Our 2025 Strategy

Published 11-JAN-2025 10:58 A.M.

|

15 minute read

- Commentary: A lot of green during the holiday. Our strategy for 2025. Global uncertainty: defense metals, defense tech, gold and silver. How and why we have changed our Investment strategy over the last 5 years.

- Quick Takes: AL3, JBY, SGQ, TTM, EIQ, MNB, MTH, IVZ, ION, LYN, DXB

Happy New Year.

New year, new market conditions...?

We certainly hope so.

Around this time every year, the ASX goes very quiet.

Starting from just before Christmas...

to around the end of January.

The perfect time to sit down, clear the brain and think about an Investment strategy for the year ahead.

(we have done our 2025 strategy, which we’ll share today in this note)

During the holiday break, ASX trading is still open on most weekdays.

But most of the usual market participants are on holidays and not paying much attention.

And certainly not being too active on the screen.

Generally, the day after the Australia Day public holiday is the “unofficial” restart day when everyone is back.

(This will be January 28th this year.)

Our team has been on a break too.

Aside from the occasional glance at the watchlist and thinking about our strategy for 2025.

Our observation of the ASX small cap market over the quiet holiday period was that there was a lot more green than there was red - albeit on very low volumes.

We take this as a positive sign for the year ahead.

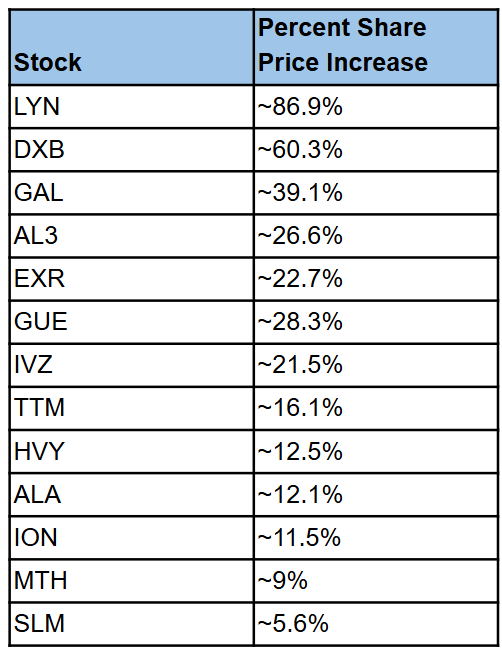

A few companies from our Portfolio have moved strongly between 23rd December and yesterday:

(Source - TradingView)

The performance of this handful of stocks while the ASX is meant to be in a “quiet holiday period” is certainly a positive sign for 2025.

Market conditions in the small end were generally tough during 2024.

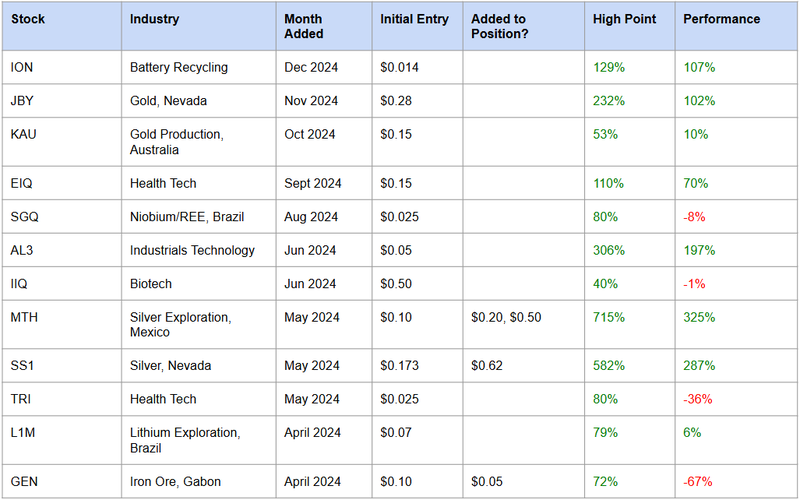

Our 2024 strategy did manage to string together a few winners from our new Portfolio additions last year.

