OJC enters Chinese Market with Aldi

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,810,715 OJC shares and the Company’s staff own 17,857 OJC shares at the time of publication. The Company has been engaged by OJC to share our commentary on the progress of our Investment in OJC over time.

New name, new chairman, new country, new deal.

Our small cap beverage manufacturing company has a new name and stock ticker:

The Original Juice Company (OJC)

The company was formerly known as The Food Revolution Group (ASX:FOD).

OJC has been working on a business turnaround since we Invested in early 2021.

Today, OJC announced that it had signed a deal with Aldi China to sell its juice products.

This is the first step on what we hope is a long and fruitful (get it) venture into the broader region.

OJC has been entirely focused on the smaller Australian market, selling its juice products in Coles and Woolworths.

But today marks the first foray into a bigger market, and bigger opportunity for the company.

Aldi has been in China since 2017, with 27 stores in Shanghai as of June 2022.

Aldi is looking to grow this number twenty-fold, with reports saying that Aldi is striving to install a further 500 to 600 stores in Shanghai by the end of 2022.

We think that Aldi is an excellent partner for OJC to get its foot into the Chinese market, as it is an established international brand looking to grow its footprint in the region.

The appetite for juice consumption is growing in China with the changing economics and demographics of the country.

As more people move into the middle class and become more health conscious they are likely to seek out products like juice - especially products with 100% Australian ingredients.

Australian products are generally viewed as high quality by Chinese consumers, and Australian juice should resonate with them given recent consumer trends.

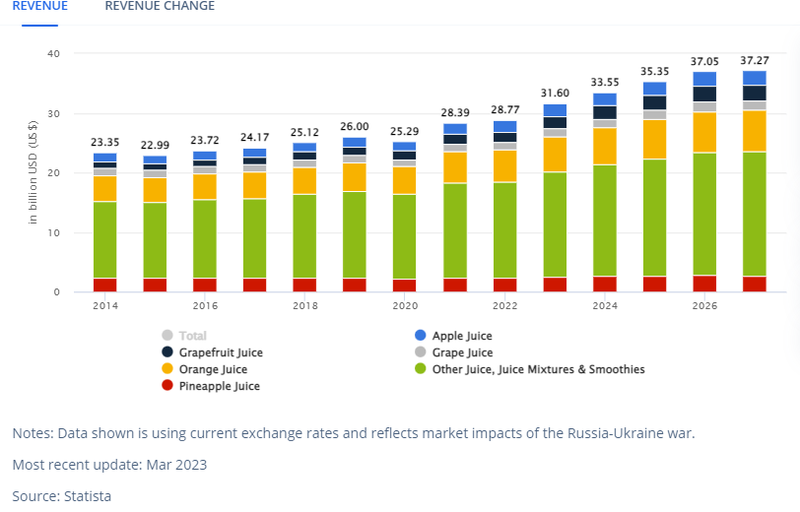

These trends are reflected in the growing revenue from juices sales in Asia, which are projected to grow ~4% year on year and could hit nearly 60% in total growth from 2014 through to 2027.

The ASX is familiar with China growth stories, companies like Treasury Wine Estates, Capilano Honey and A2 Milk each saw their share prices go exponential off the back of sales into China.

Entering a country where the population is 1.4 billion (almost 60x Australia’s population) can be game changing for a company, if the product resonates.

If OJC can capture just a small fraction of the juice market in China, it could mean millions of extra sales each year.

It is difficult to know which brands and products resonate with customers in a new market, but if OJC’s products take off in China, the upside potential is big.

However, if OJC’s products don’t gain traction in the region the company may be squeezed out by the competition.

It’s important to note that the Aldi China deal is initially small in terms of immediate revenue (two containers a month), but what it does provide is OJC a foothold into the region with an internationally recognised brand looking to grow its presence.

The juice will be sold under the private label “urban eaters” and include orange juice, apple juice and mixed green juice.

OJC currently makes its revenue by selling its popular juice based products into major supermarkets like Coles and Woolworths in Australia.

The company has been executing on its Fix → Reset → Grow strategy since we first Invested in Mach 2021.

There has been a lot of work done on the “Fix” and “Reset” stages, with former Victorial Premier Jeff Kennett coming on board as chairman earlier this year, and the company achieving multiple quarters of operating cash flow positive.

There have been some indications of “Growth” from OJC, with new product developments and year on year sales increase, however this deal with Aldi China marks the first step towards international expansion and is a big milestone for the company.

OJC originally flagged Chinese expansion before 2020 and it has been a long time coming for investors.

