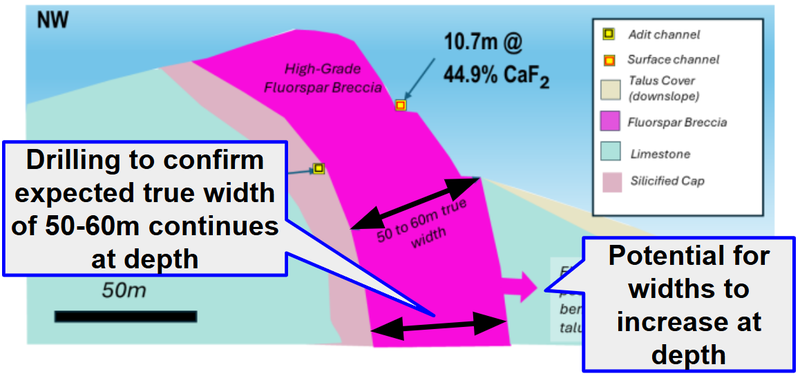

As mentioned earlier, the asset OD6 is acquiring has produced fluorspar in the past.

Previous production was from an open-pit on the side of a hill - the project has actually NEVER been drilled before.

Apart from production, there has only been channel and rock chip sampling on the project - which is basically scraping the surface and then assaying it.

Here is how it all looks in a cross section:

(source)

What we don't know YET is how big the “estimated widths” are - which will require OD6 to do some drilling to find out.

What we do know is that OD6's project DOES have a historic resource - which OD6 didn't announce because it is from 1956 and has not been verified under current JORC guidelines.

(source)

Despite that history of production and a mysterious historic resource (non-JORC compliant), the project has NEVER been drilled before.

Next we want to see OD6 drill test the project and hopefully reveal thick fluorspar rich zones behind the wall faces:

(source)

No guarantees there will be fluorspar deeper in the ground though - we’ve been burnt by a few ‘drilling into a hill face with surface mineralisation’ before - there’s always a chance OD6 drills dusters here.

We think OD6 is in the right place at the right time - USA good, Nevada, even better

OD6’s projects are first and foremost inside US borders.

Second, they are in Nevada, the top ranked mining state of the USA, ~300km by road from the newly established US Strategic Minerals Reserve.

We have had a lot of success backing projects in Nevada - which feels to us like the WA of the USA.

- Viking Mines (VKA) - up 360% at peak and currently up 280%

- Sun Silver (SS1) - up 1,478% at peak currently up 1039%

- Black Bear Minerals (BKB) - up 304% at peak currently up 228%

We also have Locksley Resources (LKY) (Not in Nevada, but right near the border in California) - up 626% at peak, currently up 74%

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Here is OD6 on the map, along with all our other Nevada ASX Investments:

(source)

Being inside US borders was another reason for us Investing in OD6.

We think the US has over the last 12-18 months been laying the groundwork to unleash its domestic mining industry.

IF/When it does, we think small companies, who came into the right assets inside the US early will be the biggest beneficiaries (like OD6).

One month ago the US passed legislation locking in parts of Trump's executive orders related to boosting domestic hardrock mining, aimed at establishing "American Mineral Dominance." (source)

Special Assistant to the US president, National Security Council - David Copley gave at Saudi Arabia’s Future Minerals Forum where he said:

“Over the next few years the US government will deploy hundreds of billions in capital into the mining sector”