Here is how our 2024 picks have performed so far...

(getting some winners in 2024 was great after the shocker we had in 2023)

Based on 2024 market conditions, later stage companies that we identified as undervalued at the time seem to be performing a lot better for now.

So what’s our Investment plan for 2025?

Every year our strategy and plan adapts to optimise for the market conditions.

We also try to get ahead of new macro themes that we predict will attract capital in the near to medium term.

(like electric vehicles and battery metals did in 2020 and 2021)

We are broadly sticking to a similar strategy that worked well in 2024, while the small end of the market continues to figure out if it wants to lift itself off the floor this year.

Here’s the high level summary of our 2025 strategy for new Portfolio additions:

- Again, a mix of resources, tech and biotech

- Between 8 to 12 new Portfolio additions in 2025

- Generally Investing in companies capped under $200M, mostly sub $30M

- Key macro theme: Rising global and geopolitical uncertainty.

- Gold and silver

- Defense technology

- Defense materials/metals

- Other strategic, critical materials (for semiconductors, critical technologies etc)

- Continue to focus on “later stage” companies we think are undervalued

- Find companies that have a near term higher probability of achieving size and liquidity to

- Qualify into a market index (= index fund buying)

- Meet the minimum threshold for institutional funds to invest

- Add one (maybe two) early stage exploration companies

- Interested in energy and alternative energy: oil & gas, uranium, natural hydrogen, geothermal. Also carbon capture.

- Biotechs - follow proven successful biotech investors into their next investments, ideally in the lead up to major catalysts like clinical trials

- Consider beaten down, high quality, advanced stage battery metals projects (countercyclical)

If you know of any ASX listed companies that fit into one of the above categories, please reply to this email with the stock code (and a short description), and we will take a look.

We are also interested in seeing private/pre-listing companies and seed offers in the above sectors - again, just reply to this email.

Generally, we will try to find companies in the $10M to $30M market cap range, with a view that they will deliver enough material to progress over 12 months to move to a $100M to $150M range.

That being said, last year we also invested in companies closer to the $100M market cap size too.

How our plan and strategy has evolved over time

Before we look to 2025, here is a very quick summary of our last 5 years to give some context and rationale for our Investment strategy for this year.

2020 and 2021 was a roaring bull market for ASX small cap stocks.

Everything was going up.

Electric vehicles, battery materials and green tech was THE macro theme attracting all the attention and capital.

VUL and LRS were our best new additions from this period.

VUL and LRS being examples of “real companies” that emerged from the capital flows into the white hot battery metals macro theme...

They both became and remain real companies even AFTER the heat dissipated and capital left the battery materials theme.

In 2021 we found an “undervalued”, later stage tech company ONE - which is still one of our best Investments to date.

The success with ONE is what first got us thinking about focusing more on finding later stage companies that we believe are undervalued.

In 2022 the small end of the market went into bear-mode.

Sentiment turned negative.

Everything started coming down.

Interest in battery metals waned... hard.

The best performers as of today that we added in 2022 are ALA and CAY.

(ALA is a biotech and CAY is a later stage resources company)

The next year 2023... was not a good year for us.

(or for most people that remained in the small end of the market)

We added new Portfolio companies that “looked cheap” thinking the market would turn around in the second half of 2023...

It did not.

It got worse.

So we paused any new Portfolio additions for about 6 months to give the market more time to find its bottom.

(we did not add any new stocks to our Portfolio from October 2023 until April 2024)

With the benefit of hindsight, in 2023 we started adding new Portfolio companies too early, before the market had found a bottom.

At the time we thought we were picking up some “bargains”... but they just got cheaper again.

We were anticipating a return of interest and capital into the small end of the market that didn’t materialise.

We got burned as money exited early stage exploration stocks.