OJC has been following the Fix → Reset → Grow trajectory, ensuring that costs were down and cash flow sustainable before pursuing international growth.

It’s taken some time, but I think we think that the turnaround strategy is finally starting to bear fruit (okay we’ll stop).

This brings us to our “Big Bet” for OJC:

Our Big Bet

“OJC executes on a growth strategy (international export) that sees the company grow to $300M valuation and $100M+ annual revenue”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our OJC Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To visualise what OJC has done since we Invested, check out our Progress Tracker for OJC:

OJC secures $3.5M from NAB to finance growth

Yesterday, OJC announced $3.5M of debt financing from NAB to accelerate growth activities.

OJC is one of the only companies in our Portfolios that hasn’t raised capital by issuing new shares in the past two years, instead, it has utilised loans from top tier banks to secure financing.

The benefits of using debt to finance growth is that it is non-dilutive.

This means that the company can maintain a tighter register of shareholders, while relying on cash flows from the business to pay down the debt over time.

Unlike other pre-revenue small cap companies, OJC can pursue this strategy because it has a product to sell and cash coming through the door.

If OJC can successfully navigate paying down its debt, while growing to a size where it can take advantage of economies of scale, the decision to raise funds through non-dilutive means will make OJC’s shares more valuable in the future.

Four things stick out for us from OJC’s recent activities:

- OJC needs to scale to drive shareholder value

- To do that OJC must change market perceptions and prove it can scale

- The proof of that will be sustained top line revenue growth (while keeping costs down)

- And, at the same time, OJC needs to pursue blue sky opportunities for rapid growth through new distribution channels/export markets that were once off the table as it focussed on its financial foundations

As for OJC’s ability to scale, we conducted a site visit in April of last year to OJC’s facilities in Victoria and can confirm that the company’s site has significant space and capacity to scale its operation.

So with that knowledge in hand, we think it is a positive sign that OJC is delivering on its promised turnaround strategy as it moves towards a new growth phase.

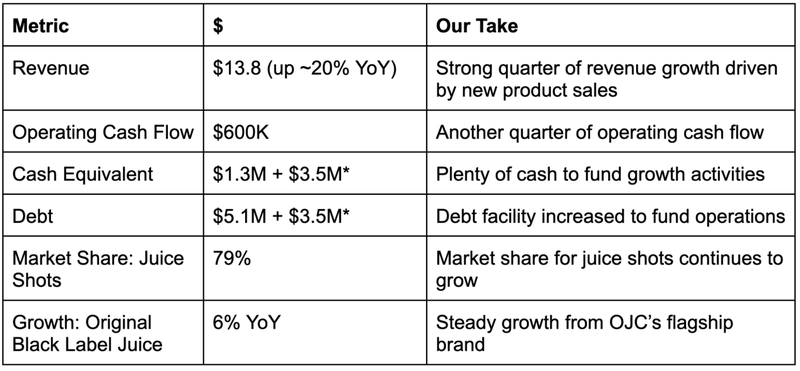

Speaking of growth, OJC announced in the recent quarter, $13.8M in revenue for the quarter which is almost a ~20% increase year on year.

This is further validation that OJC’s new products are resonating with customers, and the company’s sales strategy is working.

Accelerating growth comes with a cost (more inventory, labour, energy etc...) which is why the company has secured $3.5M in financing from NAB.

This money raised will help OJC scale faster and enter new distribution channels domestically and internationally - in particular delivering on the Aldi China deal announced today.

Although the Alid China deal is small to begin with, we think that OJC will grow its foothold in the region as Aldi grows its Chinese ambitions.

OJC has also executed distribution agreements with two other supermarkets, Evergrow and Happy Valley, to distribute its products in the Chinese and Malaysian markets.

This is the first major sign that the company is in its “growth” phase and rounds out a strong performance from the company on its first Investment Memo.

With this news, we will be reviewing our OJC investment memo and look to release a new memo in the coming months.

Who is Aldi China and what is the growth strategy?

Aldi is one of the major supermarket chains globally.

Aldi targets middle class consumers and is considered a ‘discount retailer’ utilising a low price strategy.

Aldi has been in China since 2017, with 27 stores in Shanghai as of June 2022.

Aldi is looking to grow this number twenty-fold, with reports saying that Aldi is striving to install a further 500 to 600 stores in Shanghai by the end of 2022.

CEO of Aldi China Roman Rasinger says that “China is and remains one of the most interesting markets in all areas and the rapidly increasing size of the middle class”. There are a lot of empty spaces on the map in China and Aldi wants to colour them blue (source).

