Now we are here…in Xanadu

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Speculate aims to target stocks that tend to fly under the radar, perhaps due to the fact that they don’t suit the risk averse investor or simply because they are small emerging potentially next big thing stories where the market moving news is yet to break. FinFeed will be looking to uncover such stocks on a weekly basis.

Xanadu Mines Ltd (ASX:XAM) has a highly prospective copper-gold project in an increasingly popular destination for companies seeking this type of mineralisation.

Xanadu’s near term focus is on expanding the resource at its Kharmagtai Copper-Gold Project located in the South Gobi region of Mongolia.

Kharmagtai was acquired from Rio Tinto in early 2014 by the Mongol Metals LLC joint venture in which Xanadu has now earned an 85% interest (for an effective interest of 76.5%) by funding exploration over the past few years.

Following the anticipated near-term resource expansion management will be undertaking a preliminary economic assessment with a view to developing an open pit mine.

Bell Potter analyst, Peter Arden, believes there is the prospect of a major resource upgrade in the December quarter of 2018.

However, the drilling results that will feed into the pending resource upgrade could provide share price momentum leading up to the October-December period.

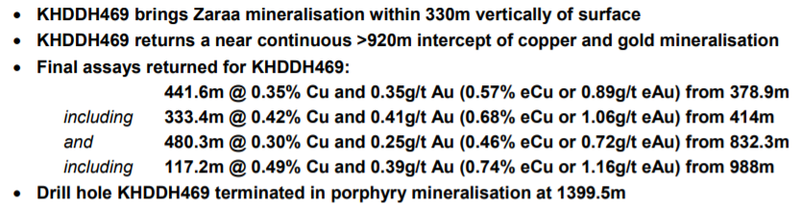

Commenting on recent exploration success at Zaraa, part of the broader project Kharmagtai project Arden said, “We have rolled forward our model and increased our valuation of Kharmagtai to reflect further recent drilling success at Zaraa, resulting in a 9% increase in our valuation of XAM’s mineral assets.

“Five recent drill holes have shown Zaraa contains nearly one kilometre of continuous copper-gold mineralisation in a down-dip extent that is located less than two kilometres to the south-east of the currently defined Resources.

“We continue to regard Kharmagtai as one of the world’s most attractive undeveloped copper-gold projects and it is favourably located in a mining-friendly jurisdiction.”

Of course Xanadu remains speculative and investors should seek professional financial advice if considering this stock for their portfolio.

Bell Potter values Xanadu at 52 cents per share, implying share price upside of more than 250% relative to its current trading range.

However, broker projections and price targets are only estimates and may not be met. Those considering this stock should seek independent financial advice.

Management targeting higher grade starter pit

The Kharmagtai Project contains gold-rich porphyry copper deposits for which the company released the Maiden JORC 2012 Resource in March 2015.

This came in at 203 million tonnes averaging 0.34% copper and 0.33 g/t gold for contained copper of 700,000 tonnes and 2.2 million ounces of gold with a higher grade core of 56 million tonnes averaging 0.47% copper and 0.59 g/t gold.

Infill and resource definition drilling has commenced at the site which should result in an upgraded resource.

Close spaced infill drilling will also allow Xanadu to refine the geological controls on mineralisation to later target down-dip and along strike mineralisation more effectively.

In discussing the upcoming drilling program Xanadu’s managing director Dr Andrew Stewart said, “Following the very significant discovery of the fourth porphyry centre at Zaraa, we believe the Kharmagtai project is approaching a near-term development opportunity and it’s now time to take the project to the next stage.

“Our number one objective at Kharmagtai is to fast-track resource drilling designed to significantly upgrade the Mineral Resource estimate and to complete a preliminary economic assessment (PEA) of a very low strip ratio, higher grade open pit ‘starter’ project contained within a larger resource.

“I am confident that Kharmagtai will further improve its status as the premier large-scale undeveloped copper-gold project in Asia”.