In 2024, after our 6 month pause and plenty of time to refine our strategy, we switched our focus to find undervalued, later stage companies.

Companies with more advanced, later stage projects but share prices beaten down in the ongoing, tough small cap market conditions.

Still with significant upside potential.

Yet their value is underpinned by real, underlying assets.

In 2024 this new strategy delivered a good number of winners.

(with a couple of “stumblers” as statistically expected across a basket of high risk small cap stocks)

Most new Portfolio additions were coming off such a low base that material progress has seen the share price go up, and importantly stay up.

A sign that the bottom is in?

SS1, MTH, AL3, EIQ and ION have all delivered and held onto significant gains since we first Invested in 2024.

While we are still interested in early stage explorers, we are a lot more selective now and have reduced the number of pure “exploration punts” taken.

(we will consider new explorers in defense raw materials or critical minerals)

We have had some solid winners in biotech since we first committed to learn about biotech Investing and launched our biotech Portfolio back in 2021.

We think it’s good to diversify away from only natural resources, and we have been following the lead of experienced, successful biotech investors.

This strategy has worked so far and we expect to add a few more biotechs to our portfolio in 2025.

We will also look at at least one new technology pick this year.

Overall the 2024 strategy worked well for us last year, even though the small end of the market was difficult.

So the strategy will be similar in 2025.

Now we just need a new major macro theme to bring the interest and capital back into the small end of the market...

What will be the “2020/2021 Electric Vehicles” theme in 2025?

So we are broadly sticking to our 2024 strategy in terms of stock selection.

Later stage, undervalued companies that can materially re-rate on good news, off a low base.

The big difference we want to see in 2025 is the emergence of a strong, new macro theme that will drive capital flow into small cap stocks in that theme.

Like we saw with electric vehicles and battery metals in 2020 and 2021.

And the ultimate recipe for success is when a strong, new macro theme joins forces with improving market-wide sentiment and “risk on” appetite.

So what could be the new “2020-2021 electric vehicles and battery metals” theme for 2025?

A global investment theme needs to be big, easy to understand and affect nearly everyone.

A general theme that started emerging in 2024 was global and geopolitical uncertainty...

(so far this has delivered us some great early winners in gold and silver)

Our plan is to place more bets in the expectation of growing “global uncertainty”.

Global uncertainty is not exactly a “theme” in itself, but our view is that growing global uncertainty will drive capital into certain sectors.

Specific sectors we will be looking for new Investments include:

- Gold and silver

- Defence technology

- Defence materials/metals

- Other strategic, critical materials (for semiconductors, critical technologies etc)

2025 Key Macro Theme: Global Uncertainty?

Reading the mainstream news and social media, geopolitical tension seems to be increasing.

Sabres are rattling all around the world.

The US and China are ramping up tit-for-tat export restrictions on AI components, critical minerals, processing technologies and defense materials and technology.

Wars in the Ukraine and Middle East are still flaring.

A new Trump led US administration is taking office in a few weeks.

And the incoming US president is already making comments about “annexing Canada in recent weeks... Donald Trump is now outlining his goals of acquiring both Greenland and the Panama Canal.” (Source)

(bit more incoming global uncertainty being telegraphed by Trump)

Trump is also expected to backpedal from the US’s current role as the “police for the world order”.

Many countries have already started to increase their defence spending as a deterrent to traditional rivals who may be emboldened by a reduced US presence.

Trump and conservatives are also actively pushing allies to increase their defence spending.

The security of waterways and seaborne trade routes will be important - we have already seen conflict in the Red Sea and South China Sea last year (not to mention the recent disruption of Baltic sea power cables and the gas pipelines)

And the US now wants to share the cost of maintaining this order while they focus their resources elsewhere.

It looks like global defence spending is going to continue to rise as the US shifts some of the responsibilities of maintaining global order to its allies over the coming years.

And there likely will be a matching defence spending response from adversaries.

In periods of global uncertainty, defence spending rises.