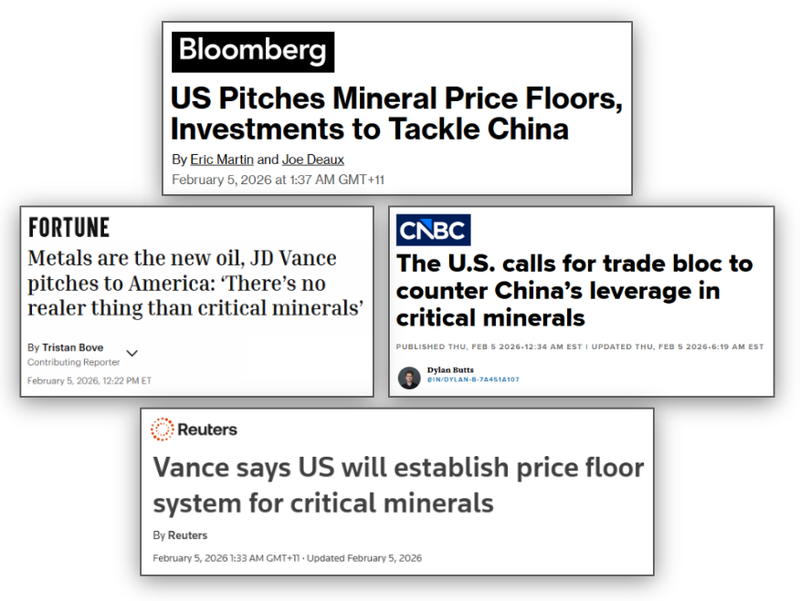

And US Vice President JD Vance gave a speech discussing critical mineral price floors, where he also said that despite all of the backing the US government has given the industry to date, private capital just hadn't reacted yet.

(implying there is a lot more work to be done to get projects off the ground)

(source)(source)(source)(source)

We think the whole US critical minerals macro thematic is only just getting started - and if the US is serious about rebuilding western critical minerals supply chains/processing capacity.

It will need trillions of dollars in investment, not billions...

For anyone wanting a deep dive into why it's a trillions problem and not a billions - we highly recommend listening to the following interview with Craig Tindale.

Craig authored the “Return to Matter” paper in early 2026, which analyses the fragility of the Western economy in the face of China's dominance in physical, tangible industries.

Craig gives one of the best articulated explainers of the US critical minerals theme we have heard.

One of the main arguments he makes is to expect a move toward sovereignty-focused state capitalism in the West, directing capital back into strategic resources, refining and munitions, with a major rotation into hard assets.

Which we are already starting to see in the US with the Department of War being put in charge of shoring up critical minerals supply chains... (and making direct investments into companies).

Now, all we need is for some of that capital and attention to come fluorspar’s way...

Investment Memo 1: OD6 Metals (ASX:OD6)

Memo Opened: 04-03-2026

Shares Held: 10,650,000

What does OD6 do?

OD6 Metals (ASX:OD6) is acquiring the Quinn Fluorspar Project in Nevada, USA.

OD6’s project has historic production dating back to the 1950s, from an open-pit mine totalling ~26,000 tonnes of Fluorspar.

OD6 also owns one of Australia's largest and highest-grade clay-hosted rare earth deposits in WA.

What is the macro theme behind OD6?

Fluorspar goes into producing hydrofluoric acid and is a designated critical mineral in the US.

Fluorspar is essential for producing missile guidance electronics (semiconductor etching), radar and satellite systems, jet engine components, military-grade lithium batteries, and AI data centre infrastructure.

The US is 100% import-reliant for fluorspar and China controls ~60% of global supply.

Capital is flowing into US critical minerals projects - especially ones where the US has ZERO domestic production and China controls ~60% of global supply - like Fluorspar.

OD6 is a first mover on the ASX into US based Fluorspar assets.

Our OD6 Big Bet

"OD6 re-rates to a +$200M market cap by defining a significant fluorspar resource at Quinn's, attracting US government funding or a strategic offtake/supply deal, and/or attracting a takeover bid at multiples of our Initial Entry Price."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our OD6 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 11 Reasons We Invested in OD6

- Low market cap with room to re-rate higher.

- OD6’s Fluorspar asset is in Nevada, USA. We have had past success in Nevada.

- OD6’s projects have produced fluorspar in the past but have never been drilled.

- OD6 is a ASX listed first mover into US fluorspar assets

- Fluorspar is listed as one of the 12 strategic defence critical minerals in the US -

- The US Department of War awarded a US$169-250M supply contract to another US based fluorspar asset in January 2026

- China controls 60% of Fluorspar supply

- There is a listed Fluorspar success story on the ASX capped at $974M

- Capital is flowing into US critical minerals macro thematic

- OD6 can follow the “US critical minerals playbook”

- Free kick on “one of Australia’s largest and highest grade clay hosted rare earths deposits”

What do we want to see OD6 do next?

Objective 1: Complete deal

We want to see OD6 complete acquisition of the US Fluorspar project.

Milestones:

🔲 Due diligence process completed

🔲 Option to acquire exercised

🔲 Acquisition completed

Objective 2: Target generation for drilling

We want to see OD6 sample in and around the old workings on its project, run some geophysics and generate high priority drill targets.