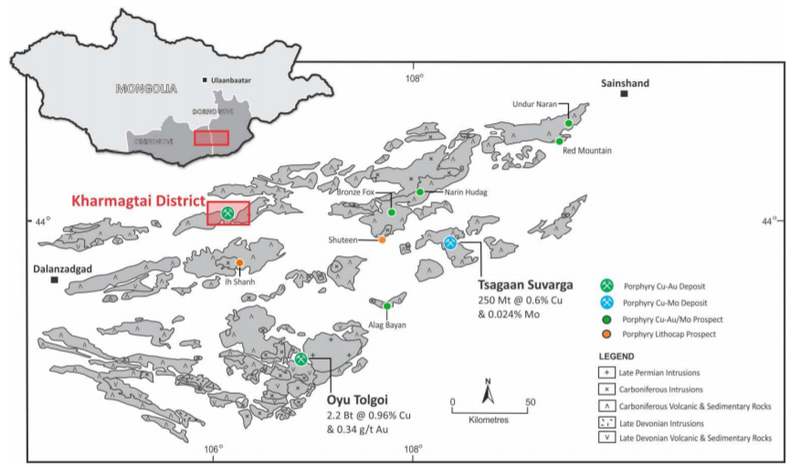

The area’s profile has been lifted by the success of the Oyu Tolgoi copper-gold project being undertaken by Rio Tinto (ASX:RIO) and its partners.

The project contains reserves and resources that make it one of the world’s largest known copper and gold deposits.

The following map demonstrates the highly prospective region being targeted by Xanadu with Oyu Tolgoi situated to the south-east.

Positive long-term trend points to a rebound

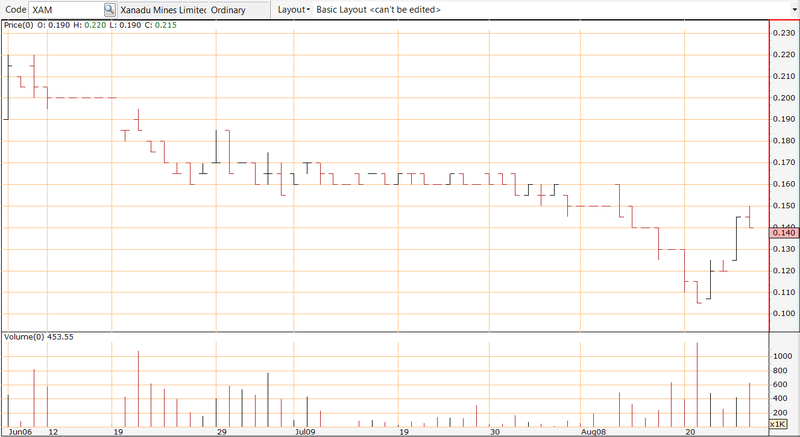

Xanadu’’s share price has been sold down heavily in 2018, and it is now trading well shy of its January levels of circa 30 cents.

However, newsflow has been positive, and it appears that the seemingly exaggerated extent of the decline could be attributed to the downturn in the gold price.

The steep fall in the gold price from circa US$1300 per ounce in mid-June to circa US$1170 per ounce in mid-August is clearly demonstrated in the first chart, while the correlation with Xanadu’s share price performance is obvious in the second.

However, I believe the most interesting chart in terms of assessing Xanadu’s long-term merits is the one below where we map the three-year performance of XAM (yellow line) against the S&P/ASX 200 Gold Index (XGD) which shows that it has generally outperformed the index.

This is an outstanding performance from a sub-$100 million market capitalisation stock, and it certainly suggests that the recent volatility is not only uncharacteristic of the stock, but it also defies long-term trends.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

The 50% decline in Xanadu’s share price from 22 cents to 11 cents was out of sync with the 10% decline in the gold price.

It would appear that investors have started to pick up on this disparity in the last week with the company’s shares recovering some of the exaggerated sell-off.

However, there still appears to be plenty of upside required to compensate for the sell-off, particularly given that the gold price has also rallied in the last week, rebounding to circa US$1200 per ounce.

Further, Bell Potter’s valuation suggests that there is significant share price upside.

Strong management team

While Xanadu can fairly be labelled a speculative play given its early-stage project status, the involvement of a highly experienced exploration team led by managing director, Dr Andrew Stewart, suggests there is a reasonable amount of well-founded confidence surrounding the project.

Stewart has been involved in the discovery and evaluation of numerous mineral deposits in various parts of the world including aspects of the discovery and evaluation of Oyu Tolgoi and other porphyry deposits.

His knowledge of both the unique regional styles of mineralisation, as well as the logistics of operating in this area will be invaluable.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.