A few months ago we wrote about countries ramping up to record defence spending.

We think defence spending is going to rise across the board over the coming years.

Increased demand globally for planes, ships, submarines, drones, vehicles, munitions, missiles, defense systems and technologies.

And the metals and materials needed to build them.

A couple of days ago Trump reiterated his long held view that the 32 NATO member countries should be spending 5% of their GDP on defence - up from the current 2% (Source)

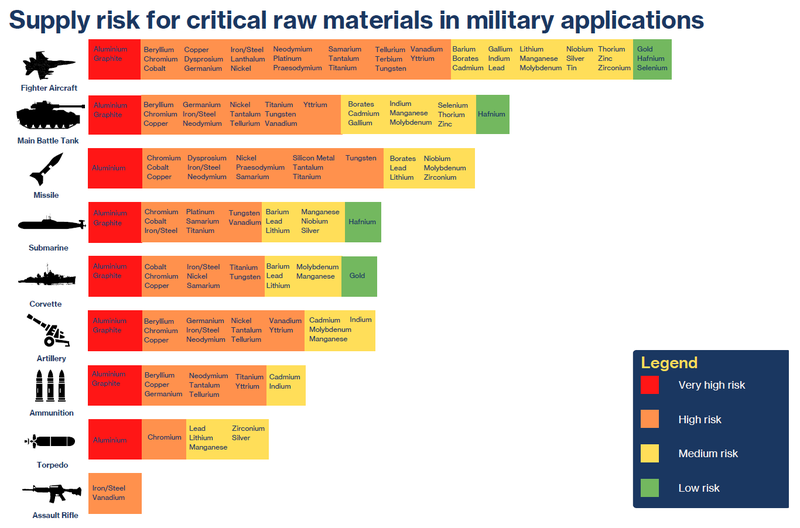

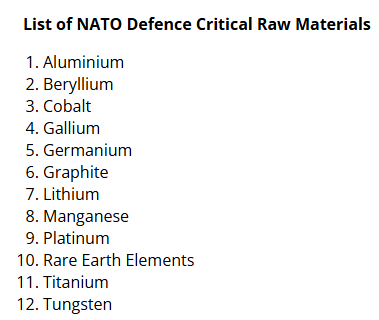

A few weeks ago NATO released a set of 12 “defence-critical raw materials”.

(Source)

Like with electric cars back in 2020 and 2021 needing “battery metals”.

Defence supply chains need “defence critical raw materials”

(Read about the NATO release here)

This is just for the 32 NATO member countries.

And the NATO defense critical raw materials list is by no means exhaustive.

There are many other countries in the world that will need to reconsider their defence spending levels over the coming decade.

While it's impossible to predict where prices for these raw materials will be in 6 or 12 months' time, we think the macro theme will definitely get a lot more attention as the year goes on.

Especially because we are already seeing export restrictions on critical raw materials being used by countries to exert power over their adversaries.

In the coming weeks we will also talk about how countries build strategic stockpiles of critical raw materials, which we think will come into play in 2025.

So in summary...

Bringing everything together, our 2025 Investment strategy will be centered around:

- Growing global uncertainty

- Safe haven assets (gold/silver)

- Increasing defence spending

- Military critical raw materials

- Other strategic, critical materials (for semiconductors, critical technologies etc)

- Biotechs and other interesting tech

If you have a favourite company that fits the bill for one or more of these things - we’d love to hear what it is and why you like it - simply reply to this email (we read all the responses).

We will also prioritise later stage companies that we think can eventually attract capital inflows from institutional investors and index funds.

As always, we are looking for 8 to 12 new stocks this year that fit in with the strategy we outlined above.

AND continue to follow the progress and cover material news from our Current Investments from previous years.

Welcome to 2025.