We think that Aldi is an excellent partner for OJC to get its products into China, as it is an internationally recognised brand with an appetite to grow in the region.

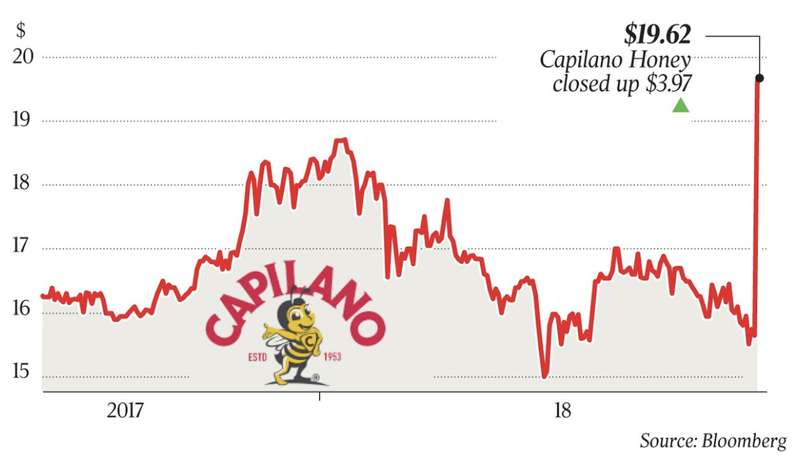

There are a number of small cap ASX listed companies that have found successful growth in China. A good comparison story is Capilano Honey, Australia’s biggest honey producer.

The company listed on the ASX in 2012 capped at $17.5M and sold for $190M in 2018 to a Chinese private investment firm.

During that time Capilano’s share price moved from ~$2 per share to ~$20 per share - a ~1,000% return.

Key to the company’s growth was the export sales in Asia, in particular China:

We think that if OJC’s products can resonate with Chinese consumers, like other Australian products in the region, sales growth for the company could be exponential.

Although it is important to note that Capilano’s past success is not an indicator of OJC’s future success in the region.

The ASX is however familiar with Australian consumer goods growth stories in China.

Companies like Treasury Wine Estates and A2 Milk both saw their share prices go exponential off the back of sales into China.

If a product resonates in a country where the population is almost 1.4 billion (60 times Australia’s population) it can be game changing for a company.

This is because the total addressable market of consumers (people who could buy the product) is much higher.

If OJC can capture just a small fraction of the juice market in China, it could mean millions in extra sales each year.

The key for OJC was finding a distribution partner that it could trust and grow with as it enters the region.

Ultimately, while the deal today with Aldi China won’t provide any immediate material revenue to OJC (only two containers a month), it is the first step into a market that could change the fortunes of the company significantly.

We are looking forward to what comes from today’s deal and hope to see OJC sign many more deals similar to this over the coming year.

A quick word on OJC’s Quarterly Performance

It was a big quarter for OJC with the company organising some key corporate activities including changing its name and ticker, undertaking a 4:1 share consolidation and introducing Jeff Kennett as Chairman.

From a growth perspective it was a strong quarter, with the company being cash flow positive and revenue up ~20% year on year.

Here were the headline growth numbers from OJC this quarter:

*Announced after quarter

New Chairman Jeff Kennett has been buying shares on market, a strong vote of confidence by the new chairman that he likes the valuation of the company at these prices.

The company also launched a new website, which you find here.

Overall another steady quarter of growth which validates the new product development strategy.

What could go wrong?

With OJC now taking on more debt, and working with tight margins the Debt Risk for the company has increased.

However, through the international expansion and distribution it has reduced its reliance on revenues from the Australian market and reduced Key Distribution Risk.

What is next for OJC?

🔄 Products resonate in Chinese market with first sales

With the Aldi China relationship now in full swing we would like to see some preliminary first sales, which hopefully indicate a strong demand for OJC’s products in the Chinese market.

⬜ Domestic distribution deal

With OJC firmly focused on growth we would like to see the company sign a deal to increase domestic distribution.

⬜ Institutional Investment

OJC has been in quiet execution mode for some time now, but with this international expansion deal announced we would like to see the company present to more investors and bring some institutional investment on to the register.

Our OJC Investment Memo:

Below is our OJC Investment Memo, where you can find a short, high level summary of our reasons for investing.

In our OJC Investment Memo, you’ll find:

- Key objectives we want to see OJC achieve

- Why we are Invested in OJC

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.