Milestones:

🔲 Rock chips

🔲 Channel sampling

🔲 Soil sampling

🔲 Geophysics

🔲 Drill targets generated

Objective 3: Drilling and a maiden resource estimate

We want to see OD6 drill out and define a maiden JORC resource estimate for its project.

Milestones:

🔲 Drilling starts

🔲 Drilling results

🔲 Maiden JORC Mineral Resource Estimate

Objective 4: Attract US government funding or strategic partnerships

Given the macro backdrop and the precedent set by Ares Strategic Mining's Pentagon contract, we want to see OD6 engage with US government agencies and explore strategic partnerships with end-users.

Milestones:

🔲 Metallurgical testwork results

🔲 Engage with US DoW, DoE, or DLA regarding domestic fluorspar supply

🔲 Secure government grant, funding, or offtake deal

🔲 Strategic partnership or MoU with a US industrial or defence counterparty

What are the risks?

Exploration risk

OD6 is at an early stage. The Quinn Fluorspar Project has never been drilled. There is no guarantee that drilling will confirm the presence of a significant fluorspar resource at depth, even though historic mining and surface mapping are encouraging.

Early-stage exploration is inherently risky and many projects fail to deliver economic mineralisation.

Commodity price risk

Fluorspar prices are currently elevated due to supply constraints and geopolitical tensions. Should fluorspar prices fall - for example, if China loosens export restrictions or new global supply comes online - this could hurt the OD6 share price and reduce the attractiveness of the Quinn project.

Funding risk/dilution risk

OD6 is a small company that will need to raise capital to fund its exploration programs, option payments, and milestone-based acquisition costs at Quinn's.

Capital raises may take place at a discount to the prevailing share price, which would dilute existing shareholders. There is no guarantee OD6 can access capital on favourable terms.

Acquisition completion risk

OD6 has secured an option over the Quinn assets but has not yet completed the full acquisition.

The deal is structured with an upfront $275k IF the option gets exercised and then milestone-based deferred payments totalling plus A$3.8M. (source)

There is a risk that OD6 does not proceed past the option stage if due diligence is unsatisfactory, or that later milestones prove difficult to fund.

Market risk

Broader market sentiment could deteriorate, particularly for small-cap explorers. If the ASX small-cap market enters a period of weakness, OD6 could struggle to attract the capital and attention needed to advance its projects, regardless of the quality of the underlying assets.

Geopolitical / policy risk

OD6's investment thesis is heavily tied to US government policy on critical minerals, defence spending, and supply chain sovereignty.

A change in US government policy - for example, a relaxation of critical minerals priorities or a thawing of trade tensions with China - could reduce the urgency of domestic fluorspar supply and hurt the re-rate potential.

Development purgatory risk

There is a risk that OD6 gets "stuck" in early-stage exploration without progressing to resource definition or feasibility. Newsflow could dry up between programs, and the share price could drift. We will be watching closely for the company to maintain momentum.

Other risks

Like any early-stage exploration company, OD6 carries significant risk, here we aim to identify a few more risks.

While OD6’s project has historical production, modern critical mineral supply chains require highly refined end products like acid-grade fluorspar. There is no guarantee that the raw ore from the Quinn project can be economically processed and upgraded to meet the strict purity specifications required by US military or battery manufacturers.

The project also relies on exploring and potentially restarting a historic 1950s mine site in Nevada. While Nevada is a tier-1 mining jurisdiction, historic sites can sometimes carry legacy environmental liabilities. Securing modern environmental approvals and drill permits for a site that hasn't operated in ~70 years could cause unforeseen delays or add unexpected compliance costs.

Additionally, OD6 is attempting to aggressively advance a brand-new US fluorspar project while also holding a massive clay-hosted rare earth deposit in Western Australia. Managing two vastly different projects across two continents requires significant management bandwidth and capital. There is a risk that company resources are stretched too thin, slowing overall progress or forcing the company to deprioritise one of the assets.

Finally, as a micro-cap company with a valuation of roughly $13.5M post-raise (at 5c per share), OD6 shares may suffer from low trading liquidity. This means investors may find it difficult to buy or sell large volumes of shares on the ASX without significantly impacting the share price, leading to heightened volatility.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our Investment Strategy?

We are Invested in OD6 to see it progress its project into development.

Our plan is to hold the majority of our position in OD6 for 3 to 5 years which we hope is enough time to see OD6 to move towards development (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may also look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.