Quick Takes 🗣️

AML3D to make tailpiece components for the US nuclear submarine program

JBY Phase 1 drilling complete and new rock chip results

SGQ secures $20M in funding for advanced Brazilian niobium/REE asset

SGQ signs niobium and rare earths tech agreement - with development in mind

TTM restarts drilling for gold and silver at Dynasty

SGQ signs niobium and rare earths tech agreement - with development in mind

EIQ requests FDA meeting for AI heart failure product.

AL3 share price performs strongly after Christmas

MNB starts construction of phosphate project

MTH team strengthened ahead - Ex CEO of Ivanhoe Mines

Tony Rovira joins the board of LYN

DXB secures $107M licencing deal in Japan, phase 3 results this year.

Macro News - What we are reading & listening to 📰

Energy:

Eni fires up €100mn supercomputer in race to find oil and gas reservoirs (Financial Times)

- Eni's €100mn HPC6 supercomputer, 5th globally, aids oil discovery and clean energy research.

- Eni relies on proprietary supercomputing, unlike rivals using cloud services.

Uranium:

PDN ASX: Uranium is set for a multi-year bull market amid supply and demand constraints (AFR)

- Uranium prices hit 15-year highs as nuclear power gains global traction for AI, data centers, and decarbonisation goals.

- Supply constraints and geopolitical risks create a strong investment case, with ASX-listed uranium stocks showing upside potential.

Defence Metals:

DOD invests in mission-critical minerals (Metal Tech News)

- The U.S. heavily depends on China for critical minerals essential to its economy, military, and clean energy, raising significant national security concerns.

- China's dominance in mining and refining these materials, like rare earths and battery metals, allows it to leverage supply chains as geopolitical tools, highlighting the need for America to develop domestic mineral resources.

US Adds Tencent (700 HK) to Chinese Military Blacklist; Shares Decline (Bloomberg)

- The US blacklisted Tencent and CATL for alleged ties to the Chinese military, impacting the world’s largest gaming publisher and leading EV battery maker. Both companies denied the claims, and their stocks dropped sharply.

- The move heightens US-China tensions, with CATL's inclusion raising concerns over global EV supply chains, while Tencent protested its listing as a mistake.

The U.S. Military and NATO Face Serious Risks of Mineral Shortages (Carnegie Endowment)

- Critical minerals underpin military and industrial power, enabling platforms like tanks, munitions, and renewable energy technologies, while shortages can undermine defense readiness.

- Rising demand, export controls, and disrupted supply routes heighten risks for the U.S. and NATO, necessitating secure supply chains and strategic stockpiles.

Weaponization of the Periodic Table Crimps U.S. Critical Minerals Supply Chains (Exiger)

- China’s ban on antimony, gallium, and germanium exposes critical vulnerabilities in U.S. defense and industrial supply chains.

- Exiger identified over 75,000 parts and 800 weapon systems affected, offering unparalleled insights to mitigate supply chain risks.

The Blueprint for Winning the Race for Critical Minerals (TIME)

- U.S.-China rivalry intensifies over critical minerals for energy and tech.

- Historic strategies like reopening mines guide modern supply chain efforts.

Listen: Perpetua Resources CEO Jon Cherry Comments on Receiving the Final Record of Decision for Stibnite

Battery Metals:

Gates-Backed KoBold Metals Raises $537 Million in Funding Round (Bloomberg)

- KoBold Metals raised $537M, valuing it at $2.96B, for AI-driven mineral exploration.

- Funds target new projects, R&D, and Zambia's Mingomba copper mine.

Curtain falls on Jervois Global (ASX: JRV) as China floods cobalt market (The Australian)

- Jervois Global enters voluntary administration, with shareholders, including AustralianSuper, losing investments due to cobalt price collapse.

- Recapitalisation with Millstreet Capital reduces debt by $170M and funds Brazil refinery restart.

Climate Predictions for 2025: Electric Vehicles, Plastic Pollution and Solar (Bloomberg)

- Coal and nuclear are regaining importance due to surging power demands from AI and data centers.

- Trump’s policies could hinder the green transition, intensifying global warming risks.

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great rest of the week,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.